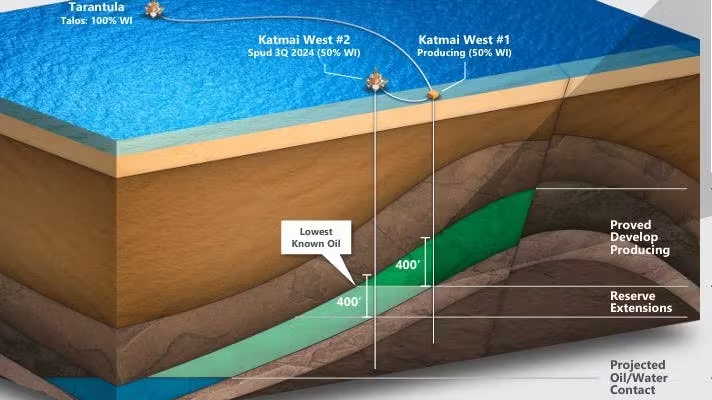

Talos announced successful drilling results at the Daenerys prospect (Katmai West #2) in the Gulf of America (Walker Ridge blocks 106, 107, 150, and 151).

Daenerys is a good example of the evolution of deepwater project ownership, which was once exclusively the domain of major international oil companies. Over the past 20 years, participation by independents increased gradually, followed by smaller independents and informed investment companies.

Impressively, the Daenerys partnership (table below) includes a tribe that has the same % ownership as a super-major, and a highly efficient investment company owned by a single person.

Talos (operator)

large US independent

27.0% share

Shell

international supermajor

22.5%

Red Willow

private company owned by the Southern Ute Tribe

22.5%

Houston Energy

private independent focused on deepwater energy resources

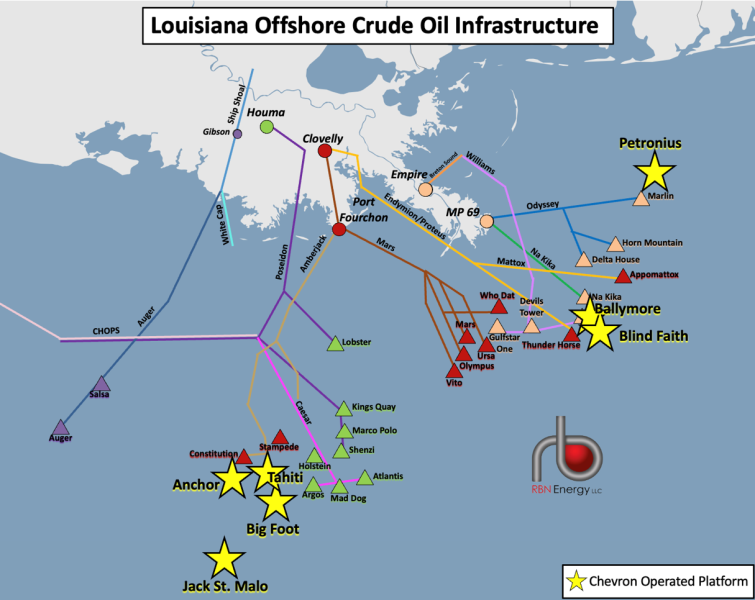

Reuters and others report that zinc from a new Chevron well has contaminated oil production destined for an Exxon refinery via Shell’s Mars Pipeline System. Because contaminated crude may cause maintenance issues and reduces the quality of refined products, Exxon will not accept crude from the Mars system until the zinc issue has been resolved.

The Mars system delivers about 575,000 bopd raising concerns about supplies to Gulf Coast refineries. But fear not, DOE authorized the delivery of up to 1 million barrels of oil from the Strategic Petroleum Reserve to the Exxon’s Baton Rouge refinery.

(Ironically, yesterday’s post pointed to the importance of the SPR and questioned the decision to drastically reduce crude oil purchases. This zinc incident is likely to be minor, and Exxon will repay the SPR in kind. However, more serious regional, domestic, and international events could call for much greater SPR withdrawals.)

The above map shows Chevron platforms that connect with the Mars system at Port Fourchon.

Speculation/commentary:

The well/platform responsible for the zinc contamination has not been identified. Given that production is ramping up at Chevron’s Anchor facility, a new well on that platform may be the source of the zinc. Other Chevron platforms that connect to the Mars system are indicated in the diagram above.

Given that zinc in crude oil is rare, a well completion fluid containing zinc bromide may be the culprit.

Note the integration of offshore production streams, and the involvement of 3 industry super-majors. These companies are highly competitive, as evidenced by the Chevron-Exxon Stabroek dispute, but are also cooperative in producing, transporting, and refining oil and gas. However, they and other majors are restricted (rather illogically) from bidding jointly for leases.

Colette Hirstius, currently Executive Vice President, Gulf of America, will take on the responsibility of President, Shell USA, in addition to her current role as Executive Vice President, Gulf of America, effective August 1, 2025.

In a city where high school ties tend to be strong and enduring, Ms. Hirstius is a graduate of St. Mary’s Dominican HS. Supreme Court Justice Amy Coney Barrett, whose father was an attorney for Shell, and my former Minerals Management Service colleague Kathy Swiler, are also St. Mary’s Dominican graduates.

Ms. Hirstius stayed in New Orleans as an undergraduate, receiving a B.S. degree in geology from Tulane.

Shell is the no. 1 oil and gas producer in the Gulf of America. In 2024, the company produced 171.7 million bbls of oil (26.2% of the GoA total) and 167.4 bcf of gas (24.4% of the GoA total).

Farther in the past, there were noteworthy failures (below) like Mobil’s acquisition of Montgomery Ward, Exxon’s investment in Reliance Electric, and Gulf’s real estate ventures.

Mobil – Montgomery WardExxon – Reliance ElectricGulf Land – Reston

Finally, don’t expect the carbon sequestration boom that some are forecasting. As wind investors have discovered, industries dependent on mandates and subsidies are risky.

Not much unites climate activists and skeptics, but they are largely aligned in their opposition to carbon sequestration (euphemism for disposal), as are fiscal conservatives. The word chutzpah comes to mind when companies seek public funds to dispose of emissions associated with the combustion of their products.

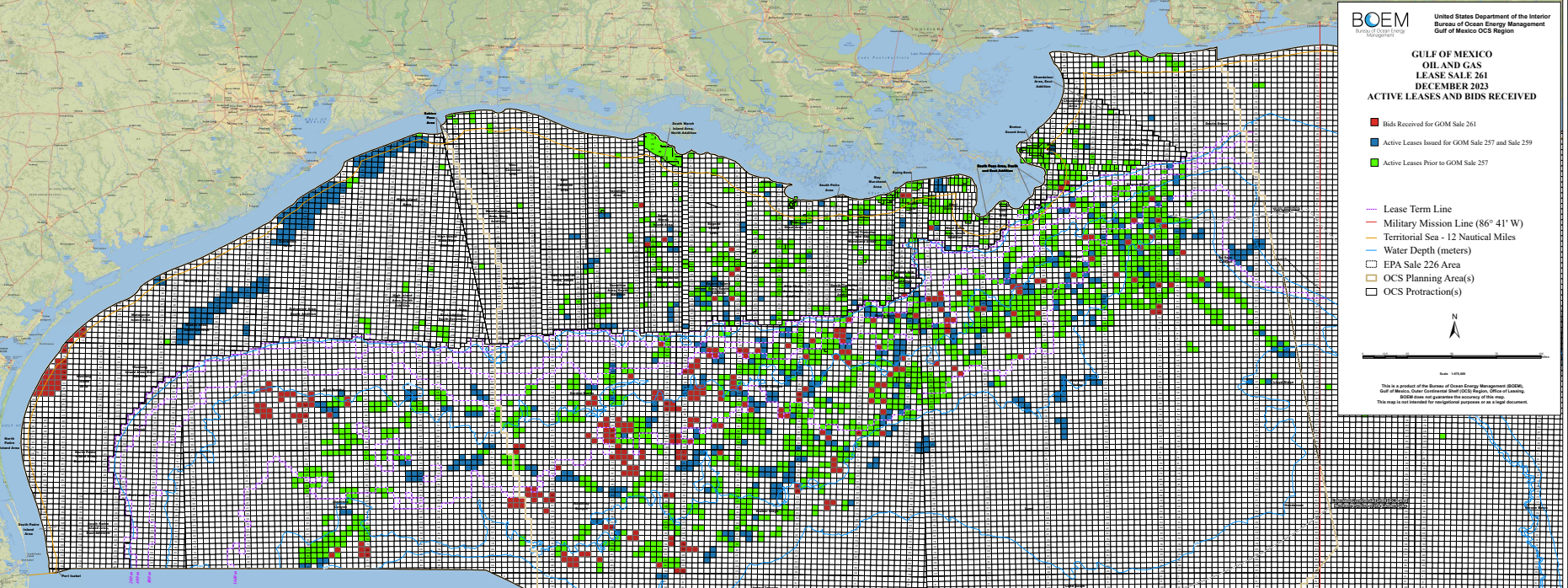

199 oil and gas leases were wrongfully acquired at Sales 257, 259, and 261 with the intent of developing these leases for carbon disposal purposes. Repsol was the sole bidder at Sale 261 for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

In the case of the Rosebank and Jackdaw fields, Lord Ericht ruled that the environmental assessment must take into account the climate effect of downstream emissions resulting from the consumption of oil and gas produced at those fields.

The Sale 257 decision was even more extreme in that Judge Contreras ruled that BOEM failed to consider the “positive” effect that higher prices (which might result from lower US offshore production) would have in reducing worldwide demand and the associated GHG emissions.

Regardless of one’s opinion on the extent to which GHGs affect the climate, halting UK and US projects will have virtually no effect on international oil and gas demand. That demand will be satisfied by other suppliers who will reap the economic benefits.

Presumably, revised environmental assessments, will allow the previously approved UK projects, for which some facilities have already been constructed and installed, to go forward. The UK government has been considering how to calculate downstream emissions. The model will no doubt yield outcomes that are highly uncertain.

In the meantime, the UK sector of the North Sea, unlike its Norwegian counterpart, continues to flounder.

“We need more of it because even the most ardent supporters of renewable energy, the most vocal proponents of net zero, quietly admit oil and, especially, gas will be needed for a couple of decades at least. That obvious truth, that inarguable necessity, is not, apparently, enough for ministers to encourage UK production, however, or temper their rhetoric around renewables.“

“Allowing our rigs and refineries to power down and relying on other countries to keep the lights on still seems a little, well, counter-intuitive. We will import oil and gas but not produce it while happily exporting contracts, skills and jobs overseas? The practical impact of Labour’s refusal to grant new exploration licences in the North Sea might remain unclear but the message it sent was absolutely crystal.“

estimated peak production:100,000 barrels of oil equivalent per day (boe/d)

water depth – 8600 ft

200 miles south of Houston

estimated recoverable resource: 480 million boe.

first oil only 7.5 years after discovery (includes COVID delay)

Vito clone: replicates 99% of the hull design and 80% of the topsides from Vito.

high efficiency gas turbines and compression systems

~ 30% lower greenhouse gas (GHG) intensity over its life cycle than the already efficient levels being achieved at Vito. (Why the push to run electric cables from shore to North Sea platforms with ample gas production?)

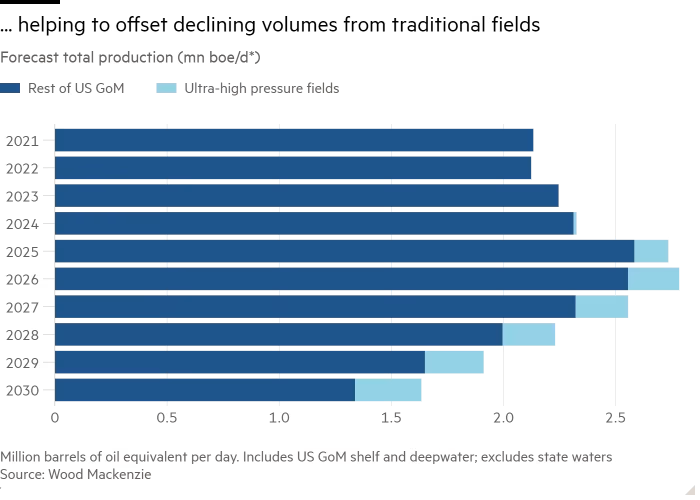

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded in this post.)

Four of the five simpler, safer, greener deepwater platforms featured on this blog are now producing. The 5th platform (Whale) is on location and scheduled to begin production later this year.

platform

operator

first production

King’s Quay

Murphy

April 2022

Vito

Shell

Feb 2023

Argos

bp

April 2023

Anchor

Chevron

Aug 2024

Whale

Shell

late 2024

These platforms are in 4000 to 8600′ of water, are expected to reach peak production rates of 100-150,000 boe/day, and have favorable emissions characteristics on a per barrel basis.

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded below.)

Chevron’s Anchor is the first deepwater, high-pressure development. Three similar deepwater hub platforms (table below) will begin production over the next 5 years. These host platforms will also facilitate additional production from nearby fields. Each will have production capacities of approximately 100,000 boe/day. Note the long lead times in achieving first production given the technological issues that had to be evaluated and addressed.

platform

operator

discovery date

first production

Kaskida

bp

2006

2029

Sparta

Shell

2012

2028

Shenandoah

Beacon

2009

2025

Wood Mackenzie sees these high pressure projects as the key to sustaining GoM production rates. Their projections for 2024 and 2025 seem optimistic based on 2024 YTD data, which adds to the importance of the projected new production.

Some of us remember the Brent Spar saga (1995). The subsequent Brent field decommissioning activities have been less controversial, including the removal of the Brent C topsides on July 9. The Allseas single lift technology is most impressive. Check out the video!

Canadian and US approvals were granted and CNOOC acquired Nexen (Canada) in 2013.

Nexen’s Guyana interest was not mentioned in the press announcement, and appears to have been a rather minor consideration in the acquisition.

So, an apparent afterthought in CNOOC’s takeover of Nexen has (1) proven to be extremely profitable, (2) given the company and the Chinese government leverage in the Exxon-Chevron supermajor dispute, and (3) opened the door for CNOOC to increase their interest in the massive Stabroek field.