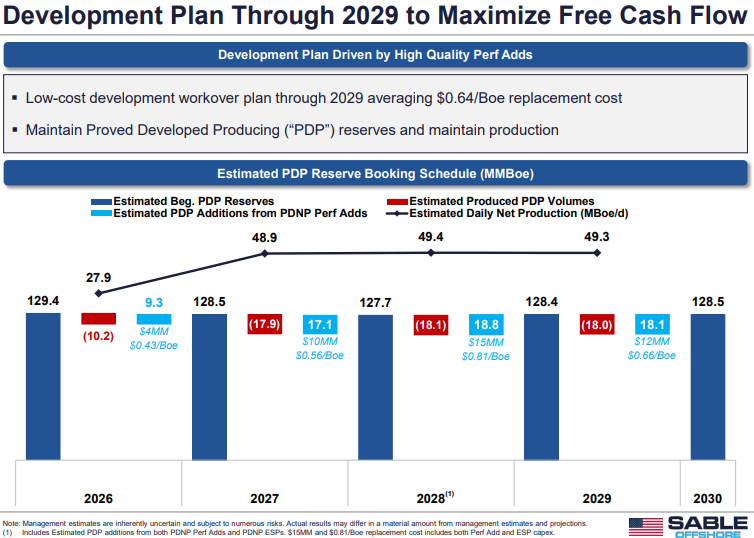

Those who have been following the Santa Ynez Unit saga should take a look at Sable’s informative PowerPoint update (attached). The presentation includes reserve data, well operation plans, production forecasts, financial and legal updates, and regional energy supply information.

Also, Sable CEO Jim Flores has announced that Energy Secretary Wright and Interior Secretary Burgum will be visiting the project this week. Transportation Secretary Duffy was also expected, but he will not be attending.

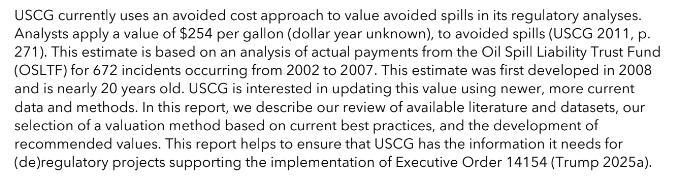

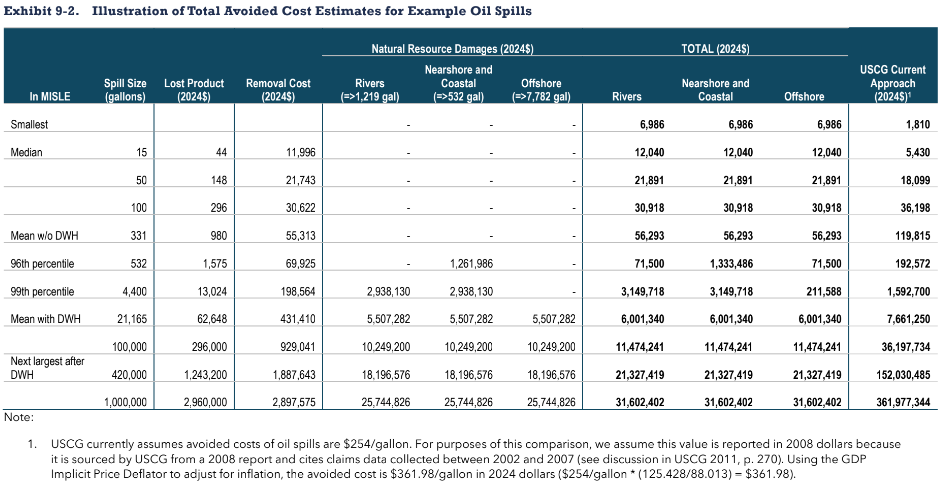

The report is intended to update the Coast Guard’s methodology for estimating the cost savings resulting from spill prevention regulations. The paragraph pasted below is a good summary of the objective.

The offshore industry could benefit from this report, because the estimated cost of spills >100 gallons is reduced, dramatically so when the DWH/Macondo blowout is excluded (see the second table below). That reduction would support regulatory reform initiatives,and could thus generate some controversy.

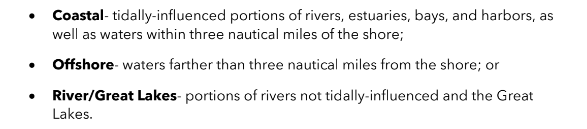

My main concern is that there is only a single distance-from-shore category for offshore spills (see text below). The natural resources damage from a spill 3 miles from shore will almost always be much greater than from an equivalent volume spill 100 miles from shore.

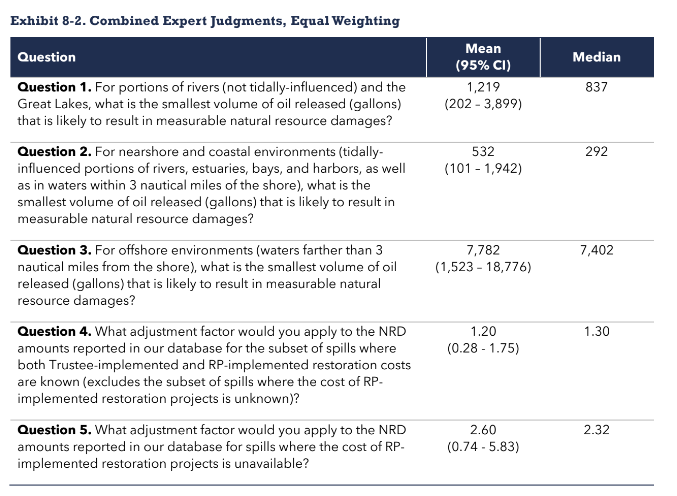

The single-offshore-category issue is illustrated in the 2 tables pasted below. The first table presents a summary of expert opinions on the smallest spill size that is likely to result in measurable natural resource damages. The mean response to Question 3 (offshore) is 7782 gallons. A spill of that size occurring 3 miles from shore is much more likely to result in resource damage than a spill originating 50 or 100 miles from shore.

In the second table, note the new methodology results in the same cost estimates for large nearshore/coastal spills as for offshore spills. Again, this is presumably because there is only a single offshore category.

The public comments on this report should be interesting.

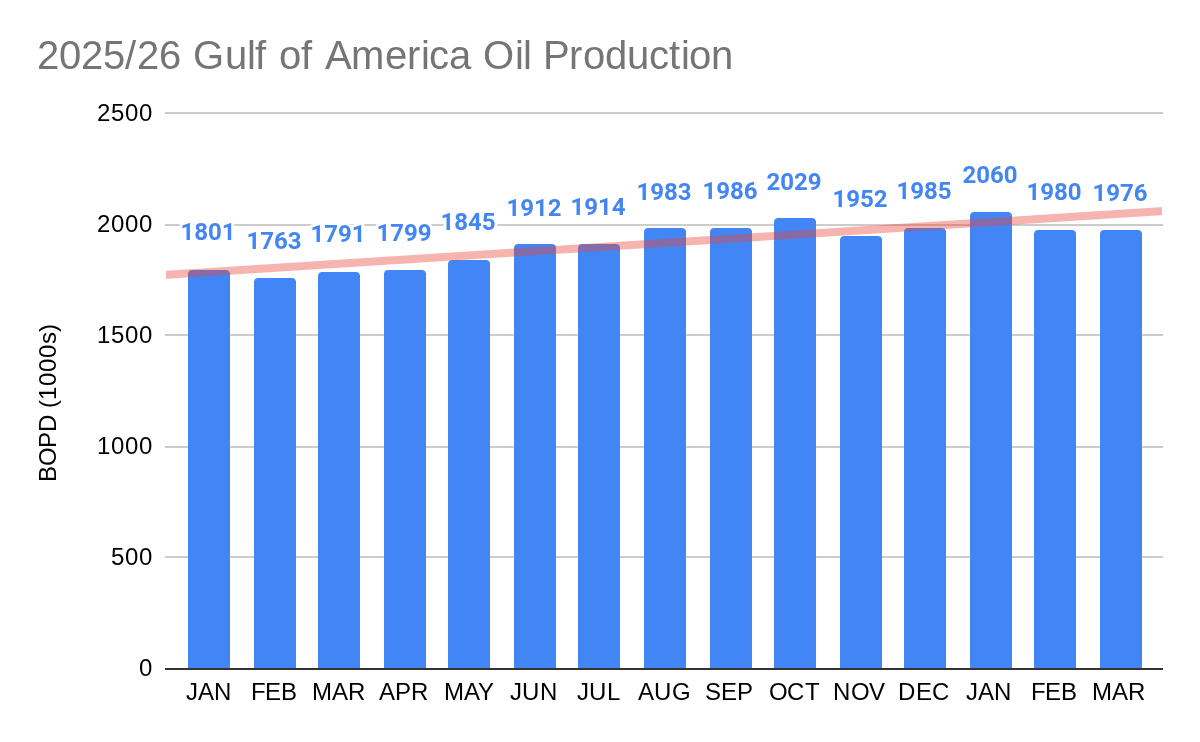

BOEM Press Release: “The Bureau of Ocean Energy Management announced today the critical role of offshore leasing, resource assessment and long-term planning in supporting record oil production on the U.S. Outer Continental Shelf, which reached more than 714 million barrels in 2025.”

Was 2025 a record OCS oil production year?No, 2025 came very close, but barring belated revisions, 2019 retains the record.

Did 2025 oil production exceed 714 million barrels? Not even close according to the US Energy Information Administration (EIA), which reported a final OCS production total of 692.6 million barrels for 2025. The Office of Natural Resources Revenue (ONRR), to whom all production data must be reported, has yet to post their final 2025 numbers, but they are normally very close to the EIA totals. Also, ONRR’s fiscal year totals do not suggest calendar year production in excess of 700 million barrels. BOEM’s announced 714 million barrel CY 2025 total is more than 60,000 bopd higher than the actual EIA CY or ONRR FY daily averages, and even exceeds the total posted in BOEM’s data center.

See the 2019 and 2025 oil production totals in the table below. The BOEM 2025 numbers appear to be erroneous.

On the plus side, per EIA’s latest update, Jan. 2026 was a record production month for the Gulf. January’s ave. production of 2.060 million bopd surpassed the Aug. 2019 ave. of 2.044 million bopd.

Barring significant tropical storm shut-ins over the next 6 months (hurricane season starts today!), a production record in 2026 seems like a good possibility.

Santa Barbara Channel, Dos Cuadras Field platforms (L to R): Hillhouse, A, B, and C; Antandrus Wiki photo

As part of the recent focus on decommissioning and financial assurance requirements, I looked at borehole data for platforms A, B, and C on Lease OCS-P 0241 in the Santa Barbara Channel. Platform “A” is where a well blew out in 1969, permanently scarring the US offshore program. Observations:

There are 140 completed and unplugged wells on the 3 platforms. None of the wells on these platforms have been permanently plugged and only one is temporarily abandoned.

The latest available production information (2024 data) indicates ave. daily oil production of 3791 bopd for the lease, including 1901 bopd from Platform A, the highest production for any platform in the region in 2024.

41 of the lease’s completed (unplugged) wells are on Platform A.

The number of these wells that are currently producing is not publicly available.

30 of the completed Platform A wells were drilled prior to 1985.

The blowout well was the 5th well drilled from platform A. All 4 of the wells drilled prior to the 1/28/1969 blowout are still unplugged:

well A-20: spudded on 11/19/1968, reached total depth on 12/2/1968

well A-41: spudded on 11/27/1968, TD on 12/19/1968

well A-25: spudded on 12/18/1968, TD on 12/28/1969

well A-38: spudded on 1/12/1969, TD on 1/24/1969

Note how quickly the wells were drilled. The wells were shallow (2299-4051′ true vertical depth), and the operator (Union Oil) saved time by omitting a casing string. (This decision was a root cause of the blowout and thus changed history 😡)

Lease documents and regulations at 30 CFR § 250.1710require that all wells be permanently plugged within one year of lease termination. For leases like 0241 that are still active, 30 CFR § 250.1711 stipulates that BSEE will order a well to be permanently plugged if the well poses a hazard to safety or the environment, or is not useful for lease operations and is not capable of oil, gas, or sulphur production in paying quantities. In the Gulf of America Region, the policy is to require wells that have not been used in the past 5 years to be permanently plugged. Allowing old wells to remain unplugged is neither prudent nor consistent with the regulations.

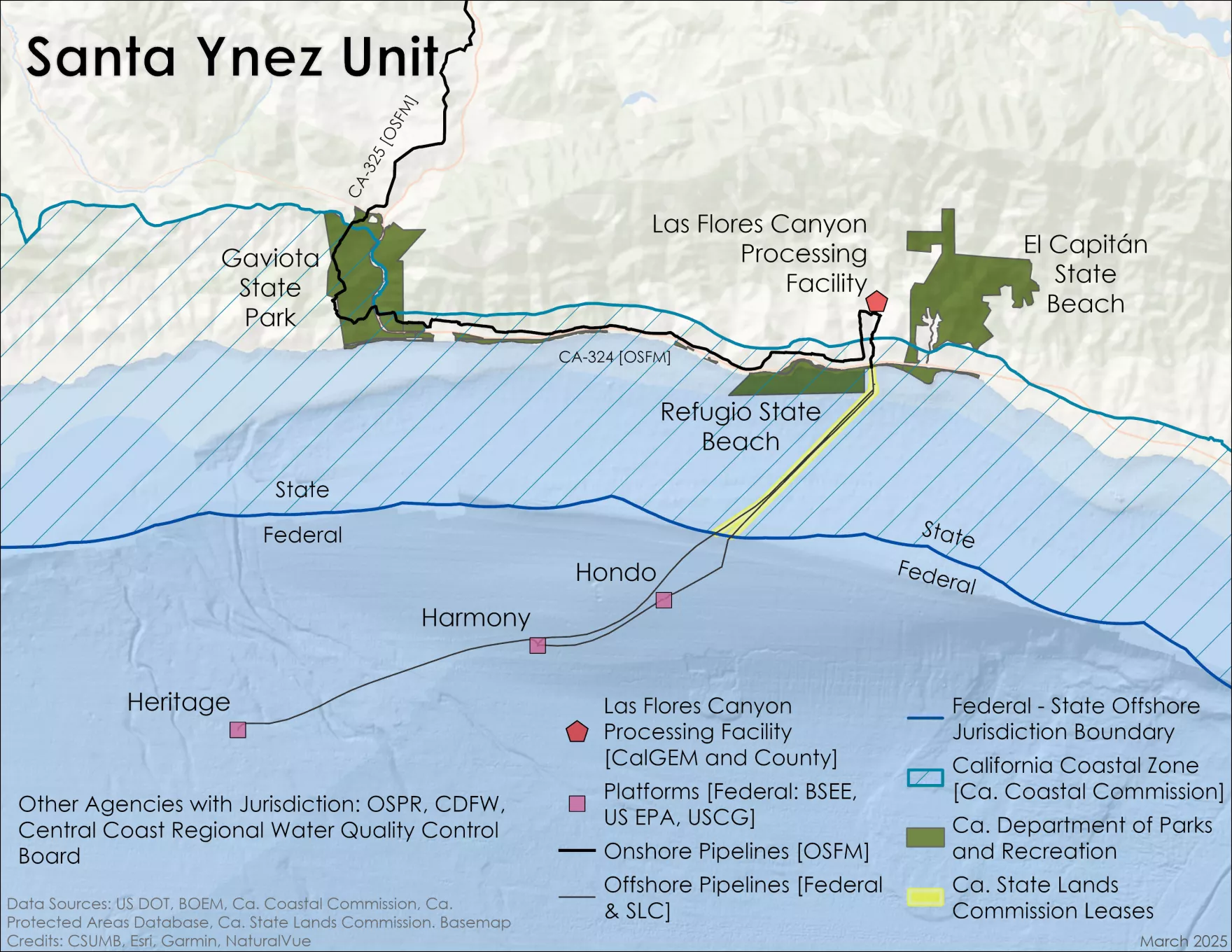

Judge Stephen V. Wilson, US District Court for the Central District of California ruled that Sable’s pipeline doesn’t imminently harm Gaviota Park. Judge Wilson said the state “is grasping at straws,” for evidence of real environmental harm, and the federal consent decree governing the terms of the system’s restart is controlled by the California Office of the State Fire Marshall, not the parks department.

The judge didn’t rule on the larger question of whether the Defense Production Act order to restart the Las Flores pipeline system was lawful.

John Smith’s update on California OCS Decommissioning Obligations is attached. His comments:

Chevron and FMC hold joint and several liability responsibilities for many platforms and all of those operated by DCOR. This reflects Chevron’s long history in developing CA onshore and offshore oil and gas resources. A 2020 report issued by BSEE estimated the nine platforms operated by DCOR had a combined decommissioning cost of $397 million.The actual cost could be 2-3-fold higher based on estimates for decommissioning California state water platforms prepared by experienced decommissioning consultants.

Chevron may be checking out of California by moving its corporate offices to Houston, but as someone once said about decommissioning – referring to the popular Eagles Hotel California song “You can check out but you can never leave.”

Official decommissioning anthem 😉: Hotel California

Excerpt from the lyrics – Hotel California, Eagles, 1976

Last thing I remember I was running for the door I had to find the passage back To the place I was before “Relax, ” said the night man “We are programmed to receive You can check out any time you like But you can never leave”

Permian drilling rigWest Vela drillship made Walker Ridge discovery for Talos

Per yesterday’s discussion comparing recent onshore and offshore lease sales, the investments are really quite different. When you acquire Permian and Delaware Basin shale tracts you are essentially buying oil in place that should be producible with current technology.

At offshore sales, you are typically acquiring the opportunity to learn more, either through site surveys or drilling. Your lease exploration and development strategy will also be influenced by drilling outcomes for similar targets on other leases. A return on your investment is far from certain.

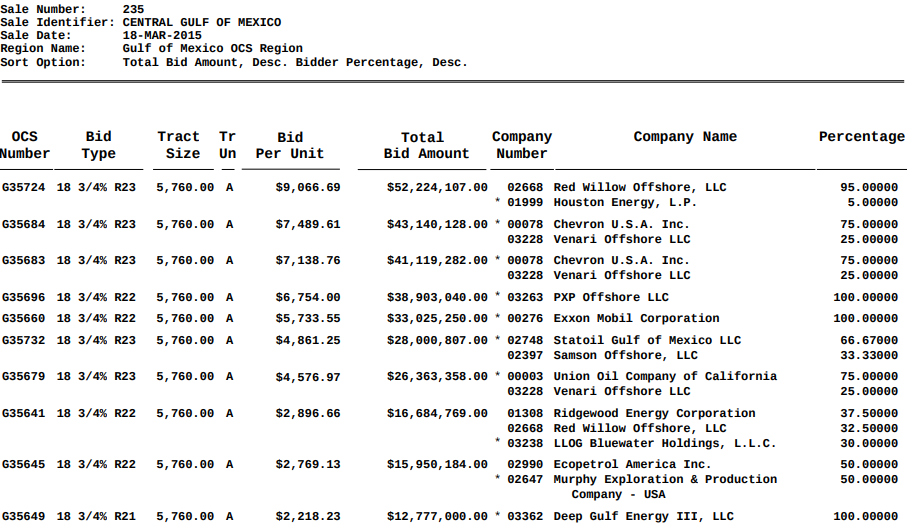

I looked back at the top ten leases (by high bid) issued at Central Gulf Sale 235. That sale was chosen because it was 11 years ago, giving time to explore and initiate development, and the bidding was strong. The top ten leases received bids ranging from $12.8 million to $52.2 million. See the screenshot below.

Surprisingly, only four of the leases were ever drilled and nine of the ten leases have expired. The only lease remaining is the highest bid block (OCS-G 35724, Walker Ridge Block 107, $52.2 million) now owned by Talos (27% and operator), Red Willow (22.5%), Shell (22.5%), CSL (9%), and two investment partnerships. This lease is being held by operations given that a well was drilled within the past year. However, Talos has announced a discovery, and the well has been temporarily abandoned to preserve future utility:

The discovery well was drilled to a total vertical depth of 33,228 feet utilizing the West Vela deepwater drillship and encountered oil pay in multiple high-quality, sub-salt Miocene sands. A comprehensive wireline program was conducted, acquiring core, fluid, and log data to evaluate the reservoir.

So the bottom line is $308.3 million in bonuses for 10 leases, 9 of which have now expired, and one discovery which could prove to be commercial down the road.

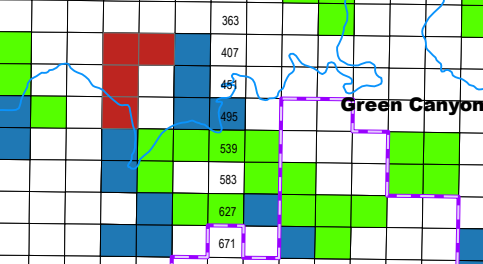

Although BOEM’s decision matrix has not yet been posted, a comparison of the acceptances with the bids submitted tells us that the Keathley Canyon Block 828 ($1,101,202) and Atwater Valley Block 63 ($650,018) bids were rejected.

Both of the rejected bids were submitted by LLOG, partnering with 4 other companies on the Atwater Valley block. LLOG’s high bids on 3 other blocks were accepted, so their rejection rate was 40%. Interestingly, 2 of the 3 BBG1 rejected bids were also submitted by LLOG.

There is no shame in bid rejections, which are part of the legislated leasing process. Why pay more than you have to (or think a block is worth)? A bid rejection may attract future competition, but otherwise the only downside is that you don’t get a lease that you can possibly acquire at another sale if desired (an advantage of regular, predictable lease sales).

BOEM is charged with making fair market value determinations and their process and decisions are publicly available. Of course, opinions differ on the value of an unexplored lease. We will see what the bidding on the BBG1 and BBG2 rejections looks like in future sales.

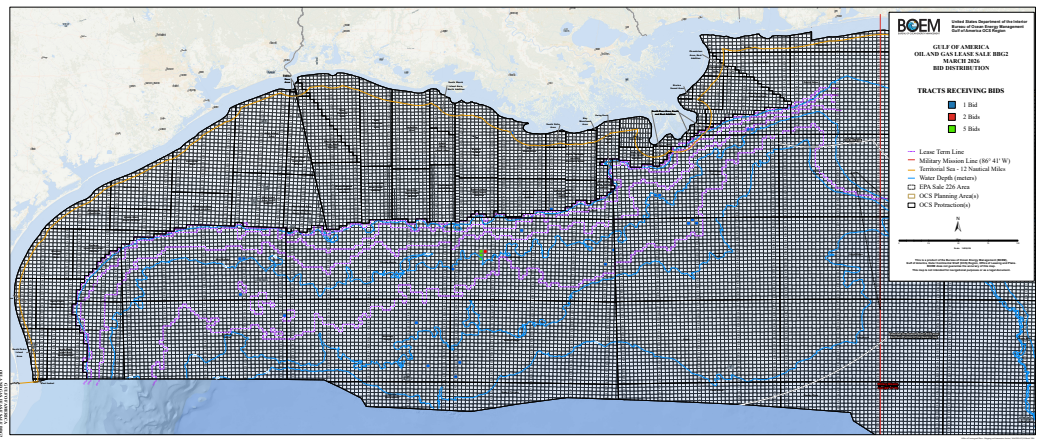

BOEM did accept the the high bids for the BBG2 “sweet spot” blocks (red in map below; also see the table) in the Green Canyon Area of the Gulf. These 4 blocks accounted for 17 of the sale’s 38 bids (45%) and $32.8 milion of the sale’s $47 million in high bids (70%). BP’s $21 million bid for GC 404 was by far the sale’s highest bid.

red=blocks receiving bids at BBG2; blue=BBG1 and Sale 261 leases; green=active leases issued prior to Sale 261

The CBD had challenged an April 2025 BOEM decision concludingthat Sable was not required to revise its development and production plan for the SYU. They sought a court order requiring a revised plan. This suit seemed to be a stretch, so its dismissal is not a surprise.

Per the Dept. of Justice, the court dismissed the lawsuit because the plaintiffs’ asserted procedural injury had no basis in the statute, was not traceable to any action by BOEM, and could not be redressed by an order of the court.(Other than that, it was just fine. 😉)

Among other problems the court identified with the plaintiffs’ case, they invoked a provision of the statute that governs “approval of a development and production plan,” not revision of an already-existing plan. It will be interesting to see the full decision so that we can better understand the context for that statement. Distinguishing revised plans in that manner could have significant policy implications.

For a full update on Sable litigation, see the section of their Quarterly Report beginning on p. 12.