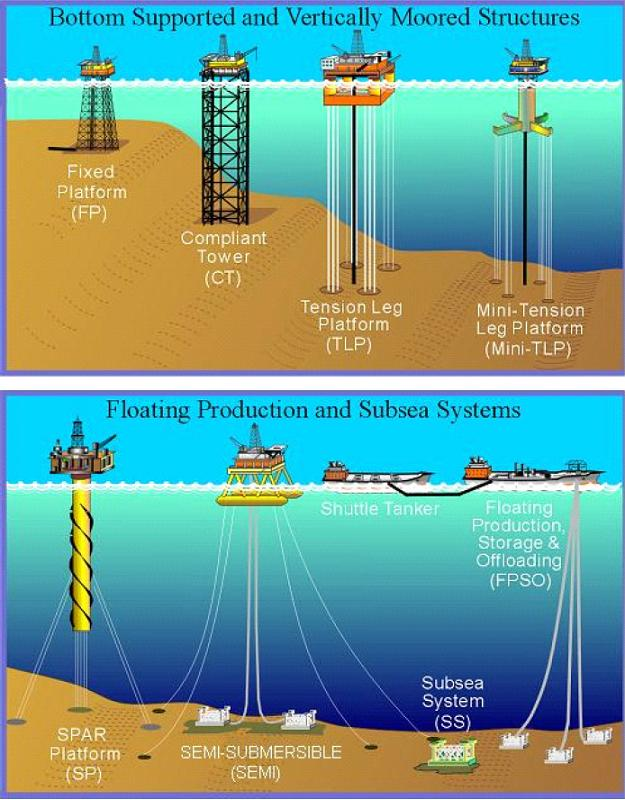

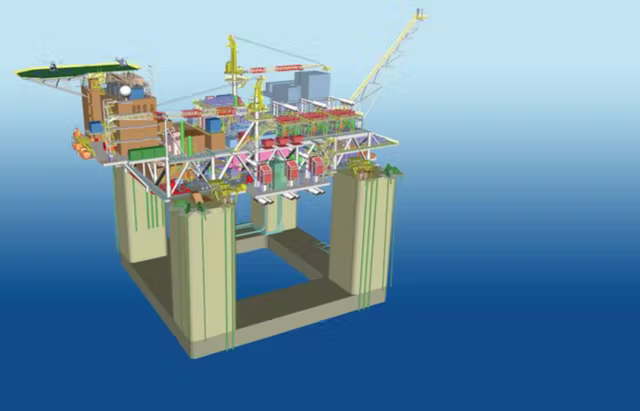

Shell’s Whale floating production unit began producing this month:

- estimated peak production:100,000 barrels of oil equivalent per day (boe/d)

- water depth – 8600 ft

- 200 miles south of Houston

- estimated recoverable resource: 480 million boe.

- first oil only 7.5 years after discovery (includes COVID delay)

- Vito clone: replicates 99% of the hull design and 80% of the topsides from Vito.

- high efficiency gas turbines and compression systems

- ~ 30% lower greenhouse gas (GHG) intensity over its life cycle than the already efficient levels being achieved at Vito. (Why the push to run electric cables from shore to North Sea platforms with ample gas production?)

All 5 of the new simpler, safer, greener floating production units are now online:

| platform | operator | first production |

| King’s Quay | Murphy | April 2022 |

| Vito | Shell | Feb 2023 |

| Argos | bp | April 2023 |

| Anchor | Chevron | Aug 2024 |

| Whale | Shell | Jan 2025 |

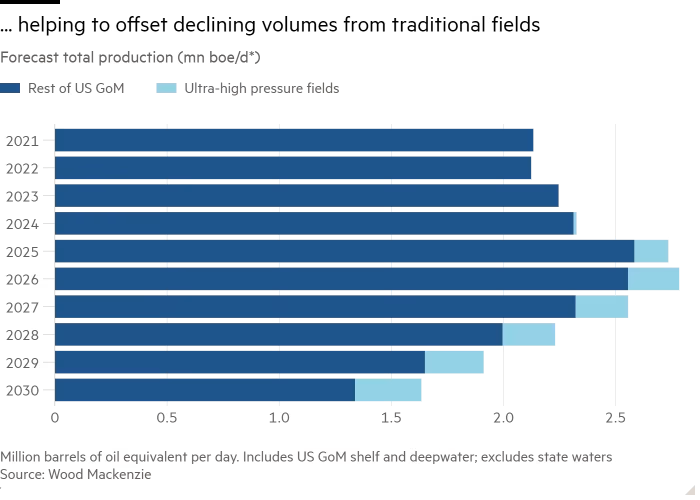

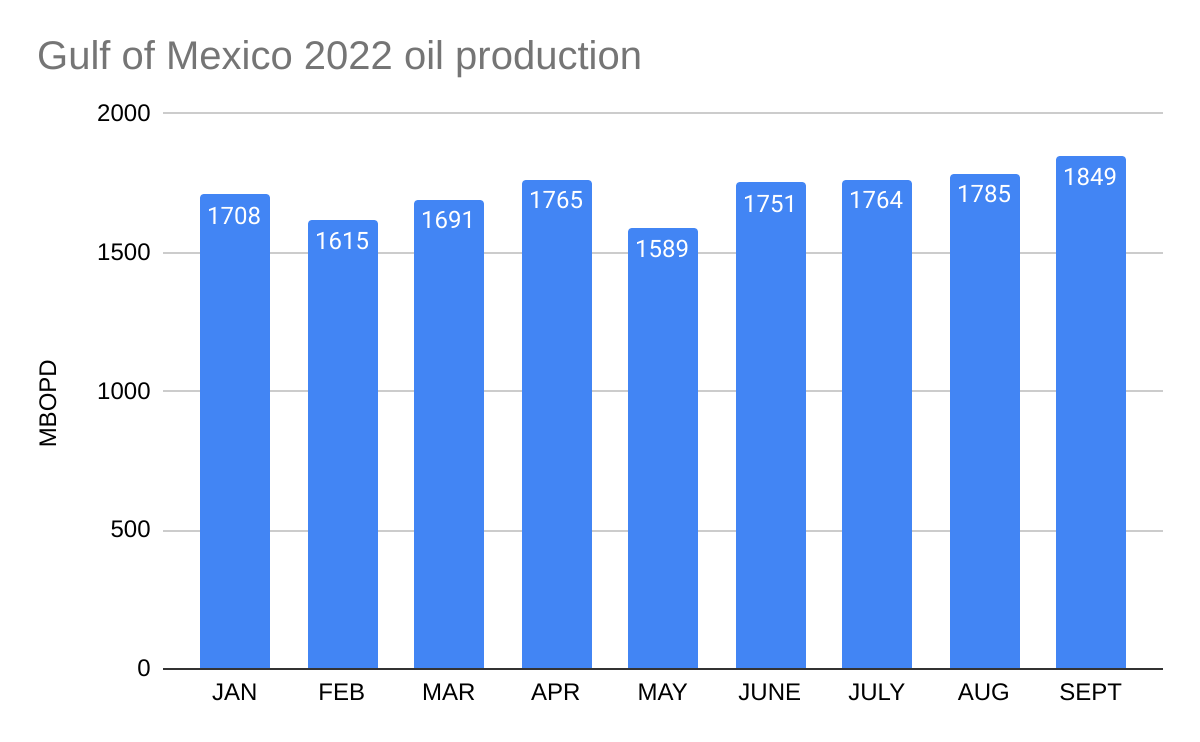

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded in this post.)

Three major high-pressure projects, ala Chevron’s Anchor, are anticipated:

| platform | operator | discovery date | first production |

| Kaskida | bp | 2006 | 2029 |

| Sparta | Shell | 2012 | 2028 |

| Shenandoah | Beacon | 2009 | 2025 Q2 |

The Gulf still has high production potential if properly managed with consistent lease sales.

Will Florida budge by supporting the lifting of the EGOM leasing moratorium? Here is why they should.