The oil patch is known for booms, busts, mergers, and acquisitions. Hess is now among the once important offshore operators that no longer exist as separate companies. Others include Amoco, Arco, Texaco, Getty, Gulf, Unocal, Sun, Anadarko, BHP, Mobil, Phillips, Noble Energy, Pennzoil, Kerr-McGee, Superior, Nexen, and Newfield.

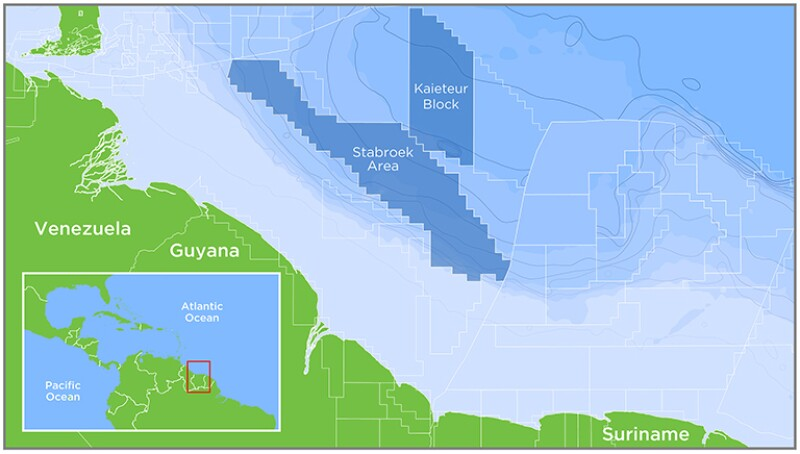

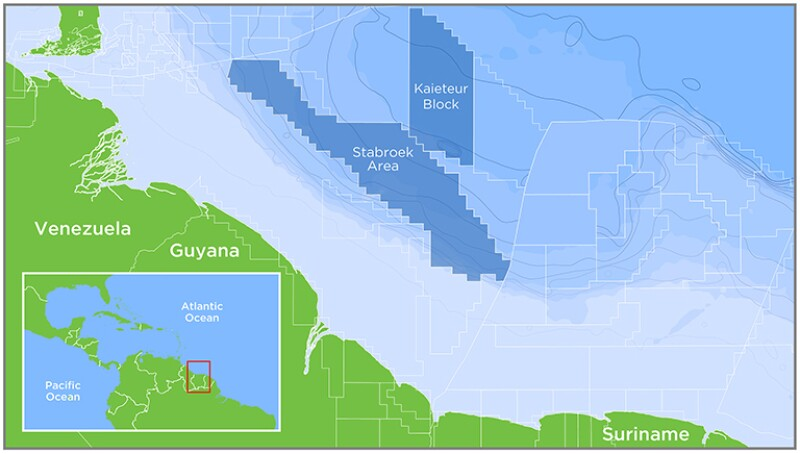

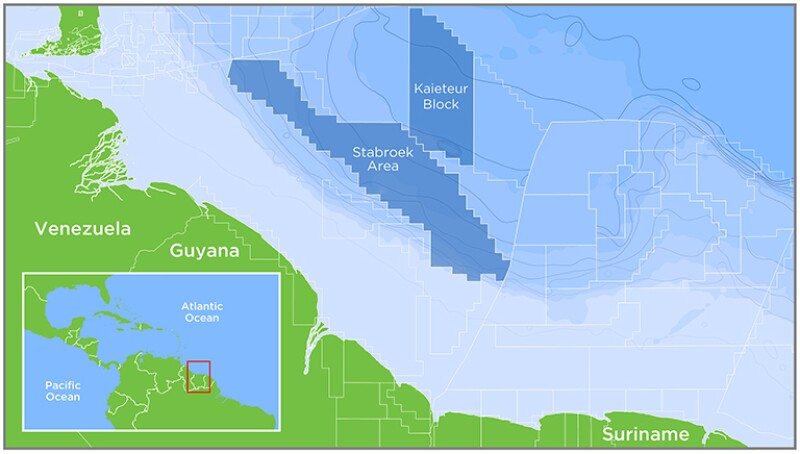

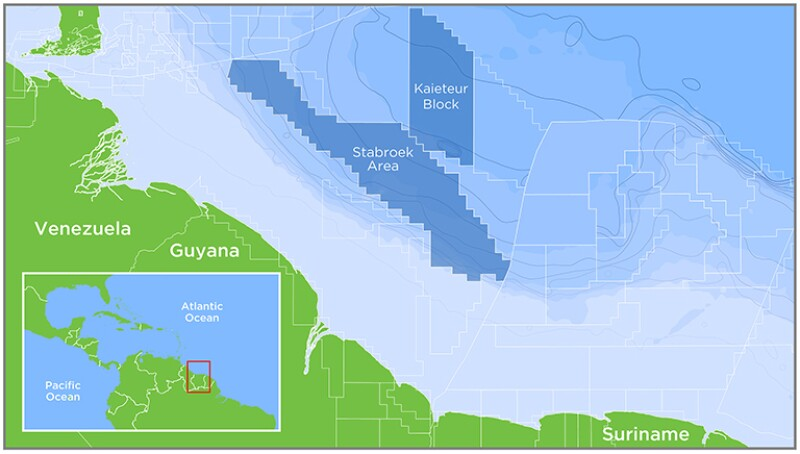

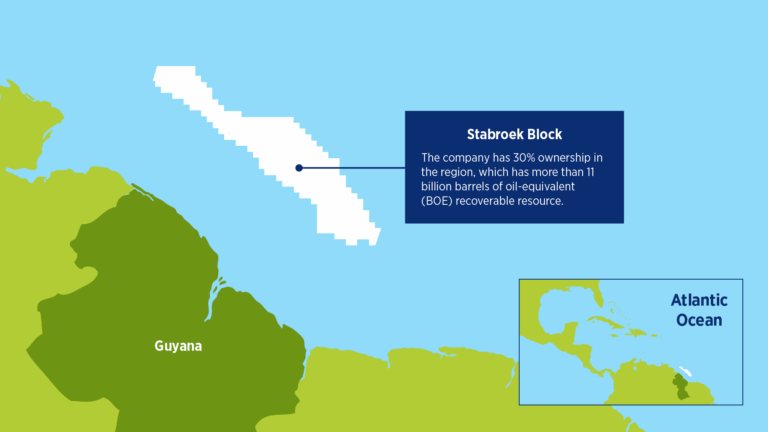

Hess would probably not have been a Chevron target had they not taken a chance in 2014 when they obtained a 30% position in Exxon’s Stabroek block offshore Guyana. The rest is history, and Stabroek is now the world’s most prized offshore block. Hess had other nice assets in the Gulf, Bakken Shale, and elsewhere, but Stabroek was Chevron’s primary target.

Paying the price for the Hess acquisition are up to 8,000 employees who will be axed by the end of 2026, starting with 575 cuts at the former Hess Tower in Houston on September 26 and matched reductions in Texas, California and North Dakota. The cuts also have to be disappointing to the Federal, Texas and North Dakota governments, given their strong support for oil and gas production. Mass layoffs don’t equate to energy dominance.

Why is the loss of Hess is significant:

- Hess was a safety compliance leader in both 2023 and 2024.

- Hess was an active participant in pre-merger lease sales.

- The combined company is unlikely to be greater than the sum of the parts in terms of US lease acquisition, exploration, and development.

- Combining companies limits the diversity of geological assessments and exploration strategies.

- Consolidation limits participation on committees engaged in assessing technology and developing standards. Declining industry participation in these activities, which are critical to offshore safety, has been a historical concern of OCS program leadership.

When the merger was announced, Chevron’s CEO Mike Wirth was quoted as saying “We’ve got too many CEOs per BOE, so consolidation is natural.” That comment makes sense from the perspective of an acquiring CEO. Employees of the companies being acquired have a somewhat different view. They would prefer increasing exploration and production rather than reducing employees.