In light of the decommissioning fire at Platform Habitat, I checked on the status of well plugging operations at Platforms Hogan and Houchin.

BSEE (2020) estimates the cost of decommissioning these facilities to be $85 million (too low), and there is no collateral or third party guarantee.

The responsibility for decommissioning these platforms has yet to be settled. ConocoPhillips, Oxy, and Devon have appealed decommissioning orders from BSEE. The Interior Board of Land Appeals (IBLA) has yet to rule on those appeals. The appellants are funding some plugging operations and facility upgrades pending the IBLA decision.

Per BSEE’s borehole file, this is the current status of the Hogan and Houchin wells:

- 33 completed and not yet plugged; these wells were drilled between 1968 and 2010

- 43 temporarily abandoned (TA) wells plugged in accordance with 30 CFR § 250.1721

- 10 wells have been updated to TA status in the past 6 months (latest 3/22/2026), so some progress is being made

- 0 permanently abandoned wells (30 CFR § 250.1715)

Therefore, by my count, 33 wells have yet to be TA’d, and all 76 wells remain to be PA’d. Note that the lease was relinquished nearly 6 years ago (10/14/2020).

If you are interested in the Hogan/Houchin mess or decommissioning liability in general, I highly recommend that you look at Devon’s informative and rather compelling appeal to IBLA. Similar appeals were submitted by Oxy and ConocoPhillips.

Lease history (excerpted from the Devon appeal):

- Lease OCS-P 0166 was issued effective January 1, 1967.

- Phillips Petroleum Company (“Phillips”) (predecessor to ConocoPhillips), Cities Service Oil Company (predecessor to Oxy), and Continental Oil Company (predecessor to ConocoPhillips) were the initial lessees

- Phillips was designated operator on January 25, 1967

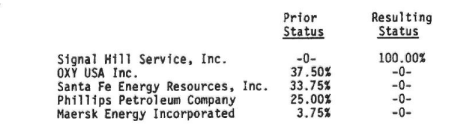

- February 28, 1983: Petro-Lewis Funds, Inc., obtained the 37.5% interest of the Continental Oil Company (which in 1979 had changed its name to Conoco Inc., now Conoco Phillips Company (“ConocoPhilips”)).

- November 1983: Cities Service Oil Company assigned its 37.5% interest to Cities Service Oil and Gas Corporation (now OXY U.S.A. Inc).

- July 2, 1987: the Minerals Management Service (“MMS”) approved two more assignments of the Lease. One, from PetroLewis Funds, Inc. to American Royalty Producing Company (“American Royalty”), was approved retroactively to December 31, 1984. The other, from American Royalty to Santa Fe Energy Company(“Santa Fe”), was approved retroactively to April 30, 1987.

- April 1, 1988: Santa Fe transferred a 3.75% interest to Maersk Energy Incorporated, reducing Santa Fe’s share to 33.75%.

1991 Assignment to Signal Hill: MMS approved assignment of the lease to Signal Hill effective February 5, 1991. The assignment was approved without any provision under which the assignors agreed to be liable for decommissioning operations on the lease. MMS’s approval actually had the opposite effect, leaving such obligations to the assignee. The assignment was approved despite concerns within the MMS about the financial strength of Signal Hill and the technical competence of Pacific Operators Offshore Inc (POOI), the affiliate that would operate the facilities.

Comments:

- The assignment to Signal Hill should have never been approved. The outcome was predictable.

- The Devon, Oxy, and ConocoPhillips appeals are very strong and would seem to have a good chance of success. Perhaps that is why the IBLA decision is taking so long (nearly 5 years to date).

- Given the uncertainty regarding this appeal, the absence of transparency about other potential decommissioning liabilities, and the uncertainties regarding the administration of predecessor liability, this is not the time to be relaxing financial assurance requirements and further exposing taxpayers to decommissioning risks.

This is the final day to comment on BOEM’s proposal:

Restart seems likely for decommissioning financial assurance rule

Posted in decommissioning, energy policy, Regulation, tagged API, BOEM, Chevron, comments, decommissioning, financial assurance, NEFSA, proposed regulation, Shell on May 18, 2026| Leave a Comment »

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectively challenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

Lastly, kudos to the New England Fisherman’s Stewardship Association for raising the concern about financial assurance for decommissioning offshore wind facilities

Read Full Post »