The Buckskin field (LLOG) is located in Keathley Canyon blocks 785, 828, 829, 830, 871, and 872 in 6,800 ft (2,073 m) of water. The KC 828 lease expired last year and LLOG’s bid for that block at the BBG2 sale was rejected.

BOEM’s Decision Information Matrix for Sale BBG2 is attached. As previously noted, 2 of the 25 high bids were rejected: Keathley Canyon Block 828 ($1,101,202) and Atwater Valley Block 63 ($650,018).

MROV=Mean of the Range-of-Value; LBCI=Lower Bound Confidence Interval

In the case of Keathley Canyon 828, BOEM’s valuation is more than 20 times the high bid. BOEM valued this block far higher than any other block in the sale.

KC 828 had been previously leased and that lease expired on 9/3/2025. The lease block was part of LLOG’s Buckskin field. Apparently, the lease expired due to inactivity given that the last well reached total depth more than a year prior to the expiration date. LLOG wanted the lease back. BOEM’s rejection sends a message that the price went up (by a lot 😉).

Finally, why didn’t any other company bid on KC 828, a block that has been publicly reported as being part of the Buckskin field?

Although BOEM’s decision matrix has not yet been posted, a comparison of the acceptances with the bids submitted tells us that the Keathley Canyon Block 828 ($1,101,202) and Atwater Valley Block 63 ($650,018) bids were rejected.

Both of the rejected bids were submitted by LLOG, partnering with 4 other companies on the Atwater Valley block. LLOG’s high bids on 3 other blocks were accepted, so their rejection rate was 40%. Interestingly, 2 of the 3 BBG1 rejected bids were also submitted by LLOG.

There is no shame in bid rejections, which are part of the legislated leasing process. Why pay more than you have to (or think a block is worth)? A bid rejection may attract future competition, but otherwise the only downside is that you don’t get a lease that you can possibly acquire at another sale if desired (an advantage of regular, predictable lease sales).

BOEM is charged with making fair market value determinations and their process and decisions are publicly available. Of course, opinions differ on the value of an unexplored lease. We will see what the bidding on the BBG1 and BBG2 rejections looks like in future sales.

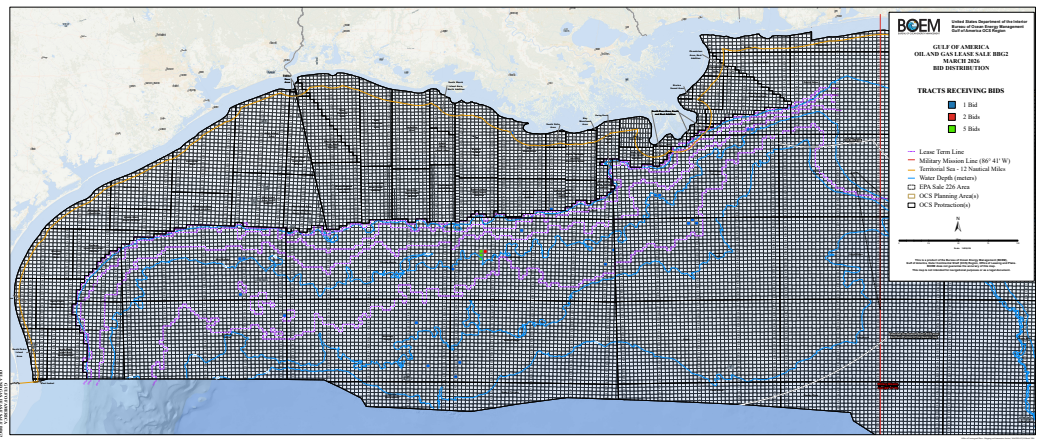

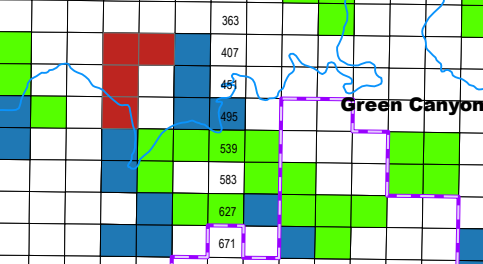

BOEM did accept the the high bids for the BBG2 “sweet spot” blocks (red in map below; also see the table) in the Green Canyon Area of the Gulf. These 4 blocks accounted for 17 of the sale’s 38 bids (45%) and $32.8 milion of the sale’s $47 million in high bids (70%). BP’s $21 million bid for GC 404 was by far the sale’s highest bid.

red=blocks receiving bids at BBG2; blue=BBG1 and Sale 261 leases; green=active leases issued prior to Sale 261

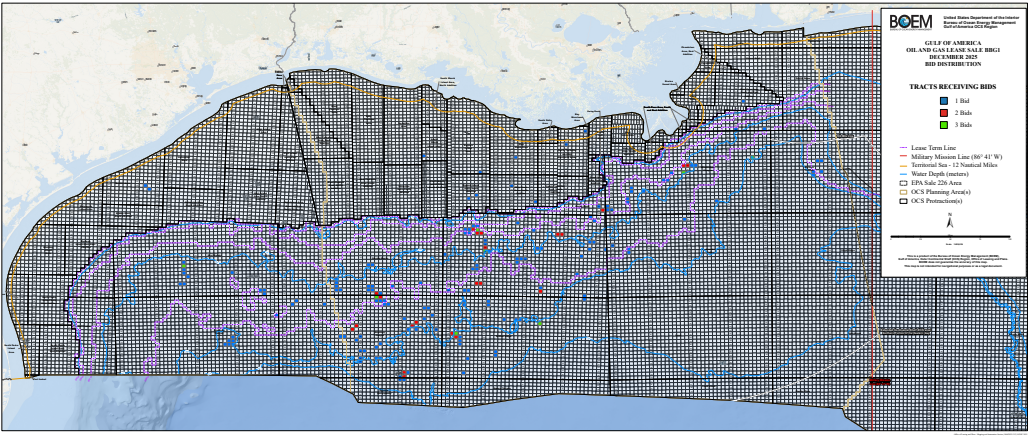

Companies seeking to acquire OCS leases are not only competing with each other, they are also competing with BOEM’s tract evaluations. In that regard, the bidders fared well at Sale BBG1. Only 3 of the 181 high bids were rejected by BOEM.and those rejections appear to be warranted.

MROV=Mean of the Range-of-Value; LBCI=Lower Bound Confidence Interval; KUSA=Karoon (Australia) Energy USA; EW=Ewing Bank; MC=Mississippi Canyon

LLOG submitted 9 other high bids (alone or with partners) that were accepted. KUSA did not submit any other bids. We’ll see if the rejected bids for these blocks are exceeded in future sales.

Nine other high bids (table below) were less than the MROV, but all were greater than the LBCI. Those bidders “beat the house,” acquiring leases for <MROV. In that regard, Equinor led the pack with no rejections even though 3 of their 7 bids were below MROV. Similarly, 2 of Beacon’s 4 bids were <MROV, with no rejections.

Block No.

Company

no. of bids

bid

MROV

LBCI

GC 345

Beacon

1

$5,302,358

$5,400,000

$4,200,000

GC 346

Beacon

1

$1,102,358

$1,500,000

$900,000

GC 547

Equinor

1

$3,200,067

$4,500,000

$2,600,000

GC 549

Equinor

1

$899,967

$1,500,000

$576,000

AT 64

LLOG

1

$7,997,018

$8,300,000

$6,700.000

KC 386

Oxy

2

$3,000,505

$3,500,000

$2,800,000

KC 429

Oxy

1

$600,505

$910,000

$470,000

KC 431

Woodside

1

$904,547

$1,200,000

$840,000

WR 56

Equinor

1

$904,547

$1,200,000

$576,000

MROV=Mean of the Range-of-Value; LBCI=Lower Bound Confidence Interval; AT=Atwater Valley, GC=Green Canyon, KC=Keathley Canyon, WR=Walker Ridge

Perhaps most interesting were the blocks that were highly valued by industry, but not by BOEM. Each of these blocks (table below) received multiple bids and high bids >$10 million. Conversely, BOEM valued the blocks at only $576,000, which (per the terms of the sale) equates to the minimum acceptable bid of $100/acre.

Block No.

high bidder

high bid

other bids

MROV

GC 845

Beacon

$11,802,358

LLOG: $613,008

$576,000

KC 25

Chevron

$18,592,086

BP: $11,507,770 Shell: $753,029

$576,000

WR 443

Woodside

$15,204,547

Chevron $1,596,189

$576,000

WR444

Woodside

$12,204,547

BP: $4,593,770 Chevron $1,482,378

$576,000

MROV=Mean of the Range-of-Value; LBCI=Lower Bound Confidence Interval; GC=Green Canyon, KC=Keathley Canyon, WR=Walker Ridge

All of this demonstrates yet again that:

the govt is leasing exploration and development opportunities, not confirmed resources,

commercial discoveries are far from certain,

informed assessments differ (I.e. great minds, and their computers, don’t always think alike 😀),

corporate priorities differ, and

exploration strategies evolve.

Superstition, tactic, AI, coded or subliminal message? 😉

All 58 BP bids end with 770. Examples: $1,707,770 and $807,770. (At Sale BBG2, all 5 BP bids ended with 990.)

All 18 Shell bids ended with 029. (At Sale BBG2, all 6 Shell bids ended with 240.)

13 of 15 Anadarko bids ended with 505, the other 2 ended with 101.

The table in the Sale 259 bid rejections post has been corrected below. That table incorrectly reported that subsequent bids for Keathley Canyon Blocks 745 and 789 were rejected at Sale 261. Those bids were in fact accepted. Houston Energy was identified as the submitter rather than Beacon Offshore Energy, the company that, per the bidding data, had the largest ownership share. (See the bidding partnership pasted below.)

The acceptance of those 2 bids significantly increases the net gain to the government as a result of the Sale 259 bid rejections. See the corrections in red to the table:

14 of the high bids at Gulf of Mexico Lease Sale 259 were rejected. Did those tracts receive bids at sale 261? What was the net gain or loss of revenue? See the summary bullets and table below

6 of the 14 tracts received no bids whatsoever

5 of the 14 tracts received higher bids that were accepted.

2 tracts received substantially higher bids that were again rejected

1 tract received a lower bid that was accepted

net bonus revenue gain to the govt from the bid rejections (pending re-offering at future sales): $1,032,877

net bonus revenue gain = 0.27% of the total high bids at sale 261

net loss in future rental and royalty payments: ????

For a net bonus revenue gain to date of only 1/4 of one per cent, 8 of the 14 sale 259 tracts with rejected high bids remain closed to exploration. The timing of any future sales is very much in doubt given the minimalist 5 year leasing plan and the associated legal challenges.

Current bid evaluation practices only make sense if regular lease sales are held on a predictable schedule, as has historically been the case.

Keathley Canyon and Walker Ridge bids at Sale 259: blue=1 bid, red=2 bids, green=3 bids

Based solely on a comparison of the bids (Sale 261 vs. Sale 259), the Sale 259 rejections were, on balance, to the benefit of the public (table below). On the plus side:

Assuming all of the high Sale 261 bids are accepted, the net gain to the US Treasury is $8,749,365

Of the 14 tracts with rejected high bids at Sale 259, 8 received bids at Sale 261

Seven of those 8 bids were higher than the Sale 259 high bids, and 5 of those 7 were more than $1 million higher.

The Sale 259 bid rejections in the Keathley Canyon and Walker Ridge areas proved to be 100% beneficial. All 6 of those tracts received much higher bids at Sale 261.

The best BOEM decisions were the rejections of the Sale 259 bids for AT 5 and WR 795 and 796. The Sale 261 high bids on these 3 tracts were $10.8 million higher than the Sale 259 bids.

WR 795 and 796 were single bid tracts at Sale 259.

AT 5 received 3 bids at Sale 259. BOEM rejected the high bid despite the competitive bidding. That proved to be the right call given that the Sale 261 high bid was $3.5 million higher.

On the other hand:

None of the 5 Green Canyon rejections received any bids at Sale 261.

The high bid for GC 777 was rejected twice (Sales 257 and 259) at a cost of $1.8 million, the BP/Talos high bid at Sale 257. At sale 259, BP was the sole bidder for GC 777, and their bid was only $583,000, less than 1/3 of their Sale 257 bid. GC 777 received no bids at Sale 261.

The worst BOEM Sale 259 decisions were the rejections of the DC 622, GC 547, and GC 591 bids at a cost of $4.6 million ($5.2 if the Sale 261 bid for DC 622 is rejected).

This is not to say that the tracts with rejected bids will not ultimately be leased. However, the uncertainty regarding future sales changes the historic GoM leasing dynamic. The next opportunity for purchasing unleased tracts is a troubling unknown. Absent leasing and exploration, their resource and revenue potential will never be known.

area and block

Sale 259 high bid – company

Sale 261 high bid

govt gain (loss)

DC 622

2,101,836 – Shell

615,628* – Shell

(1,486,208)

GC 173

307,107 – Woodside

no bid

(307,107)

GC 547

1,783,498 – Chevron

no bid

(1,783,498)

GC 591

1,291,993 – Chevron

no bid

(1,291,993)

GC 642

605,505 – Anadarko

no bid

(605,505)

GC 777

583,103 – bp

no bid

(583,103)

AT 5

1,551,130 – Anadarko

5,215,628* – Shell

3,664,498

AT 133

607,107 – Woodside

no bid

(607,107)

KC 745

707,777 – Beacon

2,422,222 – Beacon

1,714,445

KC 789

707,777 – Beacon

2,143,299 – Beacon

1,435,522

WR 794

724,744 – Beacon

1,487,624 – Beacon

762,880

WR 795

774,242 – Beacon

5,301,107 – Woodside

4,526,865

WR 796

774,242 – Beacon

3,310,107 – Woodside

2,535,865

WR 750

724,744 – Beacon

1,498,555 – Beacon

773,811

*The BOEM sale 261 bid summary misidentifies the DC 622 and AT 5 bids as being for MC 622 and GC 5 respectively. The corrected identification above is based on the “Blocks Receiving Bids” file correlated with the block number and company code.

Keathley Canyon (KC) Block 96, the tract receiving the highest bid in the entire sale ($15,911,947 by Chevron), had a BOEM MROV of only $576,000. Clearly, Chevron and the government have a very different view of the value of this tract. BP was the second bidder for KC 96, and their bid ($4,003,103) was also considerably higher than BOEM’s MROV. This one will very interesting to follow.

The only bid that was rejected in Sale 257 was the BP/Talos bid of $1.8 million for Green Canyon Block 777. BOEM’s MROV in the Sale 257 evaluations was $4.4 million. BP again bid on GC 777 in Sale 259, but their bid was only $583,000 (even though BOEM’s Sale 257 evaluation was public information). BOEM’s MROV was reduced only slightly to $4.2 million, and they again rejected BP’s bid. We’ll see what happens in the next sale.

51 of the 230 accepted bids were >$1 million, all for deepwater tracts. All of the rejected bids were for deepwater tracts, and a higher percentage (4/14) were >$1 million. This makes sense given that the higher potential prospects are in deepwater.

These results demonstrate again that resource evaluation is far from an exact science. BOEM is not selling barrels of oil and cubic feet of gas. BOEM is evaluating prospects, and companies are bidding on the opportunity to explore these prospects.

Bidding strategies differ; the more companies participating, the better the long-term prospects for the OCS program.