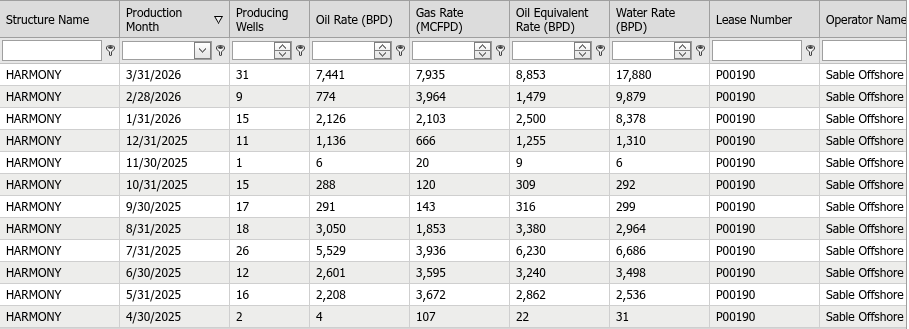

Sable Offshore began ramping up production at Platform Harmony last May delivering oil and gas to their Los Flores Canyon Processing Facility. In March, they resumed transportation to the Pentland pipeline segments and achieved first sales.

Below are BOEM production data for Harmony through March 2026. Harmony production was expected to increase to 22,000 bopd in May. Similarly, Sable forecasted Heritage production of 30,000 bopd for that month. The actual production numbers should be available in a month or two.

Nothing in the March production data for Harmony is particularly surprising. The gas-oil ratio (GOR) of ~1000 cu ft/bbl is rather typical for oil production in the region, as is the water cut, although less water production would be preferred. Produced water is not discharged from the platform, but is injected subsurface through disposal wells.

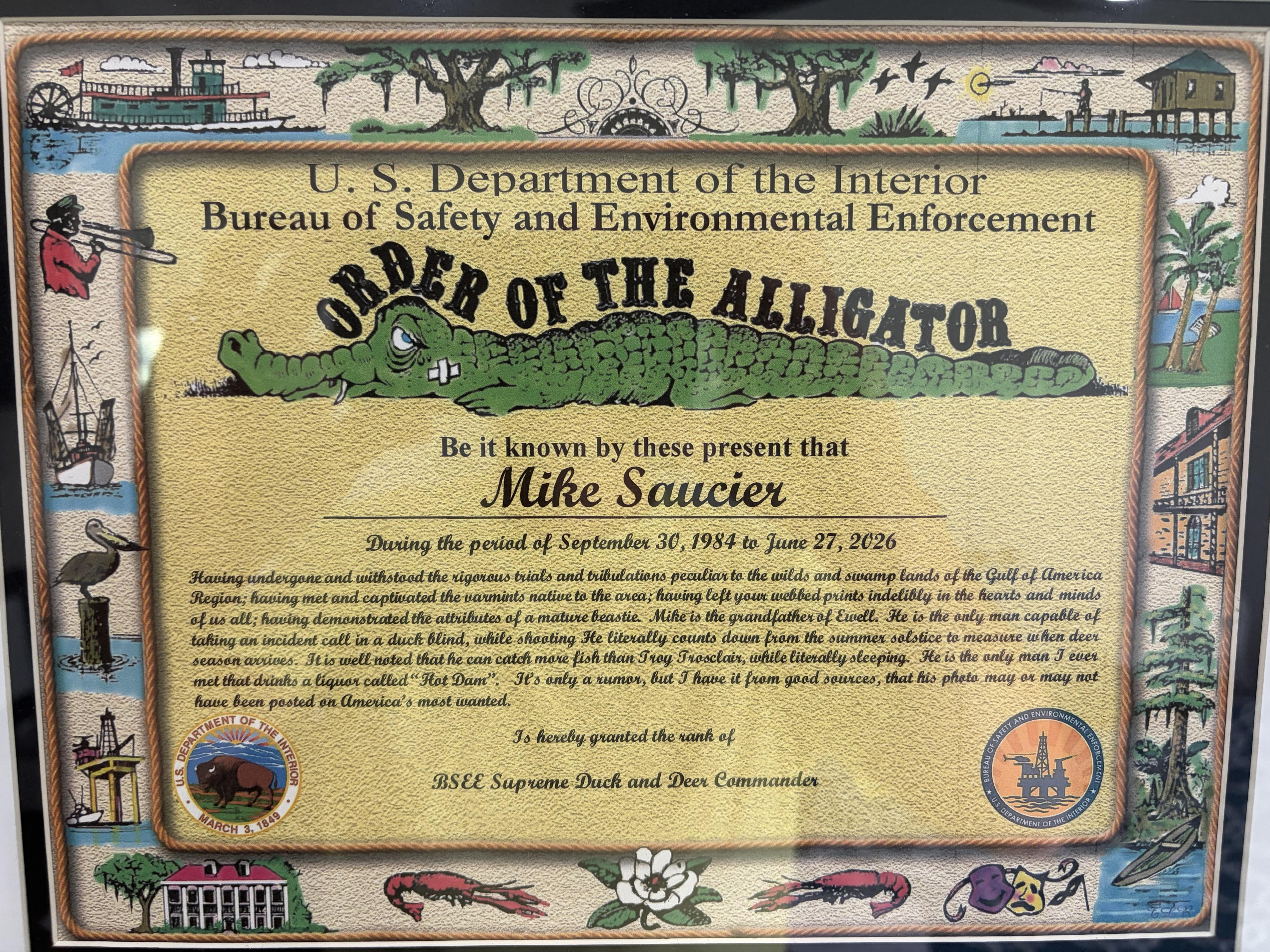

Bryan Domangue presents the coveted Order of the Alligator citation to Mike SaucierLars Herbst welcomes Mike Saucier to our prestigious retirement organization (fMMS).

After 41 years of offshore safety leadership, Mike Saucier, an outstanding engineer and manager, is retiring from the Bureau of Safety and Environmental Enforcement (BSEE).

Like many of the offshore program’s stalwarts, Mike earned a petroleum engineering degree from the Louisiana State University (LSU). In 1984, he began his Federal career in the Houma District Office of BSEE’s predecessor, the Minerals Management Service (MMS), where he was mentored by the great John Borne.

Mike has held many important engineering and supervisory positions including Drilling Engineer and District Manager in the highly regarded Houma District Office, Regional Supervisor for Field Operations, Regional Supervisor for District Field Operations, Acting Deputy Regional Director for District Operations, and Senior Technical Advisor for the Office of the Director. When the New Orleans District Manager retired during a hiring moratorium, Mike stepped up and assumed those duties as well.

Mike impressed his colleagues with his commitment to safety achievement, the essential core element of the offshore program. His diligence, and his firm, fair, and consistent enforcement of the safety and pollution prevention regulations, earned him respect throughout the offshore industry.

Mike is an avid outdoorsman who enjoys hunting and fishing, and has 4 grandsons to mentor in those skills. Note the impressive achievements cited in the Order of the Alligator certificate (below) 😉. The Order of the Alligator recognition is most fitting given Mike’s alligator hunting expertise, which greatly impressed those of us who were unfamiliar with such exploits!

In recognition of Mike’s outstanding career, the Board of Directors of the former Minerals Management Service (fMMS) has unanimously voted to induct Mike into the fMMS Hall of Fame! Mike receives (is sentenced to? 😉) lifetime membership in the fMMS and a registered copy of the offshore world’s prized masterpiece, the painting Rig at Sunset 😉. (image and short explanation below).

Congratulations to Mike! You made a difference!

“Rig at Sunset” was painted 50 years ago by a US Geological Survey (USGS) employee who chose to remain anonymous. Initially, the masterpiece was presented to USGS (later MMS) engineers and scientists who had made important contributions to the offshore oil and gas program. Understandably, the intended recipients were so humbled by the magnificence of the painting that they could not accept it. As the painting grew in value and international prominence, framed copies were presented to outstanding retirees and the original painting was kept at a secure, undisclosed location.

The Buckskin field (LLOG) is located in Keathley Canyon blocks 785, 828, 829, 830, 871, and 872 in 6,800 ft (2,073 m) of water. The KC 828 lease expired last year and LLOG’s bid for that block at the BBG2 sale was rejected.

BOEM’s Decision Information Matrix for Sale BBG2 is attached. As previously noted, 2 of the 25 high bids were rejected: Keathley Canyon Block 828 ($1,101,202) and Atwater Valley Block 63 ($650,018).

MROV=Mean of the Range-of-Value; LBCI=Lower Bound Confidence Interval

In the case of Keathley Canyon 828, BOEM’s valuation is more than 20 times the high bid. BOEM valued this block far higher than any other block in the sale.

KC 828 had been previously leased and that lease expired on 9/3/2025. The lease block was part of LLOG’s Buckskin field. Apparently, the lease expired due to inactivity given that the last well reached total depth more than a year prior to the expiration date. LLOG wanted the lease back. BOEM’s rejection sends a message that the price went up (by a lot 😉).

Finally, why didn’t any other company bid on KC 828, a block that has been publicly reported as being part of the Buckskin field?

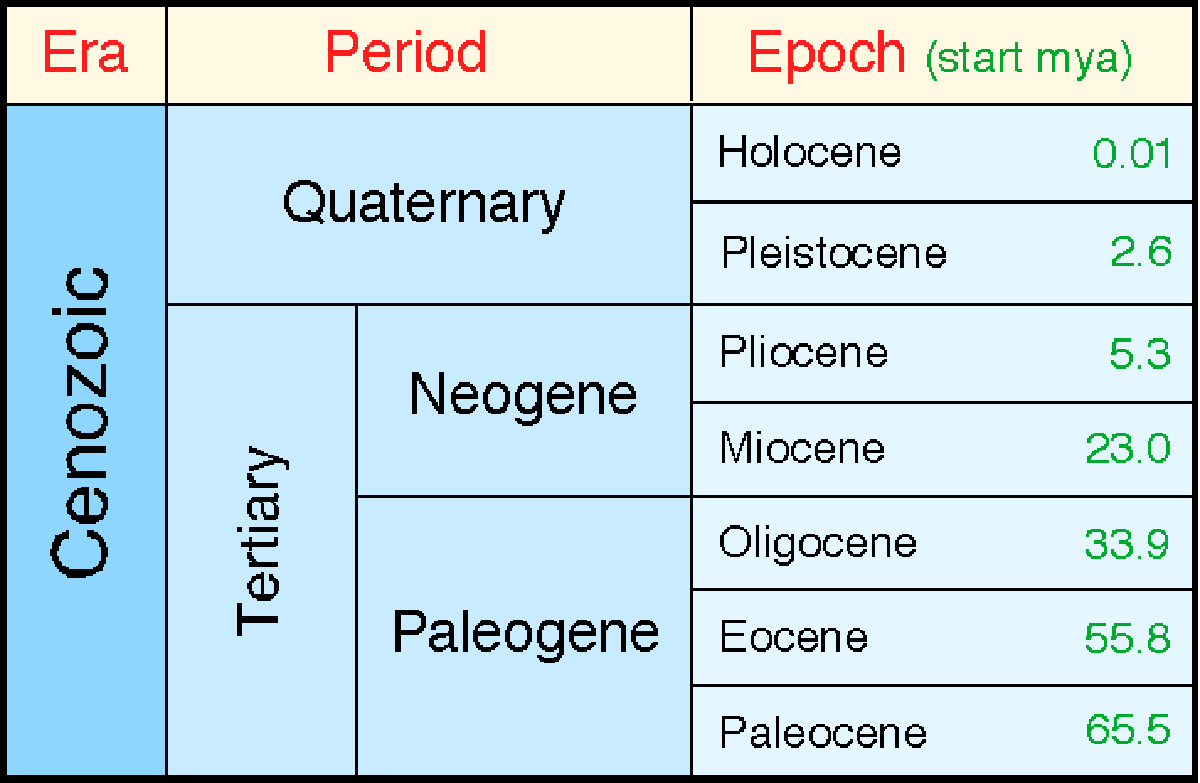

My colleague Keith Meekins shared an informative AAPG article about the importance of Miocene reservoirs in offshore oil and gas production worldwide.

“The Miocene delivered a significant amount of sand with excellent reservoir characteristics around the world,” noted Erik Scott, exploration geologist and consulting geologist/sedimentologist.

“Generally, hydrocarbons are coming from deeper, older rock – the Cretaceous, the Jurassic. By the time these source rocks get to the (hydrocarbon) generation window, the Miocene reservoirs are in place,” Scott said.

“Generally, the Miocene deposits are surrounded by fine-grained muds that produced sealing potential,” he noted.

More:

Miocene reservoirs account for more than 40 percent of established hydrocarbon reserves in the deepwater Gulf. The Bureau of Ocean Energy Management identifies more than 9 billion barrels of undiscovered, technically recoverable Miocene resources.

Recently, Eni found a giant Miocene natural gas accumulation in the Kutei Basin offshore Indonesia with an estimated 5 trillion cubic feet of gas and 300 million barrels of condensate in place.

Azule Energy, equally owned by Eni and BP, made a recent Miocene oil discovery with an estimated 500 million barrels of crude offshore Angola.

Keith points to RTM (reverse-time migration) as an important factor in helping to unlock Miocene resources. RTM produces dramatically improved images below salt bodies and in areas of complex overburden. Per AAPG, Talos Energy used reprocessed RTM seismic to identify a bypassed Miocene fault-block closure in the Green Canyon Area of the Gulf. This structure had previously been invisible.

Steve finds Equinor’s recent comment that the days of big offshore finds are over to be disingenuous. He correctly notes that this view has been echoed for decades. (Although the end of Gulf of America oil production has been predicted for 40 years, 2025 was a near record year.)

Offshore Norway, it was only in 2010 that the giant Johan Sverdrup field was ‘found’ by Equinor. Two super-majors – Exxon and Total – missed the reservoir and abandoned further exploration in the area. (How many times have we heard similar stories in the oil patch?) Equinor, then Statoil, made a relatively small find in the middle of the reservoir and was planning a limited subsea development. Geophysicists from partner Lundin created a better picture of what was in place – nearly 3 billion barrels with peak production of 750,000 b/d three years ago. Just this week, Equinor announced Phase 4 of production through further subsea development.

Who heard much about Guyana a decade ago?

How about the major new discoveries offshore Brazil? See the video below.

New production offshore Namibia, South Africa, and Mozambique looms. Finds off Indonesia and Timor Leste, and even the Falklands, await development.

“So guys, stop making out that life is tough. It might be challenging, but it has always been thus. Big risks and big rewards.”

On BP’s announcement that they were reorganizing into upstream and downstream divisions: “Wow – what a great idea! How come no one ever thought of this before? Imagine this scenario – oil companies making money on both sides of the price cycle – upstream when the price of oil is high and downstream when it is lower. Amazing – NOT!” 😉

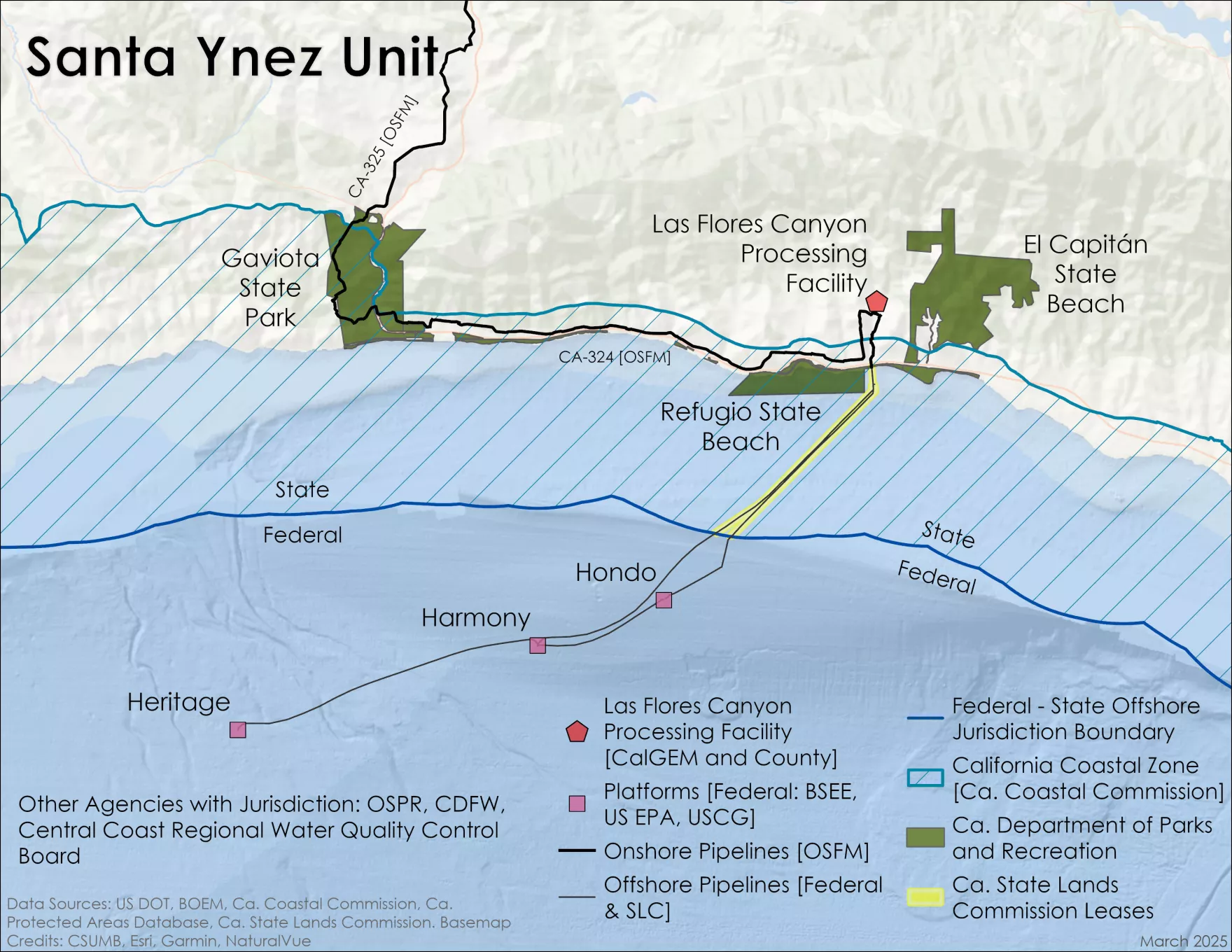

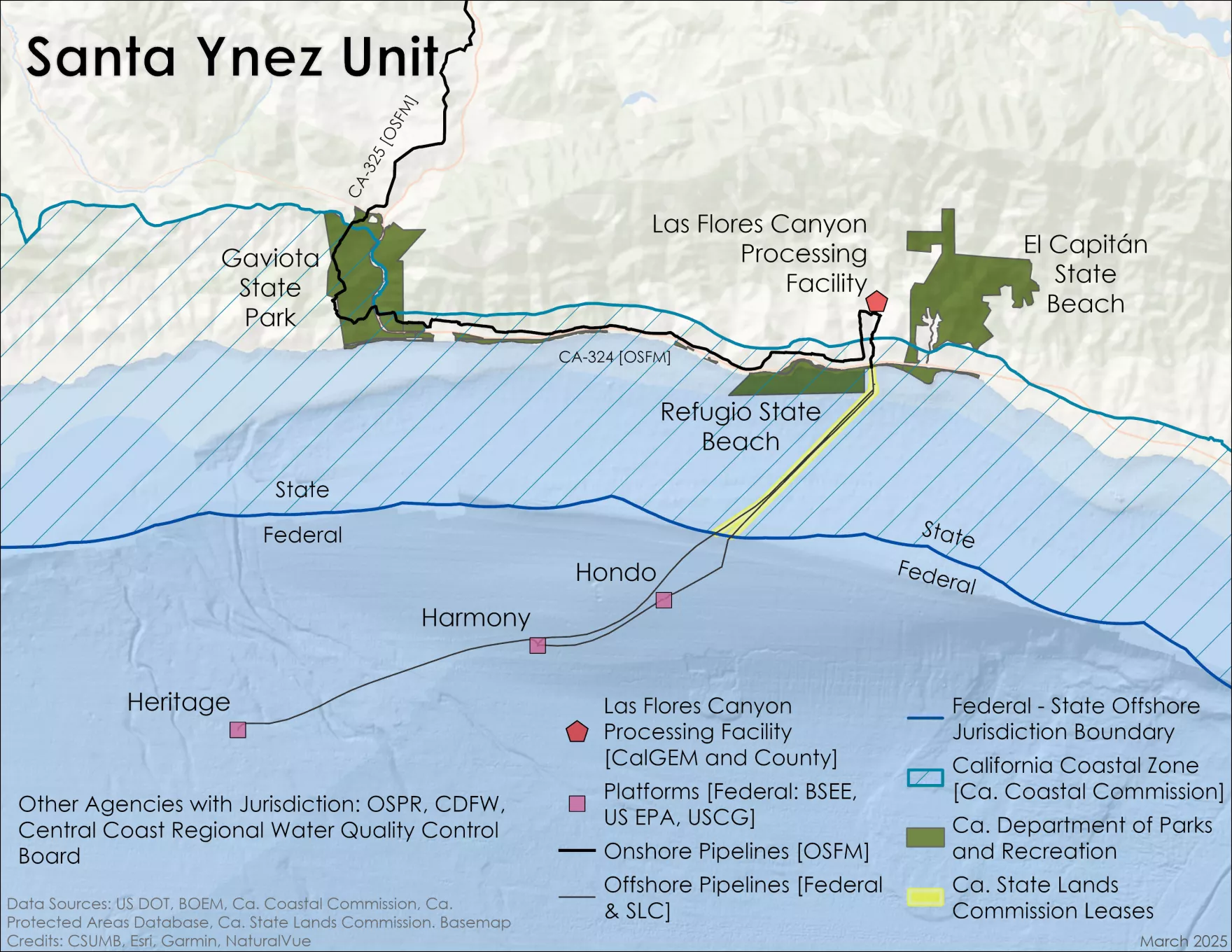

In the ongoing Santa Ynez Unit production restart saga, John Smith informs that a California Appellate Court ruled against Sable Offshore by a vote of 2-1, with a strong dissent from one of the three judges.

The decision (attached) affirms the California Coastal Commission’s regulatory authority over Sable’s Los Flores Canyon pipeline repairs, meaning that Sable could be ordered to cease operating the pipeline. However, this is just one element of a complex legal maze. An important case regarding PHMSA’s emergency special permit for the pipeline will be heard by the Federal 9th Circuit Court of Appeals in July.

The dissenting judge’s opinion beginning on p.15 of the attachment sets the stage for the upcoming arguments in the 9th Circuit. Excerpt:

“But first, a dose of reality. The repair work has been done. It is a “fait accompli.” And, pursuant to federal intervention, oil is now flowing in the pipeline without incident. The supremacy clause of the United States Constitution takes precedence. The federal Government trumped the state’s Commission “cease and desist” order and it trumps the preliminary injunction order. Based upon these events, the trial court should vacate the preliminary injunction, dismiss the matter as moot, and nullify the civil penalties.”

John Hancock Tower (pictured) is now named for its address, 200 Clarendon St

In the attached complaint, BP Hancock LLC alleges Vineyard Offshore, a Vineyard Wind parent company, is delinquent in paying rent for its space in the famous John Hancock Tower (now known as 200 Clarendon Street) in Boston.

Vineyard Wind had leased 28,370 square feet of space, constituting the entire eighteenth floor of the tower.

Per the complaint:

As of the date of this Complaint, Tenant owes Landlord $824,338.99 in Rent, Additional Rent, and late fees.

Furthermore, Tenant remains obligated to replenish the Security Deposit in the full amount of $386,810.00 as provided under Section 16.26 of the Lease.

As many of you know, Vineyard Wind is engaged in an ugly dispute with its primary contractor, GE Vernova, which was ordered to continue work on the project even though Vineyard Wind stopped making payments.

WASHINGTON –Today, the Department of the Interior announced a settlement agreement with affiliates of Invenergy, North America’s largest privately held developer, owner, and operator of independent power infrastructure, aimed at strengthening American security and lowering costs, advancing goals central to President Donald Trump’s Energy Dominance Agenda.

As part of the settlement agreement, Invenergy will voluntarily terminate its affiliates’ four offshore wind leases located in the New York Bight, Central Coast of California and the Gulf of Maine totaling $765 million, and redirect that amount towards other domestic energy sources with the demonstrated capability to deliver reliable, affordable power, including the development of natural gas-fired power plants in Indiana, Wisconsin, Iowa, Kansas, and Missouri and geothermal power generation projects in the Western U.S.

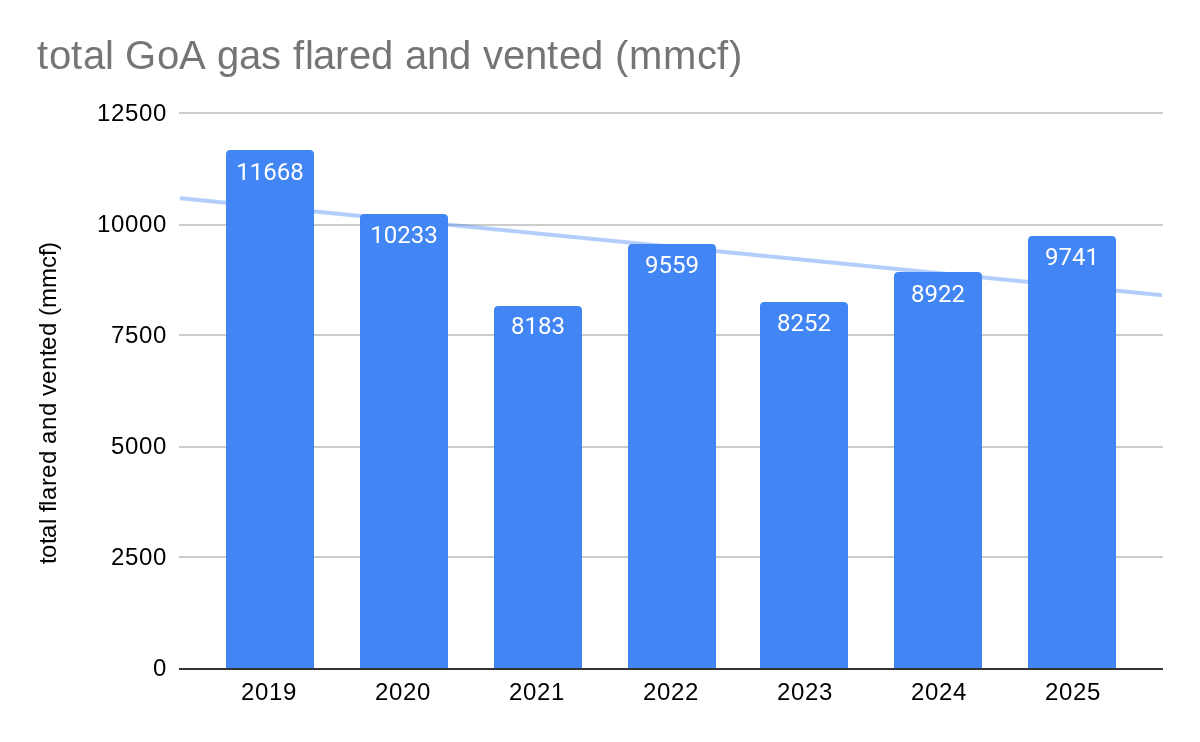

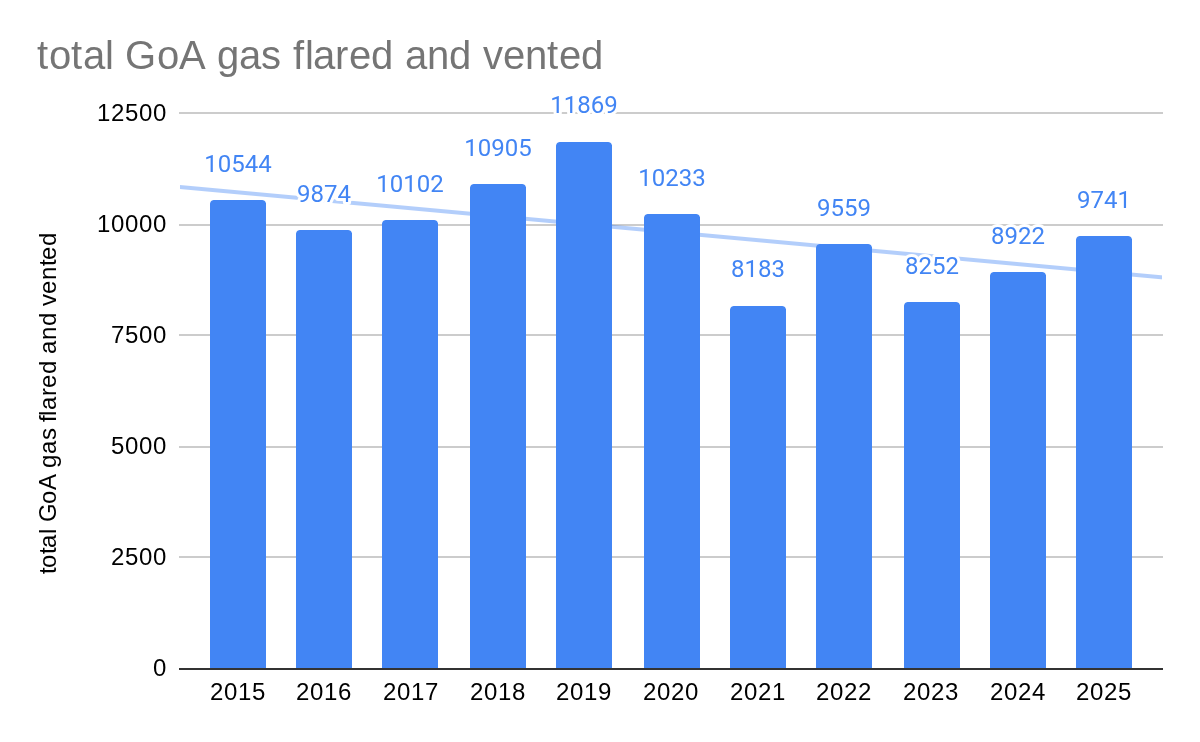

Minimizing flaring and venting is important from both environmental and resource conservation standpoints.Flaring and venting volumes are also good indicators of how well production systems are designed, managed, and maintained.

Updated flaring and venting volumes for the Gulf of America have been compiled using monthly data submitted to the Office of Natural Resources Revenue (ONRR). This is the best data source because reporting is mandatory and strictly enforced, and flaring and venting are accounted for separately.

Below are a few summary charts. Completed tables, similar to those posted for 2024, will be attached for sharing at a later date.

Total venting and flaring (fig. 1) in 2025 increased by 819 million cubic feet (mmcf) vs. 2024. However, the 7-year trend line is still favorable. Thinking that 2019, a record flaring year, may have biased the trend line, I extended the chart back to 2015, the first year for which I have ONRR data. As you can see in the second chart, the trend is still favorable.

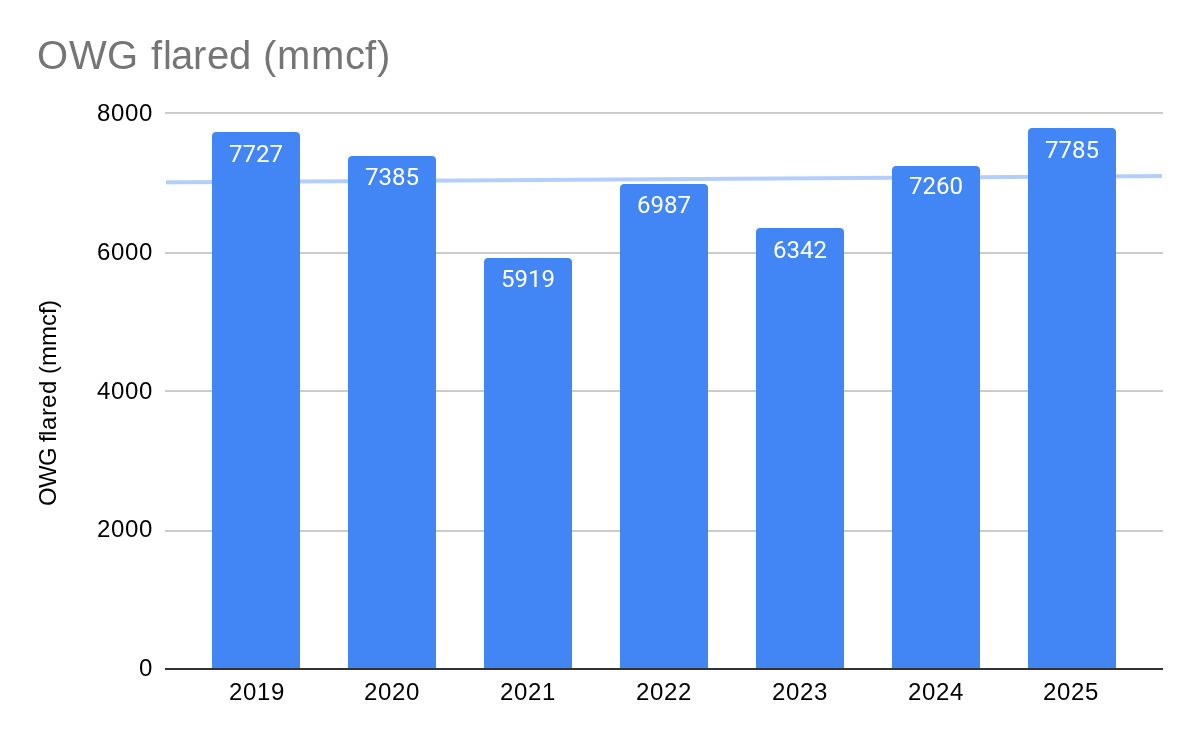

80% (7785 mmcf) of the total gas flared and vented in 2025 (9741 mmcf) was flared from oil wells (chart below). That’s unsurprising given that most of the Gulf’s gas production is from deepwater oil wells, and flaring rates are higher for oil wells than for gas wells.

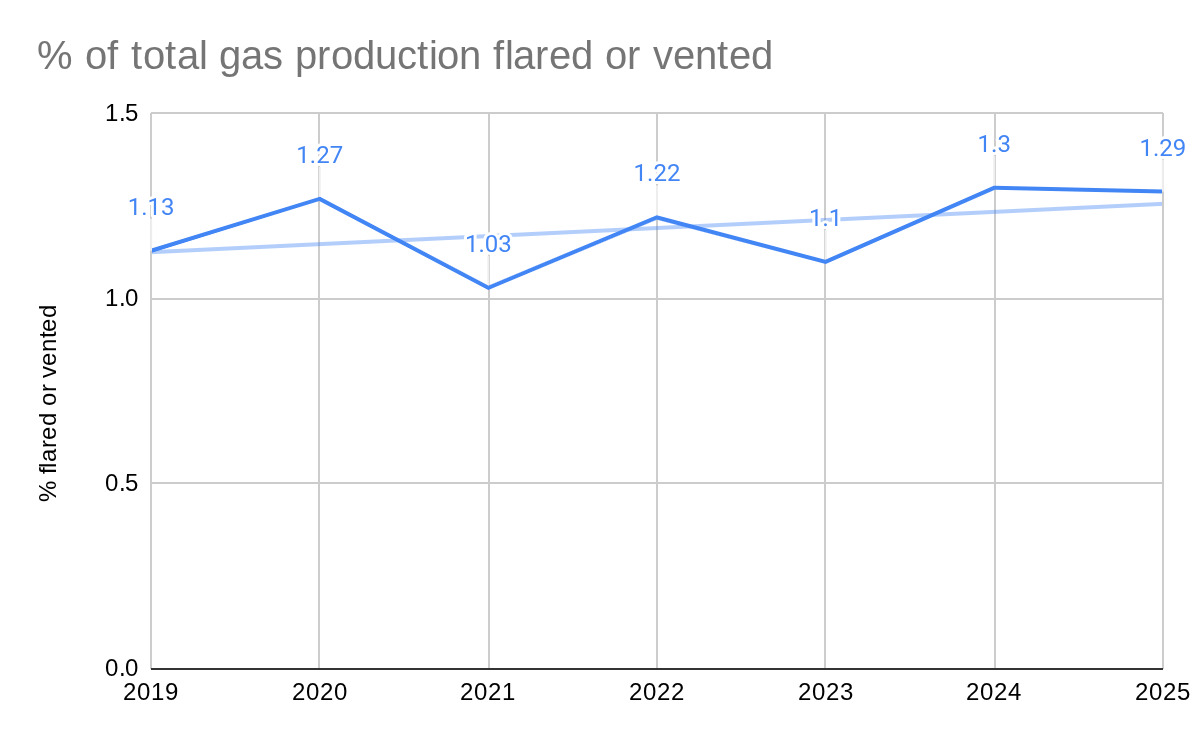

The best performance indicators are the normalized data (i.e. percentages of produced gas that are flared and vented both for oil wells and gas wells). Overall (chart below), flaring and venting volumes remain stubbornly above 1.0% of total gas production, the historical target last achieved in 2015. I’ll separate venting and flaring for both oil and gas wells in a future post.

The oil patch is known for booms, busts, mergers, and acquisitions. Hess is now among the once important offshore operators that no longer exist as separate companies. Others include Amoco, Arco, Texaco, Getty, Gulf, Unocal, Sun, Anadarko, BHP, Mobil, Phillips, Noble Energy, Pennzoil, Kerr-McGee, Superior, Nexen, and Newfield.

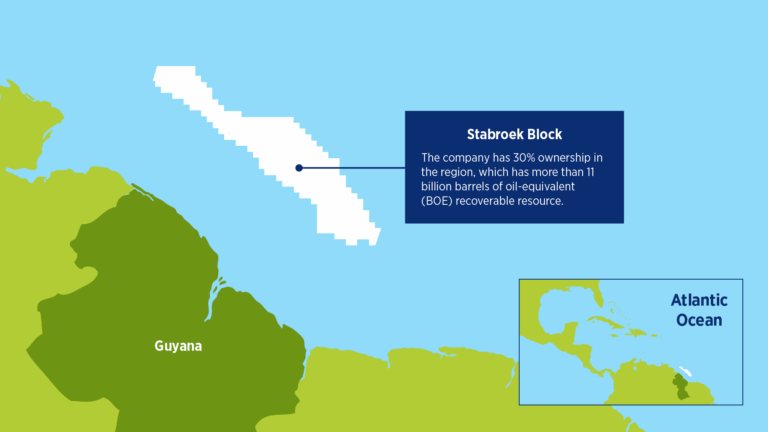

Hess would probably not have been a Chevron target had they not taken a chance in 2014 when they obtained a 30% position in Exxon’s Stabroek block offshore Guyana. The rest is history, and Stabroek is now the world’s most prized offshore block. Hess had other nice assets in the Gulf, Bakken Shale, and elsewhere, but Stabroek was Chevron’s primary target.

Hess was a safety compliance leader in both 2023 and 2024.

Hess was an active participant in pre-merger lease sales.

The combined company is unlikely to be greater than the sum of the parts in terms of US lease acquisition, exploration, and development.

Combining companies limits the diversity of geological assessments and exploration strategies.

Consolidation limits participation on committees engaged in assessing technology and developing standards. Declining industry participation in these activities, which are critical to offshore safety, has been a historical concern of OCS program leadership.

When the merger was announced, Chevron’s CEO Mike Wirth was quoted as saying “We’ve got too many CEOs per BOE, so consolidation is natural.” That comment makes sense from the perspective of an acquiring CEO. Employees of the companies being acquired have a somewhat different view. They would prefer increasing exploration and production rather than reducing employees.