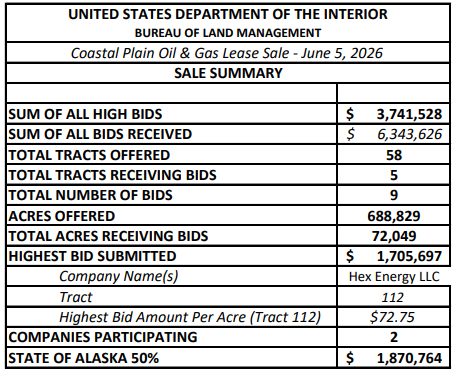

Yesterday’s mandated One Big Beautiful Bill sale in the Arctic National Wildlife Refuge turned out to be a one-on-one competition between an Alaskan independent and a State agency! Only 5 of the 58 tracts received bids, and the high bid was $1.7 million.

The competitors:

- HEX Energy, an Alaskan independent: 4 bids, 2 high bids

- Alaska Industrial Development and Export Authority (AIDEA), the state government’s economic development agency: 5 bids, 1 high bid

The implications for Arctic offshore sales are not good, but oil companies can be fickle, and opinions and investment strategies are subject to change, especially in the Arctic.