At a minimum, the fire will further delay and increase the cost of well plugging operations on Platform Habitat. Per BSEE’s borehole file, 17 wells remain to be permanently abandoned, 3 of which have yet to be temporarily abandoned. These wells are 23-44 years old, and have been inactive for 11 years.

If there is significant platform damage, the remediation delays and costs would be substantial, comparable to those associated with major Gulf platforms damaged by hurricanes. Structural damage could increase the urgency of removing the platform. Given California’s decommissioning quagmire, this would be a major challenge.

Who pays, and what does the financial assurance picture look like? Per the attached BOEM spreadsheet (excerpt pasted below):

The 2020 cost estimate for decommissioning Habitat was $44.3 million. That number is optimistic even if platform damage is minimal.

$13.6 million in supplemental assurance has been provided.

A third party guarantee has been secured.

The guarantee was provided by Freeport-McMoRan Oil & Gas (FMOG)

Per BOEM, FMOG is the guarantor for all DCOR leases. Unless BOEM has allowed otherwise, the guarantor pays all costs not covered by the lessees. Given the number of old platforms and California decommissioning challenges, the risks for FMOG are indeed large.

Although DCOR LLC is the current Habitat operator, the company owns only a 4.18% share of the project. CHANNEL ISLANDS CAPITAL, L.L.C., a private company about which little is known, holds a 95.82% share.

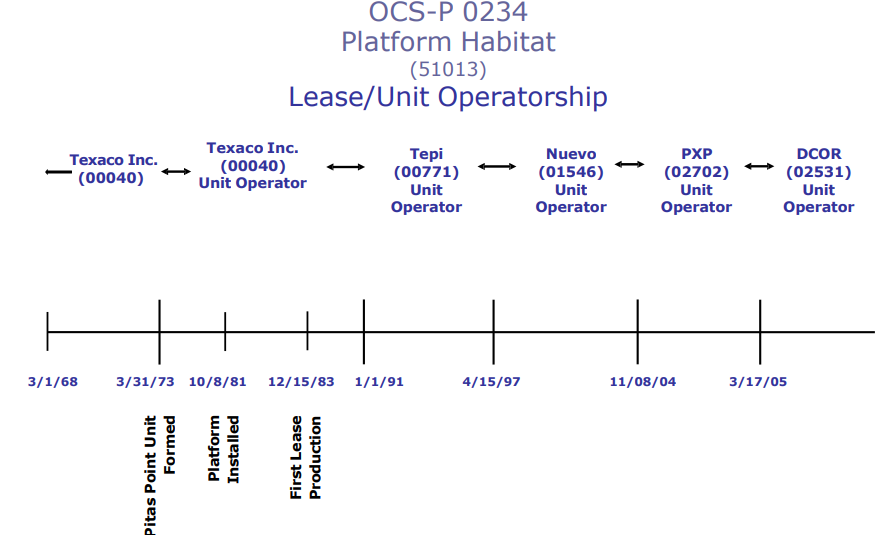

Should the 2 owners default, BOEM/MMA will look to the guarantor and predecessor lessees (see the chart below). Unfortunately for FMOG, they are both the guarantor and the predecessor lessee. FMOG acquired Plains Exploration & Production (PXP), the operator prior to DCOR. Nuevo Energy was acquired by PXP and thus also tracks back to FMOC. (This may explain FMOC’s decision to be a guarantor!).

Should FMOC fail to fulfill their obligation. Chevron would likely be the next target. The original Harvest partners were Texaco (operator) and Union Oil, both of which were acquired by Chevron.

TEPI=Texaco Expl. & Production. Nuevo Energy was acquired by Plains Expl.&Production (PXP), which was acquired by Freeport McMoRan Oil & Gas (FMOG)

Attached are my comments on BOEM’s proposed revisions to the decommissioning financial assurance regulations. These comments were submitted to Regulations.gov yesterday (3 days early 😀). Bud

Concluding Remarks

MMA’s highest priority must be assuring that facilities are safely decommissioned without public funding. Supplemental financial assurance determinations and lease assignment approvals must be consistent with that priority.

Predecessor liability is an important financial assurance principle, but legal boundaries and administrative procedures must be clearly established.

Safety and compliance are inextricably related to financial performance, and must be considered in determining supplemental assurance requirements.

Using reserve estimates to reduce supplemental assurance exposes taxpayers to geologic and accounting risks.

Unacceptable public risks have resulted from financial assurance decisions intended to advance offshore wind development.

The transition reflects more than a decade of operational experience managing offshore resources. By consolidating the planning, permitting, inspection, and enforcement responsibilities currently divided between BOEM and BSEE, the Department aims to:

Improve coordination and consistency

Reduce duplication of efforts

Strengthen oversight and environmental safeguards

Modernize organizational structure

All current regulatory responsibilities and protections will remain in place throughout the transition. There will be no disruption to permitting, environmental reviews, or enforcement activities.

What to Expect

Phased Transition: Internal alignment activities begin soon.

No Regulatory Rollbacks: Existing requirements remain in full effect.

New Website and Branding: The Marine Minerals Administration’s full digital presence will launch in the coming months.

A New York Times article suggests that the consolidation of BOEM and BSEE into the Marine Minerals Administration will weaken environmental oversight. It will not. On the contrary, regulation is likely to be strengthened as resources shift from inter-bureau coordination and redundancy management to the primary safety and environmental protection missions.

Given the challenges associated with Federal reorganizations, agency heads often opt for the status quo. I’m pleased that the current DOI leadership team, with whom I disagree on some issues, chose to merge the bureaus.

Quotes from the NYT article followed by my comments:

NYT:The Trump administration is creating a new office that critics say could weaken the environmental oversight of oil drilling and seabed mining in territorial waters.

Comment: The functional overlap and associated uncertainty that permeates the offshore regulatory regime is a weakness, not a strength. Virtually every element of the regulatory program requires coordination between the two bureaus. This includes plan and permit approvals, decommissioning and financial assurance, spill response plans, lease stipulations, assignments, pipeline regulation, environmental reviews, enforcement actions, and geologic data collection and review. Note the list of MOUs that are intended to coordinate BOEM and BSEE redundancy. The documents often do more to confuse than clarify. For example, see the MOU entitled “Environmental and NEPA.”

Multi-bureau organizational complexity is not in the best interest of safety and environmental protection. Overlapping responsibilities, coordination challenges, and “turf” issues distract the technical staff from their important risk management duties, the work they are good at and enjoy doing. BSEE and BOEM should be overseeing the offshore industry, not each other.

NYT:The new agency, the Marine Minerals Administration, will be formed by reunifying two offices that had been split up after the 2010 Deepwater Horizon oil spill in an effort to increase environmental oversight of the energy industry and prevent future oil disasters. After the split, the Interior Department’s oil-leasing activities were separated from environmental regulation and financial management. (emphasis added)

Comment: The assertion that the leasing and environmental regulation were separated is false. The leasing bureau (BOEM) was assigned lead responsibility for the review and approval of the fundamental operational planning documents – Exploration Plans, Development and Production Plans, and Development Operations Coordination Documents. This includes the environmental reviews pursuant to NEPA.

NYT:The move is “worrisome because it has the potential of bringing things back where they were, where there was this inherent conflict of interest between promotion of offshore oil and gas, and oversight safety,” according to Donald Boesch, emeritus professor at the University of Maryland Center for Environmental Science.

“In recent years various bodies have concluded that certain MMS offices and programs have violated ethical rules or guidelines. In the wake of the Deepwater Horizon disaster, some questioned whether ethical lapses played any role in causing the blowout. The Chief Counsel‘s team found no evidence of any such lapses.“

NYT:The new bureau will also take on oversight of the Trump administration’s plans to lease waters in U.S. territories to deep-sea mining companies. The first of these sales, according to the spokeswoman for the Interior Department, are likely to happen next year.

Comment: DOI’s marine minerals program is decades old and is a priority for the current administration. Reorganization should not affect the MMA’s capability to oversee these activities.

The name is especially fitting given that 1947’s first acquisition, Renaissance Offshore, operates entirely on the Gulf shelf (map below). Renaissance is a significant shelf producer ranking 19th among all Gulf operators in both oil (791,572 bbls) and gas (1,335,009 mcf) production in 2025. Renaissance ranked 6th in oil production and 7th in gas production among companies that focus on the shelf.

A challenge for 1947 will be improving Renaissance’s compliance and safety record:

Renaissance has averaged 0.93 violations (INCs) per inspection since 1/1/2020, trailing only Cox legacy Array in INC frequency.

In 2019, a worker fell to his death at the Renaissance Eugene Island 331 B platform. BSEE’s investigation found that Renaissance failed to maintain all of its walking and working surfaces in a safe condition, that supervisors failed to promptly correct or prevent employees from accessing the uncorrected and uncontrolled walking and working surface hazard area, and that Renaissance and its contractors failed to follow the agreed upon terms and conditions within their respective Safety and Environmental Management Systems (SEMS) bridging arrangements. (Renaissance incurred a seemingly modest $105,292 civil penalty for this incident. There is no public information on any settlement with the victim’s family.)

“Between 2012 and 2014 Renaissance grew substantially with the acquisition of sixteen Gulf of Mexico producing fields, fifteen of which are operated and most are 100% owned.” 1947’s financial strength is unclear. Hopefully, BOEM will verify that satisfactory decommissioning financial assurance arrangements are in place before any lease assignments are approved.

Decommissioning financial assurance regulations are “instrumental in ensuring both environmental and fiscal responsibility.“- .natural resource management students

Increased environmental risks. (Accidents, hurricanes, and other events may introduce decommissioning risks that require both immediate and longer term attention and financial resources. Such incidents typically increase decommissioning costs by orders of magnitude, and can even bankrupt financially sound companies. See “Sad End for Taylor Energy.”)

Firms with lower credit ratings would no longer have to hold as much capital in reserve and would have a lower bar of entry into projects. (See comments by John Smith.)

The possibility of cascading economic impacts in the event that bankruptcy does occur. (Which predecessors will be affected and how? What about contractors? How long will bankruptcy litigation delay resolution of claims? Will bankruptcy court asset sales increase public financial, safety, and environmental risks?)

Taxpayers would be facing a portion of the risk. (Predecessors are only accountable for the facilities they installed, so holding predecessors liable doesn’t free the taxpayers from all financial risks.)

The entire energy sector faces increased risks when operating companies fail. (Prominent failures damage the reputation of the industry and the OCS program, with implications for the economy and national security.)

Before relaxing financial assurance requirements, BOEM should consider the role that lax lease assignment and financial assurance policies had in the growth of Fieldwood, Cox, Signal Hill, Black Elk, and other failed companies.

The Case for Reefing California Platforms by John Smith

Environmental groups like the Environmental Defense Center and Get Oil Out continue to oppose converting the jackets of California oil and gas platforms to artificial reefs despite scientific studies (Claisse et al. 2014) showing “oil and gas platforms off the coast of California have the highest secondary fish production per unit area of seafloor of any marine habitat that has been studied.”

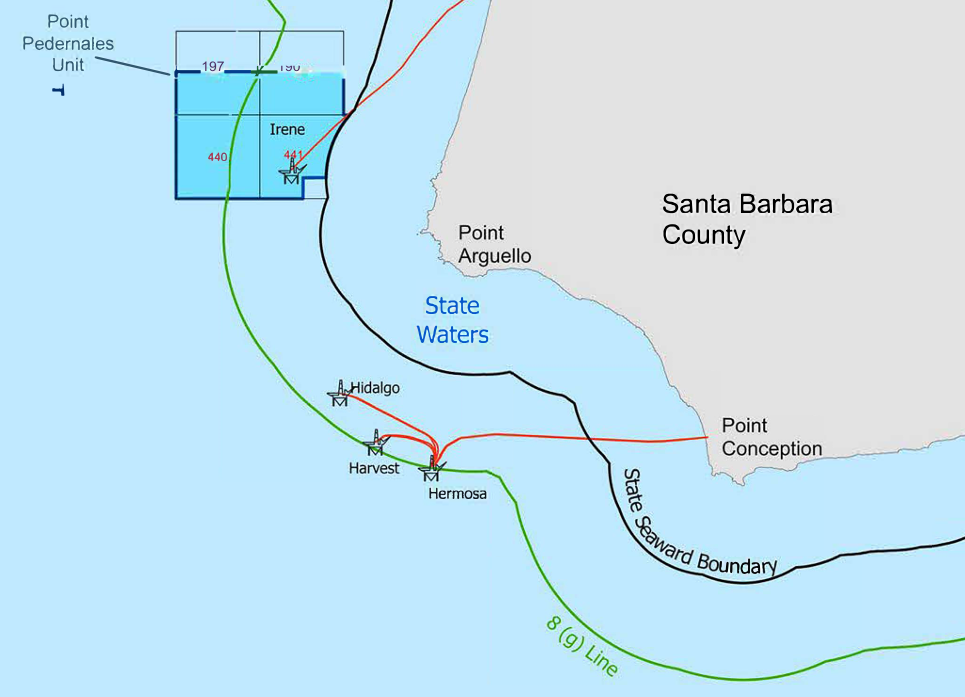

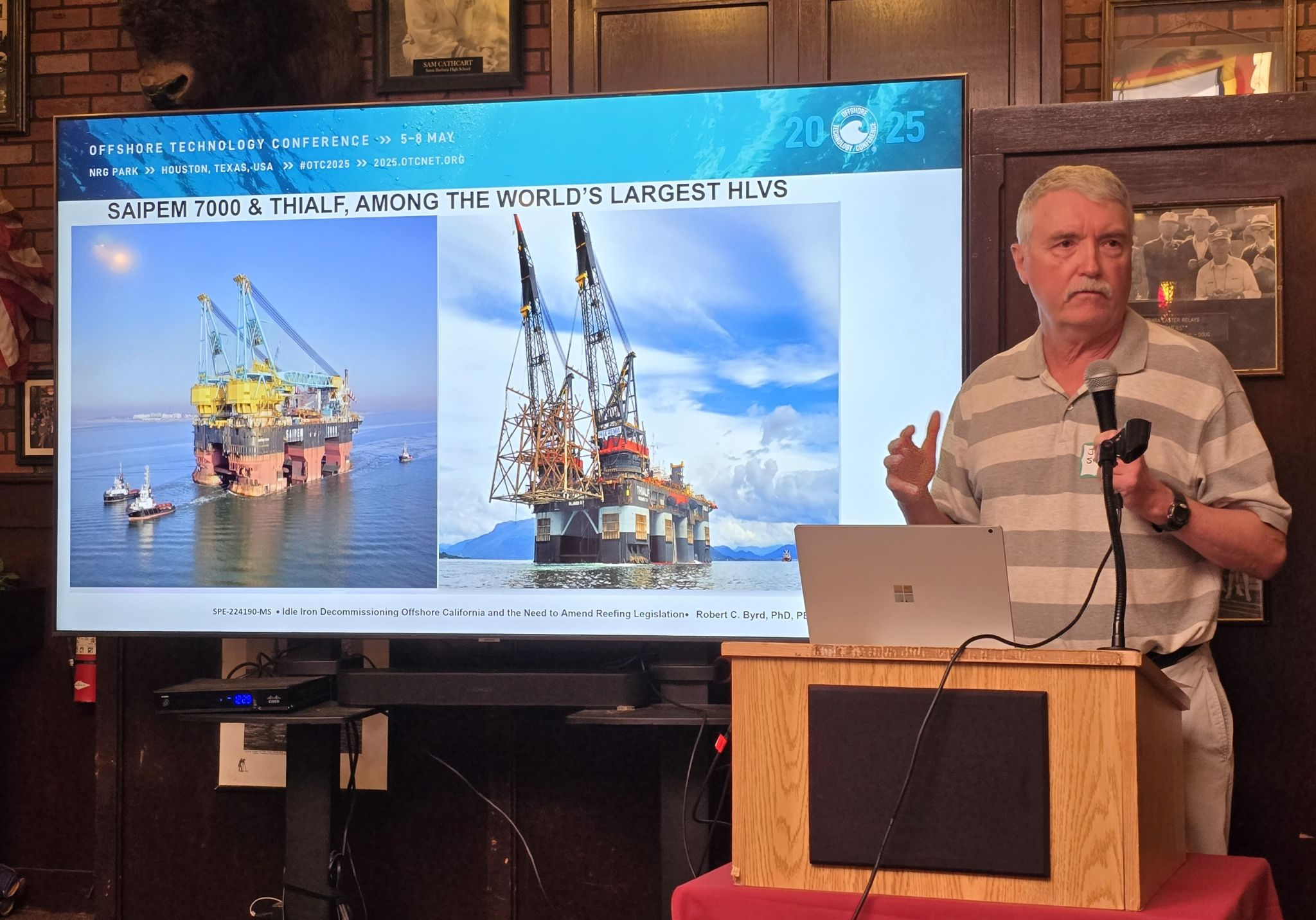

Another important factor environmental groups and the 2023 BOEM Programmatic EIS for Decommissioning failed to consider and acknowledge is the huge amount of air emissions that would be released by world-class heavy lift vessels like the Thialf or Balder Semi-submersible Crane Vessels (SSCVs) that would be required to safely and efficiently remove the large federal OCS platforms like Harvest, Hermosa, and Hidalgo (HHH). The HHH platforms are in waters depths ranging from 430-675 feet and have combined deck and jacket weights ranging from 20,000 – 25,000 tons. In comparison, the wrought iron structure of the Eiffel Tower weighs about 8,000 tons.

The SSCVs and accompanying Anchor Handling Tugs (AHTs) used to remove the HHH platforms will likely to be mobilized from distant locations like the North Sea or Gulf of America where they typically operate. Because SSCVs like the Thialf and Balder are too large to enter the Panama Canal, this would involve a 20,000 nautical mile roundtrip voyage around the tip of South America.

Three to four campaigns, and separate SSCV and AHT mobilizations and demobilizations, are projected to be required to fully remove the HHH platforms because the challenging oceanographic conditions offshore Point Arguello restrict heavy lift operations to a 150-day period between May and October.

Four campaigns by the SSCV and AHT would consume about 300,000 metric tons (mt) of marine diesel oil and release approximately 470,000 mt of CO2 and 11,000 mt of NOX emissions. To put these numbers into context, 470,000 mt of CO2 and 11,000 mt of NOX are:

the amount of CO2 emissions released by providing electrical power to 97,600 homes annually (the city of Santa Barbara has about 38,000 housing units).

the amount of CO2 emissions released by burning 1.1 million barrels of oil.

the amount of CO2 emissions released by 102,000 gasoline burning cars annually.

the amount of NOX emissions released by four large oil or coal-fired power plants annually.

the total annual NOX emissions in Santa Barbara County.

And this is only the emissions released during mobilization and demobilization of the SSCV and AHT. If full removal is required, an additional 50 days of operational time by the SSCV and AHT is estimated to be required to remove the topside and jacket of each HHH platform. This could be reduced to about 15 days per platform if the jackets are converted to artificial reefs. Only one SSCV and AHT campaign may be required if the HHH jackets are reefed, compared to the four campaigns required for the full removal scenario. This would result in a 75 percent reduction in CO2 and NOX emissions.

damaged Vineyard Wind turbine – Cape Cod Times photo

Excerpt from p.3 of Vineyard Wind’s suit against GE Renewables (attached):

“As was widely reported in national and local news, in July 2024, one of the GER offshore blades collapsed and fell into the waters off Nantucket, necessitating a massive environmental cleanup, and a six-month construction hiatus during which GER performed a “root cause” analysis. That analysis concluded that 68 of the 72 GER blades installed at the Project (nearly all manufactured by GER in Gaspé, Canada) were also defective because they were inadequately bonded together, and were so poorly made that they were beyond repair. GER’s remediation plan required it to remove all of the blades and to replace all Gaspé blades with others manufactured at a different facility in Cherbourg, France.

Regulatory issues of concern:

Nearly 2 years after the blade failure, all Vineyard Wind (VW) turbine blades have been installed, yet BSEE has still not issued their investigation report. The primary purpose of independent Federal investigations is to prevent recurrences at this or other projects in the US and worldwide. The investigation should assess the extraordinary VW blade defect rate.

DNV was the Certified Verification Agent (CVA) for the VW project, and was thus required to verify the design, fabrication, and installation procedures. When will we hear from them?

BOEM waived the requirement that the Facility Design Report (FDR) and Fabrication and Installation Report (FIR) be “received and offered no objections to” before beginning the fabrication of facilities. They did so to “allow Vineyard Wind to adhere to its construction schedule, maintain its qualification for the Federal Investment Tax Credit, and meet its contractual obligations under the Power Purchase Agreements with Massachusetts distribution companies.” Did BOEM’s commitment to promoting offshore wind and accelerating development influence their regulatory decisions?

It’s clear the proposed rules have been designed to reduce financial burdens on OCS oil and gas operators, especially small independents. The proposed rules do this by:

Waiving the requirement of the operator/lessees to obtain supplemental financial assurance to cover decommissioning obligations if jointly and severally liable predecessors are determined to have the financial capability to cover the obligations.

Lowering the credit rating threshold BOEM uses for evaluating the financial health lessees and grantees from BBB- to BB- from S&P Global Ratings (S&P) or Baa3 to Ba3 from Moody’s Investor Service Inc.

Revising the level of BSEE probabilistic estimates of decommissioning cost used for determining the amount of supplemental financial assurance required from P70 to P50.

I don’t see any rationale for lowering the credit rating threshold, which would apply to both current and predecessor lessees. A BB- and a Ba3 rating is considered “non-investment grade” or “junk,” meaning the company is more vulnerable to adverse economic conditions, such as a downturn in oil and gas prices. Current market estimates place the 3-year probability of default for a BB- rating at approximately 12.5% to 13%. Lowering the credit rating significantly increases the risks of default by lessees and transfers the risk to the federal government and taxpayers.

Reducing the BSEE probabilistic criteria for determining the amount of supplemental financial insurance required from P70 to P50 means there is a 50% chance BSEE cost estimates for decommissioning are underestimated further increasing risks borne by the federal government and taxpayer.

BOEM should reverse course and maintain the current credit rating threshold (BBB- and Baa3) and the P70 criteria.

BOEM extends comment period on the financial assurance proposal, but only by one week!

Posted in decommissioning, energy policy, Regulation, tagged BOEM, decommissioning, extension of comment period, financial assurance, proposed regulation on May 7, 2026| Leave a Comment »

BOEM has extended the public comment period and will accept comments on the proposed rule through 11:59 p.m. Eastern Time on May 15, 2026.

Interesting decision, and not the one many of us expected.

Read Full Post »