BOEM Press Release: “The Bureau of Ocean Energy Management announced today the critical role of offshore leasing, resource assessment and long-term planning in supporting record oil production on the U.S. Outer Continental Shelf, which reached more than 714 million barrels in 2025.”

Was 2025 a record OCS oil production year? No, 2025 came very close, but barring belated revisions, 2019 retains the record.

Did 2025 oil production exceed 714 million barrels? Not even close according to the US Energy Information Administration (EIA), which reported a final OCS production total of 692.6 million barrels for 2025. The Office of Natural Resources Revenue (ONRR), to whom all production data must be reported, has yet to post their final 2025 numbers, but they are normally very close to the EIA totals. Also, ONRR’s fiscal year totals do not suggest calendar year production in excess of 700 million barrels. BOEM’s announced 714 million barrel CY 2025 total is more than 60,000 bopd higher than the actual EIA CY or ONRR FY daily averages, and even exceeds the total posted in BOEM’s data center.

See the 2019 and 2025 oil production totals in the table below. The BOEM 2025 numbers appear to be erroneous.

| Oil Production (includes condensate in all cases) | 2019 | 2025 |

| Gulf of America OCS | ||

| ONRR | 692,681,303 | not yet posted; fiscal year total was 681,760,441 |

| EIA | 692,831,000 | 692,634,000 |

| BOEM | 693,004,577 | 707,847,938 |

| All OCS including Pacific & Alaska | ||

| ONRR | 697,610,350 | not yet posted; fiscal year total was 686,544,402 |

| EIA | 697,217,000 | 697,020,000 |

| BOEM | 697,933,210 | 712,543,491 |

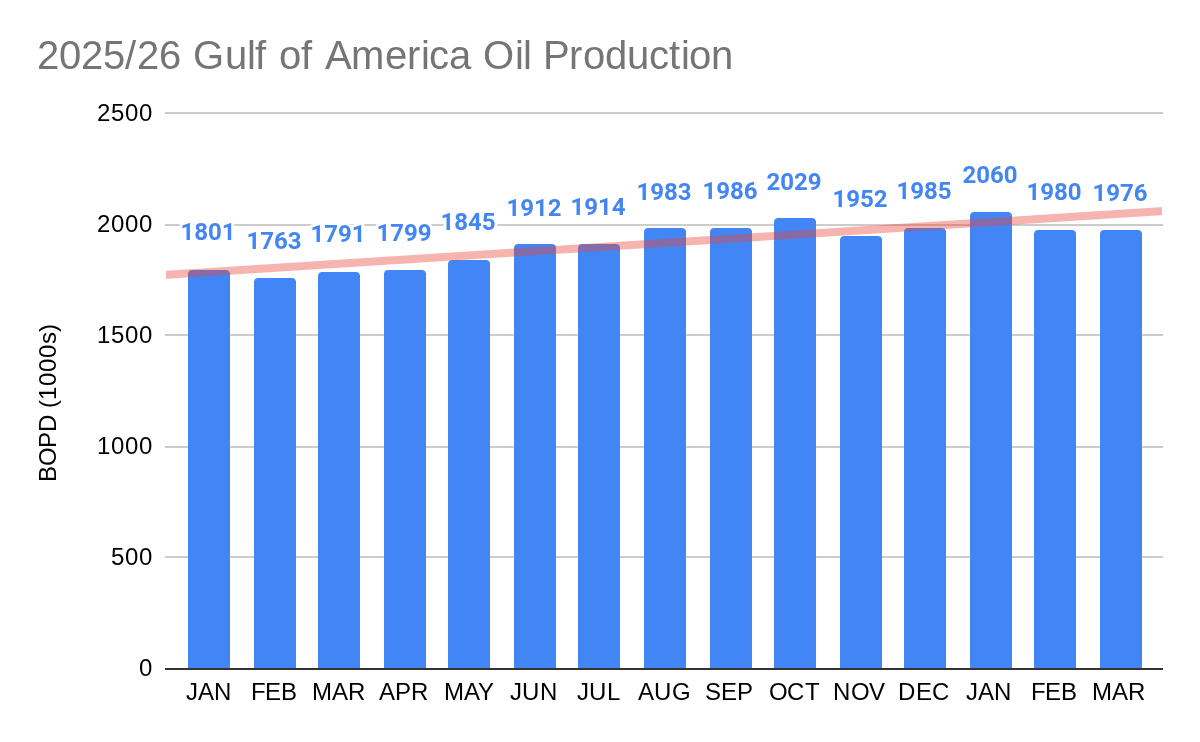

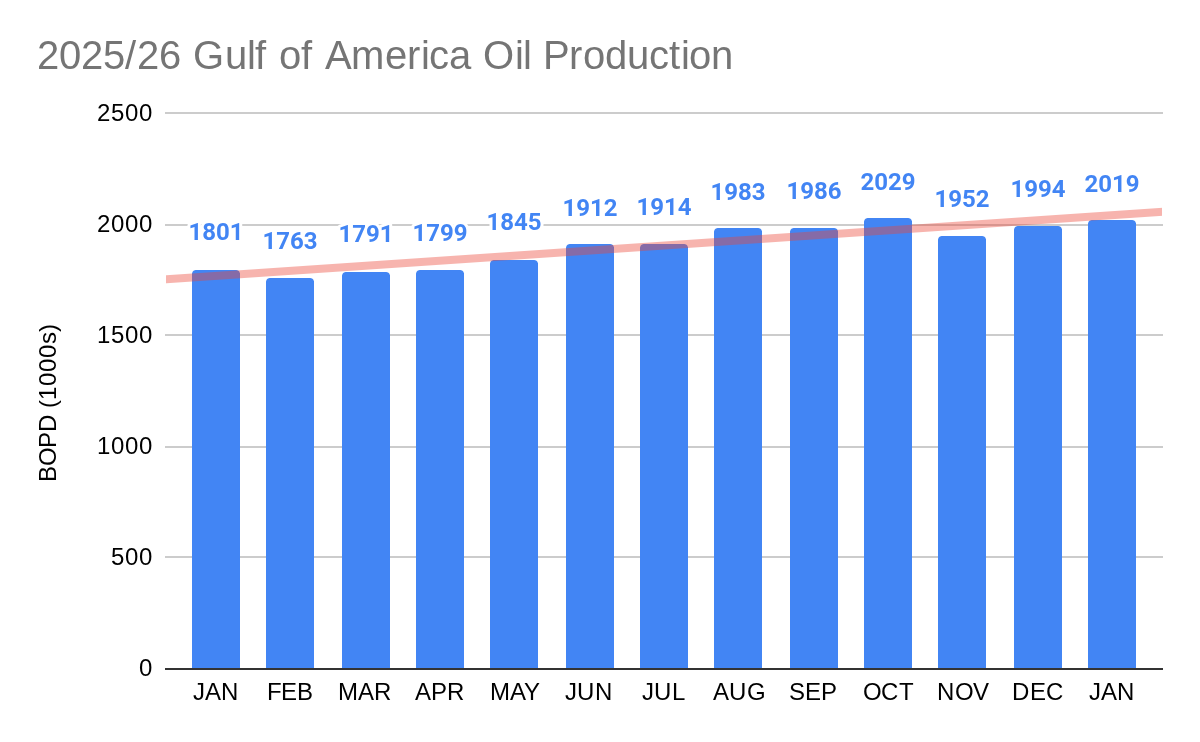

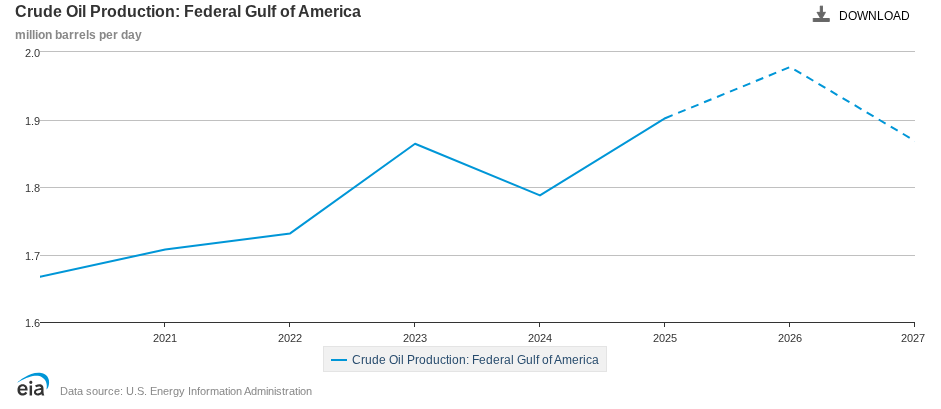

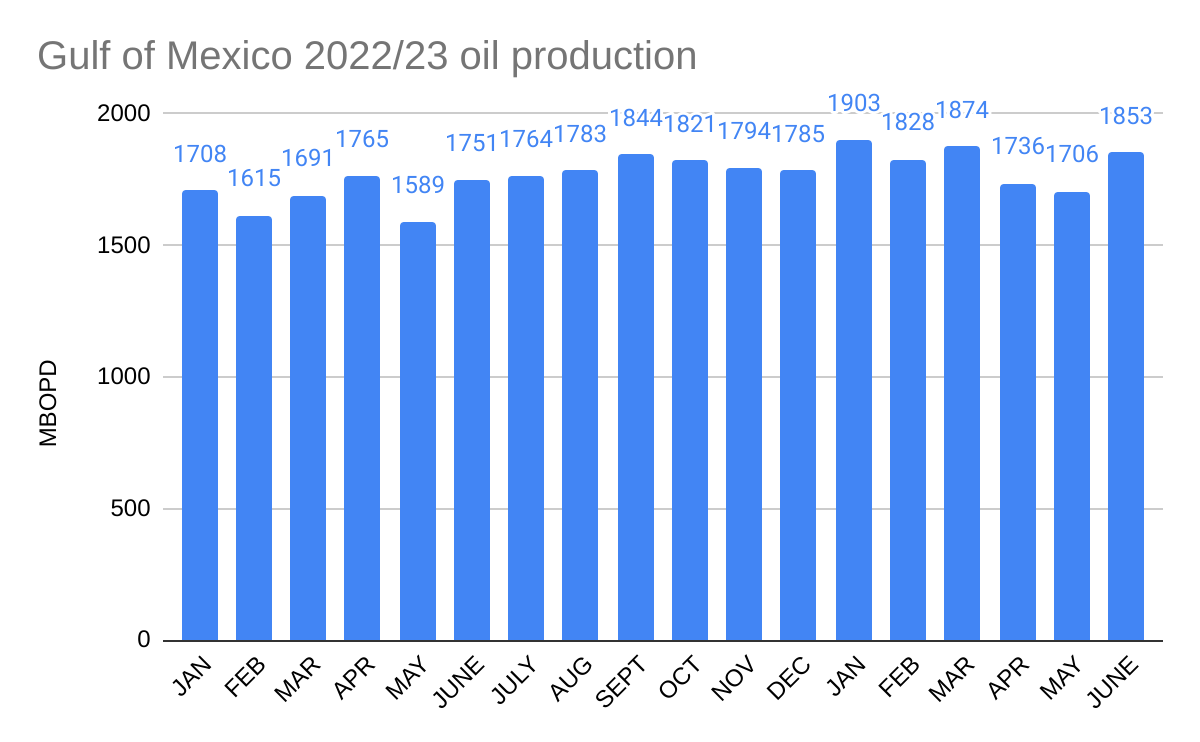

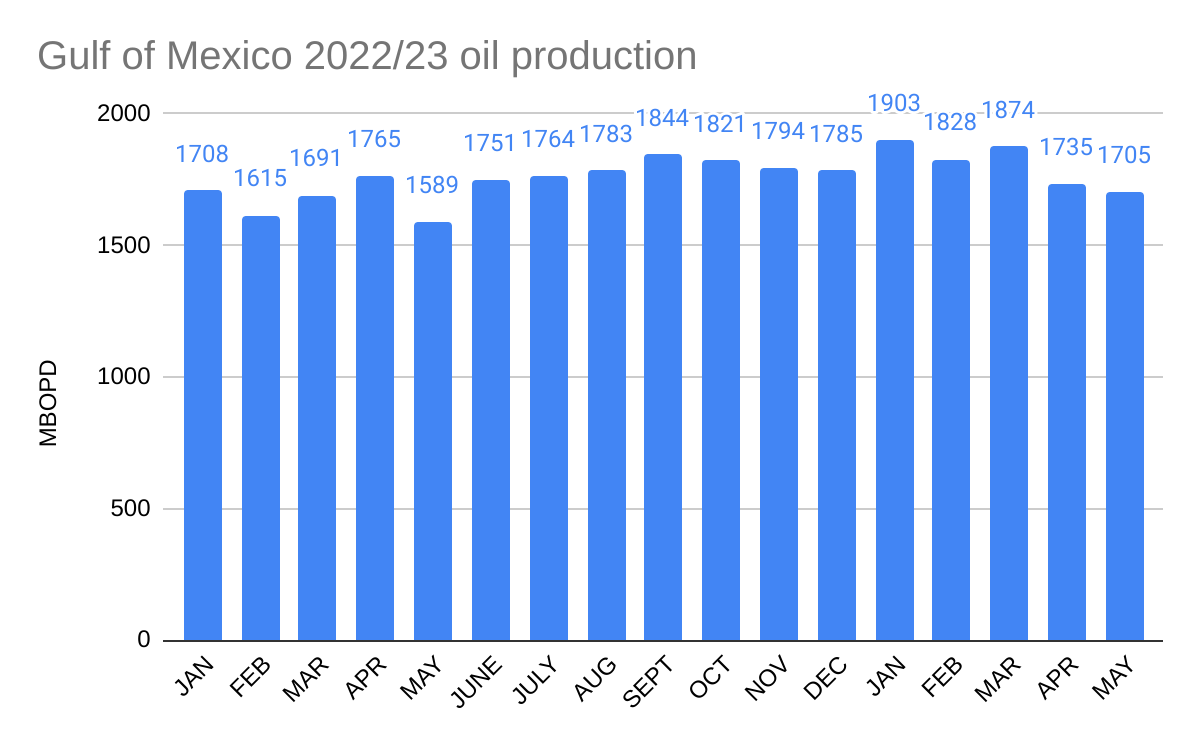

On the plus side, per EIA’s latest update, Jan. 2026 was a record production month for the Gulf. January’s ave. production of 2.060 million bopd surpassed the Aug. 2019 ave. of 2.044 million bopd.

Barring significant tropical storm shut-ins over the next 6 months (hurricane season starts today!), a production record in 2026 seems like a good possibility.