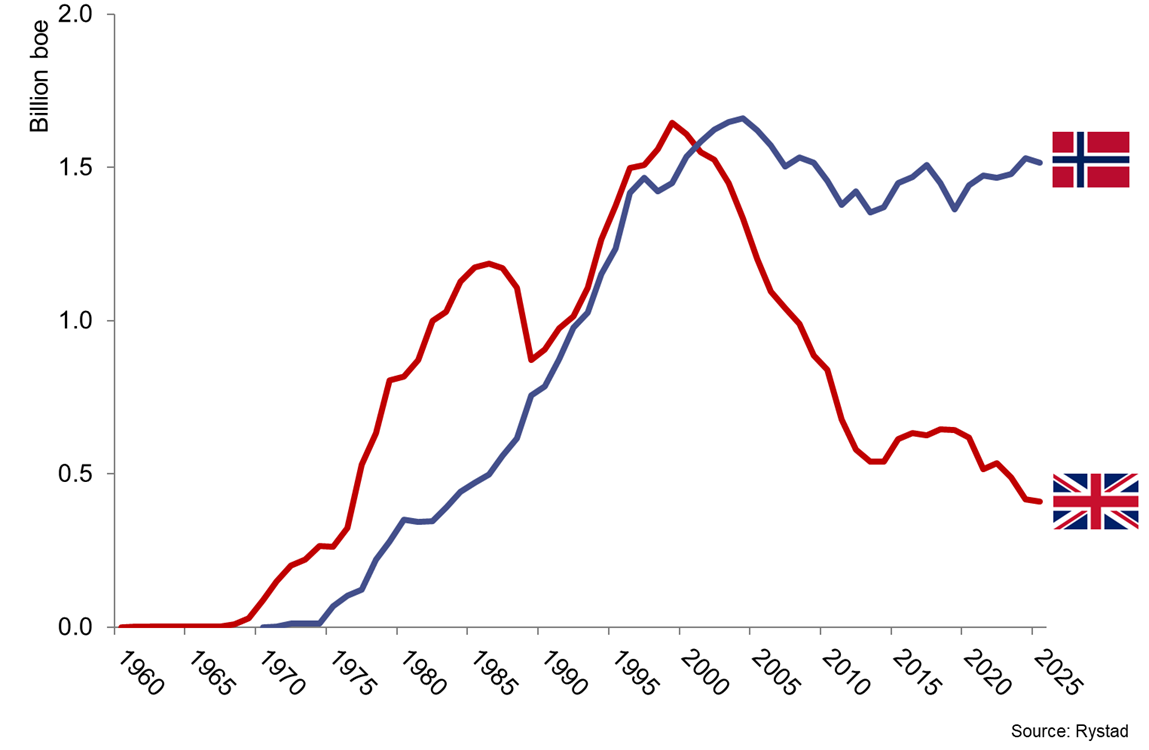

Some of us remember when the UK and Norway were friendly North Sea oil and gas rivals – competing to be tops in production, technology, safety, and even promotion at conferences like OTC. Take a look at the production chart below and note the UK’s production leadership followed by the extraordinary decline.

So what happened? Norway may have better oil and gas resource potential, but that is only part of the story. While Norway was managing their offshore sector to succeed, the UK was seemingly managing theirs to fail.

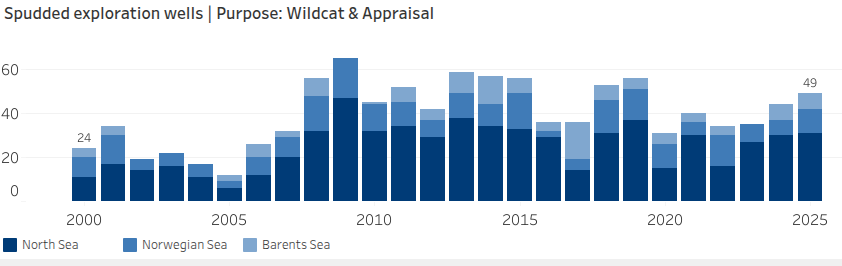

Norway’s North Sea remains far more active because the government promotes exploration through predictable licensing, cost-recovery incentives, and a focus on adding resources to existing infrastructure.

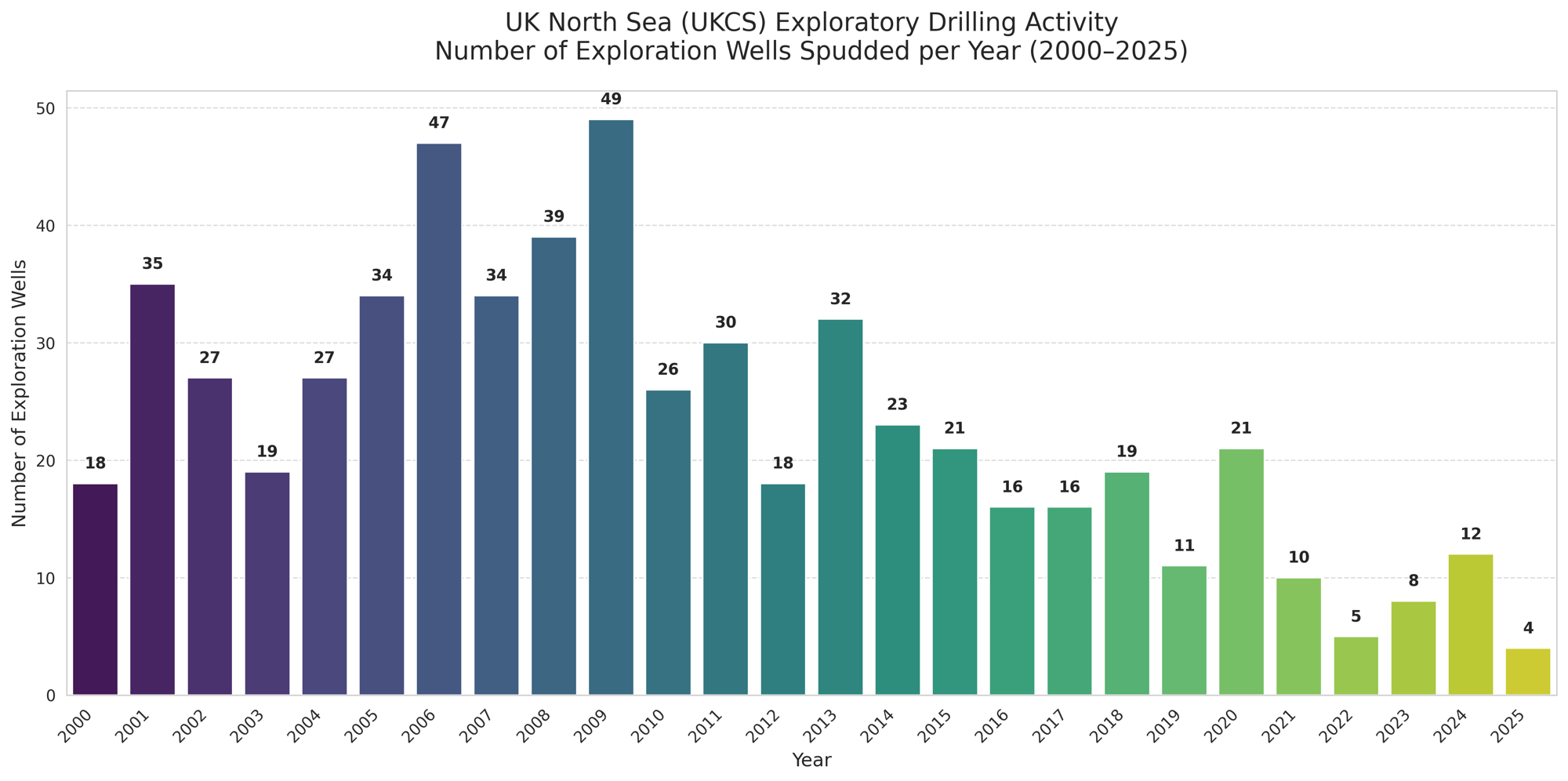

The UK, by contrast, has shifted toward limited development and decommissioning. In recent years, the UK’s windfall tax on oil and gas profits was raised to 78 percent, and licences for exploratory drilling in new areas were banned.

In 2022, the UK government even changed the name of the Oil and Gas Authority to the more trendy North Sea Transition Authority. (Changing names is one thing; delivering reliable energy at reasonable prices is quite something else.)

The stark policy differences are evident in the exploration drilling numbers – sustained drilling vs. sustained decline (charts below).

JL Daeschler shared this excellent response by Natalie Coupar (excerpts below) to tired anti-exploration arguments that are popular in the UK and elsewhere:

“Claim: Hundreds of North Sea licences have delivered only “36 days of gas”, proving new drilling does not improve energy security.

“This actually proves the opposite. In a mature basin like the North Sea, you need a constant churn of investment and new licences just to stand still. Without ongoing activity, decline accelerates and import dependence rises faster. That is why countries like Norway continue to license and develop new projects. Their approach allows them to replace what they produce and manage decline more effectively. In industry terms, this is measured through the reserves replacement ratio – how much new resource is added compared with what is produced. Norway consistently produces a higher reserves replacement ratio than the UK. Over the 5 year period 2019-2024, through exploration, Norway replaced on average 46% of the reserves that were produced, the UK however, replaced just 14%.“

“Today, the North Sea still provides over half of the UK’s oil and gas needs. With the right conditions, we can sustain production for longer, reduce exposure to imports, and manage the transition more securely. Without licensing and investment, the UK simply becomes reliant on overseas supplies sooner – regardless of demand falling.“

Claim: 93% of UK North Sea oil and gas has already been extracted, so new drilling makes little difference.

“Official projections show several billion barrels of oil and gas still expected to be produced between now and 2050. Independent analysis commissioned by OEUK shows that, with the right conditions, significantly more could be delivered from known projects and discoveries.“

“And even beyond that, the UK’s own regulator identifies large volumes of oil and gas in:

- approved projects

- existing discoveries

- areas that haven’t yet been developed“

Pressure is mounting on the UK govt to approve the Rosebank and Jackdaw projects and ease exploration restrictions. Will it work?