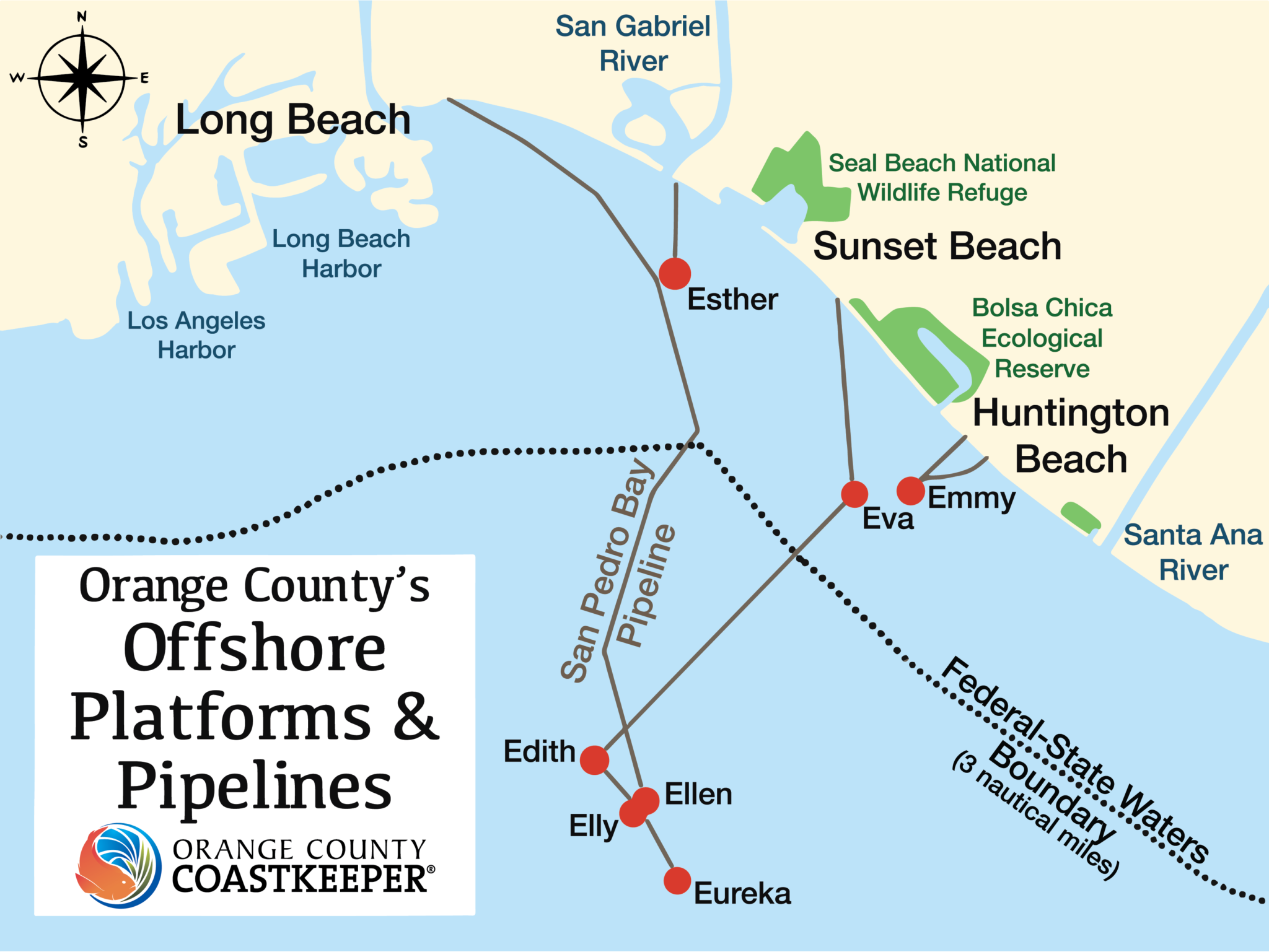

A mile offshore during the big year-end swell (map below). Rigs-to-Rides!

Posted in California, Offshore Energy - General, rigs-to-reefs, Uncategorized, tagged big swell, California, platform Esther, rigs-to-rides, surf on December 31, 2023| Leave a Comment »

Posted in climate, Gulf of Mexico, Offshore Energy - General, tagged 2 million bopd, Gulf of Mexico oil production, no tropical storm impacts on December 29, 2023| Leave a Comment »

EIA reports October production of 1.959 million bopd. September production was revised down from 2.000 to 1.999 million bopd, a very slight but symbolically significant change. Foul play? 😉

For the past 2 years, no tropical storms have significantly impacted Gulf of Mexico production. Don’t expect this to be reported elsewhere 😉

Posted in California, decommissioning, Offshore Energy - General, tagged BSEE, California, decommissioning, partial removal, PEIS, ROD on December 27, 2023| Leave a Comment »

This Santa Barbara Independent article discusses the Record of Decision (ROD) for the Programmatic Environmental Impact Statement on Pacific OCS Decommissioning. A quote from the article regarding BSEE’s support for complete removal of all infrastructure follows:

“It’s great that the federal government finally has a loose game plan for getting oil companies to clean up their rusty messes,” said Miyoko Sakashita, oceans program director at the Center for Biological Diversity.

Apparently the Center for Biological Diversity supports complete removal, the decommissioning alternative that would destroy “the most productive marine habitats per unit area in the world.” How’s that for irony?

Complete removal may be the most politically expedient alternative in California, but it is by far the most environmentally damaging and poses the greatest safety risks. Old disputes about offshore oil and gas production should not be driving decommissioning policy.

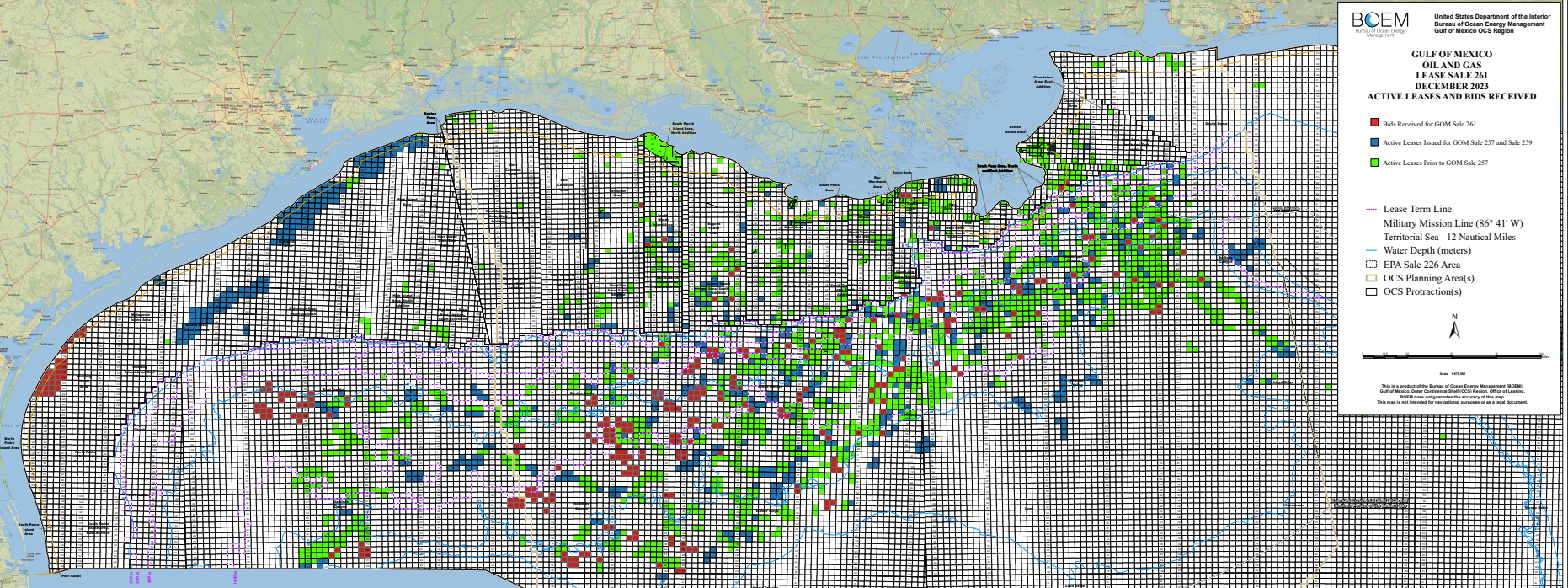

Posted in Gulf of Mexico, Offshore Energy - General, tagged Anadarko, bp, Chevron, Christmas, Equinor, Gulf of Mexico, Hess, Lease Sale 261, Red Willow, Shell, Woodside on December 22, 2023| Leave a Comment »

Holiday greetings to our friends around the world!

Stocking stuffer for that special person! 😉

Posted in Gulf of Mexico, Offshore Energy - General, tagged Chevron, Hess, high bids, Lease Sale 261, top 10, tract evaluation on December 21, 2023| 1 Comment »

It’s always interesting to compare the high bids with the “runner-up” bids on the same tracts. Usually the gap is large and, as indicated in the table below, that is the case with the Sale 261 “top 10.” This tells us that bidding is independent, that tract evaluation is far from an exact science, that information and expert opinions differ, and that companies have different business and bidding strategies.

Particularly interesting in this sale were the tracts that both Hess and Chevron, its future parent, sought to acquire. Chevron and Hess bid against each other on two of the “top 10” tracts, and Hess outbid Chevron by wide margins. Will this affect post-merger relationships? 😉

In a future post, we’ll look at the 14 rejected Sale 259 high bids and the bidding on these tracts in Sale 261.

| block | high bid (million $) | company | 2nd highest bid (million $) | company |

| MC 389 | 25.5 | Anadarko | 1.9 | LLOG |

| GC 188 | 21.0 | Hess | 4.8 | Chevron |

| GC 151 | 18.0 | Hess | 3.0 | Anadarko |

| GC 723 | 17.2 | Anadarko (55%) Chevron (45%) | 2.0 | Equinor |

| GC 116 | 14.0 | Hess | 7.5 | Anadarko |

| GC 722 | 12.0 | Equinor | 1.4 | Chevron (55%) Anadarko (45%) |

| GC 72 | 7.5 | Hess | single bidder | |

| GC 232 | 7.0 | Hess | 1.1 | Chevron |

| GB 701 | 6.7 | Shell | single bidder | |

| KC 210 | 5.3 | Shell | single bidder |

Posted in Gulf of Mexico, Offshore Energy - General, tagged BOEM, Gulf of Mexico, Lease Sale 261 on December 20, 2023| Leave a Comment »

Complete sale statistics will soon be available at BOEM.gov.

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged 5 year leasing plan, Carol Hartgen, Carolita Kallaur on December 20, 2023| Leave a Comment »

As we await Lease Sale 261, Carol Hartgen, my long-time colleague and founder of the 5 year OCS leasing program, voiced astonishment that the new 5 year plan was only for the purpose of scheduling 3 lease sales required by Congress as prerequisites to offshore wind lease auctions. Carol provides some historical context:

I couldn’t believe the release of the final Five Year Program as just a necessity to hold offshore wind sales. Back in 1969, Carolita Kallaur, Joan Davenport and I worked on a 5-year schedule based on the supply and demand needs of the nation. That approach, which developed into the elaborate process in the OCS Lands Act and the passage of the National Environmental Policy Act, is a thing of the past. Over.those 50 plus years, politics from both sides of the aisle always drove the changes

Posted in Gulf of Mexico, Offshore Energy - General, tagged presale statistics, sale 259 comparison, sale 261 on December 19, 2023| Leave a Comment »

| 261 (presale) | 259 | |

| tracts receiving bids | 311 | 313 |

| no. of bids | 352 | 353 |

| companies bidding | 20 | 32 |

| <400 m water depth | 52 | 107 |

| >400 m water depth | 259 | 206 |

Comments on the preliminary stats:

Posted in California, decommissioning, Offshore Energy - General, tagged California, Decommissioning EIS, Hogan and Houchin, Milton Love, partial removal, platform habitat, reef legislation on December 19, 2023| Leave a Comment »

“These platforms are habitat for millions of animals. My opinion is that it’s immoral to kill huge numbers of animals in any kind of habitat.”

Dr. Milton Love, UCSB marine biologist

Inexplicably, BSEE’s Record of Decision (ROD) for the Programmatic Environmental Impact Statement on Pacific OCS Decommissioning (EIS cost: $1,604,056) endorses such habitat destruction by designating the most environmentally harmful, unsafe, punitive, and costly alternative as the “preferred alternative.”

Alternative 1 (the preferred alternative) calls for “the complete removal of platforms, topside, conductors, the platform jackets to at least 4.6 m (15 ft) below the mud line, and the complete removal of pipelines, power cables, and other subsea infrastructure (i.e., wells, obstructions, and facilities).”

Ironically, the ROD correctly acknowledges that alternative 2 (partial removal) is environmentally preferable. So what drove the decision to select the alternative that destroys “the most productive marine habitats per unit area in the world?” Was there pressure to choose the alternative that is most punitive to an industry that is despised by California activists? If so, their schadenfreude is certain to be delayed by administrative and legal challenges that draw further attention to the social costs and environmental damage associated with “complete removal.”

In 2020, BOEM estimated the total cost of decommissioning the 23 Federal offshore platforms at $1.7 billion, and today’s real costs are likely to be much higher. Also, keep in mind that some thorny decommissioning liability issues remain to be resolved, particularly with regard to Platforms Hogan and Houchin.

The decommissioning costs for Hogan and Houchin are estimated by BOEM at $85.6 million, even though the cost of completing removing Platform Holly (single platform in similar water depth in CA State waters) may reach $475 million. Per the BOEM data, there is no collateral, supplemental financial assurance, or third party guarantee that could defray the Hogan and Houchin costs. The extent to which prior lessees could be held accountable is questionable given that the lease was assigned to (now bankrupt) Signal Hill in 1991, well before the predecessor liability language was added to the MMS bonding rule. Irregularities in the management of Signal Hill’s Abandonment Escrow Account for Hogan and Houchin further complicate the liability issues.

The path for timely facility decommissioning with the least environmental damage and safety risk has two essential elements:

Absent those steps, the noise will continue, the platforms will remain in place, and the best outcome for all parties will not be achieved.

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, Offshore Wind, tagged 5 year leasing plan, DOI, fewest lease sales on December 18, 2023| Leave a Comment »

The announcement boasts about “the fewest oil and gas lease sales in history” while seemingly apologizing for holding any sales at all.

Consistent with the requirements of the Inflation Reduction Act (IRA) concerning offshore conventional and renewable energy leasing, the Department of the Interior today published the final 2024–2029 National Outer Continental Shelf Oil and Gas Leasing Program (Program) with the fewest oil and gas lease sales in history.

These three lease sales are the minimum number that will enable the Interior Department’s offshore wind energy program to continue issuing leases in a way that will ensure continued progress towards the Administration’s goal of 30 gigawatts of offshore wind by 2030.