Keathley Canyon 828 is not among the blocks listed for sale at BBG3. Per the Notice of Sale (p. 4), “any lease blocks whose high bids were rejected and not appealed in the immediately preceding Big Beautiful Gulf lease sale, are expected to be included as eligible for lease.” Can we therefore assume that either the KC 828 bid rejection or the prior lease expiration is being appealed?

The legislatively mandated BBG lease terms are attractive – 10 years and 12.5% royalty for deepwater blocks. A more recent legislative directive requires (wrongly in my opinion) the approval of downhole commingling requests. This accelerates the return on investments in deepwater, high pressure reservoirs. Such commingling has presumably contributed to record Gulf oil production in 2025. The longer term concern is the impact on ultimate oil and gas recovery.

Meanwhile, the Gulf rig count and well start numbers continue to disappoint. Baker Hughes (7/2/2026) lists only 4 active rigs in the deepwater Gulf – one each in the Alaminos and Mississippi Canyon areas and two in the Green Canyon Area. BSEE’s borehole file lists only 15 new deepwater exploratory well starts YTD.

“The Outer Continental Shelf presents a significant opportunity to support the future of America’s space economy. Offshore launch, re-entry, and recovery infrastructure could expand operational flexibility, increase capacity, reduce constraints on growing launch demand, and strengthen the nation’s commercial and national security space capabilities. With approximately 3.2 billion acres under federal jurisdiction, BOEM is uniquely positioned to help evaluate this emerging opportunity,” said Acting BOEM Director Matt Giacona. “This Request for Information is an important first step in assessing how offshore development could support the next era of U.S. space leadership.”

Rigs-to-Rockets is one of the alternative OCS uses promoted on this blog. Sea Launch was the first company to launch rockets from a converted semi-submersible drilling rig (photo above).

Kudos to BOEM for this initiative. Their Federal Register Notice is attached.

The Buckskin field (LLOG) is located in Keathley Canyon blocks 785, 828, 829, 830, 871, and 872 in 6,800 ft (2,073 m) of water. The KC 828 lease expired last year and LLOG’s bid for that block at the BBG2 sale was rejected.

BOEM’s Decision Information Matrix for Sale BBG2 is attached. As previously noted, 2 of the 25 high bids were rejected: Keathley Canyon Block 828 ($1,101,202) and Atwater Valley Block 63 ($650,018).

MROV=Mean of the Range-of-Value; LBCI=Lower Bound Confidence Interval

In the case of Keathley Canyon 828, BOEM’s valuation is more than 20 times the high bid. BOEM valued this block far higher than any other block in the sale.

KC 828 had been previously leased and that lease expired on 9/3/2025. The lease block was part of LLOG’s Buckskin field. Apparently, the lease expired due to inactivity given that the last well reached total depth more than a year prior to the expiration date. LLOG wanted the lease back. BOEM’s rejection sends a message that the price went up (by a lot 😉).

Finally, why didn’t any other company bid on KC 828, a block that has been publicly reported as being part of the Buckskin field?

Pointing to the potential financial implications for GE Vernova, Recharge News cites this serious fraud accusationby Vineyard Wind (VW):

“This exceptional misconduct includes [GE Vernova’s] intentional scheme to falsify critical quality assurance data… and to intentionally misrepresent the quality of those blades to [Vineyard Wind] in a brazen fraudulent, and willful breach of the TSA, ultimately resulting in the catastrophic blade failure…”

Recharge also discusses the findings of the Project Engineer appointed by VW to resolve claims between parties. Under the terms of the contract, the engineer’s determinations are binding unless overturned in arbitration.

The engineer determined that GE Vernova was liable for project delays, blade defects, vessel costs, and a $185m rescission of previously certified payments.

The damage claims issued by the project engineer total $853m.

On the basis of those determinations, VW withheld 100% of the outstanding invoices issued by GE Vernova. Even netted against sums allegedly owed to GE Vernova, VW says the turbine maker owes around $545m.

Per the contract, there are no limitations on liability in cases of “fraud, gross negligence, deliberate default or willful misconduct.”

My take: VW’s charges against GE Vernova will be resolved in the courts. However, VW is the lessee and operator, and is thus the party responsible to the Federal govt for project safety and environmental protection.

Operator responsibility is a fundamental tenet of the OCS regulatory program. As lessee/operator, VW bears ultimate responsibility for project safety and environmental protection.

VW is responsible for contractor selection, management, and oversight.

If a contractor violates a regulation, the violation notice is given to the operator. If a contractor causes pollution, the operator is responsible for the cleanup.

DNV, the Certified Verification Agent (CVA) hired by VW, was required to verify the design, fabrication, and installation procedures. Did they raise any issues to VW and the regulators?

Did the division of responsibilities between BOEM and BSEE weaken regulatory oversight? BOEM, ostensibly just the leasing bureau, should not have been authorized to grant departures that could affect structural integrity and operational safety.

It’s surprising that VW has not been cited for civil penalties resulting from the blade failure and the resulting environmental damage.

How can a judge prevent a contractor from stopping work for an operator that has filed serious fraud allegations against the contractor, has stopped making payments, and has, along with the Governor, declared the project to be complete?

BOEM Press Release: “The Bureau of Ocean Energy Management announced today the critical role of offshore leasing, resource assessment and long-term planning in supporting record oil production on the U.S. Outer Continental Shelf, which reached more than 714 million barrels in 2025.”

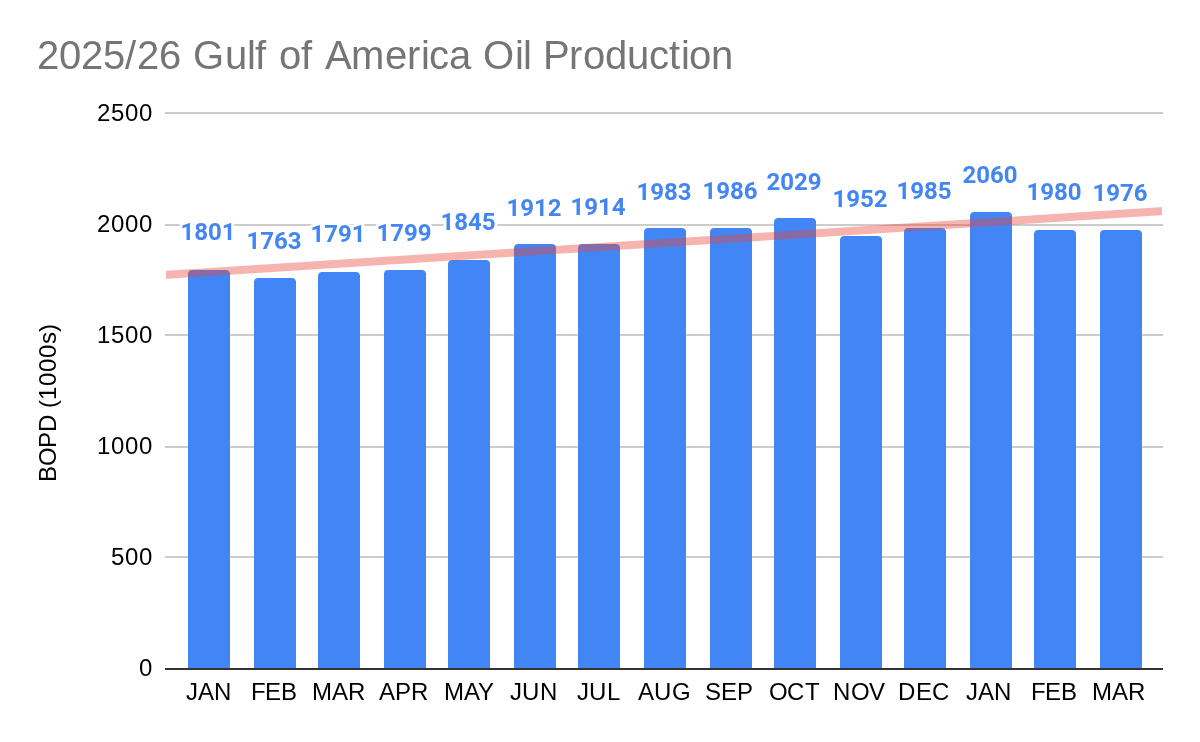

Was 2025 a record OCS oil production year?No, 2025 came very close, but barring belated revisions, 2019 retains the record.

Did 2025 oil production exceed 714 million barrels? Not even close according to the US Energy Information Administration (EIA), which reported a final OCS production total of 692.6 million barrels for 2025. The Office of Natural Resources Revenue (ONRR), to whom all production data must be reported, has yet to post their final 2025 numbers, but they are normally very close to the EIA totals. Also, ONRR’s fiscal year totals do not suggest calendar year production in excess of 700 million barrels. BOEM’s announced 714 million barrel CY 2025 total is more than 60,000 bopd higher than the actual EIA CY or ONRR FY daily averages, and even exceeds the total posted in BOEM’s data center.

See the 2019 and 2025 oil production totals in the table below. The BOEM 2025 numbers appear to be erroneous.

On the plus side, per EIA’s latest update, Jan. 2026 was a record production month for the Gulf. January’s ave. production of 2.060 million bopd surpassed the Aug. 2019 ave. of 2.044 million bopd.

Barring significant tropical storm shut-ins over the next 6 months (hurricane season starts today!), a production record in 2026 seems like a good possibility.

Although BOEM’s decision matrix has not yet been posted, a comparison of the acceptances with the bids submitted tells us that the Keathley Canyon Block 828 ($1,101,202) and Atwater Valley Block 63 ($650,018) bids were rejected.

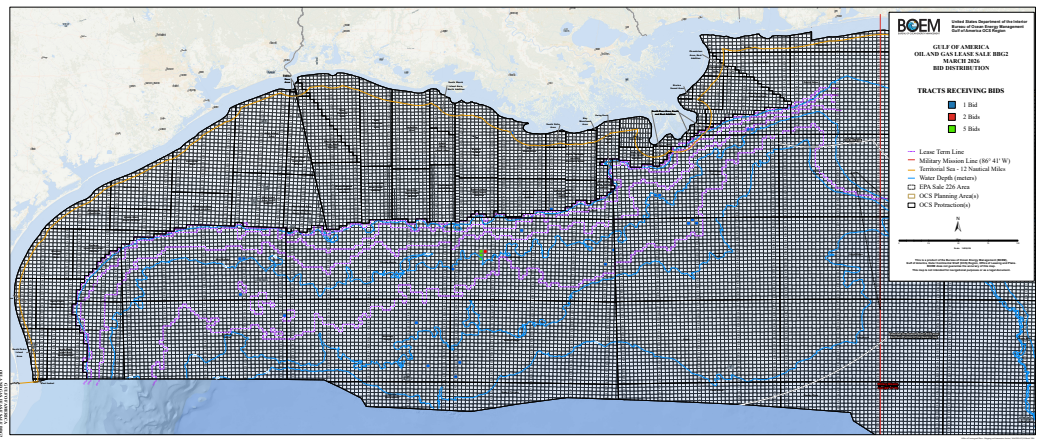

Both of the rejected bids were submitted by LLOG, partnering with 4 other companies on the Atwater Valley block. LLOG’s high bids on 3 other blocks were accepted, so their rejection rate was 40%. Interestingly, 2 of the 3 BBG1 rejected bids were also submitted by LLOG.

There is no shame in bid rejections, which are part of the legislated leasing process. Why pay more than you have to (or think a block is worth)? A bid rejection may attract future competition, but otherwise the only downside is that you don’t get a lease that you can possibly acquire at another sale if desired (an advantage of regular, predictable lease sales).

BOEM is charged with making fair market value determinations and their process and decisions are publicly available. Of course, opinions differ on the value of an unexplored lease. We will see what the bidding on the BBG1 and BBG2 rejections looks like in future sales.

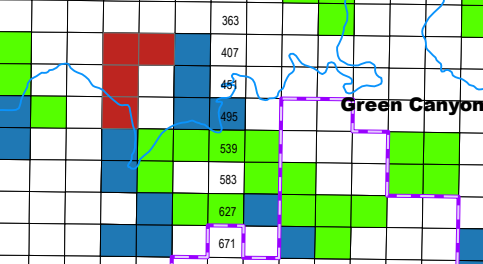

BOEM did accept the the high bids for the BBG2 “sweet spot” blocks (red in map below; also see the table) in the Green Canyon Area of the Gulf. These 4 blocks accounted for 17 of the sale’s 38 bids (45%) and $32.8 milion of the sale’s $47 million in high bids (70%). BP’s $21 million bid for GC 404 was by far the sale’s highest bid.

red=blocks receiving bids at BBG2; blue=BBG1 and Sale 261 leases; green=active leases issued prior to Sale 261

The CBD had challenged an April 2025 BOEM decision concludingthat Sable was not required to revise its development and production plan for the SYU. They sought a court order requiring a revised plan. This suit seemed to be a stretch, so its dismissal is not a surprise.

Per the Dept. of Justice, the court dismissed the lawsuit because the plaintiffs’ asserted procedural injury had no basis in the statute, was not traceable to any action by BOEM, and could not be redressed by an order of the court.(Other than that, it was just fine. 😉)

Among other problems the court identified with the plaintiffs’ case, they invoked a provision of the statute that governs “approval of a development and production plan,” not revision of an already-existing plan. It will be interesting to see the full decision so that we can better understand the context for that statement. Distinguishing revised plans in that manner could have significant policy implications.

For a full update on Sable litigation, see the section of their Quarterly Report beginning on p. 12.

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectivelychallenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

BSEE (2020) estimates the cost of decommissioning these facilities to be $85 million (too low), and there is no collateral or third party guarantee.

The responsibility for decommissioning these platforms has yet to be settled. ConocoPhillips, Oxy, and Devon have appealed decommissioning orders from BSEE. The Interior Board of Land Appeals (IBLA) has yet to rule on those appeals. The appellants are funding some plugging operations and facility upgrades pending the IBLA decision.

Per BSEE’s borehole file, this is the current status of the Hogan and Houchin wells:

33 completed and not yet plugged; these wells were drilled between 1968 and 2010

43 temporarily abandoned (TA) wells plugged in accordance with 30 CFR § 250.1721

10 wells have been updated to TA status in the past 6 months (latest 3/22/2026), so some progress is being made

If you are interested in the Hogan/Houchin mess or decommissioning liability in general, I highly recommend that you look at Devon’s informative and rather compelling appeal to IBLA. Similar appeals were submitted by Oxy and ConocoPhillips.

Lease history (excerpted from the Devon appeal):

Lease OCS-P 0166 was issued effective January 1, 1967.

Phillips Petroleum Company (“Phillips”) (predecessor to ConocoPhillips), Cities Service Oil Company (predecessor to Oxy), and Continental Oil Company (predecessor to ConocoPhillips) were the initial lessees

Phillips was designated operator on January 25, 1967

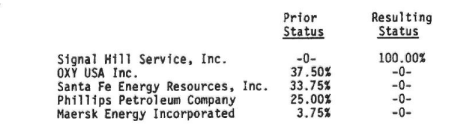

February 28, 1983: Petro-Lewis Funds, Inc., obtained the 37.5% interest of the Continental Oil Company (which in 1979 had changed its name to Conoco Inc., now Conoco Phillips Company (“ConocoPhilips”)).

November 1983: Cities Service Oil Company assigned its 37.5% interest to Cities Service Oil and Gas Corporation (now OXY U.S.A. Inc).

July 2, 1987: the Minerals Management Service (“MMS”) approved two more assignments of the Lease. One, from PetroLewis Funds, Inc. to American Royalty Producing Company (“American Royalty”), was approved retroactively to December 31, 1984. The other, from American Royalty to Santa Fe Energy Company(“Santa Fe”), was approved retroactively to April 30, 1987.

April 1, 1988: Santa Fe transferred a 3.75% interest to Maersk Energy Incorporated, reducing Santa Fe’s share to 33.75%.

1991 Assignment to Signal Hill: MMS approved assignment of the lease to Signal Hill effective February 5, 1991. The assignment was approved without any provision under which the assignors agreed to be liable for decommissioning operations on the lease. MMS’s approval actually had the opposite effect, leaving such obligations to the assignee. The assignment was approved despite concerns within the MMS about the financial strength of Signal Hill and the technical competence of Pacific Operators Offshore Inc (POOI), the affiliate that would operate the facilities.

Comments:

The assignment to Signal Hill should have never been approved. The outcome was predictable.

The Devon, Oxy, and ConocoPhillips appeals are very strong and would seem to have a good chance of success. Perhaps that is why the IBLA decision is taking so long (nearly 5 years to date).

Given the uncertainty regarding this appeal, the absence of transparency about other potential decommissioning liabilities, and the uncertainties regarding the administration of predecessor liability, this is not the time to be relaxing financial assurance requirements and further exposing taxpayers to decommissioning risks.

This is the final day to comment on BOEM’s proposal:

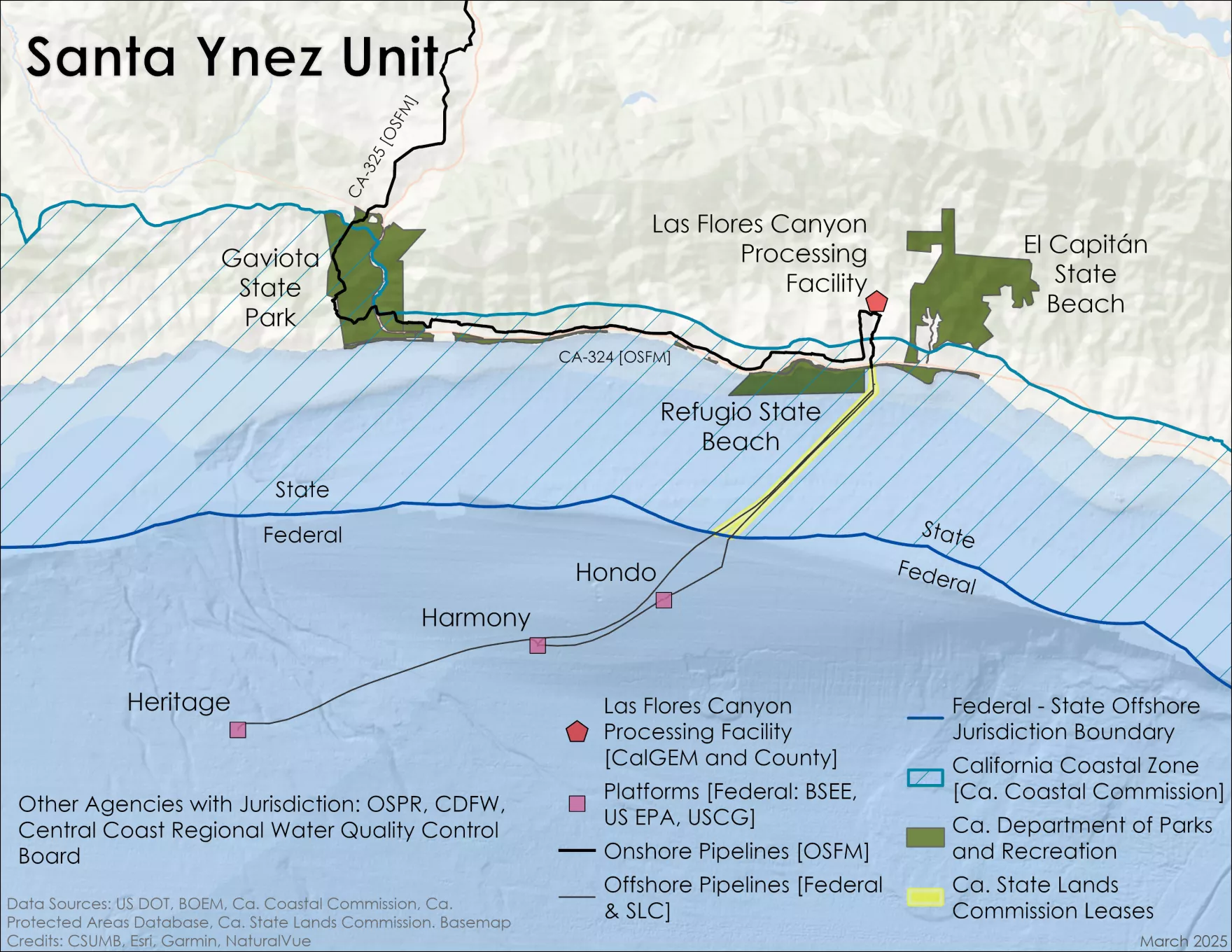

At a minimum, the fire will further delay and increase the cost of well plugging operations on Platform Habitat. Per BSEE’s borehole file, 17 wells remain to be permanently abandoned, 3 of which have yet to be temporarily abandoned. These wells are 23-44 years old, and have been inactive for 11 years.

If there is significant platform damage, the remediation delays and costs would be substantial, comparable to those associated with major Gulf platforms damaged by hurricanes. Structural damage could increase the urgency of removing the platform. Given California’s decommissioning quagmire, this would be a major challenge.

Who pays, and what does the financial assurance picture look like? Per the attached BOEM spreadsheet (excerpt pasted below):

The 2020 cost estimate for decommissioning Habitat was $44.3 million. That number is optimistic even if platform damage is minimal.

$13.6 million in supplemental assurance has been provided.

A third party guarantee has been secured.

The guarantee was provided by Freeport-McMoRan Oil & Gas (FMOG)

Per BOEM, FMOG is the guarantor for all DCOR leases. Unless BOEM has allowed otherwise, the guarantor pays all costs not covered by the lessees. Given the number of old platforms and California decommissioning challenges, the risks for FMOG are indeed large.

Although DCOR LLC is the current Habitat operator, the company owns only a 4.18% share of the project. CHANNEL ISLANDS CAPITAL, L.L.C., a private company about which little is known, holds a 95.82% share.

Should the 2 owners default, BOEM/MMA will look to the guarantor and predecessor lessees (see the chart below). Unfortunately for FMOG, they are both the guarantor and the predecessor lessee. FMOG acquired Plains Exploration & Production (PXP), the operator prior to DCOR. Nuevo Energy was acquired by PXP and thus also tracks back to FMOC. (This may explain FMOC’s decision to be a guarantor!).

Should FMOC fail to fulfill their obligation. Chevron would likely be the next target. The original Harvest partners were Texaco (operator) and Union Oil, both of which were acquired by Chevron.

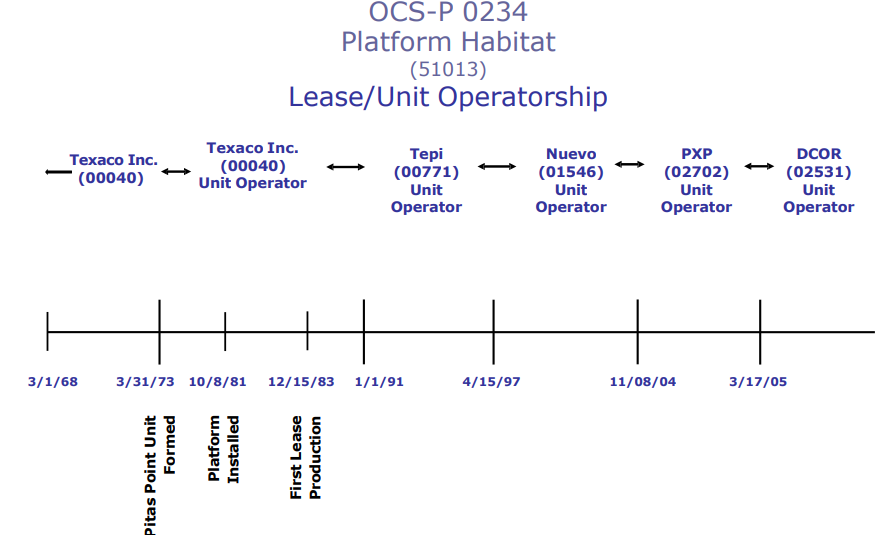

TEPI=Texaco Expl. & Production. Nuevo Energy was acquired by Plains Expl.&Production (PXP), which was acquired by Freeport McMoRan Oil & Gas (FMOG)

Restart seems likely for decommissioning financial assurance rule

Posted in Regulation, decommissioning, energy policy, tagged API, BOEM, Chevron, comments, decommissioning, financial assurance, NEFSA, proposed regulation, Shell on May 18, 2026| Leave a Comment »

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectively challenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

Lastly, kudos to the New England Fisherman’s Stewardship Association for raising the concern about financial assurance for decommissioning offshore wind facilities

Read Full Post »