Per yesterday’s discussion comparing recent onshore and offshore lease sales, the investments are really quite different. When you acquire Permian and Delaware Basin shale tracts you are essentially buying oil in place that should be producible with current technology.

At offshore sales, you are typically acquiring the opportunity to learn more, either through site surveys or drilling. Your lease exploration and development strategy will also be influenced by drilling outcomes for similar targets on other leases. A return on your investment is far from certain.

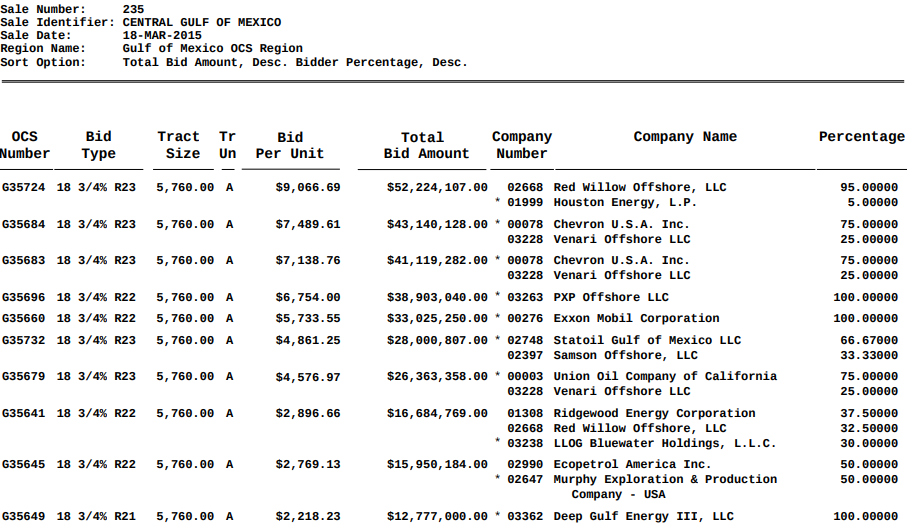

I looked back at the top ten leases (by high bid) issued at Central Gulf Sale 235. That sale was chosen because it was 11 years ago, giving time to explore and initiate development, and the bidding was strong. The top ten leases received bids ranging from $12.8 million to $52.2 million. See the screenshot below.

Surprisingly, only four of the leases were ever drilled and nine of the ten leases have expired. The only lease remaining is the highest bid block (OCS-G 35724, Walker Ridge Block 107, $52.2 million) now owned by Talos (27% and operator), Red Willow (22.5%), Shell (22.5%), CSL (9%), and two investment partnerships. This lease is being held by operations given that a well was drilled within the past year. However, Talos has announced a discovery, and the well has been temporarily abandoned to preserve future utility:

The discovery well was drilled to a total vertical depth of 33,228 feet utilizing the West Vela deepwater drillship and encountered oil pay in multiple high-quality, sub-salt Miocene sands. A comprehensive wireline program was conducted, acquiring core, fluid, and log data to evaluate the reservoir.

So the bottom line is $308.3 million in bonuses for 10 leases, 9 of which have now expired, and one discovery which could prove to be commercial down the road.