Posted in Uncategorized | 5 Comments »

Contrary to what you might see or read on social media, the Strait of Hormuz has not “opened” by continental rifting between Iran and Oman. This waterway is the locus of converging plate tectonic interactions between the Arabian and Asian plates and offers a natural laboratory to study plate tectonic subduction and collision.

This narrow waterway, only 60- to 24-miles wide, is the passage for one-fifth of the world’s oil transportation, or about 20 million barrels per day. According to the International Energy Agency, 80 percent of this oil goes to Asian markets; however, any major disruption in oil flow impacts the global economy because of the international connectedness of the oil industry.

Posted in Uncategorized | Tagged Strait of Hormuz, geology, plate tectonics, oil transport | Leave a Comment »

The proposed revisions to the Arctic drilling regulations are a positive initiative that will improve the prospects for renewal of Beaufort and Chukchi Sea exploration.

In particular, removing the same-season-relief-well (SSRW) requirements in the current regulations is an essential regulatory action. The SSRW provision has the effect of precluding exploratory drilling while providing no added environmental protection and increasing operational risks. Given that there is at least a 50% chance that rig mobilization, relief well planning, drilling, repeated surveying, and plugging the flowing well would take more than the specified 45 days, a SSRW is not a legitimate well control option.

The preamble includes important questions for respondents. These questions are compiled beginning on p. 108 of the attachment. In particular, the comments on Subsea Isolation Devices (SSIDs) should be interesting. Given the required blowout preventer stack redundancy, it’s not clear to me that SSIDs would reduce blowout risk. They would however increase operational complexity.

For floating drilling operations in the Arctic and elsewhere, the focus needs to be on well design, integrity, and control. Fortunately, by carefully verifying casing and cement integrity, ensuring complete barrier redundancy, and having standby capping and containment capability, the probability of a sustained oil blowout can be reduced to 10–6 or lower.

Lastly for now, these regulations further demonstrate the importance of consolidating BOEM and BSEE in a single bureau.

Posted in Alaska, energy policy, Offshore Energy - General, Regulation, well control incidents | Tagged Arctic drilling, BOEM, BOP, BSEE, MMA, regulations, same season relief well, subsea isolation device, well control | Leave a Comment »

The proposed revisions to the Arctic drilling regulations have just been posted and are attached for your convenience.

From a risk management standpoint, the current Arctic drilling rule, particularly the same season relief well (SSRW) provisions, is arguably the worst in the history of the OCS program. Regardless of the prospects for Arctic exploration, offshore drilling is not feasible under the current regulations. Hopefully, this proposal represents a significant improvement. More to follow after the text has been reviewed.

Posted in Alaska, drilling, energy policy, Regulation | Tagged Arctic drilling, BOEM, BSEE, Marine Minerals Administration, proposed regulations, SSRW | Leave a Comment »

Interesting article by Amanda Van Dyke. Highly recommended.

There are 67 NGOs with observer status at the International Seabed Authority (ISA) as of March 2026, which explains why nothing gets done. More than thirty years after its creation, there is still no final Mining Code for nodule exploitation.

“Deep‑sea mining disturbs low‑productivity abyssal ecosystems and may have long‑lasting local effects on small communities of widely distibuted organisms reliant upon the nodules themselves, but avoids the deforestation, human displacement and occupational hazards of many terrestrial mines. The ethical question is whether it is better to concentrate impacts on a relatively small portion of the most common habitat on Earth, or to continue expanding high‑impact mining frontiers on land like tropical rainforests.“

“The job of a regulator is not to deliver closure for activists. It is to regulate access to resources designated as the “common heritage of mankind” in a way that balances environmental protection, equitable benefit sharing and global development needs. That will always involve trade‑offs.“

Posted in deep sea mining, energy policy, Offshore Energy - General, Regulation | Tagged Amanda Van Dyke, deep sea mining, International Seabed Authority, low impact, marine minerals, Regulation | Leave a Comment »

Per EIA, Gulf of America oil production declined in May by over 200,000 bopd from April’s record production, which was corrected upward by 2000 bopd. Was the April number anomalous? We’ll need additional monthly data and the audited ONRR numbers to get a better read.

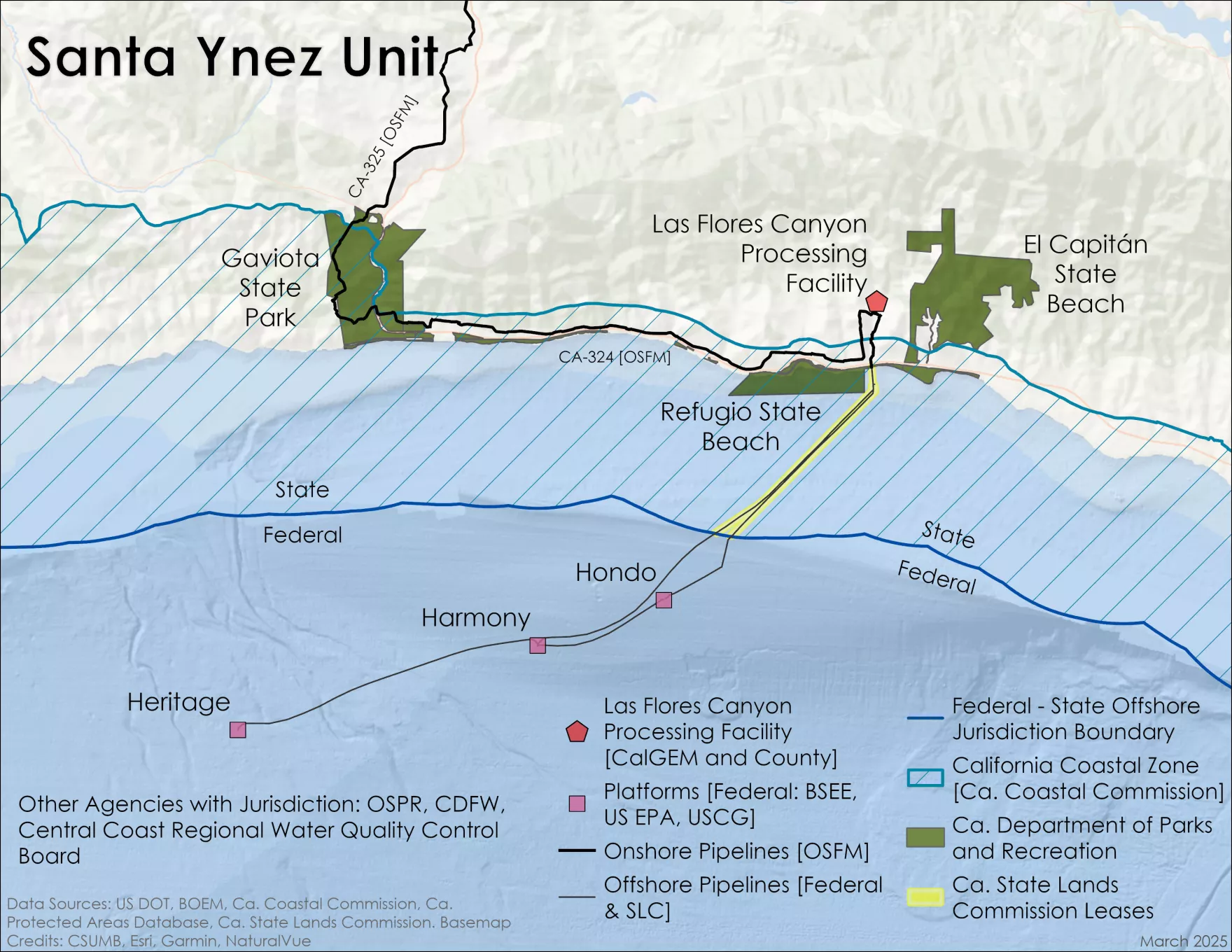

EIA posted corrected April and May totals of 30,000 bopd for the Pacific (California OCS), a 150% increase from February owing to the Sable Santa Ynez Unit restart. Although Pacific OCS production has been in the doldrums for years, the region has an impressive record of 202,000 bopd from Dec 1995.

Meanwhile EIA has still not corrected their 2025 OCS production totals to correspond with the audited ONRR data.

| 2025 OCS total – ONRR | 2025 OCS total – EIA | 2025 Gulf only – ONRR | 2025 Gulf only – EIA |

| 713,673,419 | 697,020,000 | 708,803,859 | 692,634,000 |

Posted in California, energy policy, Gulf of Mexico, Offshore Energy - General | Tagged California, Gulf of America production, offshore oil, ONRR, Sable Offshore, Santa Ynez Unit | Leave a Comment »

Excerpts from BP press release:

Atlantis is located about 150 miles south of New Orleans and has been in production for nearly 20 years. The expansion project adds two new subsea water injection wells to help increase the pressure of targeted reservoirs, unlocking additional barrels and extending the producing life of one of bp’s flagship US offshore assets.

The project, which was delivered ahead of schedule and under budget, adds approximately 10,000 barrels of oil equivalent per day (boe/d) of gross peak annualized average production, with around 5,000 boe/d net to bp.

Some of you may remember the 2009 False Claims Act allegations by a former BP contractor claiming that BP did not properly maintain the engineer-approved “as built” drawings of systems and structures aboard the Atlantis facility. The contractor alleged that the absence of the documentation created increased safety risks for the facility and to its personnel.

Following the allegations, an industry source closely involved with the project (but not a BP employee) made the following comment to the BOE blog:

Atlantis was by far, in my opinion, the best of the bunch; proceeded as a normal construction project. The PMs were the best I’ve come across.

BOEMRE (the name of the offshore safety regulator at the time) conducted a comprehensive investigation of the matter. Director Michael Bromwich sumarized the findings:

“As the report makes clear, although we found significant problems with the way BP labeled and maintained its engineering drawings and related documents, we found the most serious allegations to be without merit, including the suggestion that a lack of adequate documentation created a serious safety risk on the Atlantic facility. We found no credible evidence to support that claim.”

The BOEMRE press release is attached. Link to the full investigation report.

In August 2014, a Federal court dismissed the False Claims Act lawsuit because the plaintiffs lacked evidence and standing.

Posted in Gulf of Mexico, Offshore Energy - General, Regulation | Tagged bp, BOEMRE, Atlantis, False Claims Act, expansion project | 2 Comments »

A 7/28/2026 Dept. of Justice brief submitted to the Ninth Circuit Court of Appeals cites the 5/28/2026 Supreme Court decision in Flowers Foods Inc. v. Brock in asserting that Sable’s onshore pipeline segments are interstate and subject to Federal jurisdiction.

This filing is part of multi-faceted litigation involving Federal preemption, a 2020 Consent Decree, emergency special permits, and state environmental concerns. The Ninth Circuit is handling the expedited briefings and consolidation of petitions.

DoJ’s core argument is that Sable’s onshore segments do not interrupt the continuous “flow of commerce” from Outer Continental Shelf (OCS) offshore extraction → onshore processing → further transport to terminals (e.g., in Kern County). Thus, the system qualifies as interstate commerce subject to Federal (PHMSA) oversight rather than state regulation.

The Flowers Foods Inc. v. Brock case considered similar flow of commerce issues. The SCOTUS agreed with the Tenth Circuit that Brock delivery franchisees were engaged in interstate commerce even if they never cross State lines. The gist of the decision is as follows (emphasis added, full decision attached):

The Federal Arbitration Act (FAA) requires courts to enforce many private arbitration agreements, but it also provides that “nothing” in the law shall be used to compel arbitration in disputes involving the “contracts of employment” of any class of workers “engaged in . . . interstate commerce.” 9 U. S. C. §1. This case poses the question whether someone can qualify as a worker under the §1 exemption if he never crosses state lines and never interacts with vehicles that do. Flowers Foods, Inc., is a large producer of packaged baked goods with bakeries in 19 States. To get its products to market, the company depends in part on franchisees who buy the distribution rights to Flowers’s products in specific geographic territories. Angelo Brock is one such franchisee serving the Denver area; he picks up Flowers’s products from a warehouse in Colorado and delivers them to local stores, all without leaving the State. In 2022, Brock sued Flowers in federal district court alleging that the company had underpaid him and other distributors in violation of various federal and state laws. Flowers moved to compel arbitration, arguing that the FAA generally requires courts to stay or dismiss cases when the parties have agreed to resolve their disputes by arbitration and that Brock had signed a distribution agreement promising to arbitrate any disagreement. The district court denied Flowers’s motion, and the Tenth Circuit affirmed. Resting its decision on 9 U. S. C. §1, the Tenth Circuit reasoned that Brock belonged to a class of workers engaged in interstate commerce and thus the court lacked authority to compel arbitration.

We should soon find out what the Ninth Circuit thinks!

Posted in California, Offshore Energy - General, pipelines, Regulation | Tagged DOJ, Flowers Foods, NInth Circuit, pipeline, pipeline jurisdiction, Sable Offshore, Santa Ynez Unit, SCOTUS | Leave a Comment »

North Sea pioneer JL Daeschler comments on the passing of Sir Ian Wood: “A great North Seas leader who had an amazing career. He founded the Wood Group, an internationally important engineering firm. Mustang Engineering, well known to the US offshore industry, became part of the Wood Group in 2000.”

Last September, JL reminisced about Ian following the sale of the Wood Group:

I knew Ian in the early North Sea development stage. He became Sir Ian Wood. We used to chat at various conferences in Houston, Stavanger, and Aberdeen. Ian was an energetic man, who had a friendly a approach to our North Sea challenges. He was a true Aberdonian entrepreneur who employed 1000’s in offshore related disciplines worldwide.

Sir Ian turned his father’s fishing business into the Wood Group oil giant, leading the way as Aberdeen blossomed into Europe’s energy capital. When Sir Ian announced his retirement in 2012, Wood Group employed 41,000 people in 50 countries.

The Aberdeen Press and Journal and the BBC have posted excellent obituaries.

RIP Ian. You made the offshore world safer and more productive!

Posted in Offshore Energy - General, UK, Uncategorized | Tagged Aberdeen, engineering firm, JL Daeschler, North Sea, Sir Ian Wood, Wood Group | Leave a Comment »

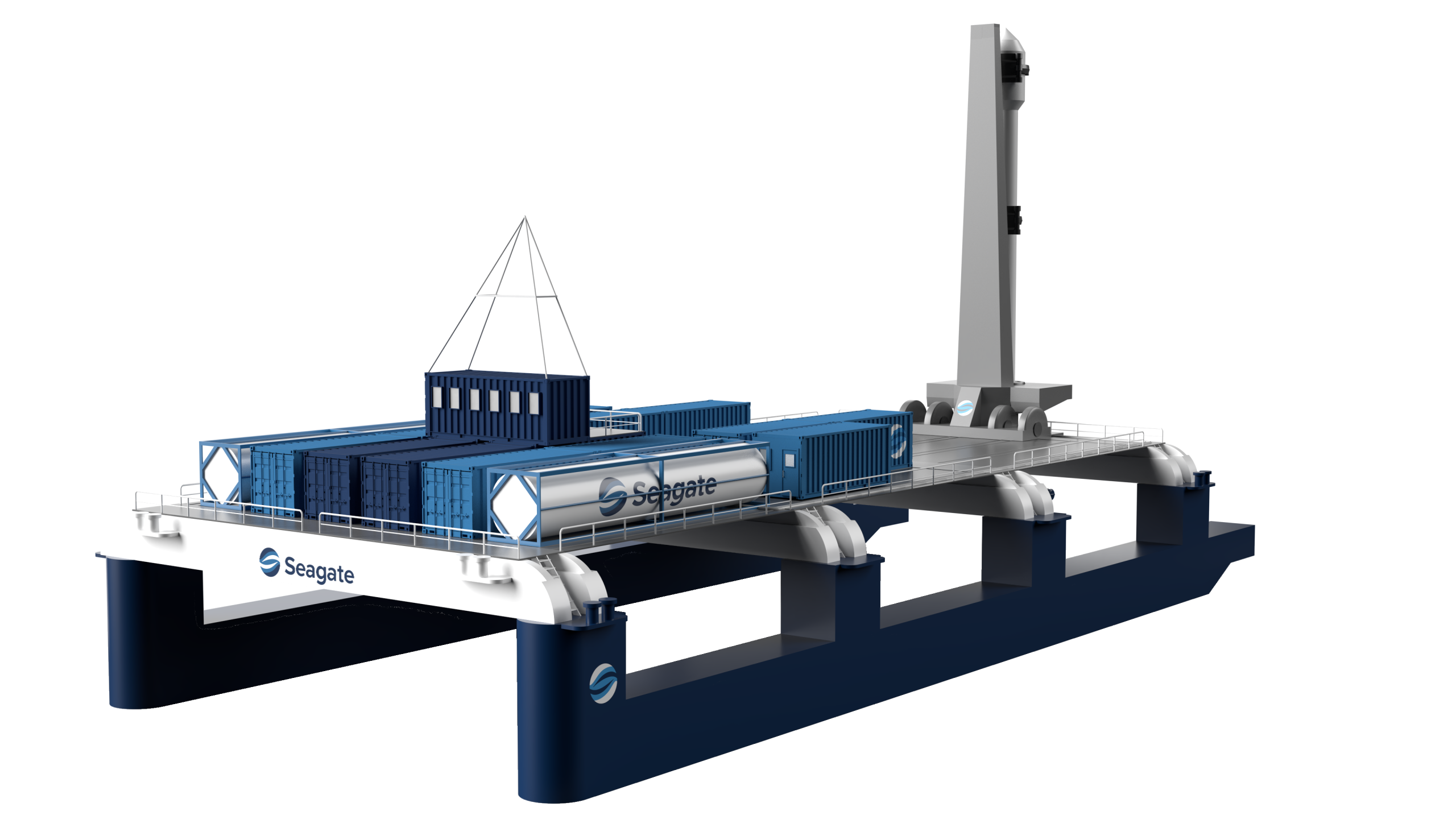

MMA’s public notice about support for space launch activities (Rigs-to-Rockets) recognizes the importance of collaboration between the highly innovative offshore and space industries.

In that regard, Seagate Space, a Florida company, is moving forward with plans for offshore launches. Seagate is “developing cutting-edge maritime infrastructure to avoid land site limitations and scale orbital launch cadence for commercial, government, and defense missions.”

Seagate’s Space Gateway-S platform has adopted features that have been widely applied by the offshore industry:

- Autonomous dynamic positioning – developed and advanced by the drilling industry

- Modular architecture – common in offshore facility design

- Pontoon design – ala semi-submersible drilling units

- Mobility – like mobile offshore drilling units (MODUs) – jackups, drillships, semi-submersibles

Space Florida, a public corporation and innovation connector, recently announced a partnership with Seagate Space:

EXPLORATION PARK, Fla.—June 2, 2026— Today, Space Florida announced Project Manta, a strategic investment in Seagate Space to expand Florida’s launch capacity through specialized maritime solutions. Space Florida’s Board of Directors approved an investment to prototype and demonstrate key elements of Seagate Space’s novel offshore launch infrastructure system, setting the stage for future development and manufacturing within the state of Florida.

Seagate has also signed an MOU with Oceaneering, a leading offshore company.

Jacksonville news clip about offshore launches:

Posted in energy policy, Florida, Uncategorized | Tagged BOEM, Gateway-S, MMA, Oceaneering, offshore and space synergy, Rigs-to-Rockets, Seagate Space, Space Florida | Leave a Comment »

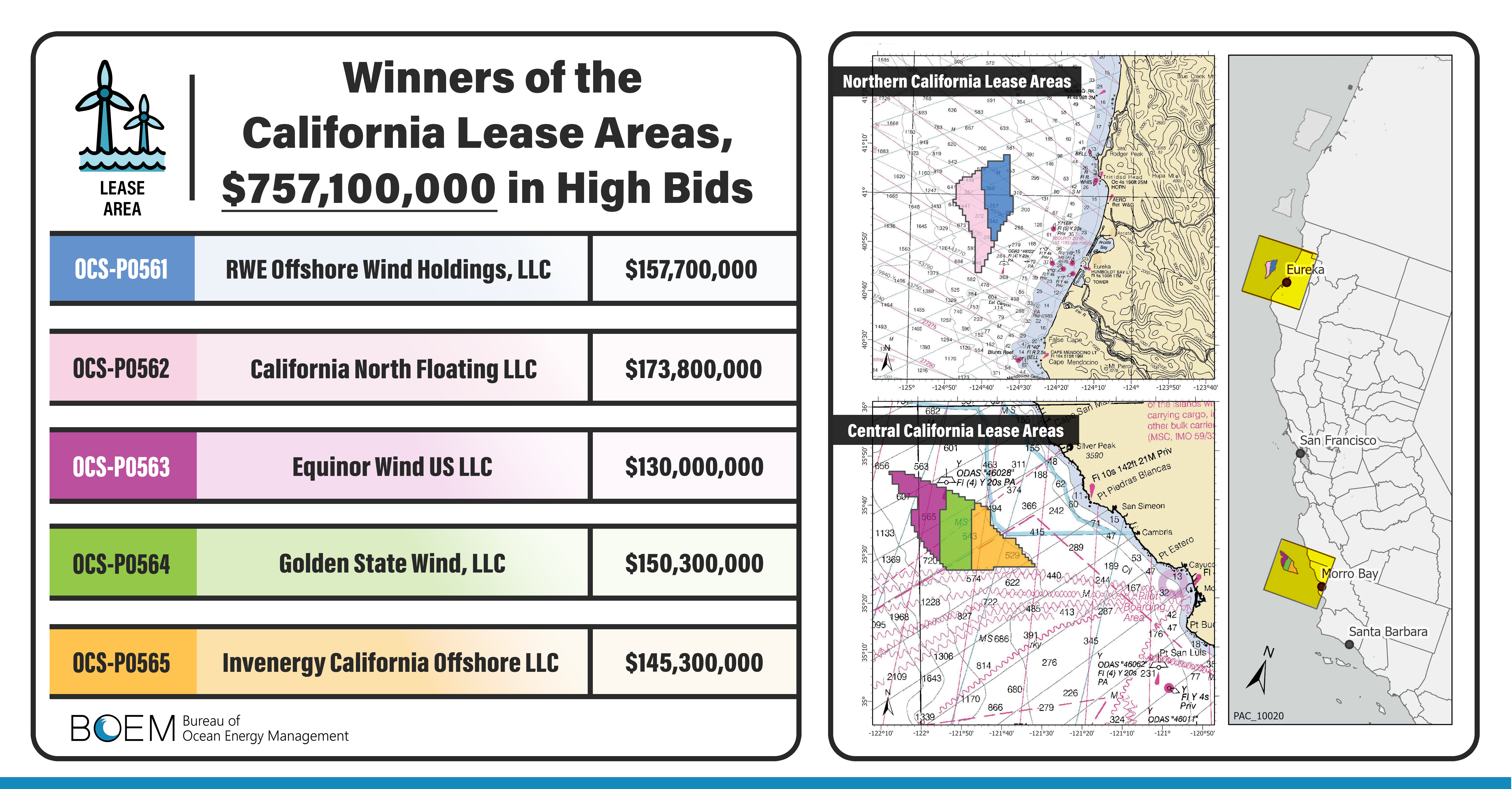

Despite strong support from the State, California’s offshore wind sector faces major challenges:

- Deepwater technology: California offshore wind development is totally dependent on expensive and still unproven floating turbine technology. Norway, once a world leader in floating wind, has lost enthusiasm and is now requiring floating projects to be ‘quality-assured.’

- Infrastructure: Major port upgrades, new transmission lines to bring power ashore, and specialized vessels are required. The supply chain is immature.

- Costs: High capital costs plus storage costs (e.g. batteries) for reliability.

- Environmental and stakeholder issues: Opposition to industrializing the coast.

- Worldwide struggles for the wind industry.

Two of the three Central Coast wind lessees (diagram below) have agreed to lease buyback deals. A lease cancellation letter is attached. The State is challenging the buyback agreements, and is thus in the difficult position of opposing deals that the wind developers voluntarily agreed to and believe are in their best interest. Does the State lose regardless of the outcome of their challenge?

The third Central Coast lessee, Equinor, is curtailing wind investments and has no plans to pursue new offshore wind projects in the US. A buyback deal with Equinor would be complicated by the company’s Empire Wind commitments, and is probably unnecessary given that Equinor has taken itself out of the game.

The two Northern California leases are still active, but the focus has been on regional planning. Funding for necessary infrastructure projects is uncertain and any wind lease development is far in the future.

Posted in California, energy policy, Offshore Wind | Tagged California, challenges, Equinor, floating turbines, infrastructure, Invenergy, lease buybacks, Offshore Wind | Leave a Comment »