Lars Herbst saw this “beauty” while sitting at a rooftop “establishment” in Pensacola. Reminded him of our temporary Pensacola office and Destin Dome drilling. Lars had visions of returning to work as Pensacola District Manager! 😉

Upon returning to his senses, Lars reports that it’s the Borr jack-up rig Odin purchased from Noble’s fleet. The rig was brought from Mexico to Pensacola for modifications, and will be under contract to Cantium to drill in the GOA, but not the Eastern GOA!

The 2025 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 5 facility inspections (0.20 INCs/facility inspection). This is a higher standard (fewer INCs) than in previous years.

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2025, there were on average 3.2 inspections for every facility inspection.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Shell

3

8

1

12

231

0.05

557

0.02

Chevron

10

8

0

18

260

0.07

772

0.02

Oxy

2

6

1

9

133

0.07

325

0.03

BP

8

2

0

10

122

0.08

304

0.03

Murphy

6

2

0

8

70

0.11

177

0.05

Cantium

5

7

4

16

121

0.13

488

0.03

Gulf-wide 2025

815

445

84

1344

3179

0.42

10218

0.13

Gulf-wide 2024

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2025, there were on average 3.2 inspections for every facility inspection

Criteria: This ranking is based solely on BSEE’s published compliance data. The absence of timely public information on safety incidents (e.g. injuries, fires, pollution, gas releases, property damage) precludes inclusion of these data. Although Panel Investigations are conducted for fatalities, serious injuries, and significant pollution events, the last panel report was for an incident on 3/25/2022, and no information is available for any ongoing investigations. BSEE District offices investigate the more significant incidents that don’t qualify for panel investigations. These District Investigation reports are more timely, but some are not issued within 90 days of the incident. The District reports will be reviewed later in the year. Note that there were no occupational fatalities in 2025.

Observations:

The overall inspection and INC results for 2025 were similar to those for 2024.

The top companies performed better in 2025 than in 2024. In 2024, only 2 companies had INC/facility inspection ratios of <0.10 and only 3 had ratios <0.15. In 2025, all 6 of the performance leaders had ratios <0.15.

Shell’s total INCs and INCs/facility inspection decreased by 73% and 78% respectively vs. 2024

Cantium, which operates 85 shallow water platforms, has demonstrated that a shelf operator can be an outstanding safety performer. Cantium’s total INCs and INCs/facility inspection decreased by 50% vs. 2024

Should fewer inspections be conducted at facilities that have such low INC rates? On the one hand, fewer inspections would reduce regulatory costs and transportation risks. On the other hand, there are benefits from BSEE inspection visits besides compliance enforcement. These include direct communication with offshore workers (including contractors) regarding regulatory policies and safety practices, witnessing safety tests, evaluating new technology, and assessing management system implementation and corporate culture at the facility level.

Absent specific details on the violations, no attempt was made to weight the INCs. Although shut-in INCs are generally considered to be more significant than warnings, that is not always the case. For example, a component shut-in INC for a safety device that is marginally out of tolerance and is corrected on the spot may be less serious than a warning that is indicative of structural deterioration, poor maintenance, or organizational shortcomings.

Not meeting one of the activity level requirements, but nonetheless noteworthy, were the compliance records of LLOG and BOE Exploration & Production (younger than and unrelated to the BOE blog 😀). See their impressive results below:

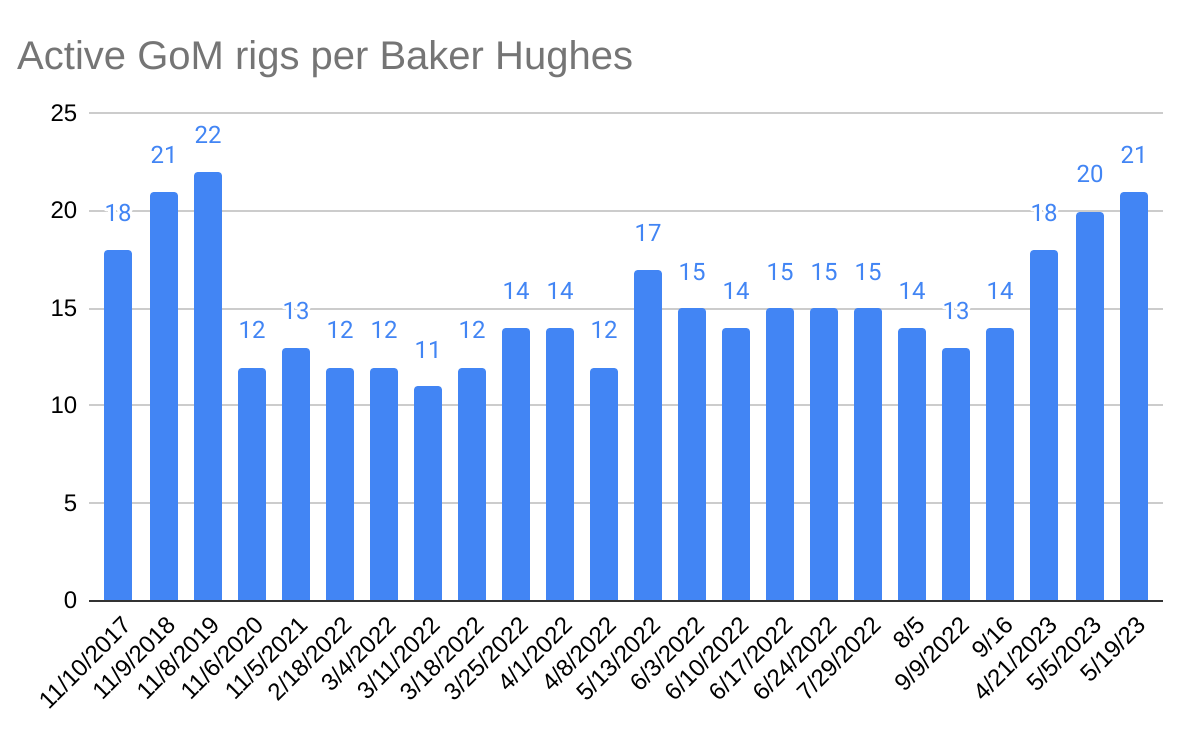

The latest Baker Hughes Rig Count Report shows only 10 rigs actively drilling in the Gulf. All are at deepwater locations – 7 in the Mississippi Canyon area, 2 in Green Canyon, and 1 in Alaminos Canyon. Per the BSEE borehole file, Shell accounts for most of the current MS Canyon wells and the Alaminous Canyon well. Beacon is also drilling in the MS Canyon, and the Green Canyon well appears to be a Chevron operation.

Only Anadarko/Oxy, Beacon/BOE, BP, Chevron/Hess, Shell, and Talos have spudded deepwater exploratory wells in 2025 YTD. Arena and Cantium are the only shelf drillers – all development wells.

Technological advances and extensions of past discoveries have sustained Gulf production, but declines are certain over the longer term if drilling activity doesn’t increase. Oil price uncertainty is an issue, but that’s always the case. Semiannual lease sales are now legislatively required and the terms will be attractive, so those issues are off the table. Let’s see what the bidding looks like at the upcoming sale.

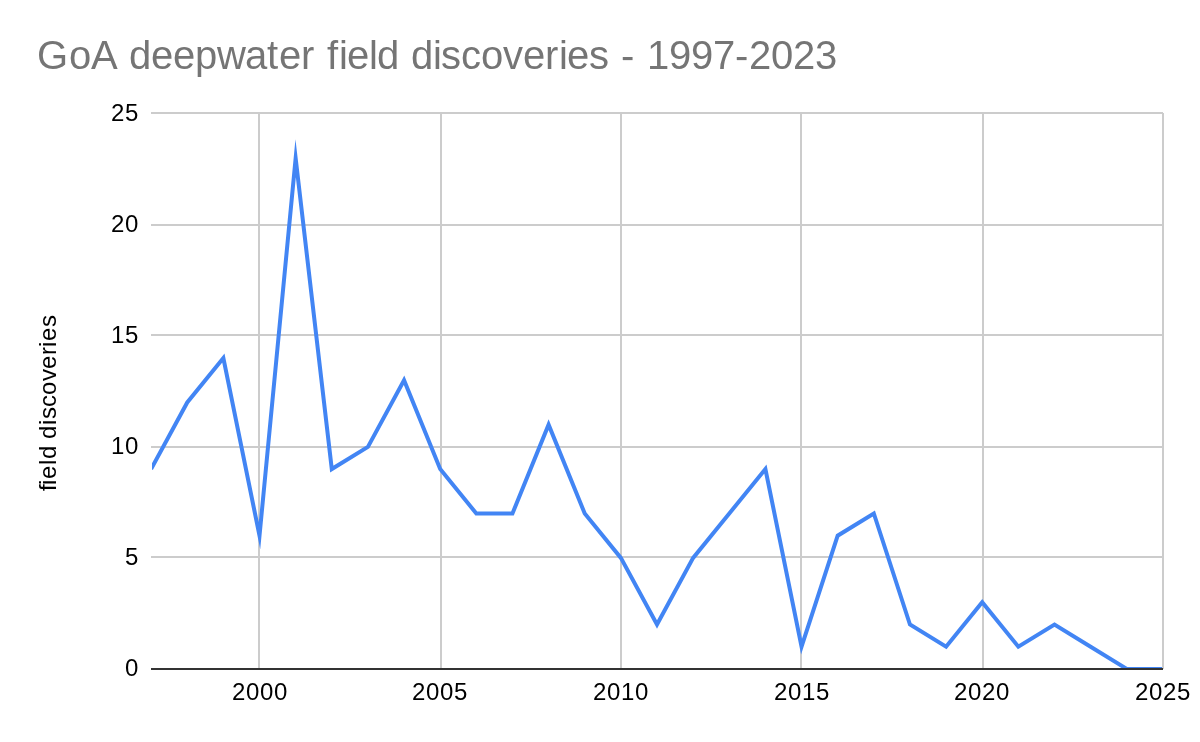

The decline in deepwater discoveries (BOEM data below) is particularly discouraging. Per BOEM, the last deepwater field discovery was in March 2023.

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

A post from last March discussed the high and seemingly unfair royalty and rental rates for new leases in the shallow waters of the Gulf of Mexico shelf. A 50% increase in the shelf royalty rate for lease sales 259 and 261 combined with rather punitive rental rates have likely contributed to the sharp decline in bidding for shelf lease blocks (see table below).

This decline in shelf bidding is unfortunate because the smaller companies that operate in the shallow waters of the Gulf are critical to sustaining the production infrastructure. These companies are also significant producers of environmentally favorable nonassociated (gas-well) natural gas.

lease sale

shelf blocks with bids (excluding CCS bids)

sum of high shelf bids ($million, excluding CCS bids)

BOEM has completed their evaluation of the Sale 261 shelf bids (see below). Each of these blocks received only a single bid, and every bid was accepted. Ironically, the invalid CCS bids for blocks that have no oil and gas value, were the first to be accepted. This was also the case for Sales 257 and 259.

Company

Block

high bid ($) per acre ($)

date accepted

Byron

SM 60

128,750 25.75

2/2

Byron

SM 70

182,235 33.32

2/20

Cantium

GI 35

125,000 25.00

2/20

Cantium

GI 36

125,000 25.00

2/20

Cantium

MP 314

125,000 25.00

3/12

Cantium

SP 63

125,000 25.00

3/12

Arena

EI 231

135,000 27.18

2/20

Arena

EI 277

135,000 27.18

2/20

Arena

EI 281

135,000 27.18

2/20

Arena

EI 340

135,000 27.18

2/20

Arena

EI 343

135,000 27.18

2/20

Arena

WD 119

135,000 26.75

3/12

Focus

V 152

121,152 25.16

2/20

Repsol

36 CCS bids

187,200 (1) 32.50

1/23

(1) All of the Repsol bids were $32.50/ac. Total bids varied by block size, but were $187,200 for the 5760 acre blocks.

Suggestions:

Seek a legislative fix to the Inflation Reduction Act😉 provision that established a 1/6 royalty rate floor for all OCS leases (formerly the royalty rate was 1/8 for leases on the shelf).

In the interim, administratively lower the royalty for shelf leases to 1/6 (from 18 3/4%).

For future oil and gas lease sales, accept all high bids that exceed the specified minimum bid (currently $25/ac for the shelf). The Gulf of Mexico shelf has been extensively explored and developed for 70 years. While prospects remain, they are generally marginal as evidenced by the recent lease sale results. Fair market value is what any company is willing to bid (above the specified minimum).

Focus on assuring that lease purchasers are technically qualified to minimize safety risks, and that financial assurance for decommissioning (for new and existing leases owned by the high bidder) has been fully addressed.

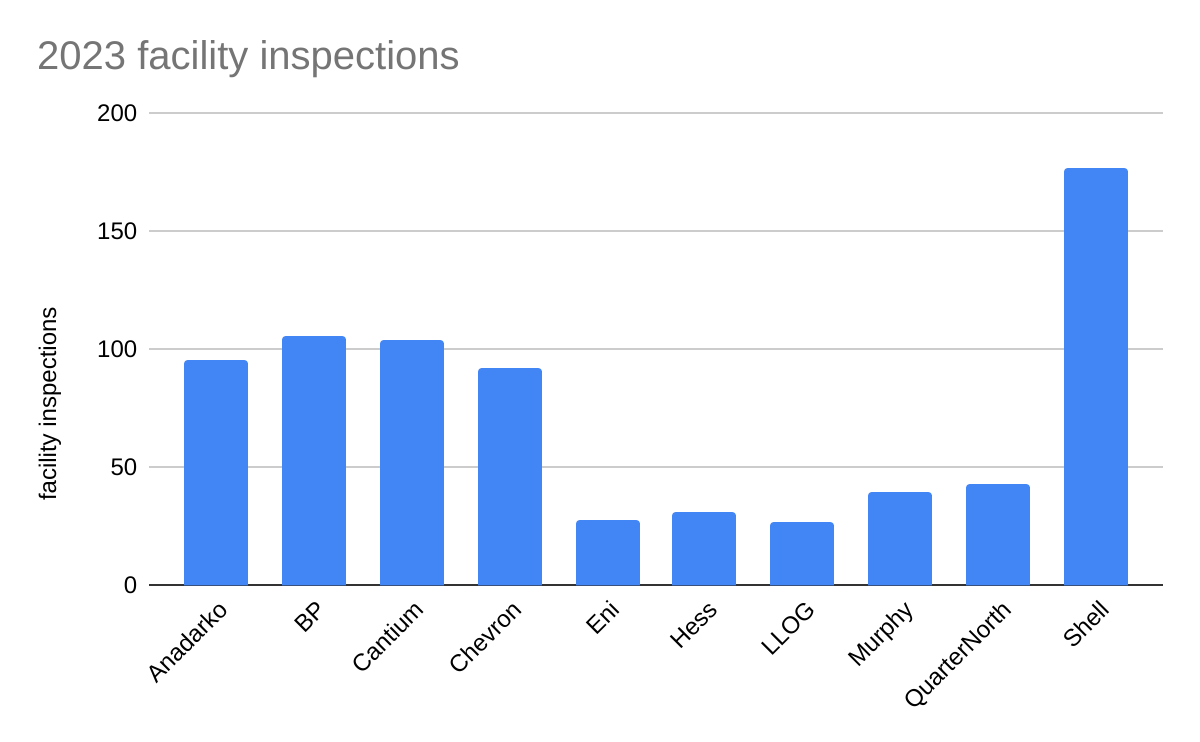

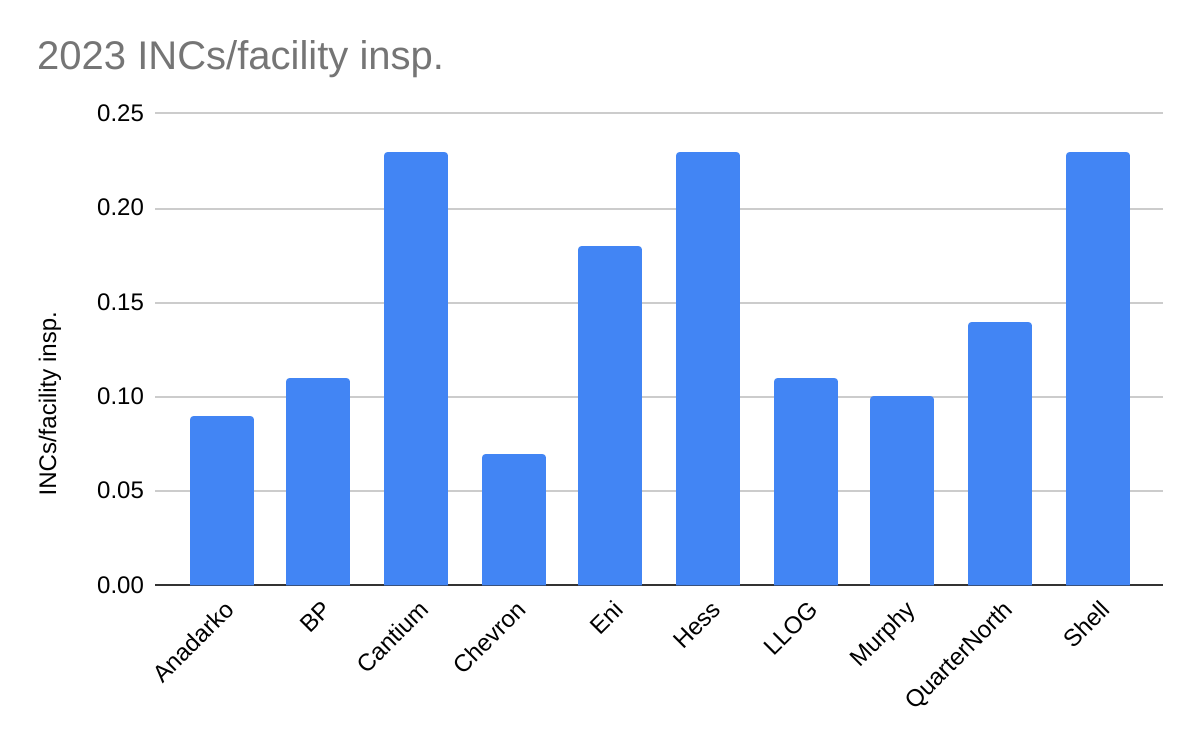

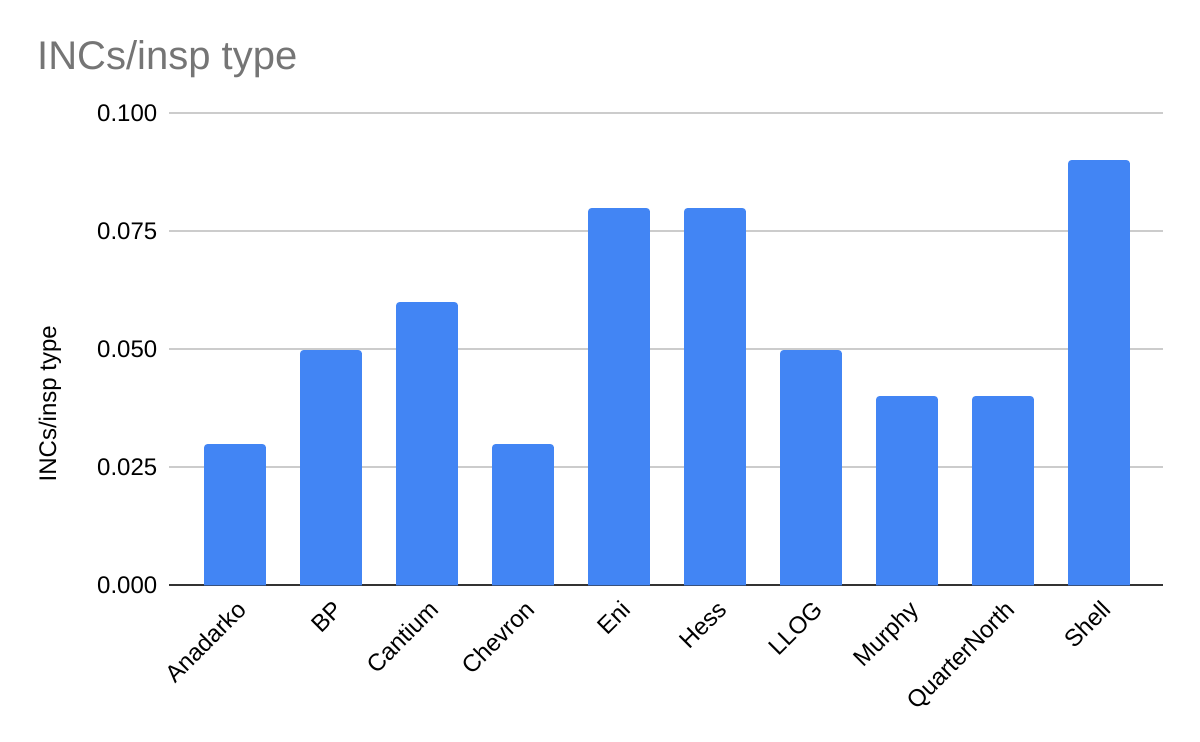

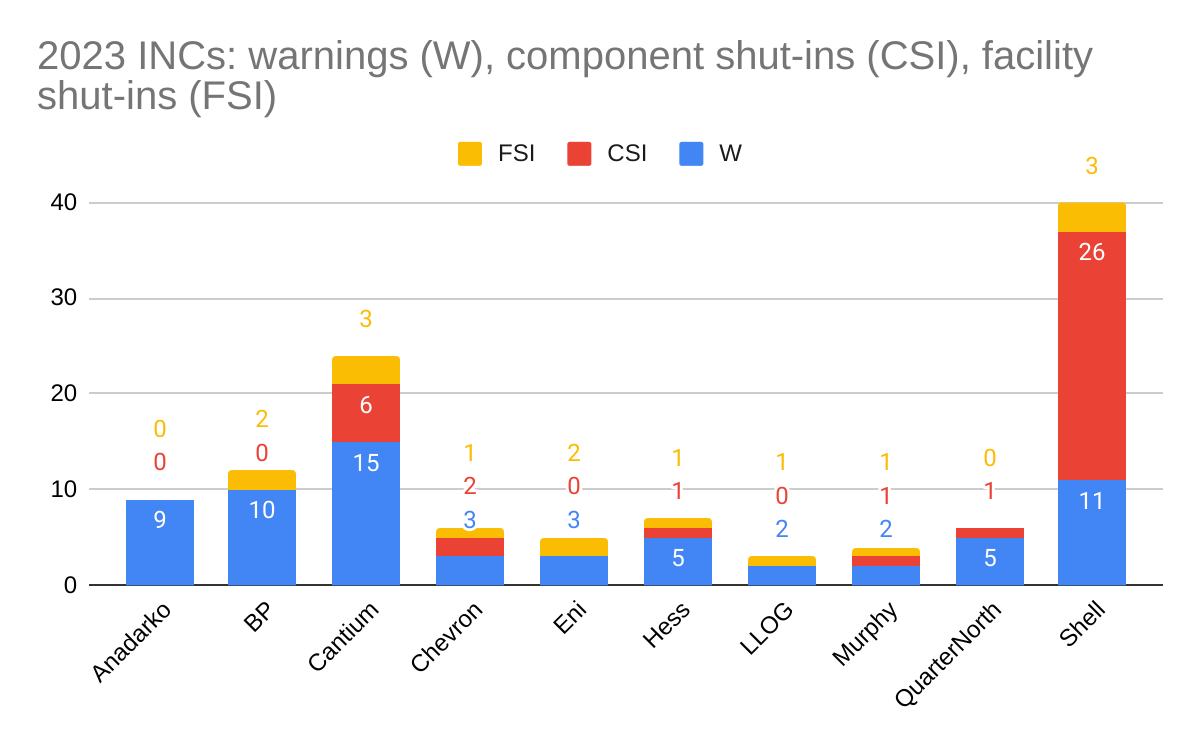

The Honor Roll companies for 2023 (listed alphabetically) are Anadarko, bp, Cantium, Chevron, Eni, Hess, LLOG, Murphy, QuarterNorth, and Shell.

BOE Honor Roll criteria:

Must average <0.3 incidents of noncompliance (INCs) per facility-inspection.

Must average <0.1 INCs per inspection-type. (Note that each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). On average, each facility-inspection included 3.3 types of inspections in 2023. Here is a list of the types of inspections that may be performed.

Must operate at least 3 production platforms and have drilled at least one well (i.e. you need operational activity to demonstrate compliance and safety achievement).

May not have a disqualifying event (e.g. fatal or life-threatening incident, significant fire, major oil spill). Due to the extreme lag in updates to BSEE’s incident tables, district investigations and media reports are used to make this determination.

platforms

2023 well starts

2023 (10 mos.) oil prod. (million bbls)

2023 (10 mos.) gas prod. (bcf)

Anadarko

10

11

66

60

BP

7

11

105

65

Cantium

96

10

5

6

Chevron

8

10

67

39

Eni

3

1

6

13

Hess

3

3

18

36

LLOG

10

7

25

35

Murphy

7

4

42

57

QuarterNorth

9

1

13

23

Shell

20

20

141

140

Also noteworthy:

Zero shut-in violations for Anadarko in 2023

<1 INC for every 10 facility inspections for Anadarko, Chevron, and Murphy

<1 INC for every 20 inspections (all types) for Anadarko, bp, Chevron, LLOG, Murphy, and QuarterNorth

Sale 261: single bid tracts in blue, multi-bid tracts in red (2), green (3), and purple (5)

The interest of the majors and most independents has shifted entirely to deepwater prospects, as evidenced by the above graphic and sale data. Nonetheless, a few resourceful companies continue to find value in the shallow waters of the continental shelf.

“There’s an art to finding oil—particularly in the Gulf of Mexico. After decades of drilling, this world-class basin still holds vast potential for those skilled enough to unlock it. Arena energy is applying expert insight and advanced technology to identify new Gulf of Mexico oil and gas exploration opportunities. This is the art of oil finding in the 21st century.“

Arena Energy, a successful shelf operator for a quarter of a century, was the leading shelf bidder with 6 high bids. In 2023 Arena was once again the most active shelf driller with 20 well starts. They claim a 94% drilling success rate. Arena currently operates 123 platforms and is the GoM’s 7th ranked natural gas producer and the 11th ranked oil producer.

Cantium, another leading shelf operator, was the high bidder on 4 tracts. Cantium drilled 10 wells in 2023 and currently operates 86 platforms. Cantium claims to maintain “the highest level of operational safety and regulatory compliance by maximizing efficiencies and empowering employees,” and publicly available compliance data bear that out. Cantium was a BOE Honor Roll company for 2022, and a preliminary look at the data indicates that their 2023 performance was also excellent. Cantium is ranked 18th in both oil and natural gas production.

Byron Energy, which is headquartered in Australia, is the only international company investing in the GoM shelf. Byron was the high bidder on 2 tracts and currently operates 2 platforms. The company drilled 3 wells in 2023. Byron intends to continue focusing on the shallow waters of the Gulf.

Thoughts on the attributes of a successful shelf operator:

Bid alone and conduct operations independently to facilitate efficiency and timely decisions.

Lean and flat organizational structure for optimal communication and effective project management.

Skilled staff and state-of-the art exploration technology.

Outstanding contractor selection and oversight.

Safety, environmental, and compliance leadership, absent which your company won’t be around for long.

Think small. Gleaning old fields and producing modest new discoveries can be profitable!

Control growth and debt. Busts follow booms and highly leveraged companies are the most vulnerable.

Study the successful shelf operators and the failures. What did they do right and wrong?

Cantium’s record is especially impressive given that most of their platforms were installed more than 40 years ago and some date back to the 1950s. They have also been a very active development well driller.

While Kosmos and Beacon have somewhat lower violation and penalty exposure because their production is via subsea wells tied back to surface facilities operated by other companies, they are demonstrating that entrepreneurial deepwater independents can also be safety leaders.

“The Pickerel-1 prospect was our first (exploration well on the Mississippi Canyon 727) and we are delighted that it was an oil discovery. Black Pearl will be the next and that will hopefully be a tieback (to Tubular Bells with first oil expected mid-2024).

“Then we have a wildcat opportunity (the Vancouver exploration prospect) later in the year in the Green Canyon. With the other 80 exploratory blocks that we have in the Gulf, we will be actively drilling for the next several years,” Hess said.

Per the BSEE borehole file, there were 2 deepwater exploratory well starts since 4/1/2023. The Shell well is another GoM milestone in that it is the 150th well spudded in >8000′ of water. The first was in the year 2000.

Operator

spud date

location

water depth

Chevron

5/5/2023

Mississippi Canyon 608

6678′

Shell

4/13/2023

Alaminos Canyon 728

8660′

Arena and Cantium continue to drive shelf drilling. Below are the shelf development wells since 4/1/2023: