John Hancock Tower (pictured) is now named for its address, 200 Clarendon St

In the attached complaint, BP Hancock LLC alleges Vineyard Offshore, a Vineyard Wind parent company, is delinquent in paying rent for its space in the famous John Hancock Tower (now known as 200 Clarendon Street) in Boston.

Vineyard Wind had leased 28,370 square feet of space, constituting the entire eighteenth floor of the tower.

Per the complaint:

As of the date of this Complaint, Tenant owes Landlord $824,338.99 in Rent, Additional Rent, and late fees.

Furthermore, Tenant remains obligated to replenish the Security Deposit in the full amount of $386,810.00 as provided under Section 16.26 of the Lease.

As many of you know, Vineyard Wind is engaged in an ugly dispute with its primary contractor, GE Vernova, which was ordered to continue work on the project even though Vineyard Wind stopped making payments.

Santa Barbara Channel, Dos Cuadras Field platforms (L to R): Hillhouse, A, B, and C; Antandrus Wiki photo

As part of the recent focus on decommissioning and financial assurance requirements, I looked at borehole data for platforms A, B, and C on Lease OCS-P 0241 in the Santa Barbara Channel. Platform “A” is where a well blew out in 1969, permanently scarring the US offshore program. Observations:

There are 140 completed and unplugged wells on the 3 platforms. None of the wells on these platforms have been permanently plugged and only one is temporarily abandoned.

The latest available production information (2024 data) indicates ave. daily oil production of 3791 bopd for the lease, including 1901 bopd from Platform A, the highest production for any platform in the region in 2024.

41 of the lease’s completed (unplugged) wells are on Platform A.

The number of these wells that are currently producing is not publicly available.

30 of the completed Platform A wells were drilled prior to 1985.

The blowout well was the 5th well drilled from platform A. All 4 of the wells drilled prior to the 1/28/1969 blowout are still unplugged:

well A-20: spudded on 11/19/1968, reached total depth on 12/2/1968

well A-41: spudded on 11/27/1968, TD on 12/19/1968

well A-25: spudded on 12/18/1968, TD on 12/28/1969

well A-38: spudded on 1/12/1969, TD on 1/24/1969

Note how quickly the wells were drilled. The wells were shallow (2299-4051′ true vertical depth), and the operator (Union Oil) saved time by omitting a casing string. (This decision was a root cause of the blowout and thus changed history 😡)

Lease documents and regulations at 30 CFR § 250.1710require that all wells be permanently plugged within one year of lease termination. For leases like 0241 that are still active, 30 CFR § 250.1711 stipulates that BSEE will order a well to be permanently plugged if the well poses a hazard to safety or the environment, or is not useful for lease operations and is not capable of oil, gas, or sulphur production in paying quantities. In the Gulf of America Region, the policy is to require wells that have not been used in the past 5 years to be permanently plugged. Allowing old wells to remain unplugged is neither prudent nor consistent with the regulations.

John Smith’s update on California OCS Decommissioning Obligations is attached. His comments:

Chevron and FMC hold joint and several liability responsibilities for many platforms and all of those operated by DCOR. This reflects Chevron’s long history in developing CA onshore and offshore oil and gas resources. A 2020 report issued by BSEE estimated the nine platforms operated by DCOR had a combined decommissioning cost of $397 million.The actual cost could be 2-3-fold higher based on estimates for decommissioning California state water platforms prepared by experienced decommissioning consultants.

Chevron may be checking out of California by moving its corporate offices to Houston, but as someone once said about decommissioning – referring to the popular Eagles Hotel California song “You can check out but you can never leave.”

Official decommissioning anthem 😉: Hotel California

Excerpt from the lyrics – Hotel California, Eagles, 1976

Last thing I remember I was running for the door I had to find the passage back To the place I was before “Relax, ” said the night man “We are programmed to receive You can check out any time you like But you can never leave”

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectivelychallenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

BSEE (2020) estimates the cost of decommissioning these facilities to be $85 million (too low), and there is no collateral or third party guarantee.

The responsibility for decommissioning these platforms has yet to be settled. ConocoPhillips, Oxy, and Devon have appealed decommissioning orders from BSEE. The Interior Board of Land Appeals (IBLA) has yet to rule on those appeals. The appellants are funding some plugging operations and facility upgrades pending the IBLA decision.

Per BSEE’s borehole file, this is the current status of the Hogan and Houchin wells:

33 completed and not yet plugged; these wells were drilled between 1968 and 2010

43 temporarily abandoned (TA) wells plugged in accordance with 30 CFR § 250.1721

10 wells have been updated to TA status in the past 6 months (latest 3/22/2026), so some progress is being made

If you are interested in the Hogan/Houchin mess or decommissioning liability in general, I highly recommend that you look at Devon’s informative and rather compelling appeal to IBLA. Similar appeals were submitted by Oxy and ConocoPhillips.

Lease history (excerpted from the Devon appeal):

Lease OCS-P 0166 was issued effective January 1, 1967.

Phillips Petroleum Company (“Phillips”) (predecessor to ConocoPhillips), Cities Service Oil Company (predecessor to Oxy), and Continental Oil Company (predecessor to ConocoPhillips) were the initial lessees

Phillips was designated operator on January 25, 1967

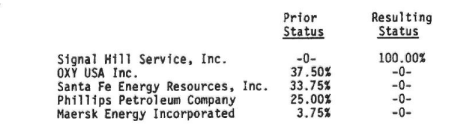

February 28, 1983: Petro-Lewis Funds, Inc., obtained the 37.5% interest of the Continental Oil Company (which in 1979 had changed its name to Conoco Inc., now Conoco Phillips Company (“ConocoPhilips”)).

November 1983: Cities Service Oil Company assigned its 37.5% interest to Cities Service Oil and Gas Corporation (now OXY U.S.A. Inc).

July 2, 1987: the Minerals Management Service (“MMS”) approved two more assignments of the Lease. One, from PetroLewis Funds, Inc. to American Royalty Producing Company (“American Royalty”), was approved retroactively to December 31, 1984. The other, from American Royalty to Santa Fe Energy Company(“Santa Fe”), was approved retroactively to April 30, 1987.

April 1, 1988: Santa Fe transferred a 3.75% interest to Maersk Energy Incorporated, reducing Santa Fe’s share to 33.75%.

1991 Assignment to Signal Hill: MMS approved assignment of the lease to Signal Hill effective February 5, 1991. The assignment was approved without any provision under which the assignors agreed to be liable for decommissioning operations on the lease. MMS’s approval actually had the opposite effect, leaving such obligations to the assignee. The assignment was approved despite concerns within the MMS about the financial strength of Signal Hill and the technical competence of Pacific Operators Offshore Inc (POOI), the affiliate that would operate the facilities.

Comments:

The assignment to Signal Hill should have never been approved. The outcome was predictable.

The Devon, Oxy, and ConocoPhillips appeals are very strong and would seem to have a good chance of success. Perhaps that is why the IBLA decision is taking so long (nearly 5 years to date).

Given the uncertainty regarding this appeal, the absence of transparency about other potential decommissioning liabilities, and the uncertainties regarding the administration of predecessor liability, this is not the time to be relaxing financial assurance requirements and further exposing taxpayers to decommissioning risks.

This is the final day to comment on BOEM’s proposal:

At a minimum, the fire will further delay and increase the cost of well plugging operations on Platform Habitat. Per BSEE’s borehole file, 17 wells remain to be permanently abandoned, 3 of which have yet to be temporarily abandoned. These wells are 23-44 years old, and have been inactive for 11 years.

If there is significant platform damage, the remediation delays and costs would be substantial, comparable to those associated with major Gulf platforms damaged by hurricanes. Structural damage could increase the urgency of removing the platform. Given California’s decommissioning quagmire, this would be a major challenge.

Who pays, and what does the financial assurance picture look like? Per the attached BOEM spreadsheet (excerpt pasted below):

The 2020 cost estimate for decommissioning Habitat was $44.3 million. That number is optimistic even if platform damage is minimal.

$13.6 million in supplemental assurance has been provided.

A third party guarantee has been secured.

The guarantee was provided by Freeport-McMoRan Oil & Gas (FMOG)

Per BOEM, FMOG is the guarantor for all DCOR leases. Unless BOEM has allowed otherwise, the guarantor pays all costs not covered by the lessees. Given the number of old platforms and California decommissioning challenges, the risks for FMOG are indeed large.

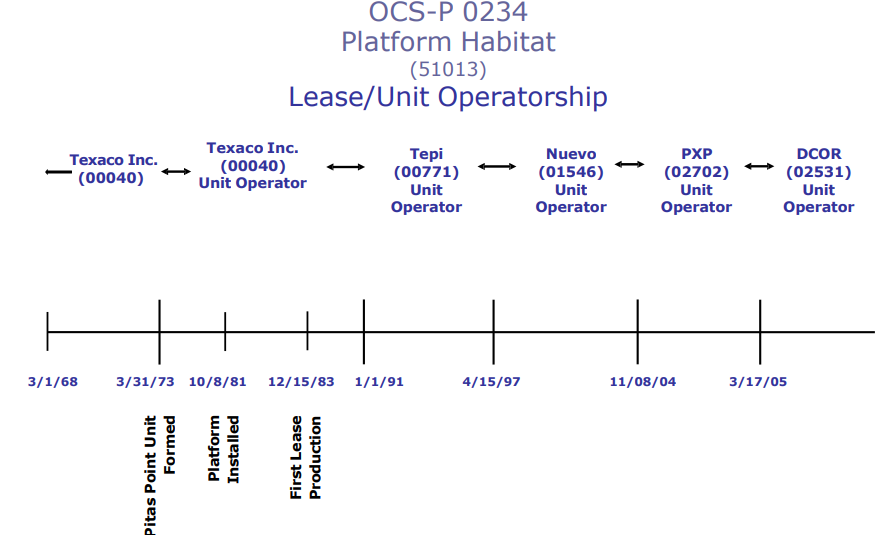

Although DCOR LLC is the current Habitat operator, the company owns only a 4.18% share of the project. CHANNEL ISLANDS CAPITAL, L.L.C., a private company about which little is known, holds a 95.82% share.

Should the 2 owners default, BOEM/MMA will look to the guarantor and predecessor lessees (see the chart below). Unfortunately for FMOG, they are both the guarantor and the predecessor lessee. FMOG acquired Plains Exploration & Production (PXP), the operator prior to DCOR. Nuevo Energy was acquired by PXP and thus also tracks back to FMOC. (This may explain FMOC’s decision to be a guarantor!).

Should FMOC fail to fulfill their obligation. Chevron would likely be the next target. The original Harvest partners were Texaco (operator) and Union Oil, both of which were acquired by Chevron.

TEPI=Texaco Expl. & Production. Nuevo Energy was acquired by Plains Expl.&Production (PXP), which was acquired by Freeport McMoRan Oil & Gas (FMOG)

Requesting a 60 day extension (double the comment period specified by BOEM)

Need more time to:

review the detailed proposed changes

conduct studies to inform agency

analyze the studies and data

consider alternatives

organize, complete, and review the findings of subject matter workgroups

In API’s favor:

Agencies have discretion on extending comment periods.

60 days is typically considered the minimum comment period; 90 days would have been more appropriate for this proposal.

API members are clearly affected parties.

The BOEM proposal relaxes financial assurance requirements for smaller companies while increasing predecessor lessee risk exposure. Those predecessors would typically be API members.

There are divisions within the industry which complicate trade association commenting.

On the other hand:

API’s letter is dated May 1, just one week prior to the end of the comment period.

The letter was not posted at Regulations.gov until May 6, 2 days before the end of the comment period. Only those tracking the comment letters would have been aware of the request even at this late date.

As of early this morning (May 7th), the docket still specifies a May 8 due date for comments.

An extension could be viewed as inequitable to other concerned parties who made special efforts to honor the deadline.

Comments:

This is why it’s best to specify a reasonable comment period at the time the regulation is proposed, and make it clear that there will be no extension. That way, everyone is treated the same.

For this proposal, 90 days would have been reasonable.

Given the number of significant issues that need to be addressed, the best outcome for this rule would be a re-proposal. See the comments submitted by John Smith and me.

Attached are my comments on BOEM’s proposed revisions to the decommissioning financial assurance regulations. These comments were submitted to Regulations.gov yesterday (3 days early 😀). Bud

Concluding Remarks

MMA’s highest priority must be assuring that facilities are safely decommissioned without public funding. Supplemental financial assurance determinations and lease assignment approvals must be consistent with that priority.

Predecessor liability is an important financial assurance principle, but legal boundaries and administrative procedures must be clearly established.

Safety and compliance are inextricably related to financial performance, and must be considered in determining supplemental assurance requirements.

Using reserve estimates to reduce supplemental assurance exposes taxpayers to geologic and accounting risks.

Unacceptable public risks have resulted from financial assurance decisions intended to advance offshore wind development.

Looking up towards Platform Gilda from a depth of 100 feet, juvenile bocaccio rockfish swirl around the anemone-covered crossbeams (photo by Dr. Milton Love)

Dr. Jeremy Claisse, Cal Poly Pomona: “The oil and gas platforms off the coast of California are the most productive marine habitats per unit area in the world.”

Dr. Milt Love, UCSB: “Even the least productive platform was more productive than Chesapeake Bay or a coral reef in Moorea.”

John Smith has made the case for reefing California platforms. He is now proposing a change in the regulations that could facilitate such partial removals of offshore structures. His full proposal is attached.

As background John notes:

“In contrast to the Gulf of Mexico (GOM), where more than 600 decommissioned platforms have been converted to artificial reefs, the State of California does not have reefing legislation considered workable by industry, nor does it have an approved or State funded artificial reefing program which is a prerequisite under MMA (formerly BSEE and BOEM) OCS oil and gas regulations (30 CFR § 250.1730) for waiving platform removal requirements which allows conversion of the structure to an artificial reef.“

He further informs that “operators of the platforms have not expressed any serious interest in reefing OCS platform jackets because they consider the California Marine Resources Legacy Act unworkable in its present form due primarily to its liability provisions, inequitable 80% cost-savings sharing requirement, and the requirement for the first reefing applicant to fund the setup costs for the artificial reefing program.“

John’s proposal is intriguing because it allows qualified 3rd parties to accept title and liability for reefed structures. This would create interesting business opportunities. A company, consortium, nonprofit, or entrepreneur could, for a fee, acquire submerged structures and obtain insurance or other financial protection in accordance with their business plan. Reef preservation and enhancement studies, and other marine research could also be conducted at the sites. Marine ecosystems would be protected, and the cost and efficiency of decommissioning operations would be significantly improved.

“So, you disconnect the jacket… you kill all the fish. There’s an awful lot of animals that die,” said Dr. Love. As our world has become dependent on fossil fuels, so too have these millions of animals become dependent on the structures that pump them from beneath the sea floor. “As a biologist, I just give people the facts, but I have my own view as a citizen, which is I think it’s criminal to kill huge numbers of animals,” said Dr. Love.

Restart seems likely for decommissioning financial assurance rule

Posted in decommissioning, energy policy, Regulation, tagged API, BOEM, Chevron, comments, decommissioning, financial assurance, NEFSA, proposed regulation, Shell on May 18, 2026| Leave a Comment »

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectively challenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

Lastly, kudos to the New England Fisherman’s Stewardship Association for raising the concern about financial assurance for decommissioning offshore wind facilities

Read Full Post »