Tyler Priest, the leading historian on US offshore oil and gas operations, has informed me that his much anticipated book, “Offshore Oildom,”is now available for order from LSU Press.Tyler’s book is a fascinating account of the history of the technologically innovative and economically important, yet controversial, OCS Oil and Gas program. See the attached flyer.

Consider this recommendation by Daniel Yergin:

“Tyler Priest, a preeminent historian of energy and the environment, explores how a single well drilled off a pier near Santa Barbara in 1898 gave rise to a major American industry—offshore oil and gas. In spirited prose, Priest demonstrates how this U.S. industry was created not only by innovation, creative engineering, and complex execution; it was also the result of fierce political battles.” ~Daniel Yergin, Pulitzer Prize–winning author of The Prize: The Epic Quest for Oil, Money, and Power and The New Map: Energy, Climate, and the Clash of Nations.

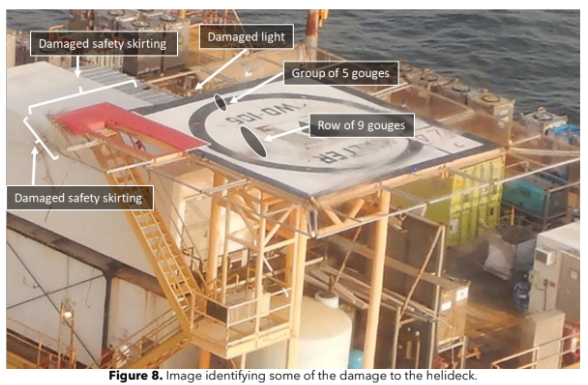

The NTSB has finally issued their report (attached) on the 12/29/2022 helicopter crash that resulted in 4 fatalities at Walter’s West Delta 106 A platform. The NTSB report on the Huntington Beach pipeline spill took a comparable amount of time (26 months) to complete. By comparison, the lengthy and complex National Commission, BOEMRE, Chief Counsel, and NAE reports on the Macondo blowout were published 6 to to 17 months after the well was shut-in.

The gist of the NTSB’s findings is pasted below.

The report summarizes operations standards, but does not consider the associated operator/contractor safety management systems that are intended to prevent such incidents. The report notes that:

Was the contractor/operator aware of these deviations from company policy? Should they have been?

The report implies that human (pilot) error was the cause of the dynamic rollover, but fails to assess the organizational controls that are intended to prevent such errors. How was a pilot with 1667.8 flight hours (1343.8 as the PIC), who had made 23 trips to this platform, repeatedly making fundamental positioning and takeoff errors?

The report also notes that:

This is interesting wording given that the perimeter light was identified as the pivot point, one of the 3 requirements for a dynamic rollover. Why wasn’t that violation observed by the operator/contractor and corrected? What helideck inspection procedures were in place? Did NTSB consider the fragmented regulatory regime for helicopter safety, particularly with regard to helidecks?

estimated peak production:100,000 barrels of oil equivalent per day (boe/d)

water depth – 8600 ft

200 miles south of Houston

estimated recoverable resource: 480 million boe.

first oil only 7.5 years after discovery (includes COVID delay)

Vito clone: replicates 99% of the hull design and 80% of the topsides from Vito.

high efficiency gas turbines and compression systems

~ 30% lower greenhouse gas (GHG) intensity over its life cycle than the already efficient levels being achieved at Vito. (Why the push to run electric cables from shore to North Sea platforms with ample gas production?)

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded in this post.)

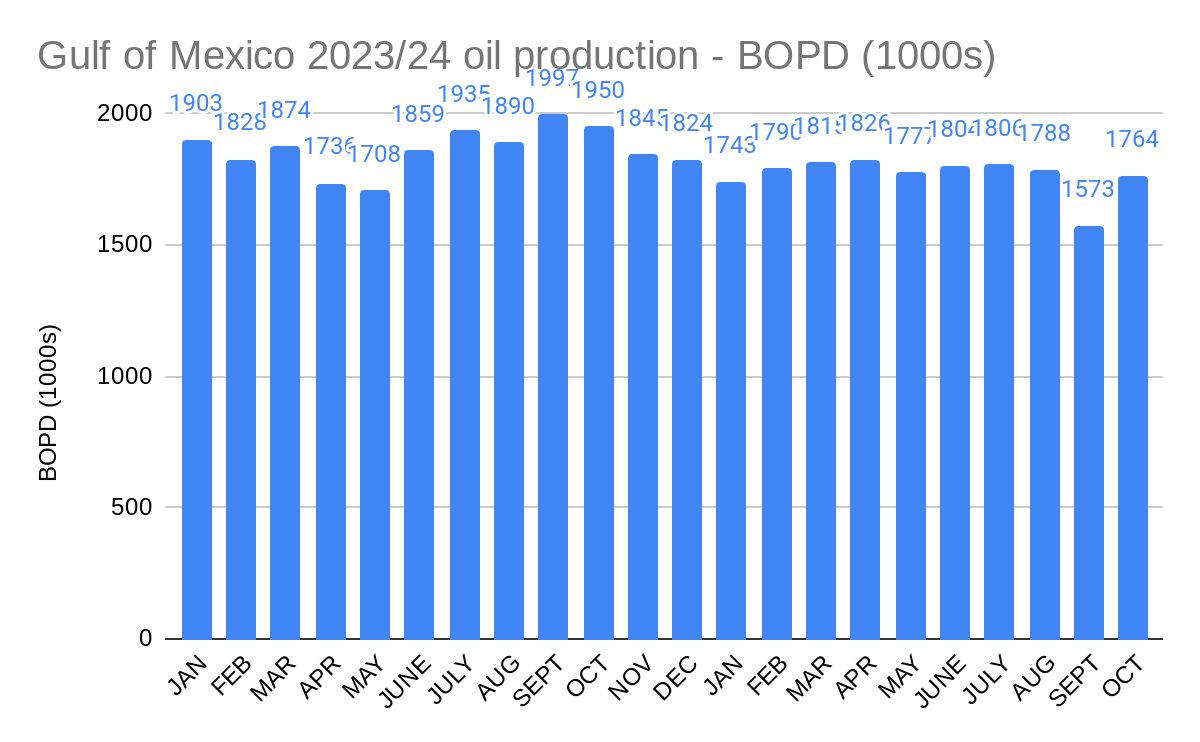

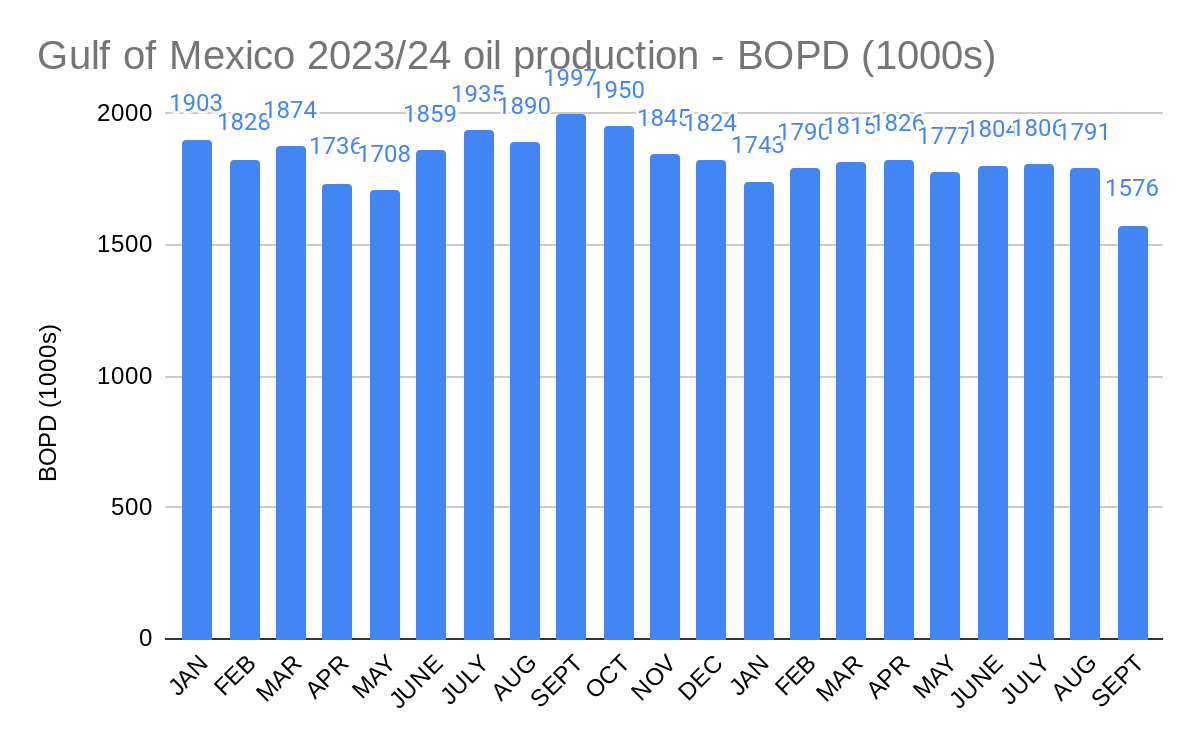

Following the 200,000 bopd decline in Sept. because of Tropical Storms Francine and Helene, Oct. GoM oil production was once again in the normal range for 2024. With the exception of Sept., average 2024 production has been remarkably consistent from month to month.

“At the heart of the dispute are rules from the federal Bureau of Ocean Energy Management – BOEM – which require energy producers in the Outer Continental Shelf to provide a bond to pay for well, platform, pipeline and facilities cleanup if the operating company fails to do so.”

“These insurance companies and their unreasonable demands for increased collateral pose an existential threat to independent operators like W&T.”

Comment: If insuring offshore decommissioning is so risk-free and lucrative, why aren’t other companies entering the market?

“Several states, including Texas, are challenging the BOEM rule and in one case they specifically cite W&T as an example of how the rule could be misused to irreparably harm energy producers.“

Comment:As previously posted, the concerned States should propose alternative solutions that would promote production while also protecting taxpayer interests. Arguing that decommissioning financial risks are not a problem is neither accurate nor a solution.

“In over 70 years of producer operations in the Gulf of Mexico, the federal government has never been forced to pay for any abandonment cleanup operations associated with well, platform facility, or pipeline operations.”

Comment: Shamefully, from the standpoints of both the offshore industry and the Federal government, that statement is no longer true. The taxpayer has now funded decommissioning operations in the Matagorda Island Area offshore Texas (BSEE photo below) and more significant decommissioning liabilities loom.

Northern Endurance Partnership (bp, Equinor, and Total) has been awarded the UK’s first permit to “store” CO2 beneath the North Sea.NEP plans to begin construction in the middle of 2025 with start-up expected in 2028 (bet the over!). Climate solution or costly virtue signaling at the public’s expense?

Fortunately, from the standpoint of US consumers and taxpayers, the push for carbon disposal in the Federal waters of the Gulf of Mexico has stalled, perhaps permanently. Oct.1 marked the 2 year anniversary of the 94 leases improperly acquired by Exxon at Sale 257 for carbon disposal purposes. Those leases will expire in 33 months (with the remaining 105 rogue leases expiring 1-2 years later) barring another legislative maneuver by industry advocates.

All of the previously posted questions about carbon disposal in the Gulf of Mexico remain, and most apply elsewhere. In particular, detailed cost-benefit analyses and risk assessments for these projects have not been provided. The intended permanency of offshore, subsurface carbon disposal raises complex monitoring, maintenance, liability, and decommissioning issues.

What are the carbon disposal proponents selling and why should governments be buying? If CO2 emissions are a significant threat to society (and informed opinions differ), is carbon disposal a cost effective solution?Policy decisions on subsidies for carbon disposal will be a good indication of how serious the new administration is about cutting Federal spending.

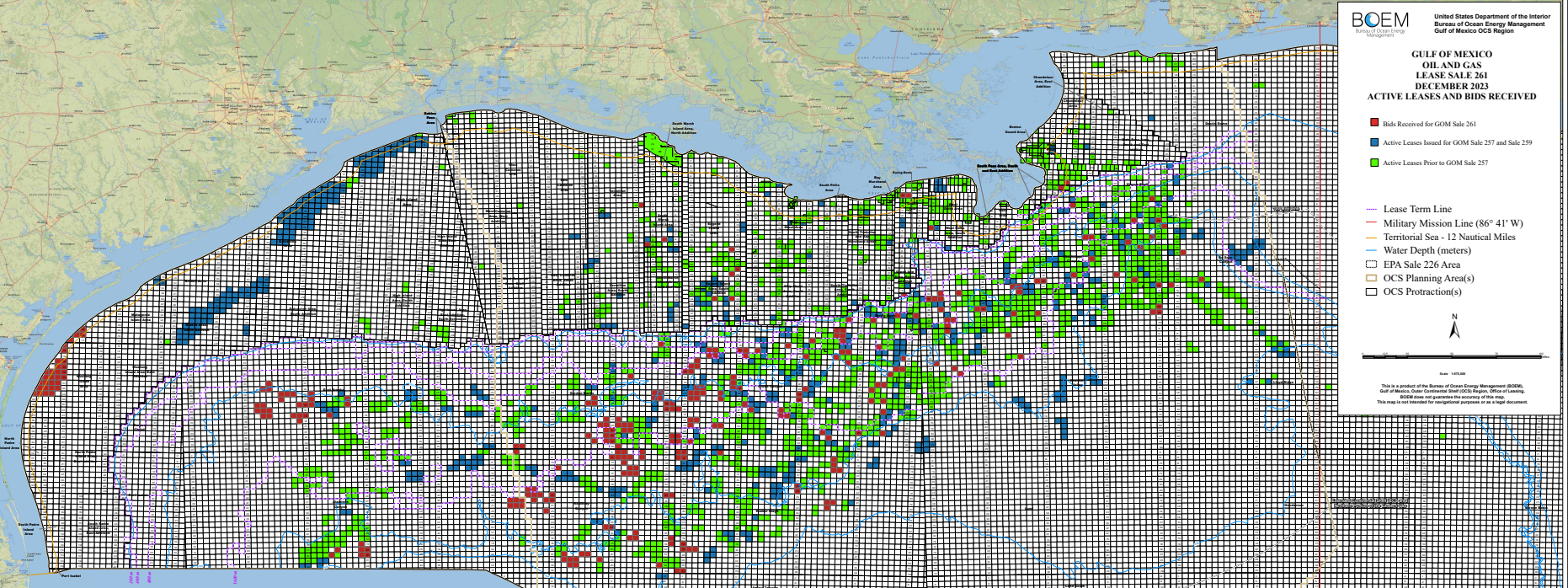

199 GoM oil and gas leases were wrongfully acquired for carbon disposal purposes. At Sale 261, Repsol acquired 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon had acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

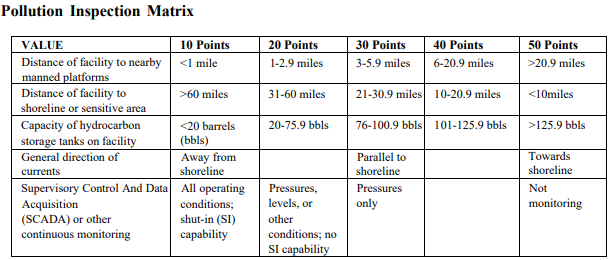

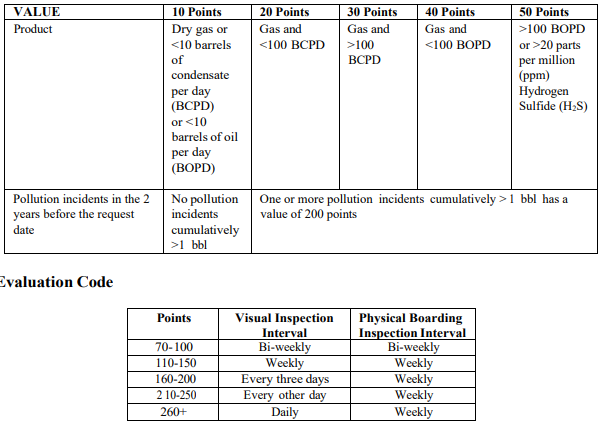

The attached BSEE document provides guidance for determining pollution inspection frequencies for unmanned facilities. Thoughts:

Reasonable risk-based approach

A minimum of bi-weekly visual and physical inspections for low risk platforms producing dry gas

Any platform with significant oil production and storage, and no real time monitoring system, will have to be visually inspected at least every 3 days (daily if other risk factors apply) and boarded weekly

Any platform that had spillage totaling > 1 bbl in the past 2 years will have to be visually inspected every other day and boarded weekly.

Provides for the application of technology (cameras, drones, innovative monitoring systems) to reduce inspection frequencies.

As expected, the Gulf of Mexico’s remarkable 7 month production consistency streak ended in September as a result of shut-ins associated with Tropical Storms Francine and Helene. Nonetheless, average daily production still amounted to 88% of the ~1.8 million bopd average that had been achieved for the previous 7 months. Rather impressive resiliency!

The Secretary of the Interior is the most important energy production position in the US govt, particularly for the offshore sector.

In recent years energy policy has been increasingly influenced (if not directed) by White House staff, most notably the White House Climate Office. Given that Burgum will also lead the new created National Energy Council, direction from White House staffers or other departments should not be an issue.

Burgum should work effectively with Dept. of Energy appointee Chris Wright, an engineer who understands energy production.

There is no apparent Republican dissent, so Burgum should have no problem being confirmed.

All of the offshore policy forecasts in the post-election post still stand.

Burgum is currently the Governor of North Dakota. Some energy production stats for the state:

ND ranks 4th if the OCS, for which Bergum will soon be responsible, is included. The OCS ranked 2nd in oil production, behind only TX, despite seemingly being managed to fail.

Wind: In 2023, wind was the second-largest electricity generating source in ND behind coal. At the beginning of 2024, ND had about 4,000 megawatts of installed wind power generating capacity.

What about carbon sequestration (disposal)?

As Governor, Burgum supported CCS projects that could be lucrative for North Dakota.

As Interior Secretary and Energy Czar, he will have to consider the high Federal subsidy costs, efficacy, and net environmental benefits.

Companies looking to benefit from publicly financed CCS projects will lobby hard for Federal support. Budget hawks and most environmental activists will be strongly opposed. It will be interesting to see who prevails.