The proposed revisions to the Arctic drilling regulations have just been posted and are attached for your convenience.

From a risk management standpoint, the current Arctic drilling rule, particularly the same season relief well (SSRW) provisions, is arguably the worst in the history of the OCS program. Regardless of the prospects for Arctic exploration, offshore drilling is not feasible under the current regulations. Hopefully, this proposal represents a significant improvement. More to follow after the text has been reviewed.

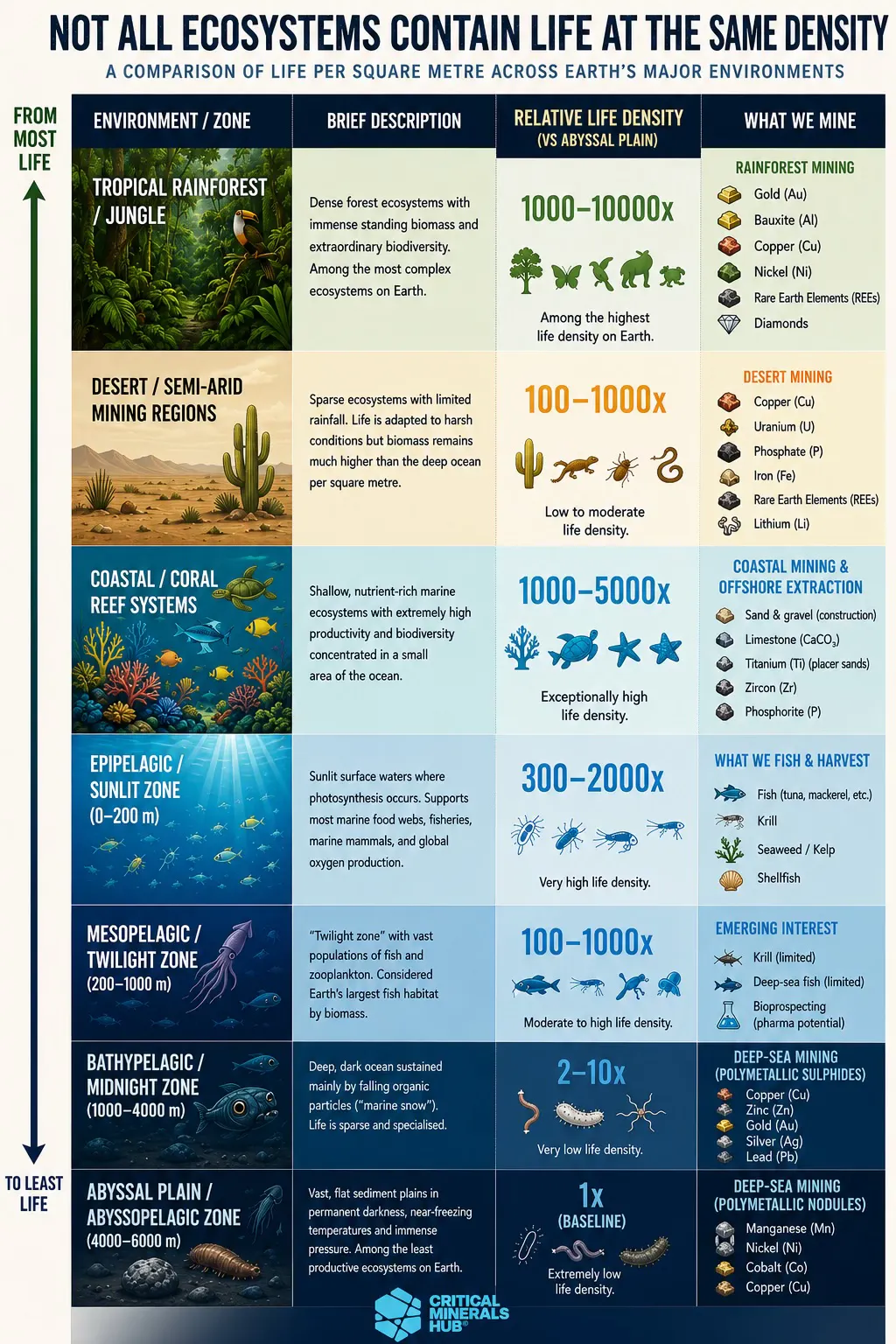

There are 67 NGOs with observer status at the International Seabed Authority (ISA) as of March 2026, which explains why nothing gets done. More than thirty years after its creation, there is still no final Mining Code for nodule exploitation.

“Deep‑sea mining disturbs low‑productivity abyssal ecosystems and may have long‑lasting local effects on small communities of widely distibuted organisms reliant upon the nodules themselves, but avoids the deforestation, human displacement and occupational hazards of many terrestrial mines. The ethical question is whether it is better to concentrate impacts on a relatively small portion of the most common habitat on Earth, or to continue expanding high‑impact mining frontiers on land like tropical rainforests.“

“The job of a regulator is not to deliver closure for activists. It is to regulate access to resources designated as the “common heritage of mankind” in a way that balances environmental protection, equitable benefit sharing and global development needs. That will always involve trade‑offs.“

Per EIA, Gulf of America oil production declined in May by over 200,000 bopd from April’s record production, which was corrected upward by 2000 bopd. Was the April number anomalous? We’ll need additional monthly data and the audited ONRR numbers to get a better read.

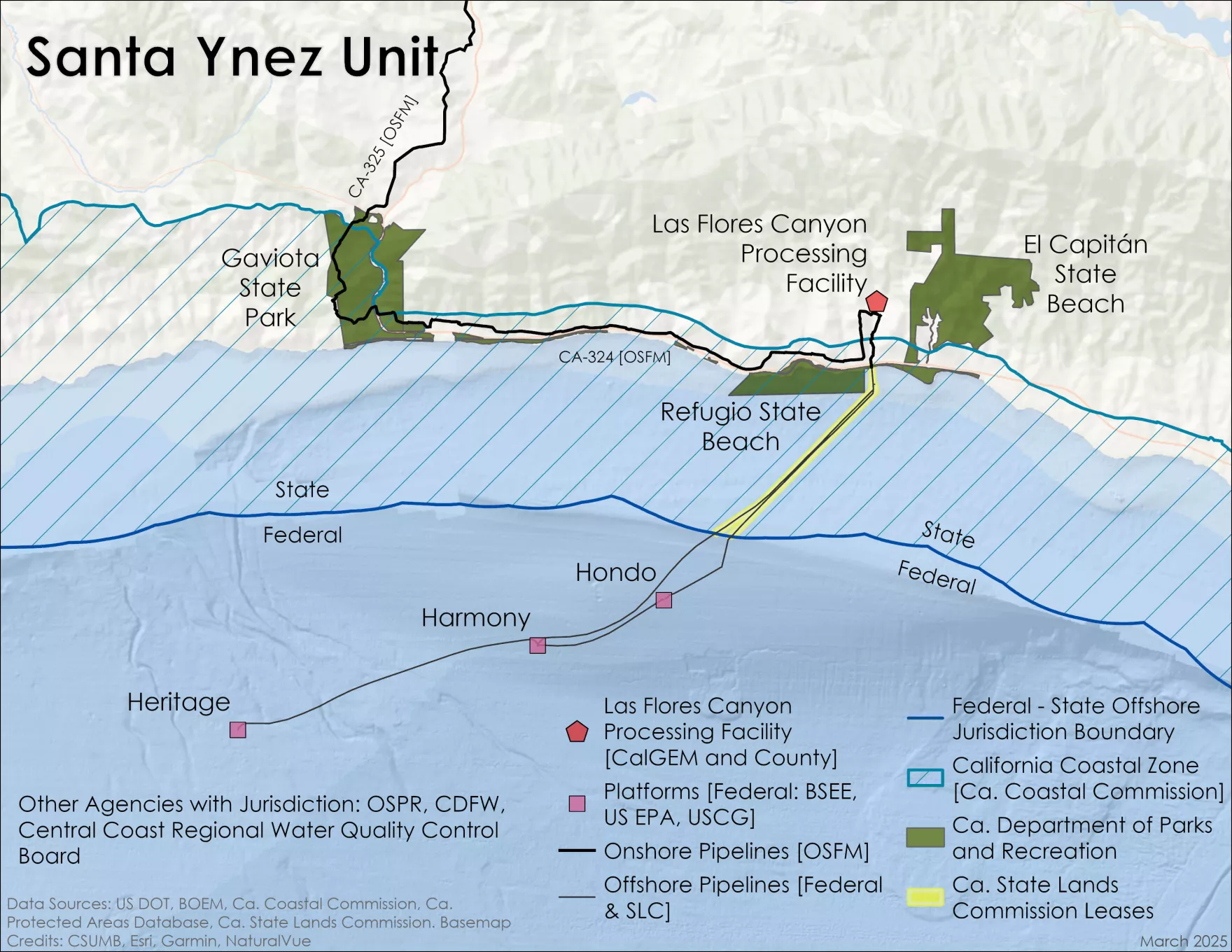

EIA posted corrected April and May totals of 30,000 bopd for the Pacific (California OCS), a 150% increase from February owing to the Sable Santa Ynez Unit restart. Although Pacific OCS production has been in the doldrums for years, the region has an impressive record of 202,000 bopd from Dec 1995.

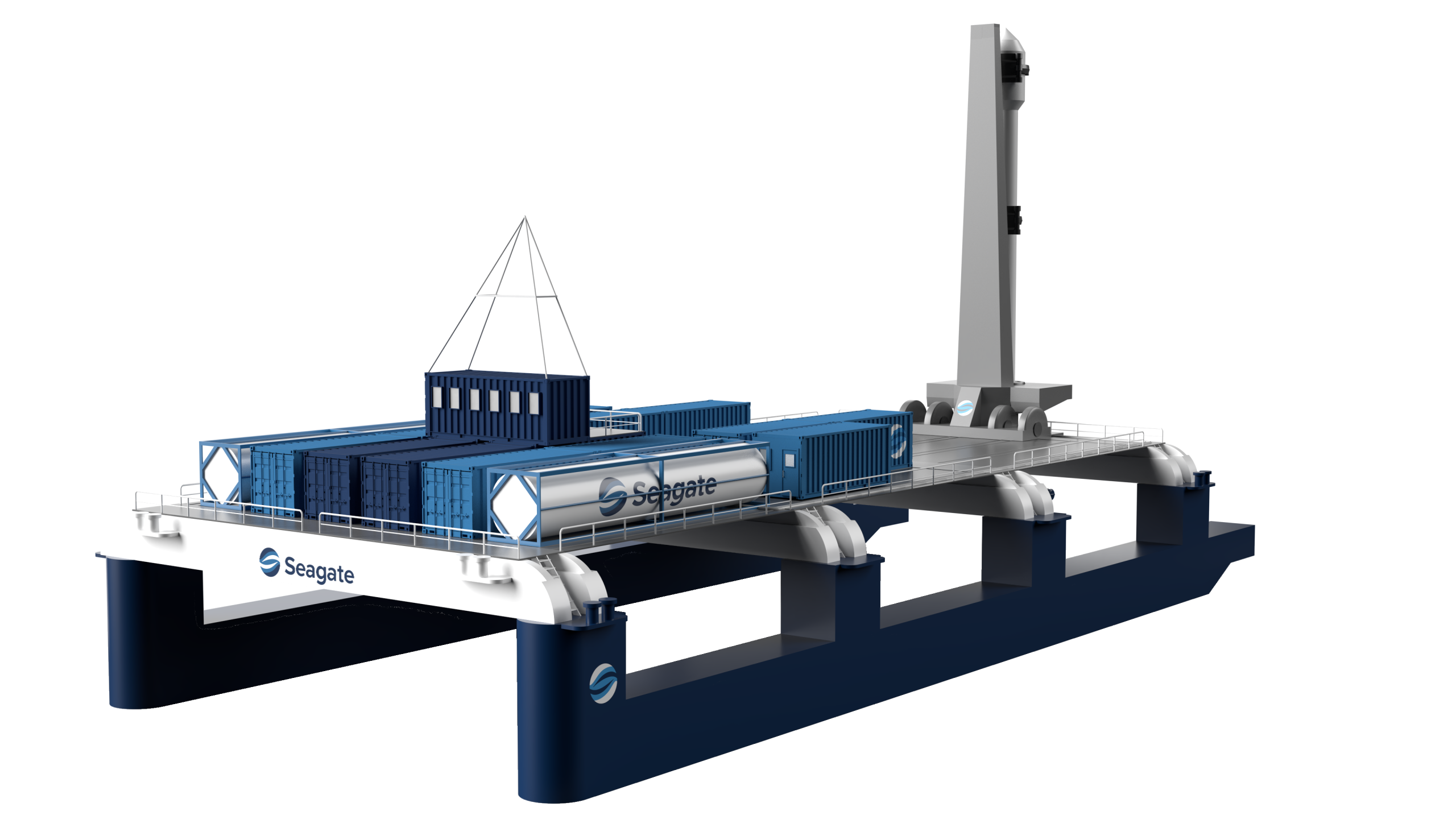

MMA’s public notice about support for space launch activities (Rigs-to-Rockets) recognizes the importance of collaboration between the highly innovative offshore and space industries.

In that regard, Seagate Space, a Florida company, is moving forward with plans for offshore launches. Seagate is “developing cutting-edge maritime infrastructure to avoid land site limitations and scale orbital launch cadence for commercial, government, and defense missions.”

Seagate’s Space Gateway-S platform has adopted features that have been widely applied by the offshore industry:

Autonomous dynamic positioning – developed and advanced by the drilling industry

Modular architecture – common in offshore facility design

Pontoon design – ala semi-submersible drilling units

Mobility – like mobile offshore drilling units (MODUs) – jackups, drillships, semi-submersibles

Space Florida, a public corporation and innovation connector, recently announced a partnership with Seagate Space:

EXPLORATION PARK, Fla.—June 2, 2026—Today,Space Florida announced Project Manta, a strategic investment in Seagate Space to expand Florida’s launch capacity through specialized maritime solutions. Space Florida’s Board of Directors approved an investment to prototype and demonstrate key elements of Seagate Space’s novel offshore launch infrastructure system, setting the stage for future development and manufacturing within the state of Florida.

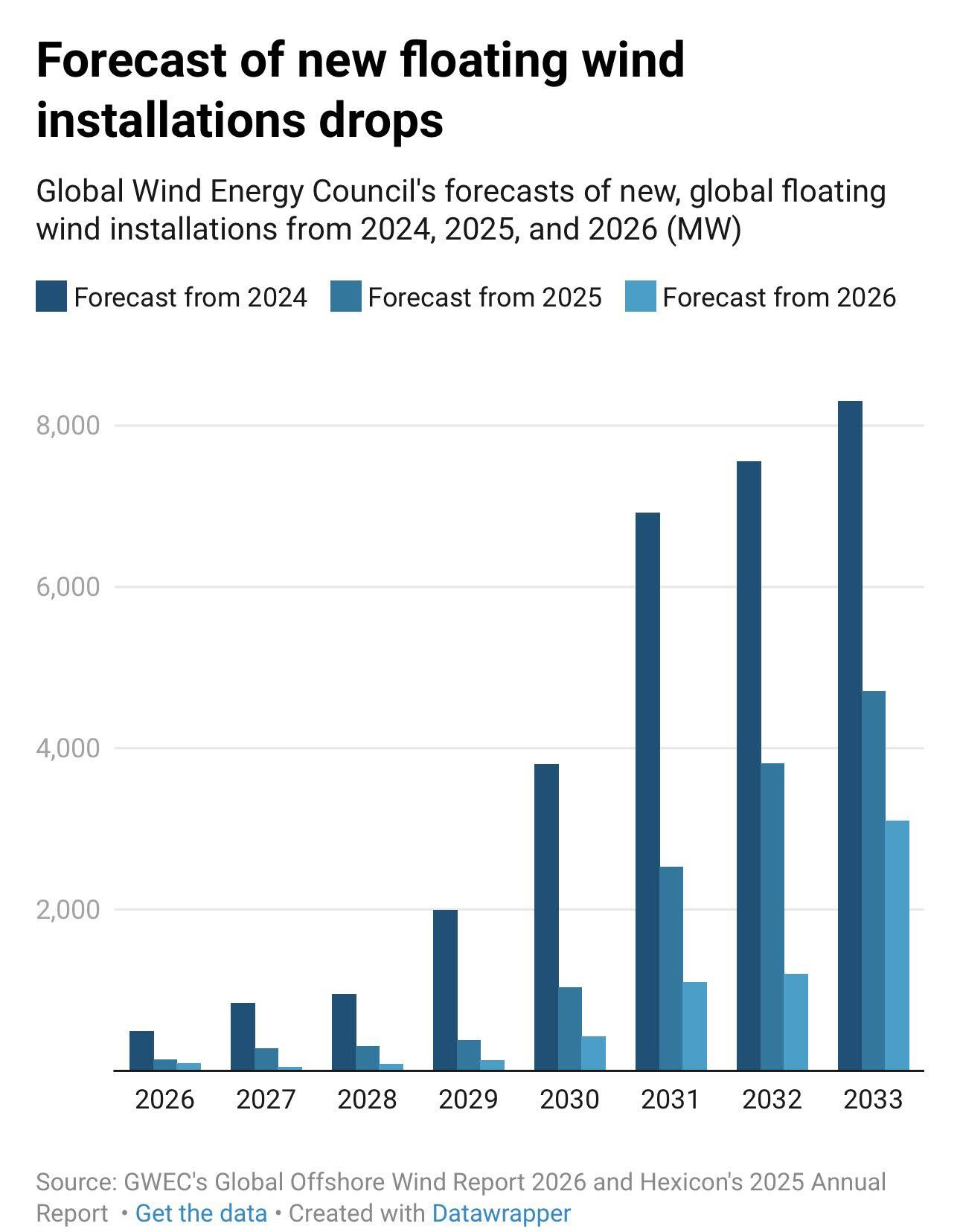

GWEC, the voice of the wind industry, continues to scale down estimates for floating turbines. In 2024, the GWEC expected 835MW of floating wind to be installed in 2027. Last year, this was lowered to 278MW, and expectations dropped further in the 2026 report to just 42MW. A similar trend applies to GWEC’s forecasts for the following years.

Despite strong support from the State, California’s offshore wind sector faces major challenges:

Deepwater technology: California offshore wind development is totally dependent on expensive and still unproven floating turbine technology. Norway, once a world leader in floating wind, has lost enthusiasm and is now requiring floating projects to be ‘quality-assured.’

Infrastructure: Major port upgrades, new transmission lines to bring power ashore, and specialized vessels are required. The supply chain is immature.

Costs: High capital costs plus storage costs (e.g. batteries) for reliability.

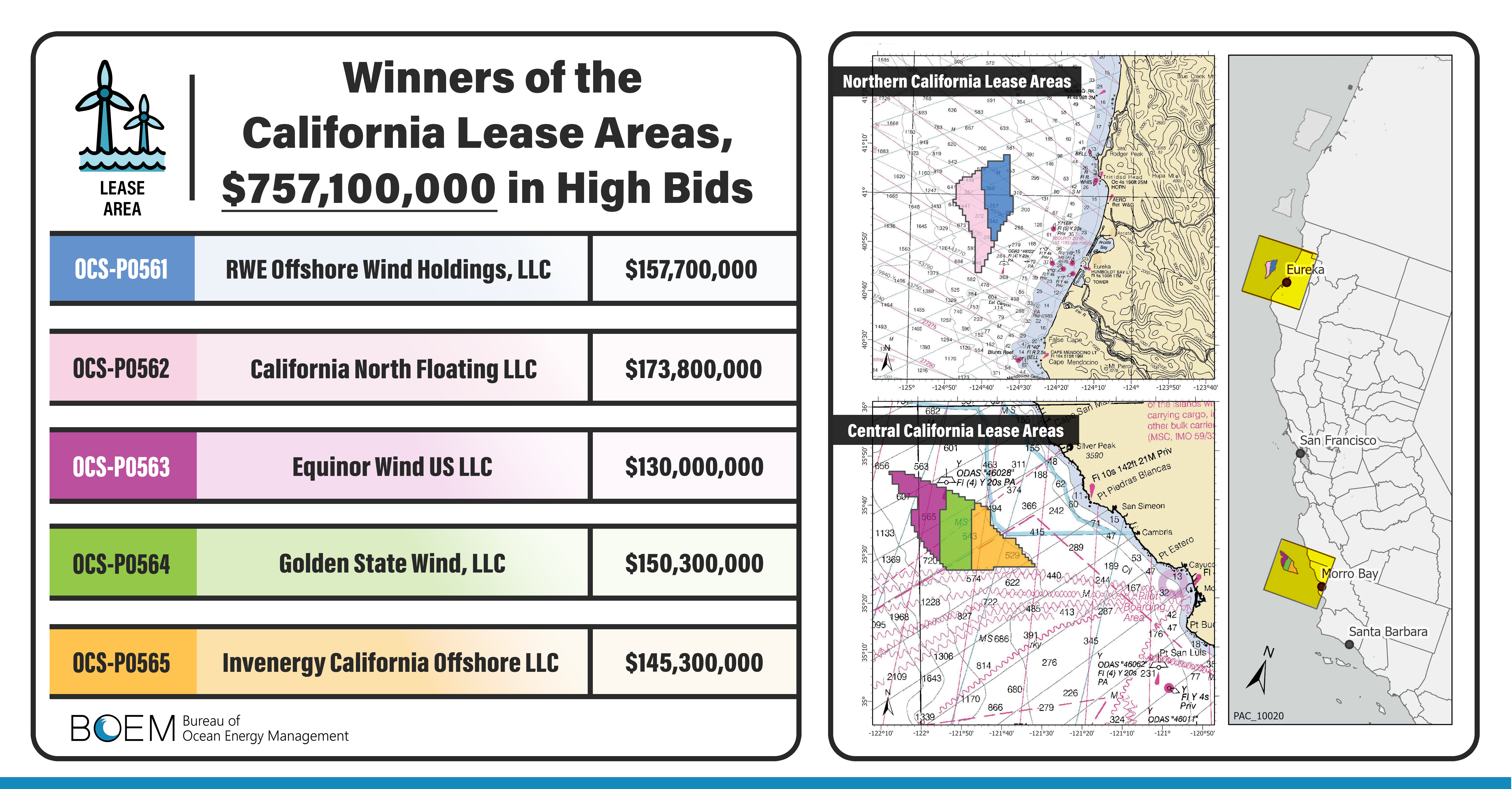

Two of the three Central Coast wind lessees (diagram below) have agreed to lease buyback deals. A lease cancellation letter is attached. The State is challenging the buyback agreements, and is thus in the difficult position of opposing deals that the wind developers voluntarily agreed to and believe are in their best interest. Does the State lose regardless of the outcome of their challenge?

The third Central Coast lessee, Equinor, is curtailing wind investments and has no plans to pursue new offshore wind projects in the US. A buyback deal with Equinor would be complicated by the company’s Empire Wind commitments, and is probably unnecessary given that Equinor has taken itself out of the game.

The two Northern California leases are still active, but the focus has been on regional planning. Funding for necessary infrastructure projects is uncertain and any wind lease development is far in the future.

The National Defense Authorization Act (NDAA), as passed by the House this week, includes an amendment (attached) authorizing the Federal govt to acquire all lands along the Santa Ynez Pipeline System route. Wesley Hunt (TX), who introduced the amendment, comments in the short video below. The Senate has yet to approve the bill.

Assuming Sable’s attorneys are able to continue navigating through the legal minefield, the success of the project will depend on the performance of Sable’s well operations and production teams, and the extent to which they have the authority and confidence to curtail operations when deemed necessary to protect workers and the environment. In that regard, MMA engineers and inspectors have an important role in identifying risks and assuring that they are mitigated.

Excerpt from the amendment:

SEC. 28ll. ACQUISITION OF EASEMENTS FOR DEFENSE FUEL SUPPLY INFRASTRUCTURE. (a) AUTHORITY TO ACQUIRE.—The Secretary of Defense is authorized to acquire, by purchase, donation, exchange, or condemnation, on behalf of the United States, such permanent easements over all lands along the route of the Santa Ynez Pipeline System, including all lands owned or otherwise held by the State of California or any agency, department, or instrumentality thereof, as the Secretary of Defense determines necessary to ensure continuous pipeline transportation of crude oil from the Santa Ynez Unit to domestic refineries supplying Department of Defense installations in the State of California

“Submerged reactor systems have been safely deployed in naval applications for decades, demonstrating their potential as a reliable source of energy in demanding marine environments. While no commercial deployment on the Outer Continental Shelf is planned or approved at this time, it could greatly strengthen America’s energy security in the future,” said MMA Acting Director Matt Giacona. “With nearly 3.2 billion acres of the Outer Continental Shelf under federal jurisdiction, this MOU is an important step toward building the technical expertise, regulatory clarity, and interagency coordination needed to assess whether and how this technology could be responsibly implemented in the years ahead.”

See attached. This is a well written directive. Kudos to the authors.

Retaining the revenue management functions in ONRR is prudent.

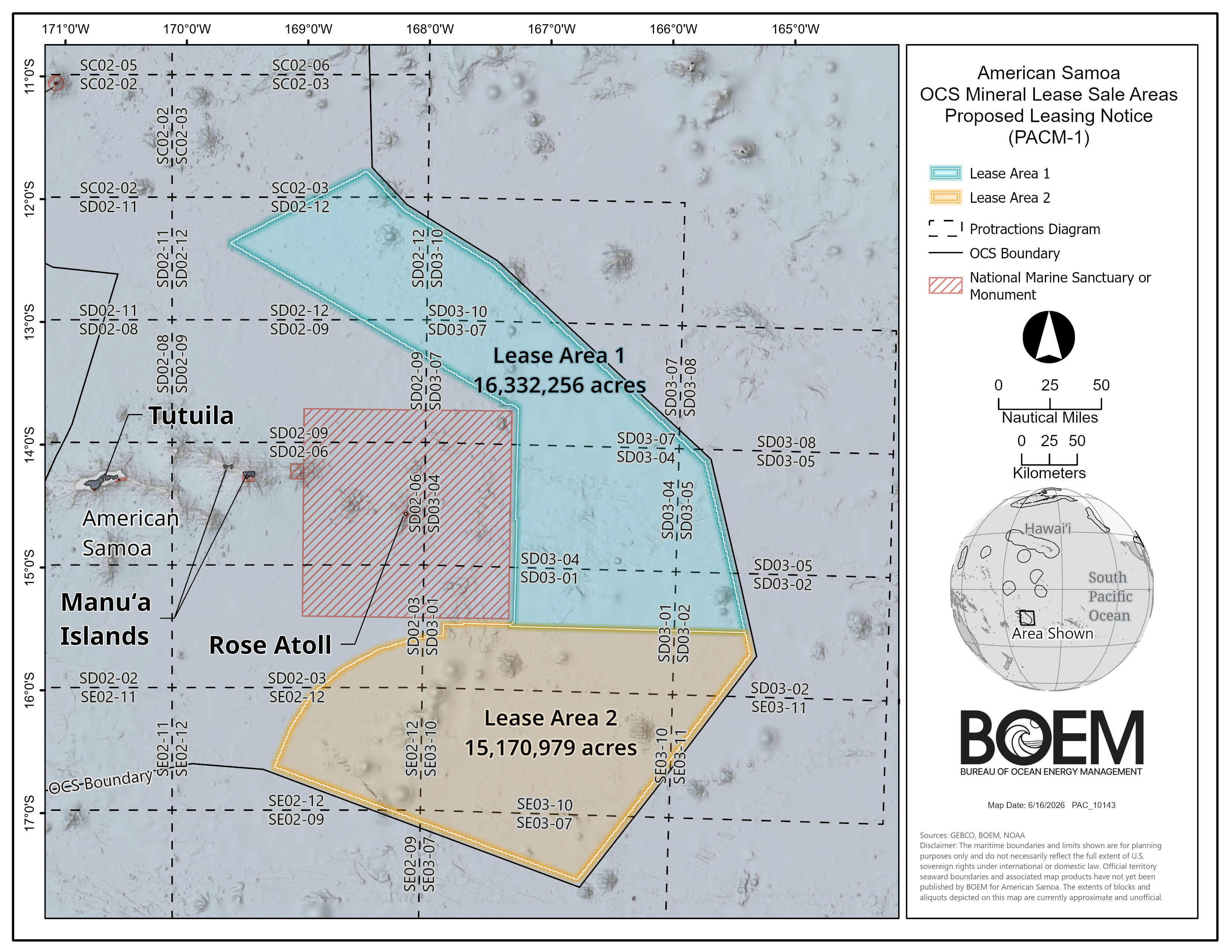

There has been no specific announcement regarding the MMA Director, but a quote in the American Samoa lease sale announcement cites Matt Giacona, Acting MMA Director. Congrats to him.

Federal Judge Dolly Gee, Central District of California

Sable Offshore and Exxon had alleged that Santa Barbara County’s refusal to transfer title and permits for Santa Ynez Unit facilities from Exxon to Sable amounted to an unconstitutional taking of their property rights. Judge Gee disagreed.

As colorfully put by Nick Welsh at the Santa Barbara Independent, Judge Gee told Sable and Exxon to “go pound sand” (not literally, but the judicial equivalent). The judge refused to even allow Sable to amend their filing. The judge will however allow Exxon to file an amended complaint, given that the company still has vested rights to the facilities and is still on the hook for the decommissioning costs.

As always with these Santa Ynez Unit matters, there is much more to come!