WASHINGTON – Today, the Department of the Interior announced a settlement agreement with affiliates of Invenergy, North America’s largest privately held developer, owner, and operator of independent power infrastructure, aimed at strengthening American security and lowering costs, advancing goals central to President Donald Trump’s Energy Dominance Agenda.

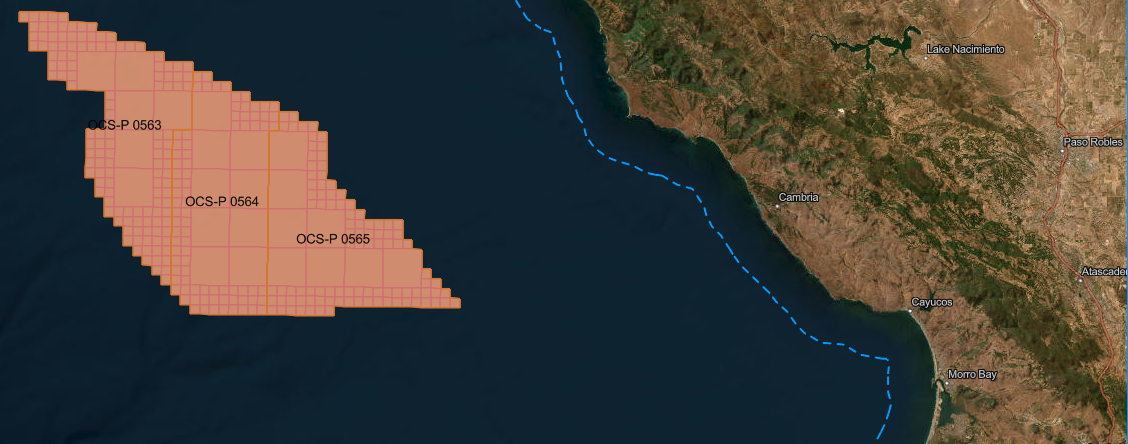

As part of the settlement agreement, Invenergy will voluntarily terminate its affiliates’ four offshore wind leases located in the New York Bight, Central Coast of California and the Gulf of Maine totaling $765 million, and redirect that amount towards other domestic energy sources with the demonstrated capability to deliver reliable, affordable power, including the development of natural gas-fired power plants in Indiana, Wisconsin, Iowa, Kansas, and Missouri and geothermal power generation projects in the Western U.S.