Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectivelychallenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

If Beacon and HEQ are willing sellers of their majority share in the impressive Shenandoah field, as appears to be the case (per Reuters), the big dogs are interested in buying. And why wouldn’t they be? Production began last July and the targeted rate of 100,000 bopd has already been achieved from just four phase-one wells.

Reuters reports that Total, Shell, BP, Repsol, and Chevron are interested in Beacon and HEQ’s 51% stake. More about Shenandoah:

located in Walker Ridge blocks 51, 52, and 53

~150 miles off the coast of Louisiana

floating production unit (FPU) in 5800′ of water in WR block 52

Investment companies like Beacon (owned by Blackstone) are positive, and increasingly necessary, contributors to the offshore program. These companies bring capital and new exploration strategies that increase development and production. They must, of course, be committed to safety excellence, which seems to be the case for Beacon.

It’s noteworthy that Anadarko and Conoco Phillips, Shenandoah’s major original partners holding 33% and 30% interest respectively, withdrew from the project in 2018 citing unsatisfactory appraisal results and weak commodity prices. Evaluation mistakes like this are common, which is why broad and diverse industry participation is needed. With mergers reducing the number of US majors (remember Amoco, Arco, Sun, Texaco, Getty, Mobil, Phillips, Marathon, Unocal, Superior, Hess, etc.), investment companies play an increasingly important role in OCS development.

Shenandoah, WR 51, 52, 53 (center blocks); green=active leases prior to Sale 261; blue=leased issued after Sale 261

red=blocks receiving bids at BBG2; blue=BBG1 and Sale 261 leases; green=active leases issued prior to Sale 261

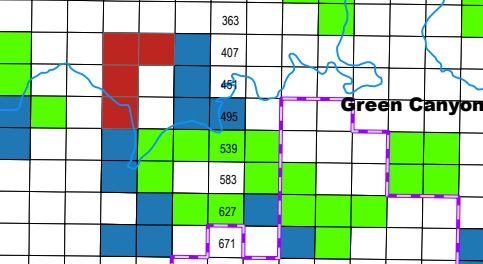

Although bidding at Sale BBG2 was rather subdued, Gulf heavyweights BP, Chevron, Shell, and Oxy/Anadarko, along with increasingly important Woodside Energy, competed for the 4 red blocks in the Green Canyon area (map above and table below). These elephant hunters presumably see excellent Paleogene (Wilcox) prospectivity in those blocks.

17 of the sale’s 38 bids (45%) and $32.8 milion of the sale’s $47 million in high bids (70%) were for these 4 blocks. BP’s $21 million bid for GC 404 was by far the sale’s highest bid.

Green Canyon Block No.

No. of bidders

High Bidder

Bid

404

5

BP

$21,009,990

405

2

BP

$885,99

448

5

Chevron

$4,967,067

492

5

Chevron

$5,887,188

At this time, the high costs and technical complexities (e.g. deepwaterand high pressure/high temperature reservoirs) limit Wilcox development to major oil companies and well financed, technically savvy independents. Expect some of the international majors that did not participate in BBG2 to acquire lease interest at a later date, which will again raise questions about the merits of joint bidding restrictions.

From AAPG graphic-Wilcox trend map. Eastern area can be subdivided into an outboard and inboard trend, with wells in the latter area showing variable thickness due to salt tectonics contemporaneous with deposition (From Zarra et al. 2019’s AAPG Search and Discovery article).

Imbedded below is a good presentation on the Paleogene Wilcox by Dr. Mike Sweet, Univ. of Texas:

Although no one was expecting a barnburner only 3 months after the previous sale, BBG2 was historically weak for a Gulf-wide sale. The table below compares BBG2 with the previous 4 Gulf sales, none of which were particularly impressive.

However, the sale was not without highlights. There was some spirited bidding for tracts in the Green Canyon area. BP’s bid was the highest of 5 for GC Block 404. BP bid $21 million for the block, 45% of the high bids sum for the entire sale. The BP bid was also $20 million higher than the next highest bid for that tract (ouch!).

Also interesting was Chevron edging Shell $5,887,188.00 to $5,501,240.00 to acquire GC Block 492.

Sale No.

257

259

261

BBG1

BBG2

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

3/11/2026

companies participating

33

32

26

30

13

total bids

2233

2842

3161

219

38

tracts receiving bids

2143

2442

2751

181

25

sum of all bids $millions

198.5

309.8

441.9

371.9

69.9

sum of high bids ($millions)

101.7

263.8

382.2

279.4

47.0

highest bid company block

$10,001,252 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

$18,592,086 Chevron KC 25

$21,009,990 bp GC 404

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

50 bp 61.0

6 Anadarko (Oxy) 4.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

61.0 bp

22.6 bp

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

14-Murphy

5-LLOG

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

For historical comparison purposes, Gulf Sale 206 drew $3.7 billion ($5.6 billion in today’s dollars) in 2008. Twenty-siz sales between 1972 and 2013 garnered more than $1 billion in high bids.

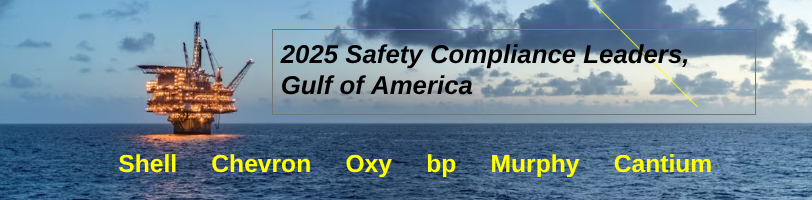

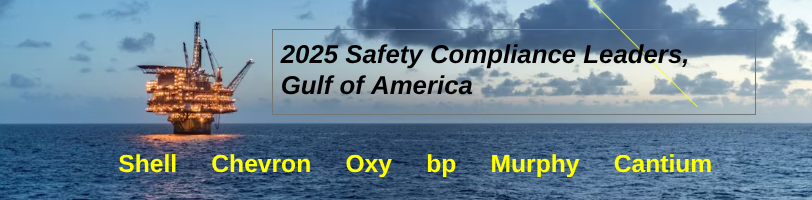

The 2025 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 5 facility inspections (0.20 INCs/facility inspection). This is a higher standard (fewer INCs) than in previous years.

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2025, there were on average 3.2 inspections for every facility inspection.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Shell

3

8

1

12

231

0.05

557

0.02

Chevron

10

8

0

18

260

0.07

772

0.02

Oxy

2

6

1

9

133

0.07

325

0.03

BP

8

2

0

10

122

0.08

304

0.03

Murphy

6

2

0

8

70

0.11

177

0.05

Cantium

5

7

4

16

121

0.13

488

0.03

Gulf-wide 2025

815

445

84

1344

3179

0.42

10218

0.13

Gulf-wide 2024

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2025, there were on average 3.2 inspections for every facility inspection

Criteria: This ranking is based solely on BSEE’s published compliance data. The absence of timely public information on safety incidents (e.g. injuries, fires, pollution, gas releases, property damage) precludes inclusion of these data. Although Panel Investigations are conducted for fatalities, serious injuries, and significant pollution events, the last panel report was for an incident on 3/25/2022, and no information is available for any ongoing investigations. BSEE District offices investigate the more significant incidents that don’t qualify for panel investigations. These District Investigation reports are more timely, but some are not issued within 90 days of the incident. The District reports will be reviewed later in the year. Note that there were no occupational fatalities in 2025.

Observations:

The overall inspection and INC results for 2025 were similar to those for 2024.

The top companies performed better in 2025 than in 2024. In 2024, only 2 companies had INC/facility inspection ratios of <0.10 and only 3 had ratios <0.15. In 2025, all 6 of the performance leaders had ratios <0.15.

Shell’s total INCs and INCs/facility inspection decreased by 73% and 78% respectively vs. 2024

Cantium, which operates 85 shallow water platforms, has demonstrated that a shelf operator can be an outstanding safety performer. Cantium’s total INCs and INCs/facility inspection decreased by 50% vs. 2024

Should fewer inspections be conducted at facilities that have such low INC rates? On the one hand, fewer inspections would reduce regulatory costs and transportation risks. On the other hand, there are benefits from BSEE inspection visits besides compliance enforcement. These include direct communication with offshore workers (including contractors) regarding regulatory policies and safety practices, witnessing safety tests, evaluating new technology, and assessing management system implementation and corporate culture at the facility level.

Absent specific details on the violations, no attempt was made to weight the INCs. Although shut-in INCs are generally considered to be more significant than warnings, that is not always the case. For example, a component shut-in INC for a safety device that is marginally out of tolerance and is corrected on the spot may be less serious than a warning that is indicative of structural deterioration, poor maintenance, or organizational shortcomings.

Not meeting one of the activity level requirements, but nonetheless noteworthy, were the compliance records of LLOG and BOE Exploration & Production (younger than and unrelated to the BOE blog 😀). See their impressive results below:

Will the oil and gas lease sale boldly named Big Beautiful Gulf 1 (BBG1) live up to its grand name? Given the more favorable lease terms and the 2 year gap since the last sale, BBG1 should surpass the previous 3 sales (table below). Questions:

Which majors will be the most active bidders? Chevron? Shell? BP? Oxy/Anadarko?

Will former Gulf of Mexico stalwarts Exxon and Conoco Phillips participate for the first time in years? Probably not, but US super-majors should participate in the US offshore program.

How many companies will submit bids? Would like that to be a number >35.

How many tracts will receive bids? A number >300 would be very encouraging.

Will the total high bids exceed $400 million?

Will we see an increase in shelf interest?

Which independents will be the most active?

After the not-so-clever carbon disposal acquisitions in the last 3 sales, will the number of carbon disposal bids be zero? For the first time ever, the Federal government felt compelled to stipulate the obvious (see the proposed notice for OCS Sale 262) – that an Oil and Gas Lease Sale is only for oil and gas exploration and development.

See the summary data below for the last 3 Gulf lease sales. We’ll fill in the blanks next week.

Sale No.

257

259

261

BBG1

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

companies participating

33

32

26

total bids

2233

2842

3161

tracts receiving bids

2143

2442

2751

sum of all bids $millions

198.5

309.8

441.9

sum of high bids ($millions)

101.7

263.8

382.2

highest bid company block

$10,001,252.00 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

Every deepwater platform installed since Feb. 2018, when Chevron installed its Big Foot tension leg platform (TLP), has been a Floating Production Unit (aka FPU or production semisubmersible). During that period, no new SPARs, FPSOs, or TLPs were installed.

The list (below) of these simpler, safer, greener FPUs has grown by two with the initiation of production at Shenandoah and Salamanca. Note the water depth range from 3725 to 8600 ft.

platform

operator

water depth (ft)

first production

Appomattox

Shell

7400

May 2019

King’s Quay

Murphy

3725

April 2022

Vito

Shell

4050

Feb 2023

Argos

bp

4440

April 2023

Anchor

Chevron

4600

Aug 2024

Whale

Shell

8600

Jan 2025

Shenandoah

Beacon

5840

July 2025

Salamanca

LLOG

6405

Sept 2025

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades is facilitatihg production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded in this post.)

All of the operators note the cost-saving similarities in their FPU designs. For example, Vito and Whale are very much the same despite the 4550′ difference in water depth.

The latest Baker Hughes Rig Count Report shows only 10 rigs actively drilling in the Gulf. All are at deepwater locations – 7 in the Mississippi Canyon area, 2 in Green Canyon, and 1 in Alaminos Canyon. Per the BSEE borehole file, Shell accounts for most of the current MS Canyon wells and the Alaminous Canyon well. Beacon is also drilling in the MS Canyon, and the Green Canyon well appears to be a Chevron operation.

Only Anadarko/Oxy, Beacon/BOE, BP, Chevron/Hess, Shell, and Talos have spudded deepwater exploratory wells in 2025 YTD. Arena and Cantium are the only shelf drillers – all development wells.

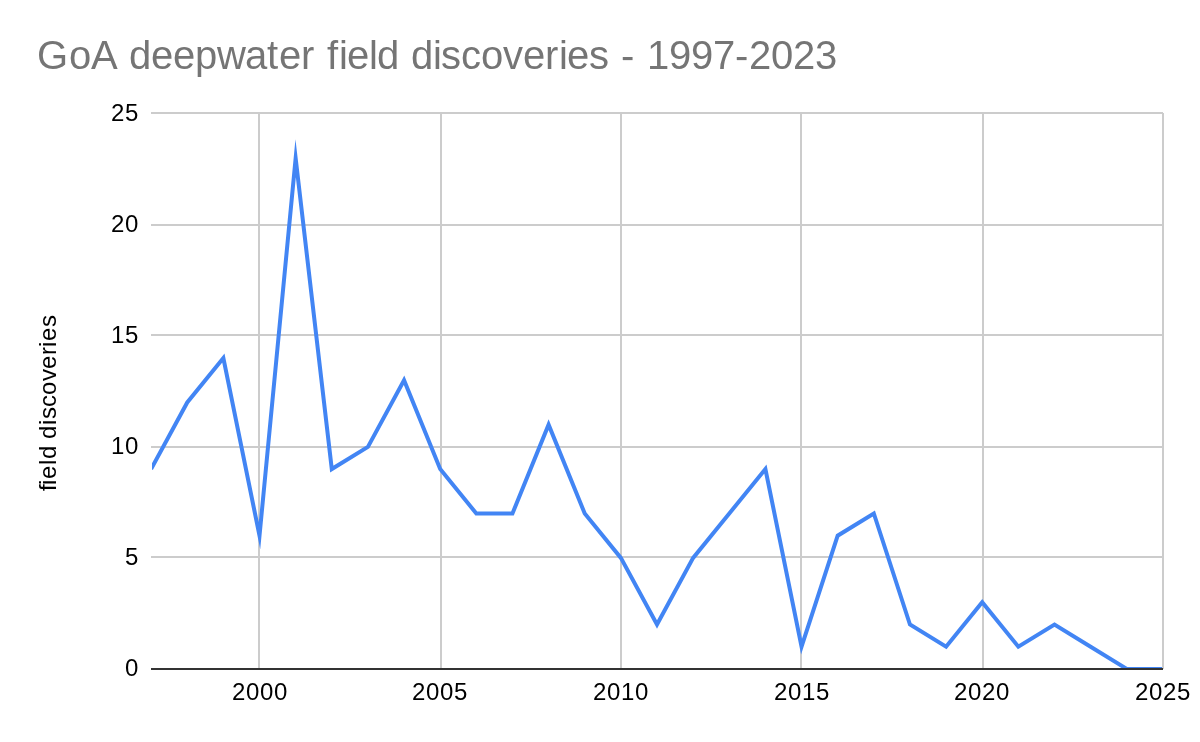

Technological advances and extensions of past discoveries have sustained Gulf production, but declines are certain over the longer term if drilling activity doesn’t increase. Oil price uncertainty is an issue, but that’s always the case. Semiannual lease sales are now legislatively required and the terms will be attractive, so those issues are off the table. Let’s see what the bidding looks like at the upcoming sale.

The decline in deepwater discoveries (BOEM data below) is particularly discouraging. Per BOEM, the last deepwater field discovery was in March 2023.

Restart seems likely for decommissioning financial assurance rule

Posted in Regulation, decommissioning, energy policy, tagged Chevron, Shell, decommissioning, BOEM, API, financial assurance, comments, NEFSA, proposed regulation on May 18, 2026| Leave a Comment »

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectively challenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

Lastly, kudos to the New England Fisherman’s Stewardship Association for raising the concern about financial assurance for decommissioning offshore wind facilities

Read Full Post »