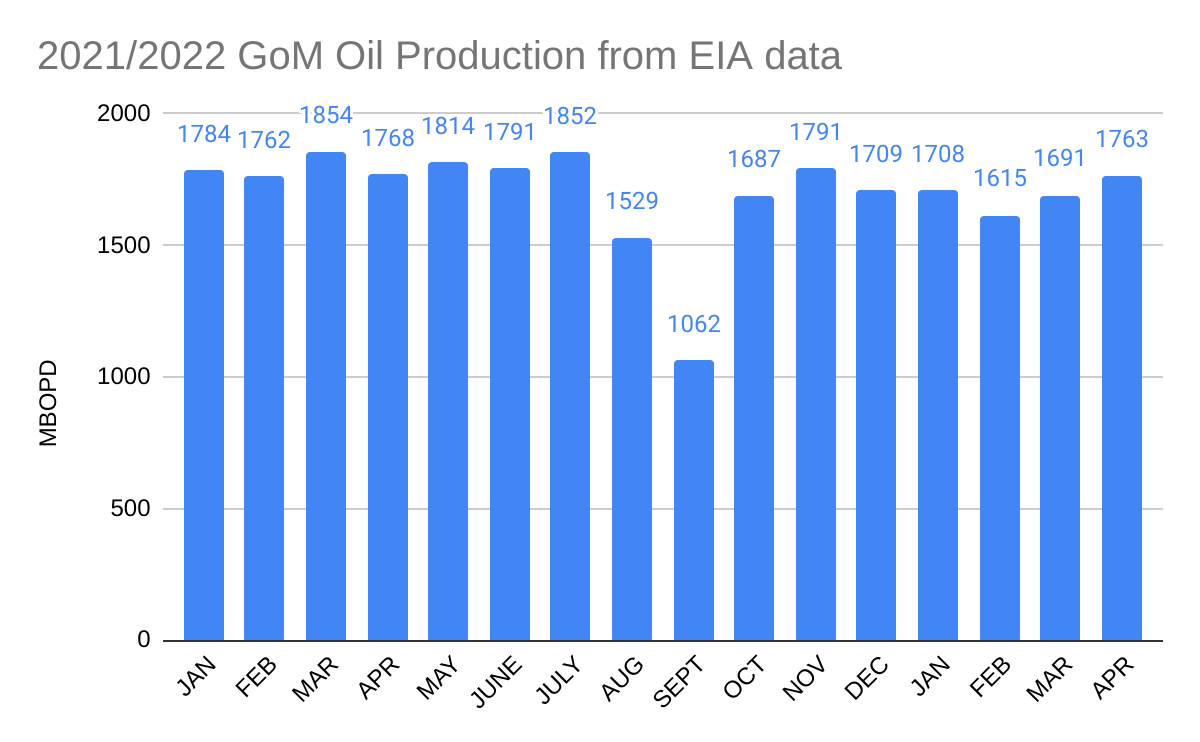

Four of the five simpler, safer, greener deepwater platforms featured on this blog are now producing. The 5th platform (Whale) is on location and scheduled to begin production later this year.

| platform | operator | first production |

| King’s Quay | Murphy | April 2022 |

| Vito | Shell | Feb 2023 |

| Argos | bp | April 2023 |

| Anchor | Chevron | Aug 2024 |

| Whale | Shell | late 2024 |

These platforms are in 4000 to 8600′ of water, are expected to reach peak production rates of 100-150,000 boe/day, and have favorable emissions characteristics on a per barrel basis.

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded below.)

Chevron’s Anchor is the first deepwater, high-pressure development. Three similar deepwater hub platforms (table below) will begin production over the next 5 years. These host platforms will also facilitate additional production from nearby fields. Each will have production capacities of approximately 100,000 boe/day. Note the long lead times in achieving first production given the technological issues that had to be evaluated and addressed.

| platform | operator | discovery date | first production |

| Kaskida | bp | 2006 | 2029 |

| Sparta | Shell | 2012 | 2028 |

| Shenandoah | Beacon | 2009 | 2025 |

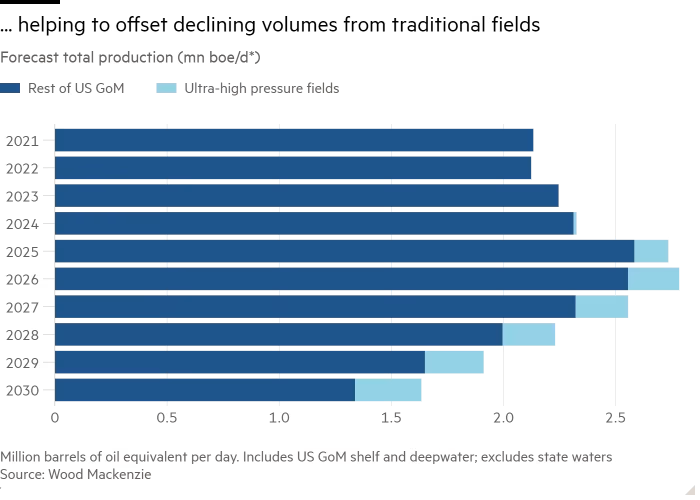

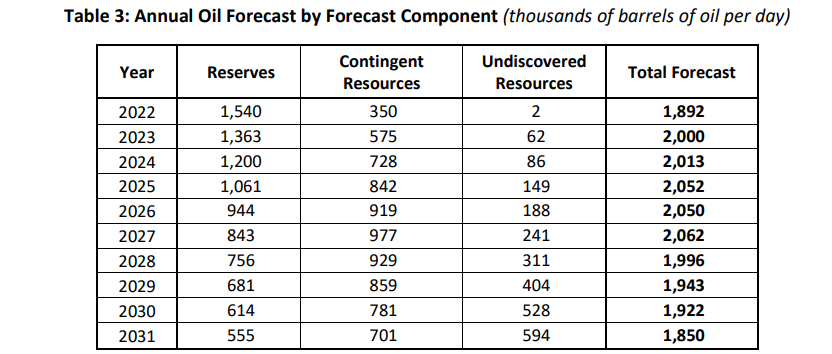

Wood Mackenzie sees these high pressure projects as the key to sustaining GoM production rates. Their projections for 2024 and 2025 seem optimistic based on 2024 YTD data, which adds to the importance of the projected new production.