Federal Judge Dolly Gee, Central District of California

Sable Offshore and Exxon had alleged that Santa Barbara County’s refusal to transfer title and permits for Santa Ynez Unit facilities from Exxon to Sable amounted to an unconstitutional taking of their property rights. Judge Gee disagreed.

As colorfully put by Nick Welsh at the Santa Barbara Independent, Judge Gee told Sable and Exxon to “go pound sand” (not literally, but the judicial equivalent). The judge refused to even allow Sable to amend their filing. The judge will however allow Exxon to file an amended complaint, given that the company still has vested rights to the facilities and is still on the hook for the decommissioning costs.

As always with these Santa Ynez Unit matters, there is much more to come!

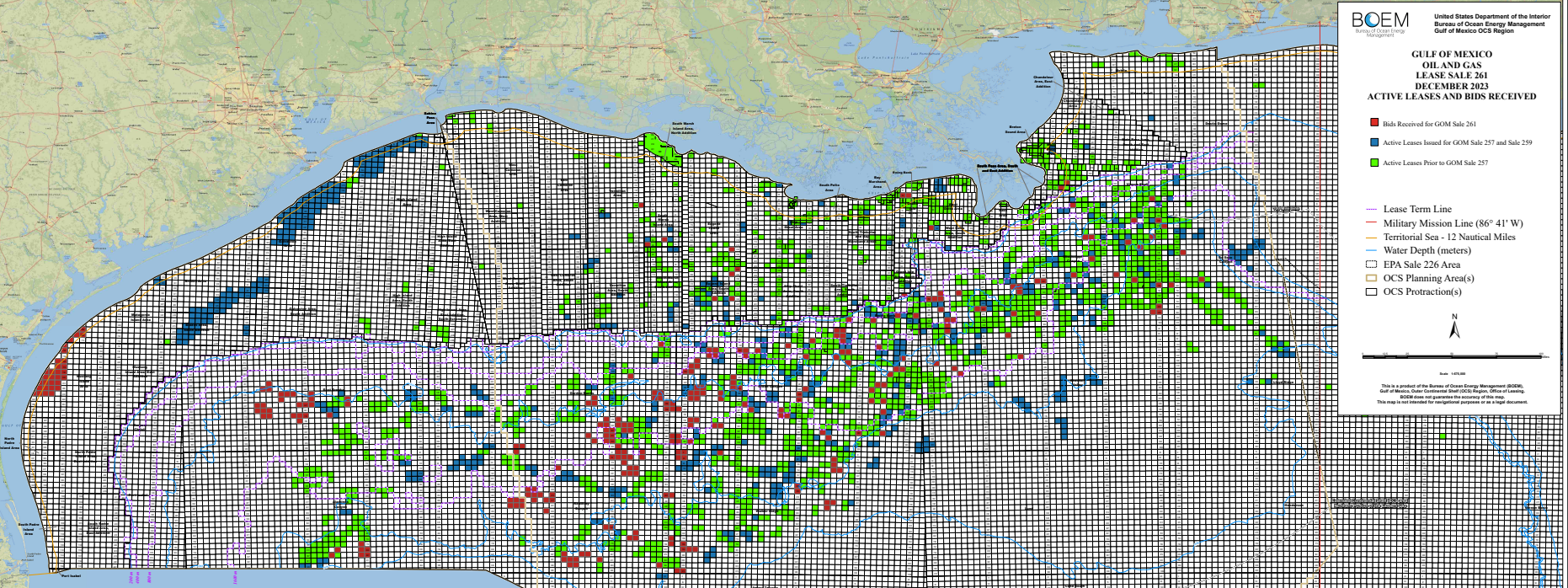

Gulf of America lease map: 199 oil and gas leases were wrongfully acquired for carbon disposal purposes. At Sale 261, Repsol acquired 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon had acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

As expected, the carbon disposal era in Federal offshore waters is ending before it began, and rightfully so.

Energy Intelligence is reporting that Exxon is relinquishing “more than 160 leases” in nearshore Federal waters off Texas. The actual number of oil and gas leases that the company improperly acquired for carbon disposal purposes is 163 (map above).

The reason being cited for the lease relinquishments is that the Dept. of the Interior has shelved regulations for carbon disposal on the OCS. Kudos to the DOI officials responsible for that decision. Carbon disposal has the support of no one except the companies that hope to profit from it. Further, there is no scenario under which Interior could have allowed these wrongfully acquired oil and gas leases to be converted to carbon disposal leases.

Now that these carbon disposal leases are being relinquished, it would be nice to see Exxon start acquiring OCS oil and gas leases for their intended purposes. Exxon and Mobil are historic Gulf operators who were once important contributors to the success of the OCS program.

The oil patch is known for booms, busts, mergers, and acquisitions. Hess is now among the once important offshore operators that no longer exist as separate companies. Others include Amoco, Arco, Texaco, Getty, Gulf, Unocal, Sun, Anadarko, BHP, Mobil, Phillips, Noble Energy, Pennzoil, Kerr-McGee, Superior, Nexen, and Newfield.

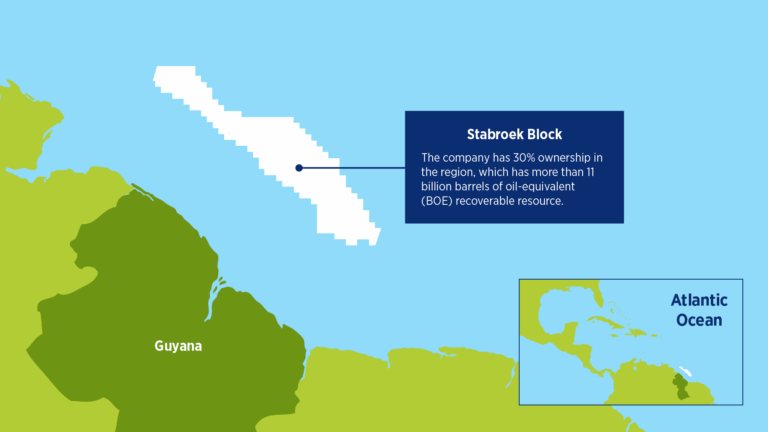

Hess would probably not have been a Chevron target had they not taken a chance in 2014 when they obtained a 30% position in Exxon’s Stabroek block offshore Guyana. The rest is history, and Stabroek is now the world’s most prized offshore block. Hess had other nice assets in the Gulf, Bakken Shale, and elsewhere, but Stabroek was Chevron’s primary target.

Hess was a safety compliance leader in both 2023 and 2024.

Hess was an active participant in pre-merger lease sales.

The combined company is unlikely to be greater than the sum of the parts in terms of US lease acquisition, exploration, and development.

Combining companies limits the diversity of geological assessments and exploration strategies.

Consolidation limits participation on committees engaged in assessing technology and developing standards. Declining industry participation in these activities, which are critical to offshore safety, has been a historical concern of OCS program leadership.

When the merger was announced, Chevron’s CEO Mike Wirth was quoted as saying “We’ve got too many CEOs per BOE, so consolidation is natural.” That comment makes sense from the perspective of an acquiring CEO. Employees of the companies being acquired have a somewhat different view. They would prefer increasing exploration and production rather than reducing employees.

I had the pleasure of visiting the Hibernia gravity-based structure while it was still under construction in Bull Arm, Newfoundland (photo). This pioneering facility, where Newfoundland’s offshore production began in Nov. 1997, continues to impress.

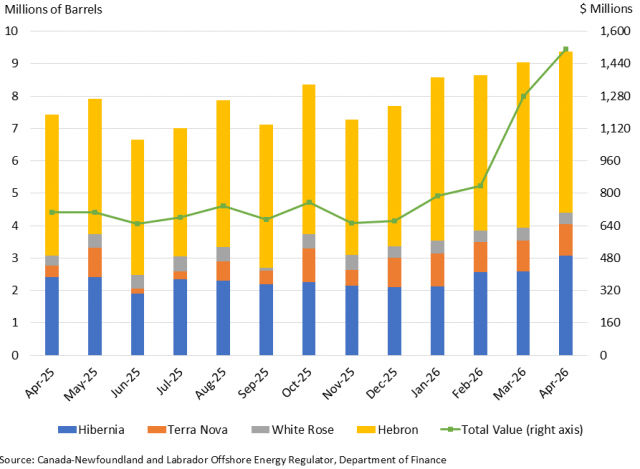

Offshore Newfoundland’s total April production, increased to 9.4 million barrels, with a sharp increase in the value of production (see figure below). This is the highest monthly production level for the province since March 2020, and the second highest monthly production value on record, only behind July 2008.

Meanwhile, production at Hebron, another Exxon GBS structure, has reached record levels this year (chart below). The facility is producing more than 5 million bbls/month.

Finally, Suncor’s decision to refurbish the Terra Nova FPSO and resume production may be paying off given production levels of ~1 million bbls/month.

Oil Now Guyana reports that an Exxon artificial intelligence model built using Guyana’s offshore seismic data was able to identify already-discovered crude oil accumulations with a 90% success rate.

Neil Chapman, Exxon: “…in Guyana, we have built an agent, a model…which if we give it the seismic data that we’ve run and we say, go find the crude oil, it can find all the crude oil that we’ve already found with a 90% success rate.”

(Note: Humans are also great at identifying discoveries after the fact 😉. How many false positives were there?)

Chapman said the company has also used artificial intelligence to review well data from across the industry.

“We have analyzed the well data from 50,000 wells that have been drilled in the industry all over the world, 50,000,” Chapman said. “It would have taken us 15 years to do that analysis. We’ve done it in a matter of weeks.”

Despite the many advances in exploration technology over the years, one caveat remains unchanged: “We don’t know if they’re going to be successful or not until you drill a hole, you can never be sure,” Chapman said.

AI should enhance not just geophysical interpretations, but all aspects of offshore exploration and production including site surveys, well planning and construction, drilling, well control, structure designs, production and pipeline monitoring, and safety management. Hopefully, the net result will be increased production at lower cost with improved safety and environmental performance, and that the workforce will not be reduced, but will become more efficient.

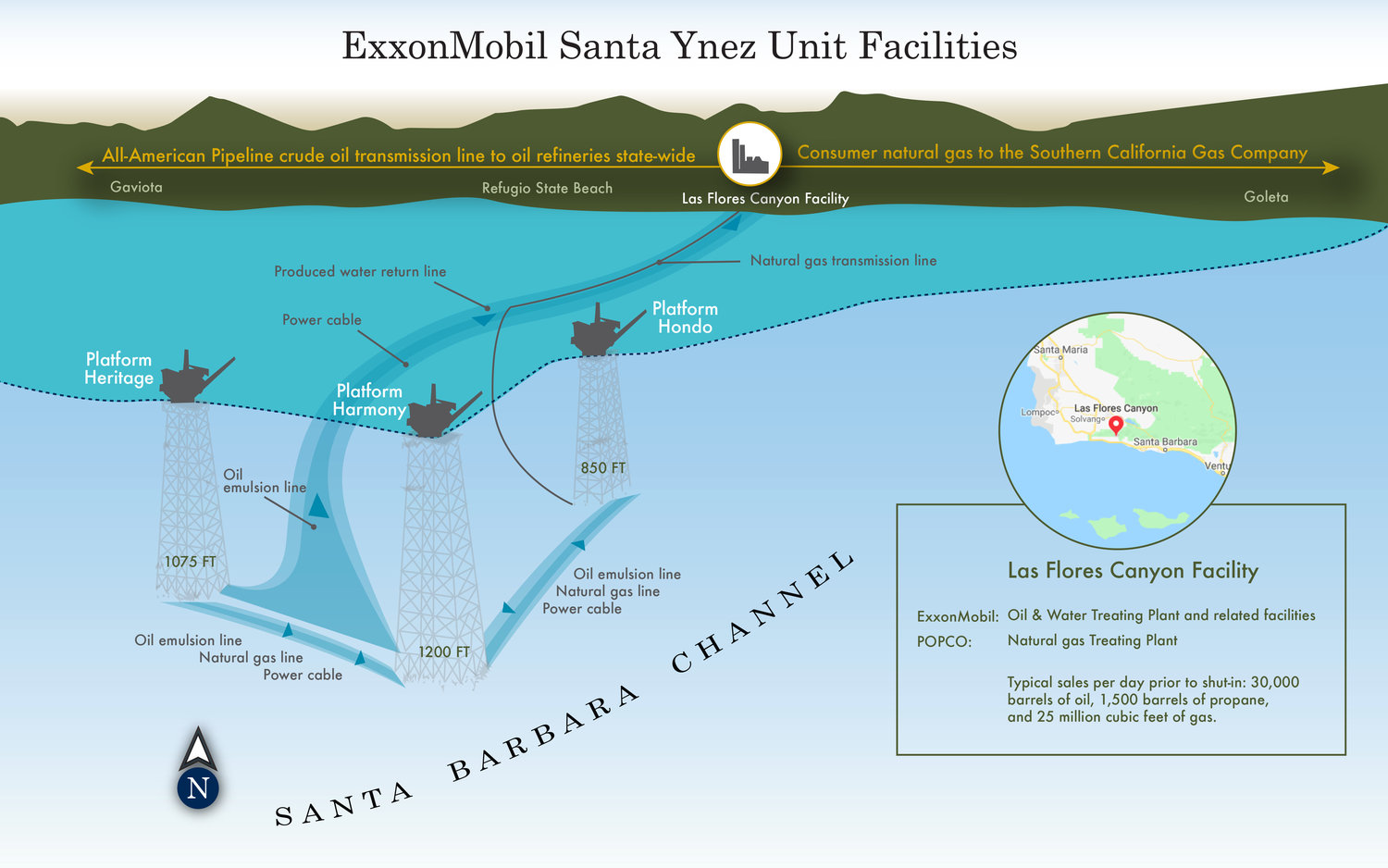

The potential rewards are great – 500+ million barrels of oil, 3 major production platforms, associated pipelines, onshore processing facilities – but can Sable survive the costly legal and administrative challenges? What is Exxon’s plan for the Santa Ynez Unit if Sable should fail?

Pasted below are excerpts from Sable’s Prospectus Supplement. Is Sable serious about pursuing a Santa Ynez Unit strategy that employs a production and treatment vessel 3.5 miles from shore ala the development option that was reluctantly approved by the Federal govt in 1974, two decades before the onshore infrastructure was in place?

The OS&T option is inferior to onshore treatment and pipeline transportation in every way – spill risks, air emissions, economics, ultimate oil recovery, transportation to market, natural gas utilization, and public benefit.

This blogger supports a resumption of Santa Ynez Unit production. However, the only responsible path forward is to do the right thing and continue to pursue the onshore pipeline approvalsadministratively and legally. It is far better to defend a good project than a contrived workaround.

When will BOEM share Sable’s proposed “update”(actually a massive revision) to the SYU Development and Production Plan, as they are obligated to do?

Evaluation of the revised plan will require a detailed environmental review.

Operationally, BSEE and the Coast Guard will need to carefully consider vessel integrity, treatment capabilities, mooring and offloading plans, transportation schemes, gas utilization/injection, and many other technical details.

Meanwhile, does Exxon, the previous (and future?) owner, remain on the sidelines when the OS&T permitting circus begins in earnest?

On September 29, 2025, Sable announced that it is evaluating and pursuing an offshore storage and treating vessel (“OS&T”) strategy to provide access to domestic and global markets via shuttle tankers for federal crude oil produced from the SYU in the Pacific Outer Continental Shelf Area (the “OS&T Strategy”). Continued delays related to the Santa Ynez Pipeline System have prompted Sable to evaluate and pursue the OS&T Strategy. On October 9, 2025, Sable submitted a Development and Production Plan update for the SYU to the Bureau of Ocean Energy Management (“BOEM”). Prior to implementation of the OS&T Strategy, regulatory authorizations are required, including clearance from BOEM.

Preparations for the OS&T Strategy include the acquisition of a suitable OS&T vessel, certain refitting and upgrades to the vessel and the SYU equipment, transportation of the vessel to SYU, and related installation. In connection with implementation of the OS&T Strategy, the Company expects to opportunistically acquire an existing OS&T in the first quarter of 2026, with delivery of the vessel to SYU expected in the third quarter of 2026. Following the acquisition of the vessel, and vessel and platform upgrades and installation, Sable would expect to begin sales from all SYU platforms in the fourth quarter of 2026, with expected comprehensive oil production rates of over 50,000 barrels of oil per day, utilizing the OS&T within the SYU federal leases, provided the Company receives regulatory clearances. Sable estimates that the total capital required to execute the OS&T Strategy is approximately $475.0 million. The Company has already incurred a small portion of such capital expenditures, with the vast majority of such capital expenditures remaining, provided the Company receives regulatory clearances. See “Risk Factors—Risks Associated with Our Operations—In order to commence operations pursuant to an OS&T offtake strategy, we will require clearances and permitting, including from BOEM.”

John comments that the project description, which calls for removing the jacket, seep tents and pipelines, and partially removing the upper 5 feet of the 23-foot-high shell mounds, does not make much sense given the abundant fish and invertebrates that reside on or around the platform jacket.Cutting the jacket off 85 feet below the water line and converting the remaining structure to an artificial reef would make more sense and should have been designated the proposed project.

The plan is to send the materials to the Ports of Long Beach, Los Angeles or Hueneme or possibly Ensenada, Mexico. The project involves complex logistics and is going to be a very long (3 years), ambitious and expensive project that will likely set a precedent for future platform decommissioning projects.

According to their agreement with the CSLC, Exxon is responsible for the decommissioning costs.

Scientific American: The steel “jackets” that support California’s offshore oil platforms are covered in millions of organisms and provide habitat for thousands of fishes. Joe Platko

Unsurprisingly, President Trump was not particularly pleased with Darren Woods’ “uninvestable” quote, the main media takeaway from Friday’s meeting on redevelopment of Venezuela’s oil and gas resources.

Exxon CEO Darren Woods: “If we look at the legal and commercial constructs and frameworks in place today in Venezuela — today, it’s uninvestable.”

The response from President Trump: “I didn’t like Exxon’s response,” Trump said to reporters on Air Force One as he departed West Palm Beach, Florida. “They’re playing too cute.” He told reporters he was inclined to deny Exxon any role in rebuilding Venezuela’s oil industry.

If Exxon is now in the President’s doghouse, what does this mean for the Santa Ynez Unit, an Exxon orphan that was adopted by Sable Offshore? Given Sable’s financial challenges, the SYU may soon be returning to Exxon.

Regardless of ownership, an SYU production restart faces strong opposition in California and is fully dependent on an assertive and supportive Federal government. Meanwhile, an injunction on SYU production remains in place, and despite rumors to the contrary, Sable confirms they are complying with that order.