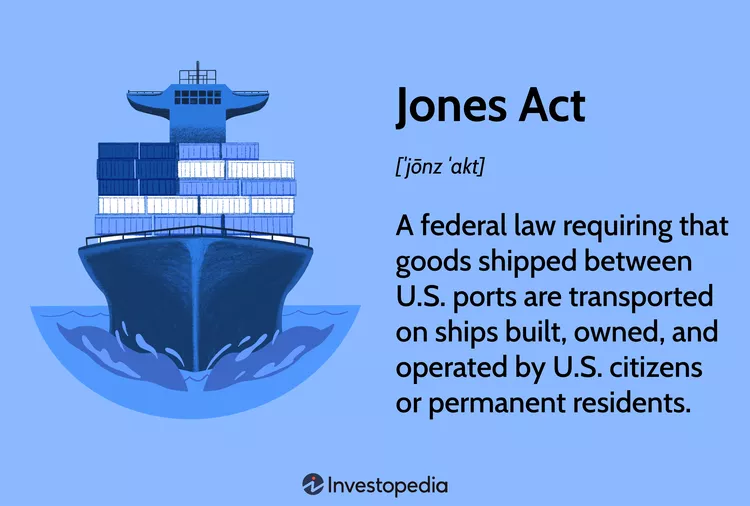

Sen. Mike Lee has introduced legislation to repeal the Jones Act, which is drawing additional scrutiny for the increased cost of transporting US oil production and LNG to US ports.

Because facilities on the Outer Continental Shelf are US ports under the Jones Act, the Act has been problematic for both the offshore oil and wind industries. The attached Customs and Border Patrol document delves into the nuances of Jones Act compliance for lifting operations (p.14-15) and “points” on the OCS (p.17).

EXAMPLE: CBP interprets the OCSLA to extend the Jones Act to artificial islands and similar structures, as well as to mobile oil drilling rigs, drilling platforms, and other devices attached to the seabed of the OCS for the purpose of resource extraction and/or exploration operations. Such objects located on the OCS are considered points or places in the United States for purposes of the Jones Act. Similarly, floating warehouse vessels, when anchored on the OCS to supply drilling rigs on the OCS, are also coastwise points.

Check out this complex CBP ruling on the transportation of well fluids from one location in a subsea well cluster to another. See if you understand and agree with their conclusion (below).

The transportation of fluids as described in the FACTS section above, by a dynamically-positioned, foreign-flagged drill ship between wells located within an IF (integrated facility), which subsequently, transships the fluids to a coastwise qualified barge for transportation to a coastwise point, violates 46 U.S.C. § 55102.

On a related matter, it’s still unclear to me whether the attachment of the lower marine riser package to a subsea wellhead makes a floating, dynamically positioned drillship a US port under the Jones Act.