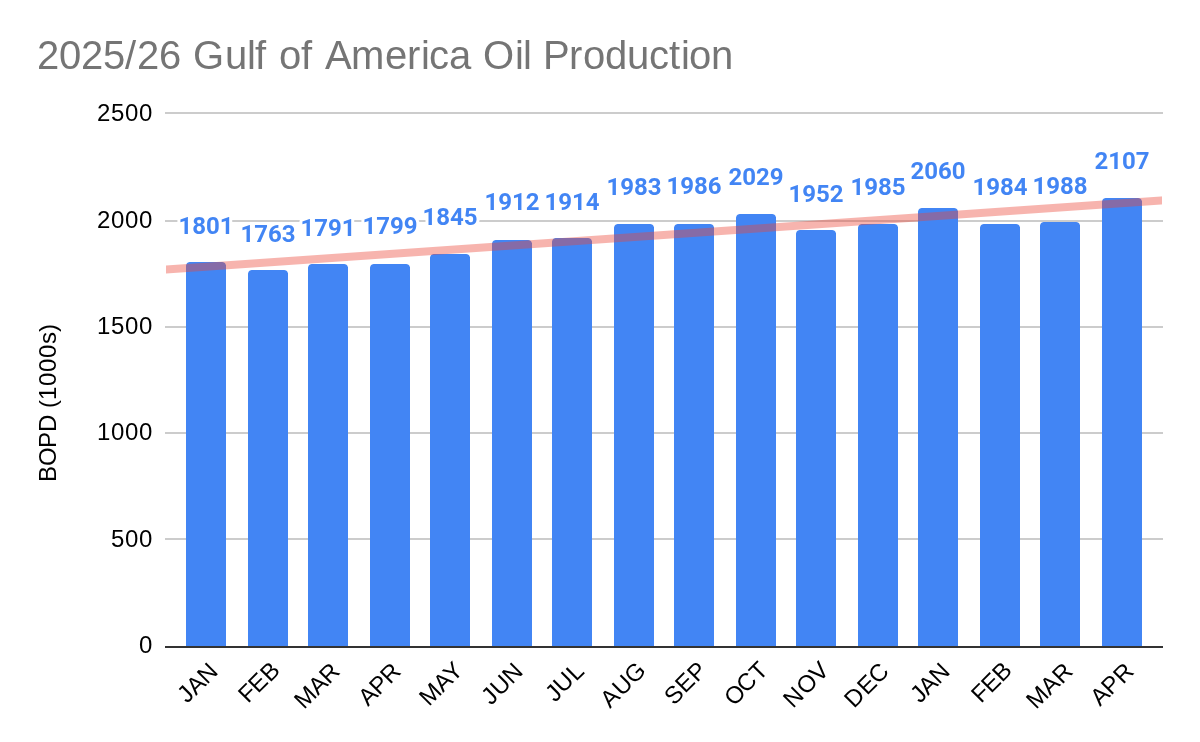

Per the preliminary EIA data for April, Gulf of America OCS facilities produced an average of 2.107 million bopd in April. This surpasses the previous record of 2.060 million bopd set in January.

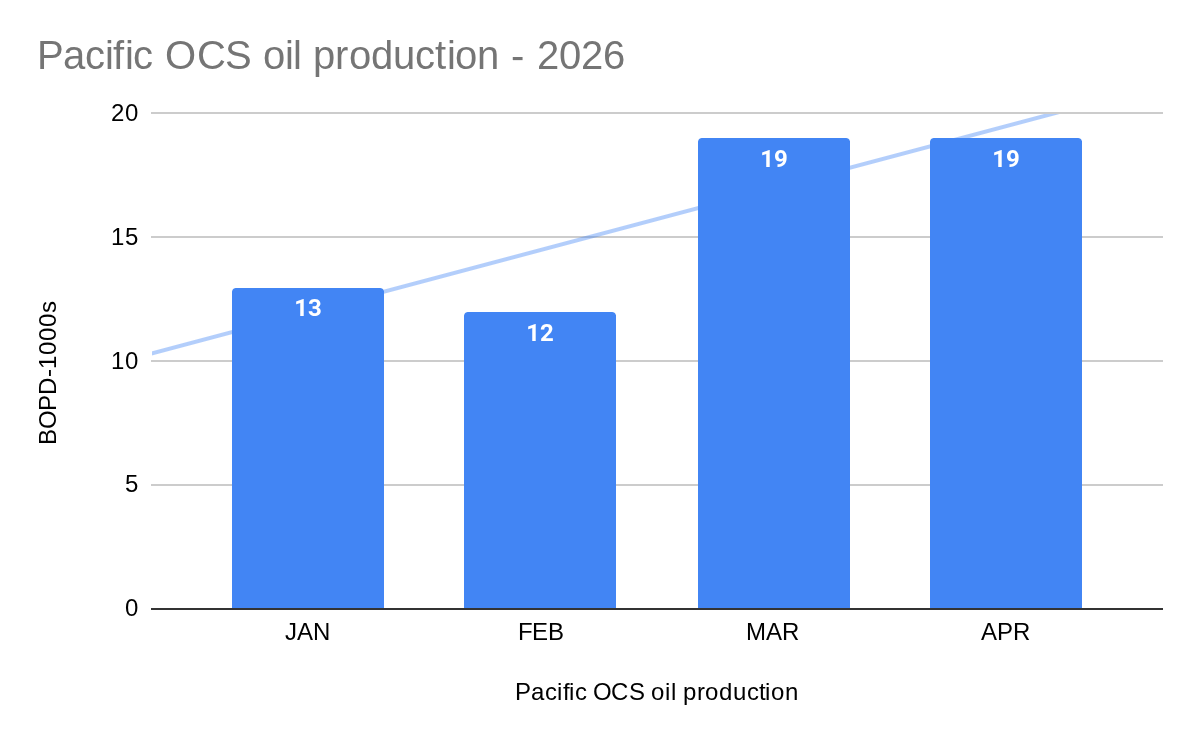

Meanwhile, the Sable bump is now evident in the EIA’s Pacific OCS production data with a ~50% March-April increase from January-February. A bigger increase should be apparent when the May numbers are posted. How will Sable fare in the upcoming court battles?

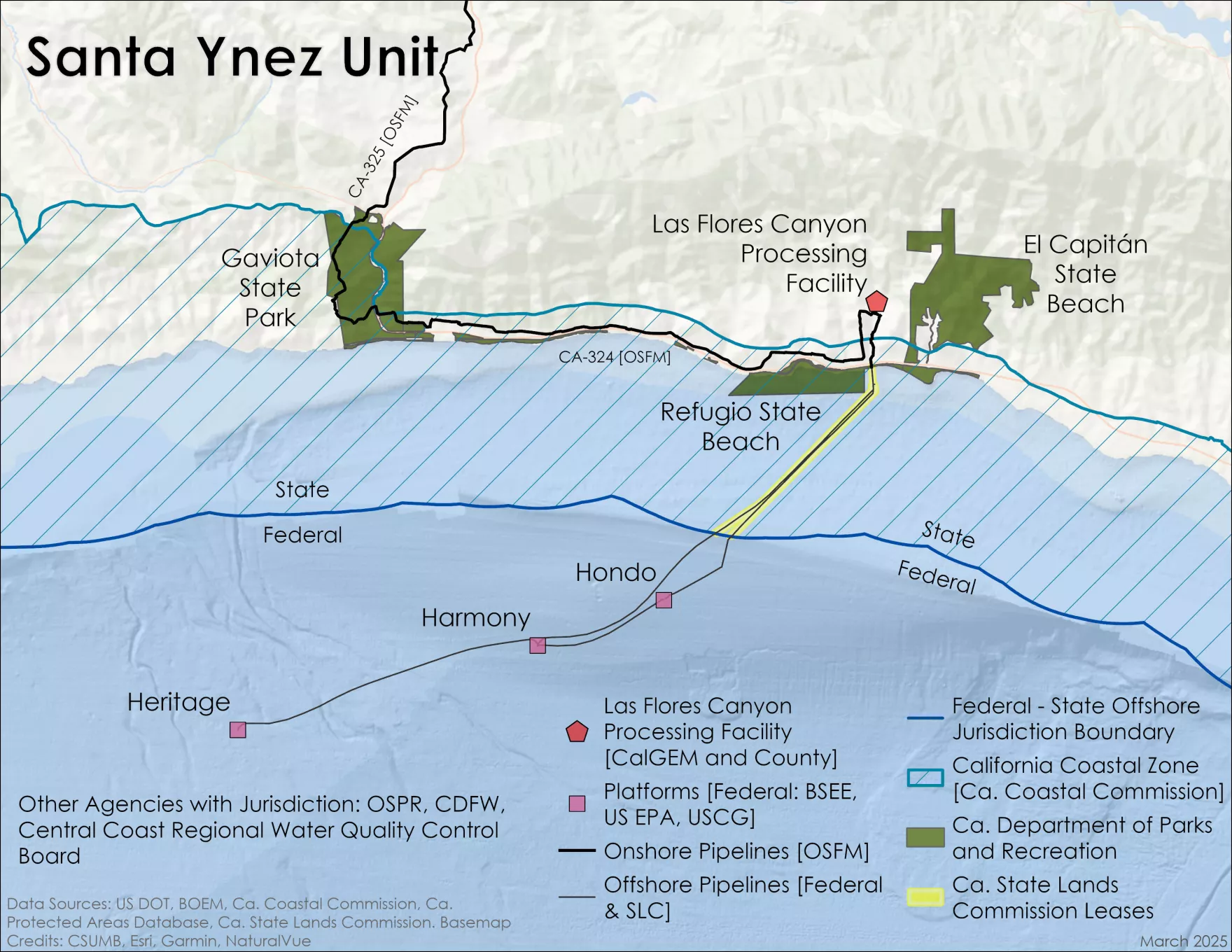

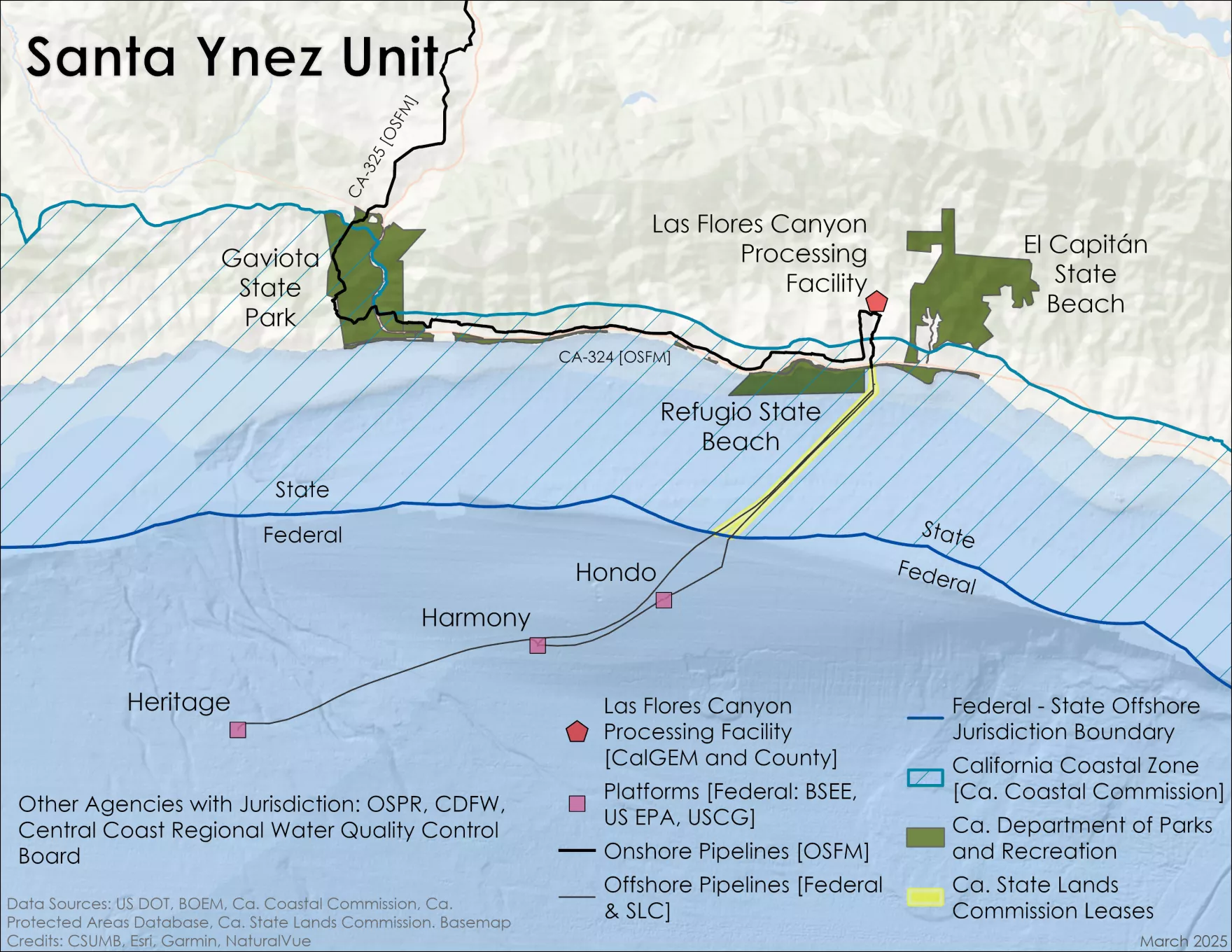

Sable Offshore began ramping up production at Platform Harmony last May delivering oil and gas to their Los Flores Canyon Processing Facility. In March, they resumed transportation to the Pentland pipeline segments and achieved first sales.

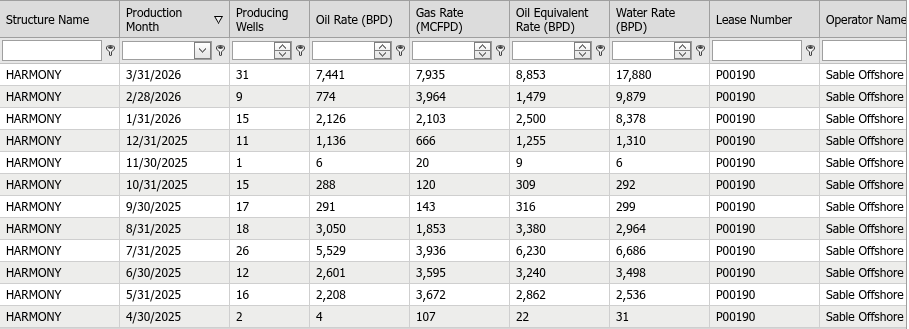

Below are BOEM production data for Harmony through March 2026. Harmony production was expected to increase to 22,000 bopd in May. Similarly, Sable forecasted Heritage production of 30,000 bopd for that month. The actual production numbers should be available in a month or two.

Nothing in the March production data for Harmony is particularly surprising. The gas-oil ratio (GOR) of ~1000 cu ft/bbl is rather typical for oil production in the region, as is the water cut, although less water production would be preferred. Produced water is not discharged from the platform, but is injected subsurface through disposal wells.

In the ongoing Santa Ynez Unit production restart saga, John Smith informs that a California Appellate Court ruled against Sable Offshore by a vote of 2-1, with a strong dissent from one of the three judges.

The decision (attached) affirms the California Coastal Commission’s regulatory authority over Sable’s Los Flores Canyon pipeline repairs, meaning that Sable could be ordered to cease operating the pipeline. However, this is just one element of a complex legal maze. An important case regarding PHMSA’s emergency special permit for the pipeline will be heard by the Federal 9th Circuit Court of Appeals in July.

The dissenting judge’s opinion beginning on p.15 of the attachment sets the stage for the upcoming arguments in the 9th Circuit. Excerpt:

“But first, a dose of reality. The repair work has been done. It is a “fait accompli.” And, pursuant to federal intervention, oil is now flowing in the pipeline without incident. The supremacy clause of the United States Constitution takes precedence. The federal Government trumped the state’s Commission “cease and desist” order and it trumps the preliminary injunction order. Based upon these events, the trial court should vacate the preliminary injunction, dismiss the matter as moot, and nullify the civil penalties.”

Meanwhile, the California Coastal Commission notified Sable Offshore that it intends to issue a cease and desist order aimed at shutting down crude oil extraction in the Santa Barbara Channel.

Sable responds:“Sable Offshore Corp. (“Sable”) through its subsidiary, Pacific Pipeline Company (“PPC”), continues to lawfully operate through its existing coastal development permits which were issued in 1986.”

DOT and others shouldn’t make statements they can’t back up (see the X post below).

As a supporter of responsible offshore oil and gas operations, I find statements like this to be irresponsible and embarrassing. Sable Offshore is not using newer or safer drilling technology than is used in many other areas.

The Sable Offshore Project is using new technology to drill oil that is more safe and environmentally friendly than anywhere in the WORLD@PHMSA_DOT is proud to be a part of this and making America ENERGY DOMINANT 💪 https://t.co/q3ztD1G0R4

— U.S. Department of Transportation (@USDOT) June 10, 2026

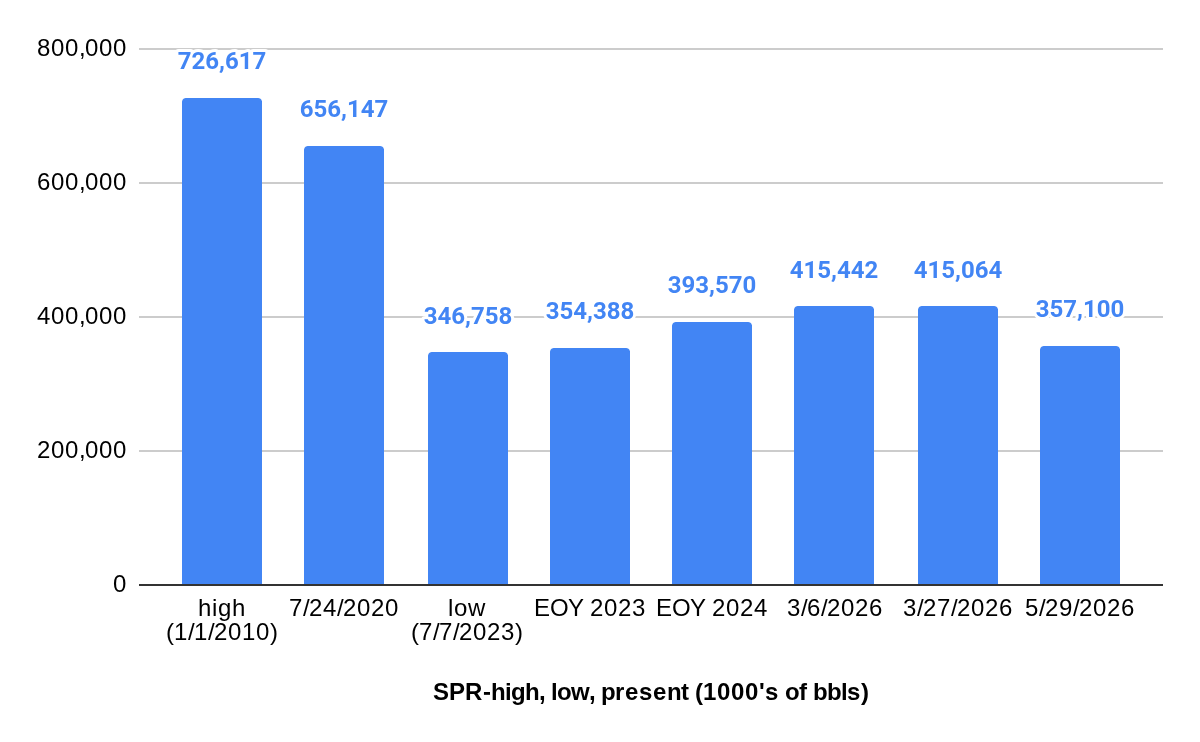

Nothing tilts public opinion more than high gasoline prices, or worse yet shortages! Hence the 1975 legislation establishing the SPR, the massive SPR drawdown in 2022, and this year’s withdrawals.

Looking back to the halcyon days of the US offshore program, it was the gas lines in the 1970s that drove the remarkable and rather unlikely growth in the program during the Carter Administration (1977-1981). A few highlights from those four years:

15 lease sales including 3 offshore Alaska, 3 in the Atlantic, and 1 offshore California

Drilling activity in all 4 regions: GoM, Pacific, Alaska, and Atlantic

North, Mid, and South Atlantic District offices for permitting and inspections

5300 well starts including 97 in water depths > 1000′

314 new platforms including Cognac, the world’s first platform in > 1000′ of water

Perhaps unthinkable today, the Governor of Massachusetts from 1979-1983, Ed King, was a strong supporter of offshore drilling. Absent that support, the exploratory drilling on Georges Bank would probably have never occurred. /s/ Nostalgic Old Man 😉

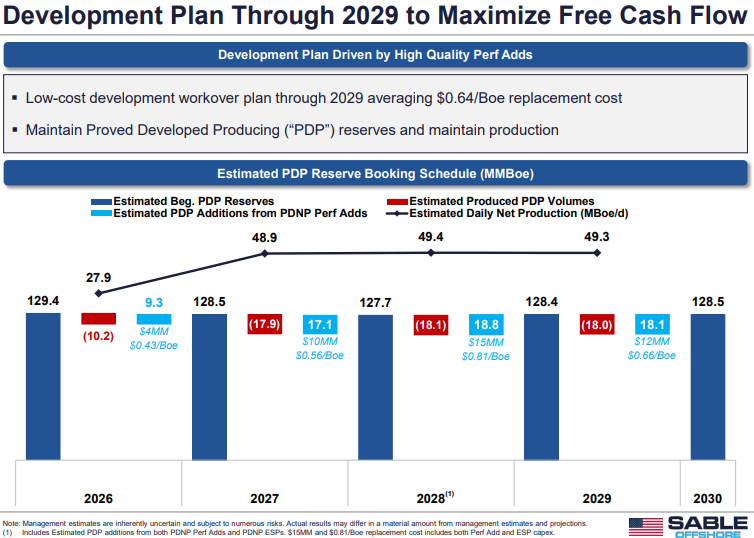

Those who have been following the Santa Ynez Unit saga should take a look at Sable’s informative PowerPoint update (attached). The presentation includes reserve data, well operation plans, production forecasts, financial and legal updates, and regional energy supply information.

Also, Sable CEO Jim Flores has announced that Energy Secretary Wright and Interior Secretary Burgum will be visiting the project this week. Transportation Secretary Duffy was also expected, but he will not be attending.

Santa Barbara Channel, Dos Cuadras Field platforms (L to R): Hillhouse, A, B, and C; Antandrus Wiki photo

As part of the recent focus on decommissioning and financial assurance requirements, I looked at borehole data for platforms A, B, and C on Lease OCS-P 0241 in the Santa Barbara Channel. Platform “A” is where a well blew out in 1969, permanently scarring the US offshore program. Observations:

There are 140 completed and unplugged wells on the 3 platforms. None of the wells on these platforms have been permanently plugged and only one is temporarily abandoned.

The latest available production information (2024 data) indicates ave. daily oil production of 3791 bopd for the lease, including 1901 bopd from Platform A, the highest production for any platform in the region in 2024.

41 of the lease’s completed (unplugged) wells are on Platform A.

The number of these wells that are currently producing is not publicly available.

30 of the completed Platform A wells were drilled prior to 1985.

The blowout well was the 5th well drilled from platform A. All 4 of the wells drilled prior to the 1/28/1969 blowout are still unplugged:

well A-20: spudded on 11/19/1968, reached total depth on 12/2/1968

well A-41: spudded on 11/27/1968, TD on 12/19/1968

well A-25: spudded on 12/18/1968, TD on 12/28/1969

well A-38: spudded on 1/12/1969, TD on 1/24/1969

Note how quickly the wells were drilled. The wells were shallow (2299-4051′ true vertical depth), and the operator (Union Oil) saved time by omitting a casing string. (This decision was a root cause of the blowout and thus changed history 😡)

Lease documents and regulations at 30 CFR § 250.1710require that all wells be permanently plugged within one year of lease termination. For leases like 0241 that are still active, 30 CFR § 250.1711 stipulates that BSEE will order a well to be permanently plugged if the well poses a hazard to safety or the environment, or is not useful for lease operations and is not capable of oil, gas, or sulphur production in paying quantities. In the Gulf of America Region, the policy is to require wells that have not been used in the past 5 years to be permanently plugged. Allowing old wells to remain unplugged is neither prudent nor consistent with the regulations.

Judge Stephen V. Wilson, US District Court for the Central District of California ruled that Sable’s pipeline doesn’t imminently harm Gaviota Park. Judge Wilson said the state “is grasping at straws,” for evidence of real environmental harm, and the federal consent decree governing the terms of the system’s restart is controlled by the California Office of the State Fire Marshall, not the parks department.

The judge didn’t rule on the larger question of whether the Defense Production Act order to restart the Las Flores pipeline system was lawful.