The Rigs-to-Resistors category in our World Famous Rigs-to-Reefs +++ list has been expanded to include offshore data centers, a concept that is attracting investor interest (see attached brochure).

Advantages of offshore data centers include power availability (natural gas, hydro-kinetic, wind, solar), cooling water, sovereignty, and growth potential.

“use, for energy-related purposes or for other authorized mariner elated purposes, facilities currently or previously used for activities authorized under this Act,”

The attachment summarizes plans to install modular data centers on existing offshore platforms. The advocates see “using fixed platforms ready for decommissioning as a low-cost solution with simpler execution.” Are they a bit too optimistic? 😉

The attached legal petition from Save LBI and Green Oceans, asserts that BOEM improperly amended OCS wind leases at the end of the previous Administration.

The amended language makes it more difficult to cancel leases by stipulating that an OCS wind lease must be suspended for 5 years before it can be cancelled, and that in the event of cancellation, the lessees must be compensated.

The sentence of concern:

Any cancellations are subject to the limitations and protections contained in subsections 5(a)(2)(B) and (C) of the Act (43 U.S.C. § 1334 (a)(2)(B) and (C)). (Those subsections are pasted at the end of this post in their entirety.)

Compensation could be very costly to the Federal govt (taxpayer) given the wild (irrational?) bidding for some leases and subsequent planning and development costs.

See Section 8 of this lease for an example of the amended language. Note that the lease changes are not highlighted or otherwise identified; nor was there any public notice of this change.

The petitioners are requesting that the new lease language be rescinded and that cancellation language in the lease be aligned with the regulations.

(B) that such cancellation shall not occur unless and until operations under such lease or permit shall have been under suspension, or temporary prohibition, by the Secretary, with due extension of any lease or permit term continuously for a period of five years, or for a lesser period upon request of the lessee;

(C)that such cancellation shall entitle the lessee to receive such compensation as he shows to the Secretary as being equal to the lesser of (i) the fair value of the canceled rights as of the date of cancellation, taking account of both anticipated revenues from the lease and anticipated costs, including costs of compliance with all applicable regulations and operating orders, liability for cleanup costs or damages, or both, in the case of an oilspill, and all other costs reasonably anticipated on the lease, or (ii) the excess, if any, over the lessee’s revenues, from the lease (plus interest thereon from the date of receipt to date of reimbursement) of all consideration paid for the lease and all direct expenditures made by the lessee after the date of issuance ofsuch lease and in connection with exploration or development, or both, pursuant to the lease (plus interest on such consideration and such expenditures from date of payment to date of reimbursement), except that (I) with respect to leases issued before September 18, 1978, such compensation shall be equal to the amount specified in clause (i) of this subparagraph; and (II) in the case of joint leases which are canceled due to the failure of one or more partners to exercise due diligence, the innocent parties shall have the right to seek damages for such loss from the responsible party or parties and the right to acquire the interests of the negligent party or parties and be issued the lease in question;

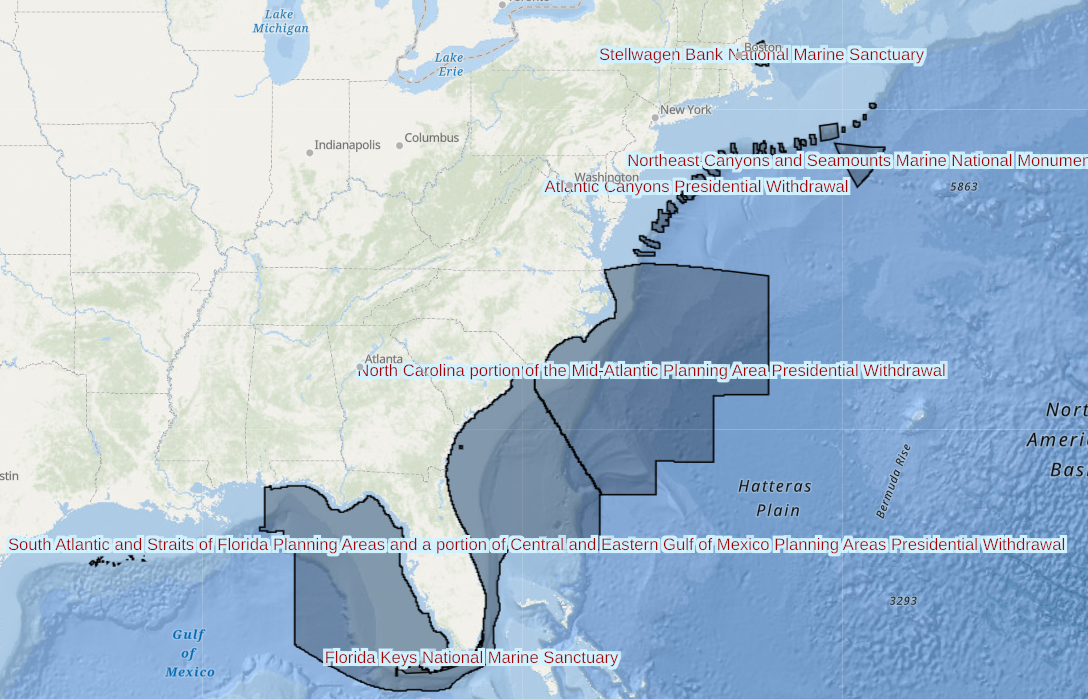

As expected, the White House announced the largest ever permanent ban on offshore oil and gas leasing in the US, and to the best of my knowledge, anywhere in the world.

The sheer magnitude of the ban makes other such withdrawals appear modest by comparison. It’s amazing how bold Presidents (and their handlers) become when they are about to leave office.

The permanent ban includes:

The entire Atlantic Outer Continental Shelf (OCS): While there are no current oil and gas leases in the US Atlantic, the region is highly prospective and could contain more than 20 billion barrels of oil equivalent (BOE).

The Eastern Gulf of Mexico: This is the OCS area that many petroleum geologists find most attractive. The best prospects are >100 miles from shore which minimizes coastal risks, and the high natural gas potential aligns with Florida legislation supporting the use of gas for power generation.

The entire Pacific OCS: While the resources are substantial, their loss has been a foregone conclusion for 25 years. When you can’t even decommission old platforms or restore production on important existing facilities (i.e. the Santa Ynez Unit), how can you possibly expect to issue new leases?

The remainder of the OCS offshore western Alaska. The wishes of the majority of Alaskans, who support offshore exploration and development, have been largely ignored for decades.

President-elect Trump has vowed to reverse President Biden’s leasing ban, but that may not be so easy. This is not a matter of simply reversing an executive order. Sec. 12(a) of OCSLA grants the authority to withdraw lands to the President and does not provide for reversal by future Presidents. The attached NYU Law brief concludes that “a subsequent president lacks authority to restore previously withdrawn lands to the federal oil and gas leasing inventory.”

The new Administration will no doubt have a different view than that expressed in the NYU Law brief, but any reversal decision will likely be challenged in court.

Those who wrote and approved Sec. 12(a) should have had more foresight. However, 72 years ago the authors presumably thought Presidents would only use the authority to remove small, especially sensitive areas from leasing consideration, and never thought that a President would remove both of our oceans and much of the Gulf of Mexico!

Congress could of course reverse the Biden bans, but given the complexity of offshore energy issues, such legislation may be difficult to pass.

“Offshore wind, I have decided to put the project on pause” with Trump’s return, Total Chief Executive Officer Patrick Pouyanne said at an energy industry conference in London on Tuesday.

“I said to my team, the project in New York, we’ll see that in four years,”he said. “But the advantage is it’s only for four years.”

Perhaps Mr. Pouyanne thinks Total owns those 84,332 acres in the Atlantic or that they have the right to hold the leased area indefinitely. They do not. The OCS Lands Act calls for diligent development of leases and BOEM has promulgated implementing regulations.

The Total (Attentive Energy) lease was issued on 5/1/2022. Per 30 CFR § 585.235(a)(1), the company must submit a Construction and Operations Plant (COP) no later than 5/1/2027, more than 20 months before the end of the Trump administration. BOEM will have ample time to act on the plan prior to the next administration.

BOEM could also call for progress updates and an earlier COP submittal if there is evidence that the lessee is not moving forward with development plans (as would already seem to be the case given Mr. Pouyanne’s public statements in London).

In the absence of progress in developing the lease, BOEM could seek cancellation (§ 556.1102) for failure to comply with the diligence mandate in OCSLA (556.1102 (a)). Cancellation could also be pursued based on misrepresentations in acquiring the lease (556.1102 (c)) or the threat of unacceptable harm to the environment or national security (556.1102 (d)).

Rather than making rash comments at a public forum in London, perhaps Mr. Pouyanne would have been wise to first meet with energy officials of the new administration early next year. At a minimum, the CEO’s comments will help justify any attempts to cancel the Total (Attentive Energy) lease on diligence grounds.

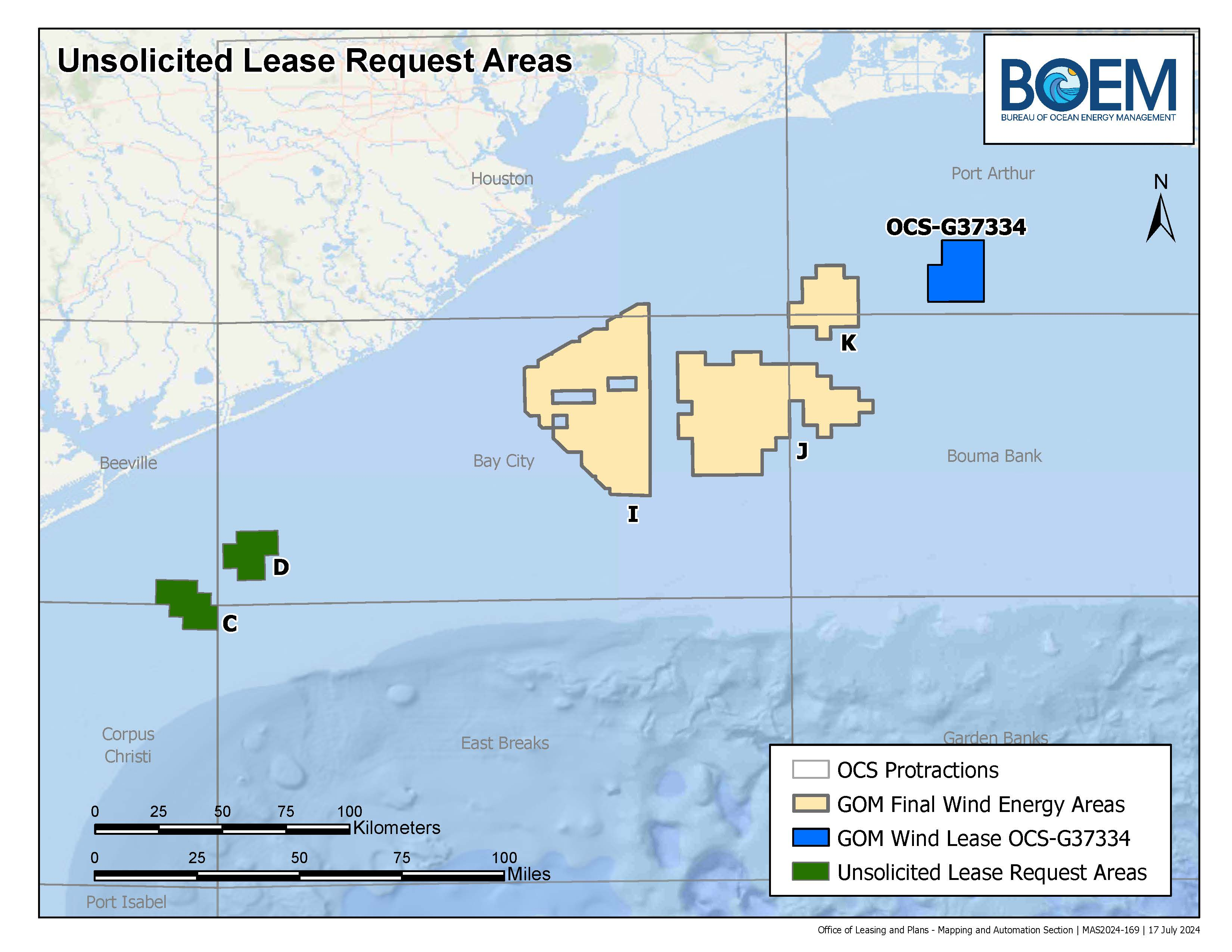

Hercate lease request – C & D. Wind areas that were considered for 2nd GoM sale – I, J, & K. Active RWE lease – blue.

GoM wind leasing update:

BOEM’s highly promoted 2023 GoM wind sale was a bust. The sole bidder, the German company RWE, acquired a single lease.

BOEM’s second GoM wind sale failed to get off the ground. Because only one company expressed interest in participating, that sale has been cancelled.

BOEM is now surveying interest in other GoM areas as a result of an unsolicited lease request from Hercate Energy.

If BOEM does not receive competing indications of interest, they may (and probably will) issue a noncompetitive lease to Hecate.

BOEM calls Hercate an “industry leader.” However, per their website, Hecate is mainly a solar energy company with only 2 wind projects. Both of those wind projects are onshore (Kentucky), and are “in development” (i.e. not yet operating). Hercate is no doubt a fine company, but have they demonstrated the technical expertise and financial strength needed for offshore wind development?

BOEM’s aggressive wind leasing policy stands in stark contrast to their current oil and gas policy. Not a single oil and gas sale will be held in 2024. Were it not for a provision in the “Inflation Reduction Act,” the last 3 GoM sales (257, 259, and 261) would probably not have occurred.

The new 5 year oil and gas leasing plan confirms that the Dept. of the Interior (DOI) has no intention of fulfilling their statutory oil and gas leasing mandate. In announcing the new 5 year plan, DOI boasted that the plan includes the fewest sales (3) of any plan in the history of the program. DOI strongly implied that the only reason those 3 sales were included was to sustain the wind program.,

When we drafted the OCSLA amendments that authorize offshore wind leasing, we envisioned complementary and synergistic programs, not a dogmatic pro-wind bias. As experts like Daniel Yergin have repeatedly warned, the notion that wind energy can eliminate the need for oil and gas is pure folly.

CP’s acquisition of Marathon is an endorsement of shale production, most of which is from private lands. Sadly, these historically important OCS operators no longer have an interest in the Federal offshore sector.

Sec. 12(a) of OCSLA (43 U.S. Code § 1341(a)): “The President of the United States may, from time to time, withdraw from disposition any of the unleased lands of the outer Continental Shelf.”

The language “from time to time” implies that withdrawing OCS lands from oil and gas leasing consideration is a casual exercise at the whim of the President for any particular reason. That is indeed how the provision has been implemented.

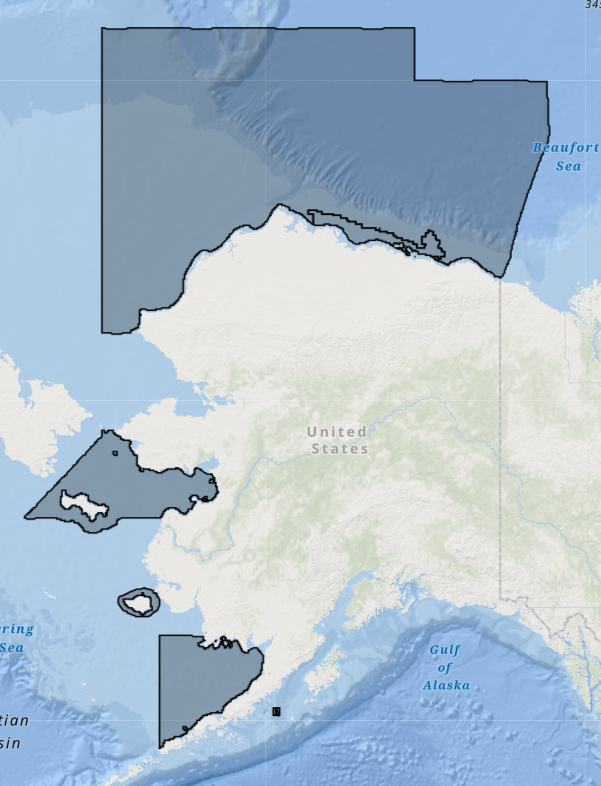

Alaska Presidential withdrawals are shaded (BOEM map)Atlantic and GoM withdrawals are shaded (BOEM map)

Over the last 8 years, Presidents Obama, Trump, and Biden have unilaterally exercised this authority without prior notice or opportunity for public comment. Their actions were timed to extend oil and gas leasing prohibitions well beyond their term in office (perhaps permanently), seek an edge in an upcoming election, or sacrifice OCS leasing in an attempt to placate opponents of another executive decision. More specifically:

In his last month in office, President Obama removed canyon areas of the Atlantic from leasing consideration “for a time period without specific expiration.”

In his last month in office, President Obama removed the Northern Aleutian planning area from leasing consideration “for a time period without specific expiration.”

Two months before the 2020 election, President Trump removed the South Atlantic planning area from leasing consideration through June 30, 2032.

Two months before the 2020 election, President Trump removed the Eastern Gulf of Mexico area from leasing consideration through June 30, 2032.

On March 13 2023, coincident with his approval of theWillow project (North Slope of Alaska), President Biden removed the remainder of the Beaufort Sea from leasing consideration “for a time period without specific expiration.”

In light of the rather cynical abuses of this authority and their potential economic and national security implications, Congress should consider repealing Sec. 12(a) of OCSLA or revising the language to limit the timing, scope, and duration of such withdrawals, and establish a process that prevents the withdraw of lands without fully considering the potential implications.

ENERGYWIRE has reported that the Department of the Interior will publish the legislatively mandated carbon sequestration rule later this year. Given that even close followers of the OCS program were completely unaware of the enabling legislative provisions prior to their enactment, the proposed DOI rule will provide the first opportunity to formally comment.

Within the oil and gas industry and the environmental community, there are considerable differences of opinion about carbon sequestration in general, and more specifically, offshore sequestration. All interested parties are encouraged to submit comments on these important regulations.

Some background information on the sequestration legislation and subsequent actions:

amend the OCS Lands act to authorize “the injection of a carbon dioxide stream to sub-seabed geologic formations for the purpose of long-term carbon sequestration.”

exempt CO2 injection from the restrictions on ocean dumping by stipulating that such injection “shall not be considered to be material (as defined in section 3 of the Marine Protection, Research, and Sanctuaries Act of 1972.” Without this exemption, CO2 streams would clearly be “material,” as defined in 33 U.S.C. 1402, and would be subject to the stringent requirements of that act.

direct that “not later than 1 year after the date of enactment of this Act, the Secretary of the Interior shall promulgate regulations to carry out the amendments made by this section.” (This deadline has been missed, which is rather common for such directives.)

3/29/23: Exxon bid at Sale 259 on 69 nearshore tracts with little oil and gas potential. Once again, this was strictly an oil and gas lease sale and Exxon’s CCS intentions were clear. Nonetheless, the leases were awarded.

Exxon and other companies intend to commercialize carbon sequestration, and Exxon projects an astounding $4 trillion CCS market by 2050. Such a market will of course be dependent on mandates and subsidies, and the costs will ultimately be borne by taxpayers and consumers.

Is it not a bit unsavory and hypocritical for hydrocarbon producers to capitalize on the capture and disposal of emissions associated with the consumption of their products? Perhaps companies that believe oil and gas production is harmful to society should exit the industry, rather than engage in enterprises that sustain it.

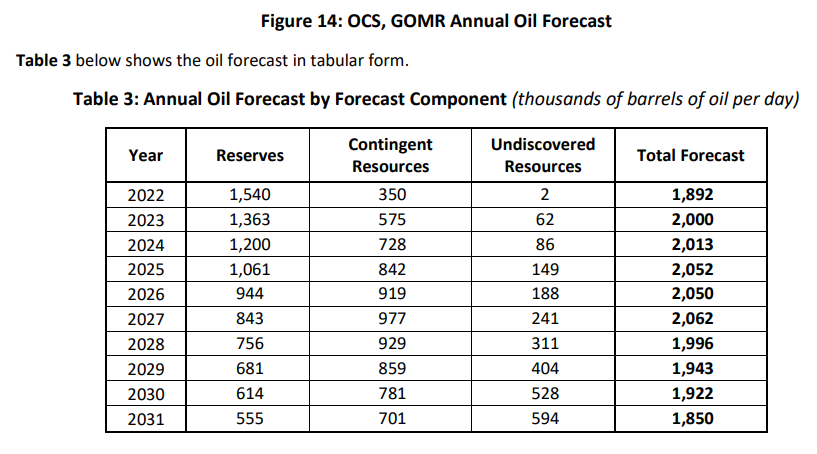

The EIA 2022 figure is spot-on, as it should be given that 10 months of 2022 production data are now in hand. However, BOEM’s 2022 forecast (published in July) missed the mark considerably. (In fairness to BOEM staff, their work was probably completed months before publication pending internal reviews.)

Of greater concern, given the policy implications, is the rosy BOEM forecast for the out-years. Despite historically low levels of leasing and exploratory drilling, BOEM forecasts oil production to exceed 2 million BOPD through 2027 and to remain well above the current (2022) level through 2031 (second table below).

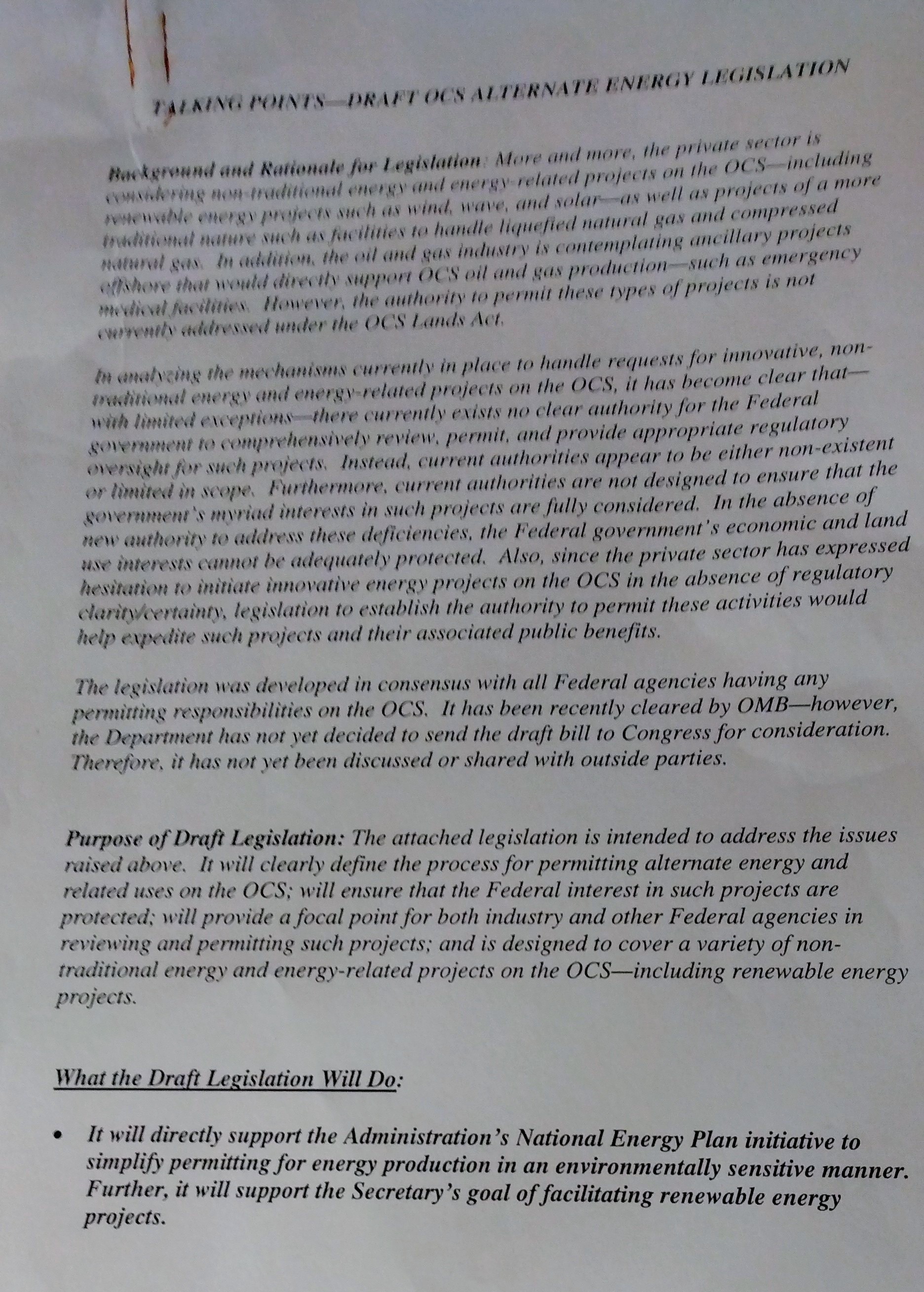

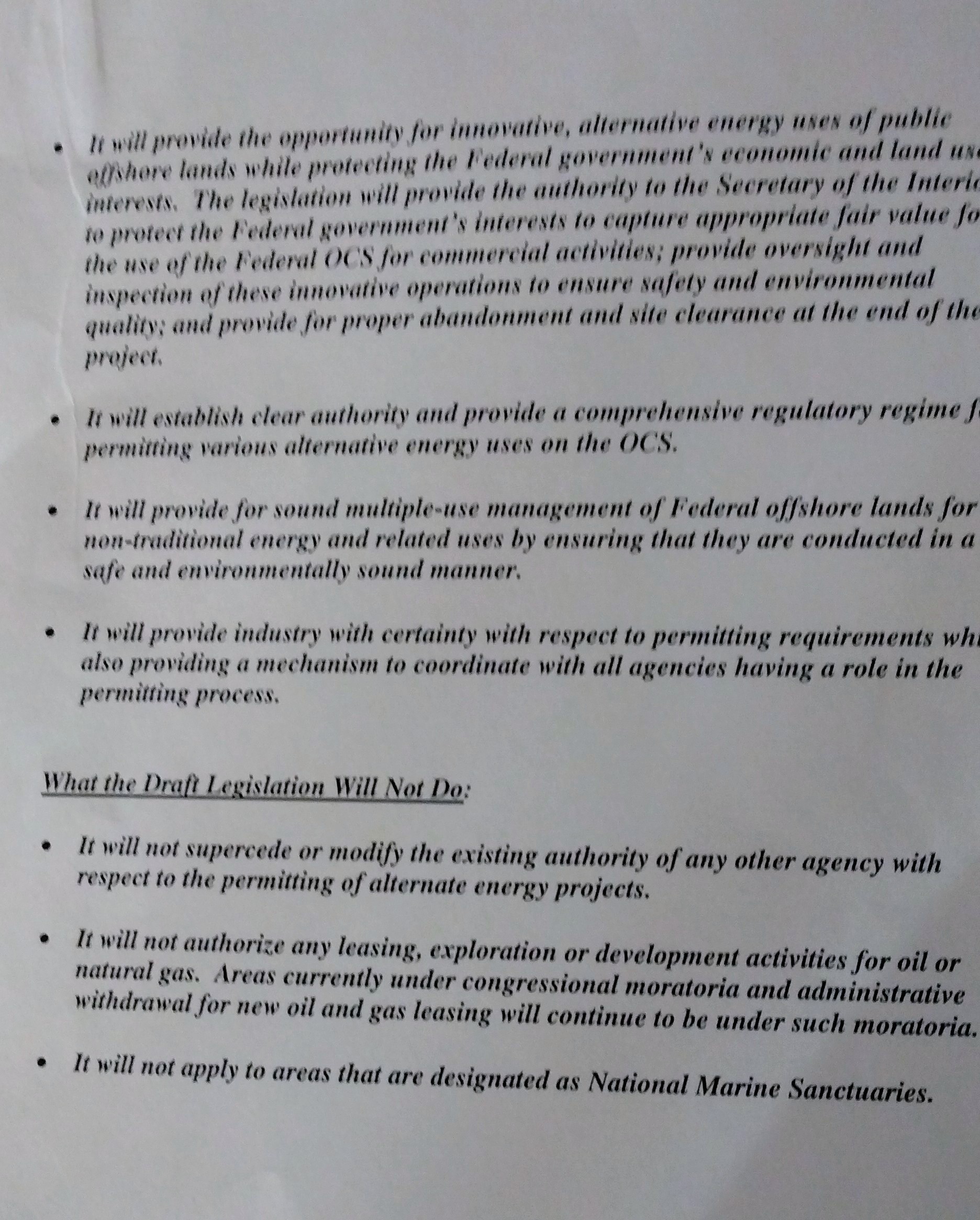

The need for alternate energy/use legislation was obvious to Minerals Management Service (predecessor of BSEE and BOEM) personnel decades ago given the growing interest in renewable energy projects and the reuse of offshore platforms. Twenty years ago, MMS staff took the initiative to draft alternate use amendments to the OCS Lands Act that MMS Director Johnnie Burton and the congressional liaison office worked closely with Congresswoman Barbara Cubin of Wyoming to gain support for the amendments and they were adopted as part of the Energy Policy Act of 2005

Attached below are the talking points used by MMS in briefing congressional staff and other agencies. These talking points were spot-on and have endured the test of time.

Total wants to sit on their wind lease until the next administration (2029). Can they do that?

Posted in energy policy, Offshore Wind, tagged Attentive Energy, BOEM, CEO comments, COP deadline, diligent development, lease cancellation, OCSLA, Total, wind lease on December 3, 2024| Leave a Comment »

Impressive arrogance from the CEO of a foreign company that paid $795 million for a lease (OCS-A 0538) that was worth pennies on the dollar even before the Presidential election:

“Offshore wind, I have decided to put the project on pause” with Trump’s return, Total Chief Executive Officer Patrick Pouyanne said at an energy industry conference in London on Tuesday.

“I said to my team, the project in New York, we’ll see that in four years,” he said. “But the advantage is it’s only for four years.”

Perhaps Mr. Pouyanne thinks Total owns those 84,332 acres in the Atlantic or that they have the right to hold the leased area indefinitely. They do not. The OCS Lands Act calls for diligent development of leases and BOEM has promulgated implementing regulations.

The Total (Attentive Energy) lease was issued on 5/1/2022. Per 30 CFR § 585.235(a)(1), the company must submit a Construction and Operations Plant (COP) no later than 5/1/2027, more than 20 months before the end of the Trump administration. BOEM will have ample time to act on the plan prior to the next administration.

BOEM could also call for progress updates and an earlier COP submittal if there is evidence that the lessee is not moving forward with development plans (as would already seem to be the case given Mr. Pouyanne’s public statements in London).

In the absence of progress in developing the lease, BOEM could seek cancellation (§ 556.1102) for failure to comply with the diligence mandate in OCSLA (556.1102 (a)). Cancellation could also be pursued based on misrepresentations in acquiring the lease (556.1102 (c)) or the threat of unacceptable harm to the environment or national security (556.1102 (d)).

Rather than making rash comments at a public forum in London, perhaps Mr. Pouyanne would have been wise to first meet with energy officials of the new administration early next year. At a minimum, the CEO’s comments will help justify any attempts to cancel the Total (Attentive Energy) lease on diligence grounds.

Read Full Post »