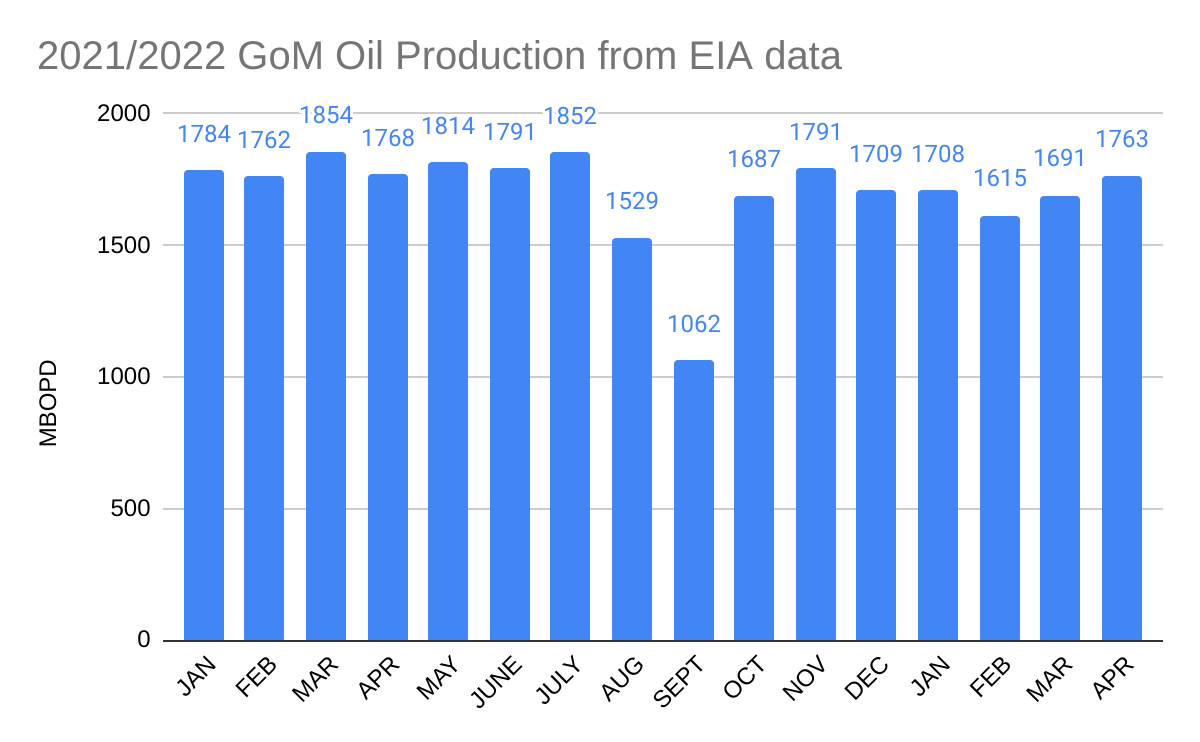

April production increased from March by 72,000 BOPD to 1.763 million BOPD. The increase is associated, at least in part, with Murphy’s King’s Quay field which began producing in early April. 2022 GoM production remains below the levels reached in the first 7 months (pre-Hurricane Ida) of 2021, and is well below BOEM’s forecasted 2022 production rate of 1892 MBOPD. Perhaps BOEM was assuming earlier startup dates for other projects that will begin production later this year or next year. The 2022 YTD dip in production points to the importance of sustained exploration and development.

BOEM’s short-term production forecast is considerably more optimistic than EIA’s. This optimistic forecast, along with unrealistic expectations regarding the “energy transition” are reasons for proposing so few lease sales in the new 5 year leasing program. The logic for this minimalist leasing program seems to be that future production is neither necessary nor desirable. Indeed the program implies that the long-term nature of offshore production is a liability and is justification for limiting OCS oil and gas leasing:

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

5 Year Leasing Program, p.3

Basing leasing decisions on “future climate pathways” would seem to be a considerable stretch of the Secretary’s authority under the OCS Lands Act and may be inconsistent with the recent SCOTUS decision in West Virginia vs. EPA. A strategic shutdown of the offshore oil and gas program would dramatically increase energy supply and security risks going forward, and should be authorized by Congress.

Leave a comment