In light of the decommissioning fire at Platform Habitat, I checked on the status of well plugging operations at Platforms Hogan and Houchin.

BSEE (2020) estimates the cost of decommissioning these facilities to be $85 million (too low), and there is no collateral or third party guarantee.

The responsibility for decommissioning these platforms has yet to be settled. ConocoPhillips, Oxy, and Devon have appealed decommissioning orders from BSEE. The Interior Board of Land Appeals (IBLA) has yet to rule on those appeals. The appellants are funding some plugging operations and facility upgrades pending the IBLA decision.

Per BSEE’s borehole file, this is the current status of the Hogan and Houchin wells:

- 33 completed and not yet plugged; these wells were drilled between 1968 and 2010

- 43 temporarily abandoned (TA) wells plugged in accordance with 30 CFR § 250.1721

- 10 wells have been updated to TA status in the past 6 months (latest 3/22/2026), so some progress is being made

- 0 permanently abandoned wells (30 CFR § 250.1715)

Therefore, by my count, 33 wells have yet to be TA’d, and all 76 wells remain to be PA’d. Note that the lease was relinquished nearly 6 years ago (10/14/2020).

If you are interested in the Hogan/Houchin mess or decommissioning liability in general, I highly recommend that you look at Devon’s informative and rather compelling appeal to IBLA. Similar appeals were submitted by Oxy and ConocoPhillips.

Lease history (excerpted from the Devon appeal):

- Lease OCS-P 0166 was issued effective January 1, 1967.

- Phillips Petroleum Company (“Phillips”) (predecessor to ConocoPhillips), Cities Service Oil Company (predecessor to Oxy), and Continental Oil Company (predecessor to ConocoPhillips) were the initial lessees

- Phillips was designated operator on January 25, 1967

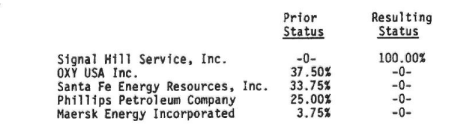

- February 28, 1983: Petro-Lewis Funds, Inc., obtained the 37.5% interest of the Continental Oil Company (which in 1979 had changed its name to Conoco Inc., now Conoco Phillips Company (“ConocoPhilips”)).

- November 1983: Cities Service Oil Company assigned its 37.5% interest to Cities Service Oil and Gas Corporation (now OXY U.S.A. Inc).

- July 2, 1987: the Minerals Management Service (“MMS”) approved two more assignments of the Lease. One, from PetroLewis Funds, Inc. to American Royalty Producing Company (“American Royalty”), was approved retroactively to December 31, 1984. The other, from American Royalty to Santa Fe Energy Company(“Santa Fe”), was approved retroactively to April 30, 1987.

- April 1, 1988: Santa Fe transferred a 3.75% interest to Maersk Energy Incorporated, reducing Santa Fe’s share to 33.75%.

1991 Assignment to Signal Hill: MMS approved assignment of the lease to Signal Hill effective February 5, 1991. The assignment was approved without any provision under which the assignors agreed to be liable for decommissioning operations on the lease. MMS’s approval actually had the opposite effect, leaving such obligations to the assignee. The assignment was approved despite concerns within the MMS about the financial strength of Signal Hill and the technical competence of Pacific Operators Offshore Inc (POOI), the affiliate that would operate the facilities.

Comments:

- The assignment to Signal Hill should have never been approved. The outcome was predictable.

- The Devon, Oxy, and ConocoPhillips appeals are very strong and would seem to have a good chance of success. Perhaps that is why the IBLA decision is taking so long (nearly 5 years to date).

- Given the uncertainty regarding this appeal, the absence of transparency about other potential decommissioning liabilities, and the uncertainties regarding the administration of predecessor liability, this is not the time to be relaxing financial assurance requirements and further exposing taxpayers to decommissioning risks.

This is the final day to comment on BOEM’s proposal: