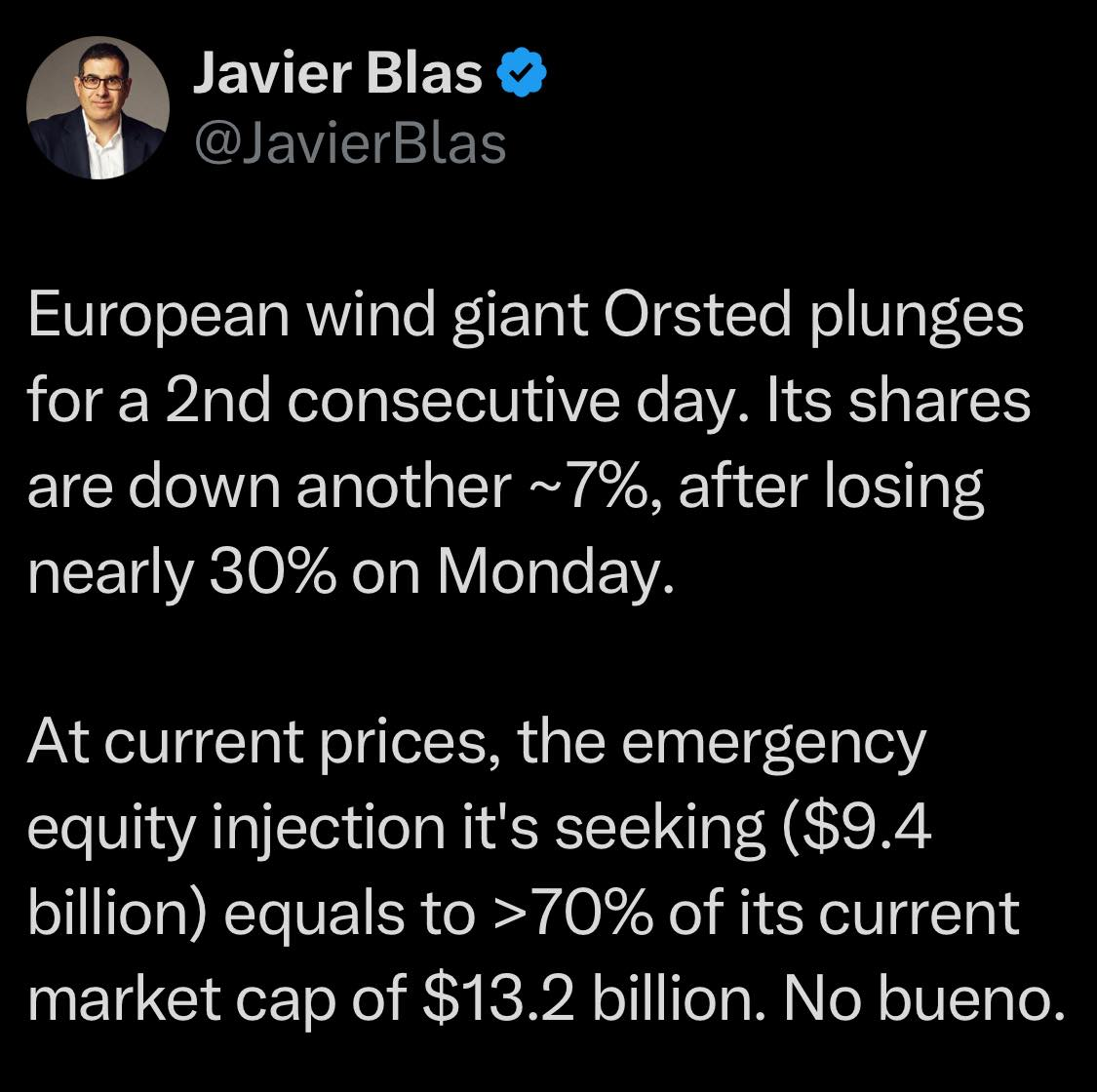

JL Daeschler informs that UK offshore wind energy is 82% foreign-owned. Foreign companies are thus the primary beneficiaries of the UK’s generous renewable energy subsidies (chart below).

David Turner comments as follows in his informative piece on UK wind energy:

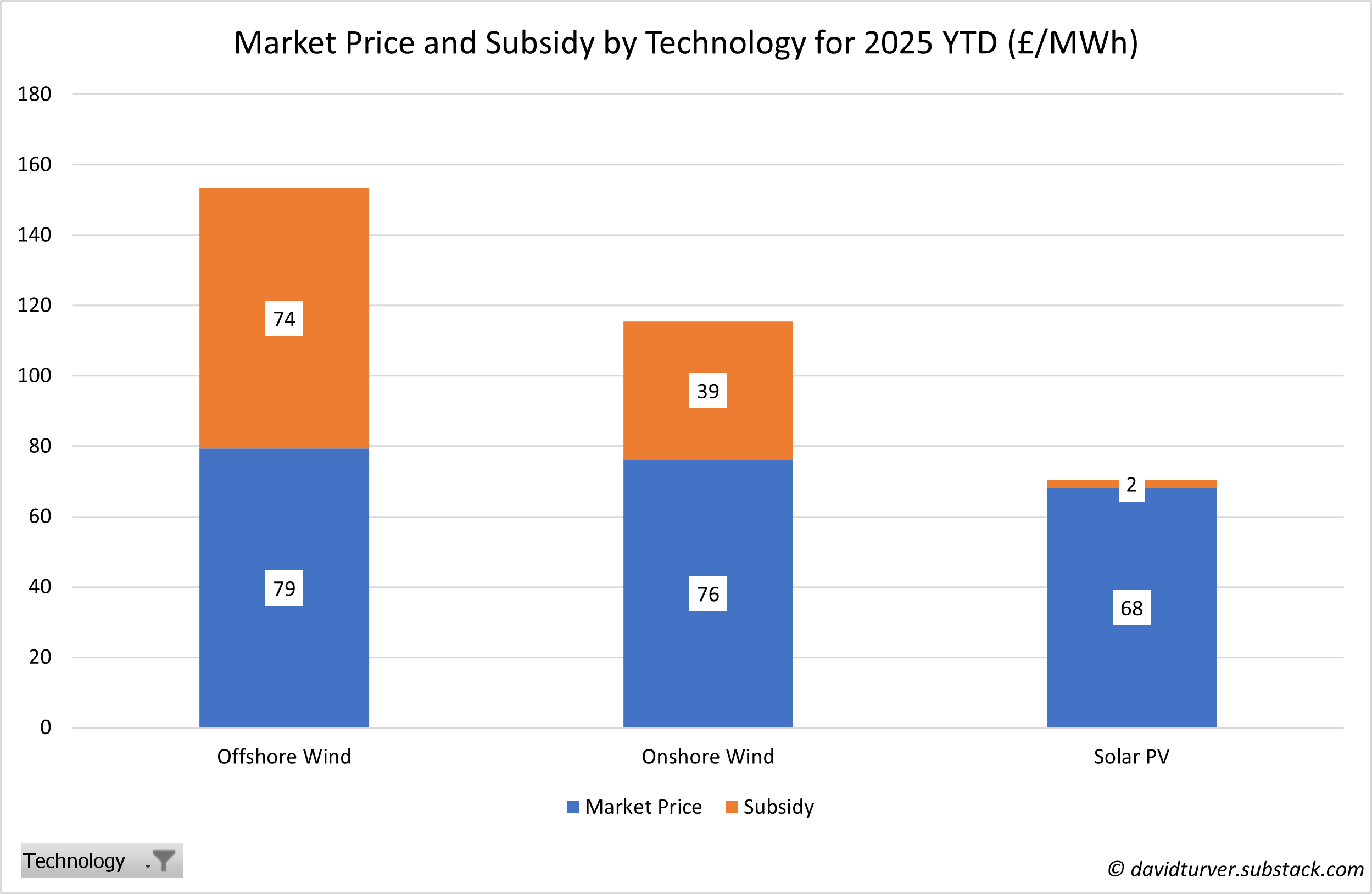

“We have been warning for some time that it is crazy for a developed economy to try and run its electricity generation system using technologies that are dependent on the weather. Even though there has been only a relatively modest decline in wind output this year, the operators and owners of wind farms are learning the hard way that it is very difficult to run a business that is at the mercy of the vagaries of the weather. Many of these companies are up to their eyeballs in debt. They better hope the wind blows hard this Autumn and Winter so they can collect higher subsidies, or they will be in real trouble.“

We have consistently raised concerns about decommissioning financial assurance for offshore wind facilities. Turner echoes those concerns noting that the wind industry’s “perilous finances are an even bigger reason to insist that proper funds are set aside to fund decommissioning or the long-suffering taxpayer will be on the hook for another hidden cost of renewables.“