Equinor has cut planned investments in renewable energy by roughly EUR 3.5bn for 2026–2027, while the company maintains and expects growth in oil and gas production.

Cheap shot from panicked Ørsted investor:

“From a sustainability perspective, it’s certainly sad that one of the most ‘green’ fossil fuel companies now turns out to have merely been a ‘tourist’ in the green sector, but unfortunately, that’s just the way things are these days,” says Anders Schelde, investment chief at AkademikerPension, according to Finans.

Perhaps the premium for climate virtue signaling has shrunk, and Equinor, like other energy giants, is making a prudent business decision for its shareholders, which include the Norwegian govt.

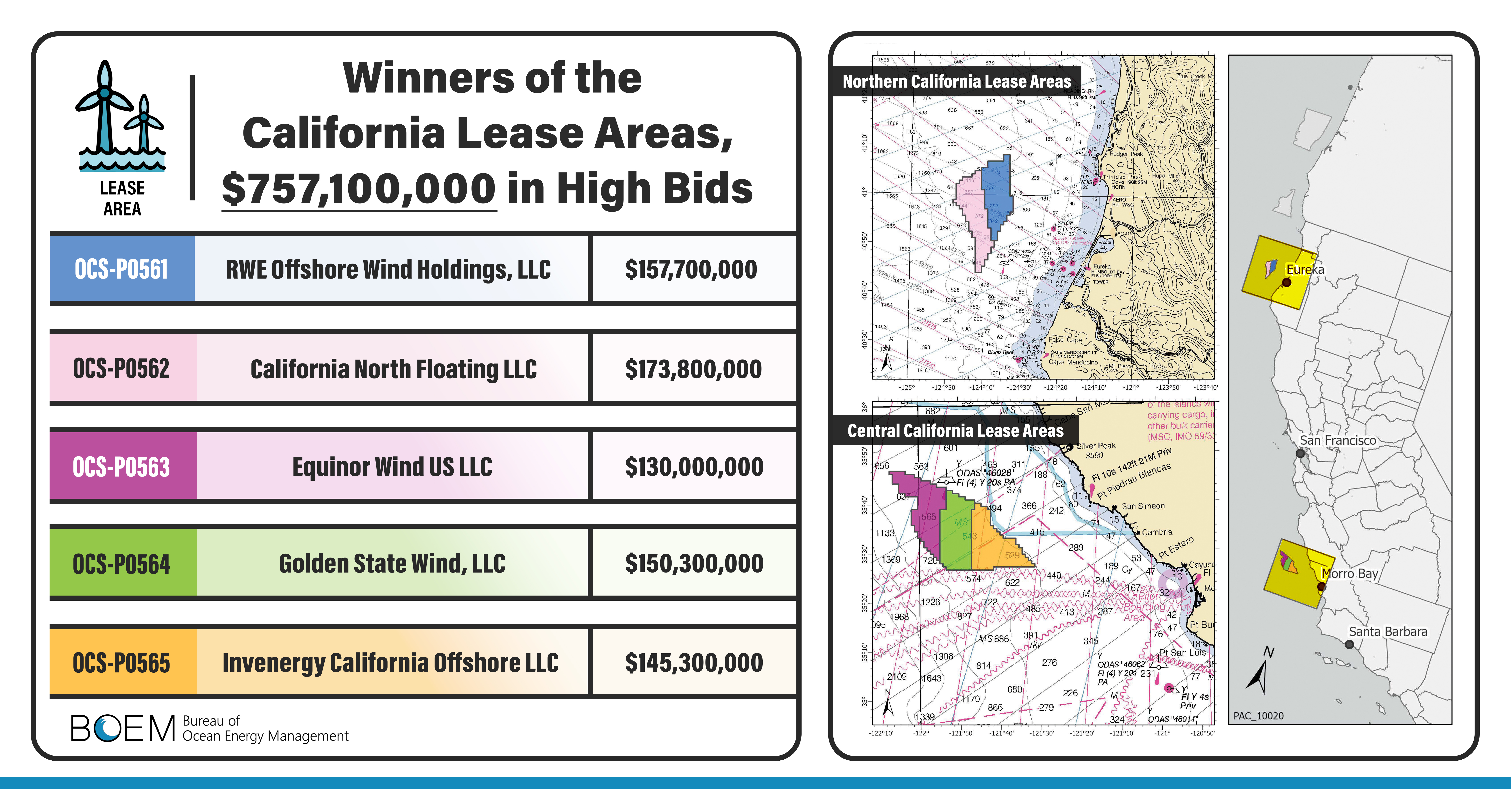

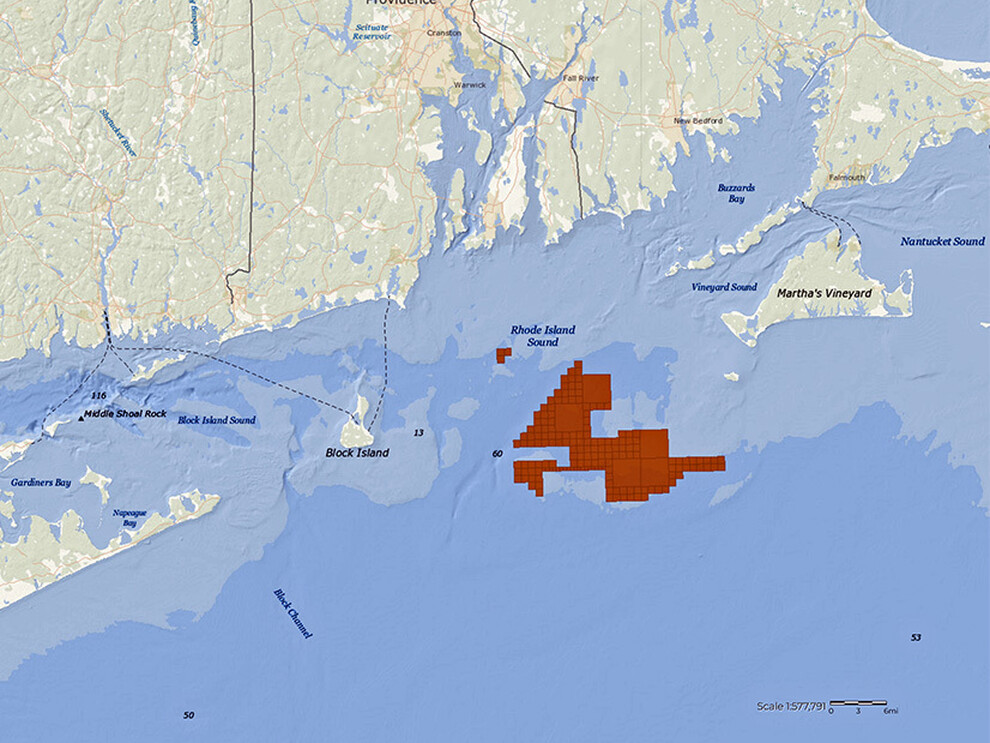

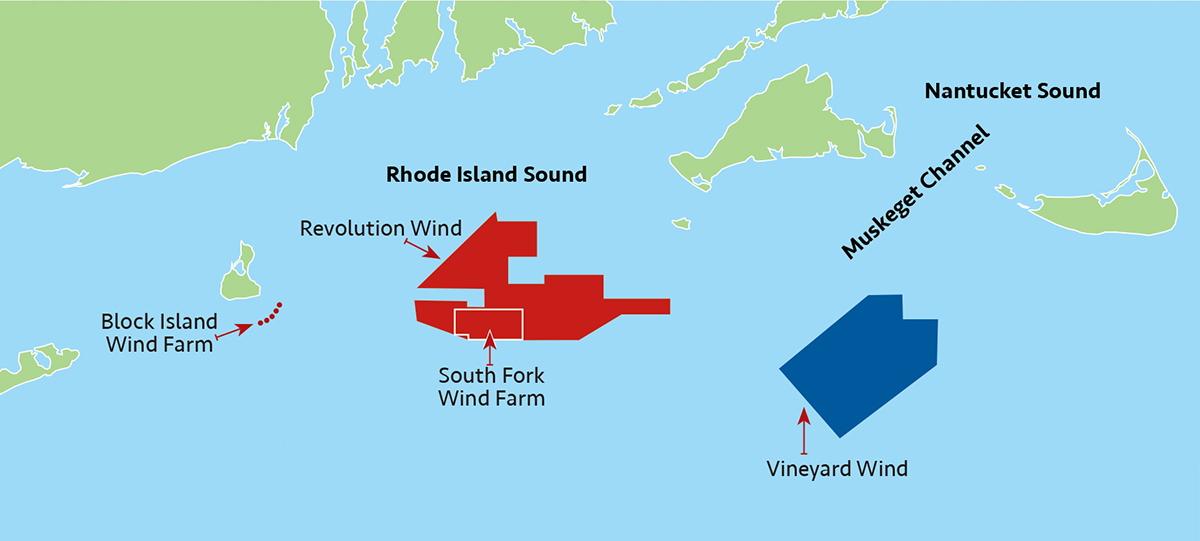

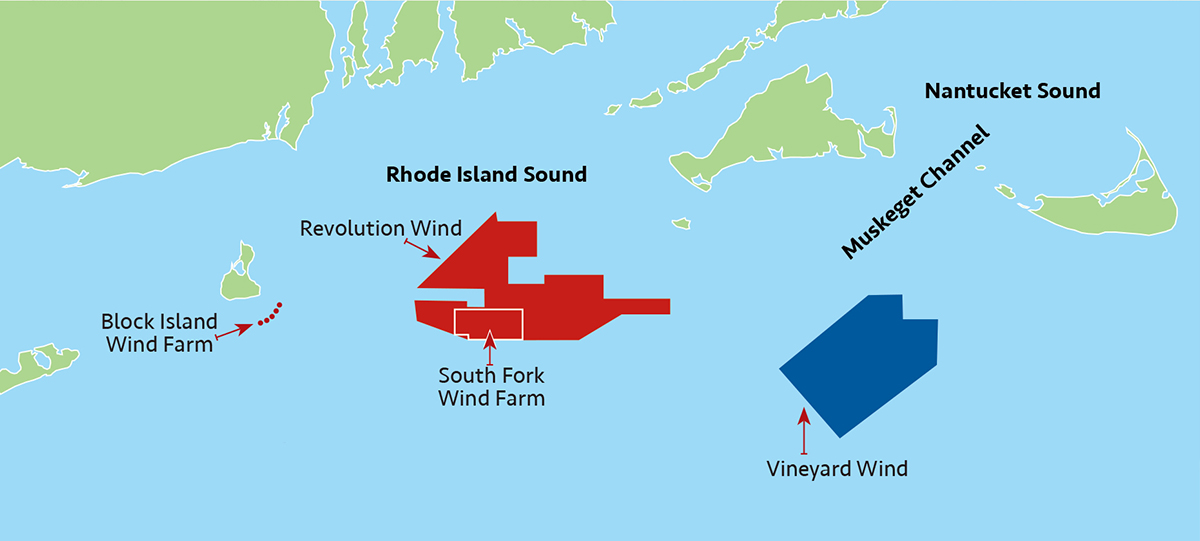

Meanwhile, what are the implications for Equinor’s offshore wind investments in the US? Equinor’s embattled Empire Wind project is probably too far along to reverse course. Their Central Atlantic (Lease 0557) and California (Lease 0563, Atlas Wind) may be a different story. However, buyback negotiations would be complicated by the Empire Wind situation, and perhaps by the Norwegian government’s 2/3 ownership. On the other hand, Equinor is a significant oil and gas leaseholder in the Gulf of America, so they would have ample options for investing wind lease rebates.