Requesting a 60 day extension (double the comment period specified by BOEM)

Need more time to:

review the detailed proposed changes

conduct studies to inform agency

analyze the studies and data

consider alternatives

organize, complete, and review the findings of subject matter workgroups

In API’s favor:

Agencies have discretion on extending comment periods.

60 days is typically considered the minimum comment period; 90 days would have been more appropriate for this proposal.

API members are clearly affected parties.

The BOEM proposal relaxes financial assurance requirements for smaller companies while increasing predecessor lessee risk exposure. Those predecessors would typically be API members.

There are divisions within the industry which complicate trade association commenting.

On the other hand:

API’s letter is dated May 1, just one week prior to the end of the comment period.

The letter was not posted at Regulations.gov until May 6, 2 days before the end of the comment period. Only those tracking the comment letters would have been aware of the request even at this late date.

As of early this morning (May 7th), the docket still specifies a May 8 due date for comments.

An extension could be viewed as inequitable to other concerned parties who made special efforts to honor the deadline.

Comments:

This is why it’s best to specify a reasonable comment period at the time the regulation is proposed, and make it clear that there will be no extension. That way, everyone is treated the same.

For this proposal, 90 days would have been reasonable.

Given the number of significant issues that need to be addressed, the best outcome for this rule would be a re-proposal. See the comments submitted by John Smith and me.

Attached are my comments on BOEM’s proposed revisions to the decommissioning financial assurance regulations. These comments were submitted to Regulations.gov yesterday (3 days early 😀). Bud

Concluding Remarks

MMA’s highest priority must be assuring that facilities are safely decommissioned without public funding. Supplemental financial assurance determinations and lease assignment approvals must be consistent with that priority.

Predecessor liability is an important financial assurance principle, but legal boundaries and administrative procedures must be clearly established.

Safety and compliance are inextricably related to financial performance, and must be considered in determining supplemental assurance requirements.

Using reserve estimates to reduce supplemental assurance exposes taxpayers to geologic and accounting risks.

Unacceptable public risks have resulted from financial assurance decisions intended to advance offshore wind development.

An apology letter from the California Coastal Commission (CCC) to SpaceX was part of a lawsuit settlement. SpaceX alleged political bias in the commission’s 2024 decision to deny increased Falcon 9 launches at Vandenberg Space Force Base, based on comments about Elon Musk’s political views and SpaceX’s labor practices.

Excerpt:

“In 2024, the Commission reviewed consistency determinations by the U.S. Space Force for SpaceX’s Falcon 9 launch program at Vandenberg Space Force Base. During that review, some Commissioners made negative comments about SpaceX’s labor practices and its Chief Executive Officer’s political views. The Commission acknowledges that these political comments were irrelevant to the Commission’s consistency review and were improper, and the Commissioners apologize for those comments.”

AI confirms my suspicions that formal CCC apologies are highly unusual 😉

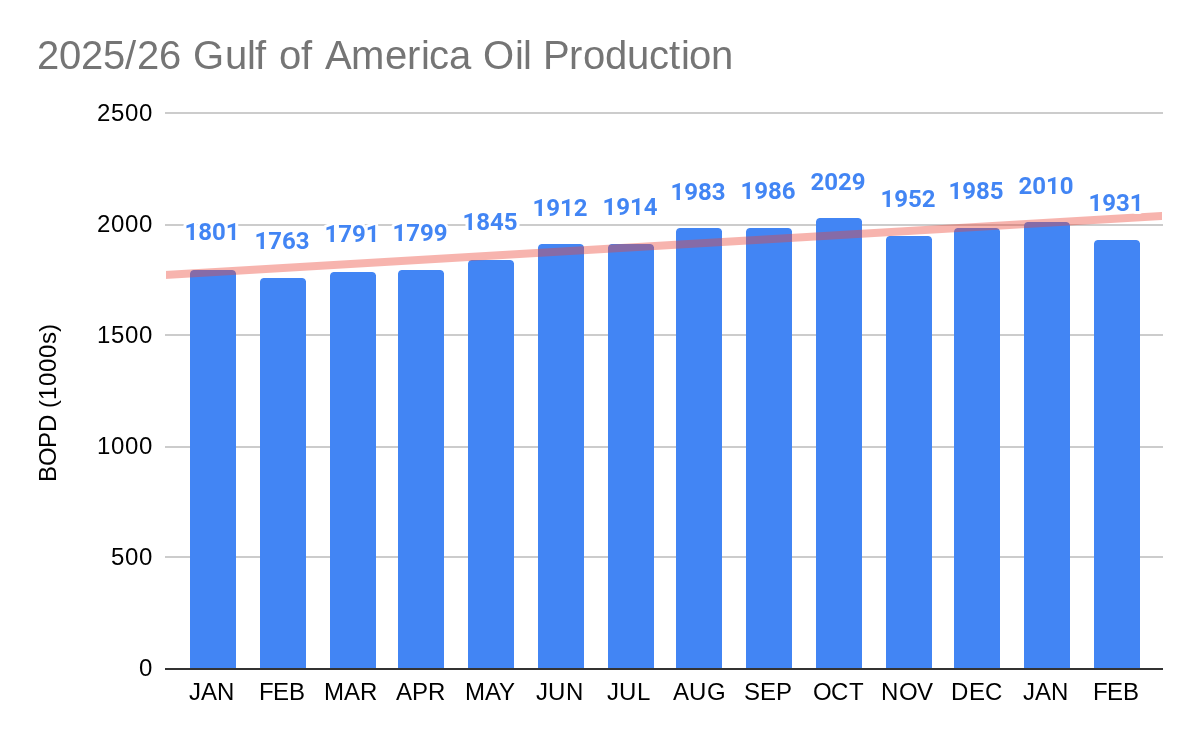

Update: Another EIA revision to Gulf of America oil production for Dec. 2025 (1.994 to 1.985 million bopd) means that 2019 retains the production record by the narrowest of margins – 1.898 to 1.897 million bopd. Stay tuned because this may not be the final word 😉.

Per EIA, Feb. 2026 production dipped a bit to 1.931 million bopd (chart below).

Meanwhile, California OCS oil production for FEB continued at about 10,000 bopd. This number may increase a bit for March, and more for April data when the first Sable sales are included. A big increase, by as much as 500%, should be apparent in the June report barring a court ordered shutdown.

Sable’s updated PowerPoint presentation is attached.

Also, the 2025 compensation package for Sable CEO Jim Flores is attracting attention. Flores received $76 million in total compensation. The bulk of his pay came from more than $69 million in stock awards, alongside a $1.3 million salary and a $3.9 million bonus.

Equinor has cut planned investments in renewable energy by roughly EUR 3.5bn for 2026–2027, while the company maintains and expects growth in oil and gas production.

Perhaps the premium for climate virtue signaling has shrunk, and Equinor, like other energy giants, is making a prudent business decision for its shareholders, which include the Norwegian govt.

Meanwhile, what are the implications for Equinor’s offshore wind investments in the US? Equinor’s embattled Empire Wind project is probably too far along to reverse course. Their Central Atlantic (Lease 0557) and California (Lease 0563, Atlas Wind) may be a different story. However, buyback negotiations would be complicated by the Empire Wind situation, and perhaps by the Norwegian government’s 2/3 ownership. On the other hand, Equinor is a significant oil and gas leaseholder in the Gulf of America, so they would have ample options for investing wind lease rebates.

The transition reflects more than a decade of operational experience managing offshore resources. By consolidating the planning, permitting, inspection, and enforcement responsibilities currently divided between BOEM and BSEE, the Department aims to:

Improve coordination and consistency

Reduce duplication of efforts

Strengthen oversight and environmental safeguards

Modernize organizational structure

All current regulatory responsibilities and protections will remain in place throughout the transition. There will be no disruption to permitting, environmental reviews, or enforcement activities.

What to Expect

Phased Transition: Internal alignment activities begin soon.

No Regulatory Rollbacks: Existing requirements remain in full effect.

New Website and Branding: The Marine Minerals Administration’s full digital presence will launch in the coming months.

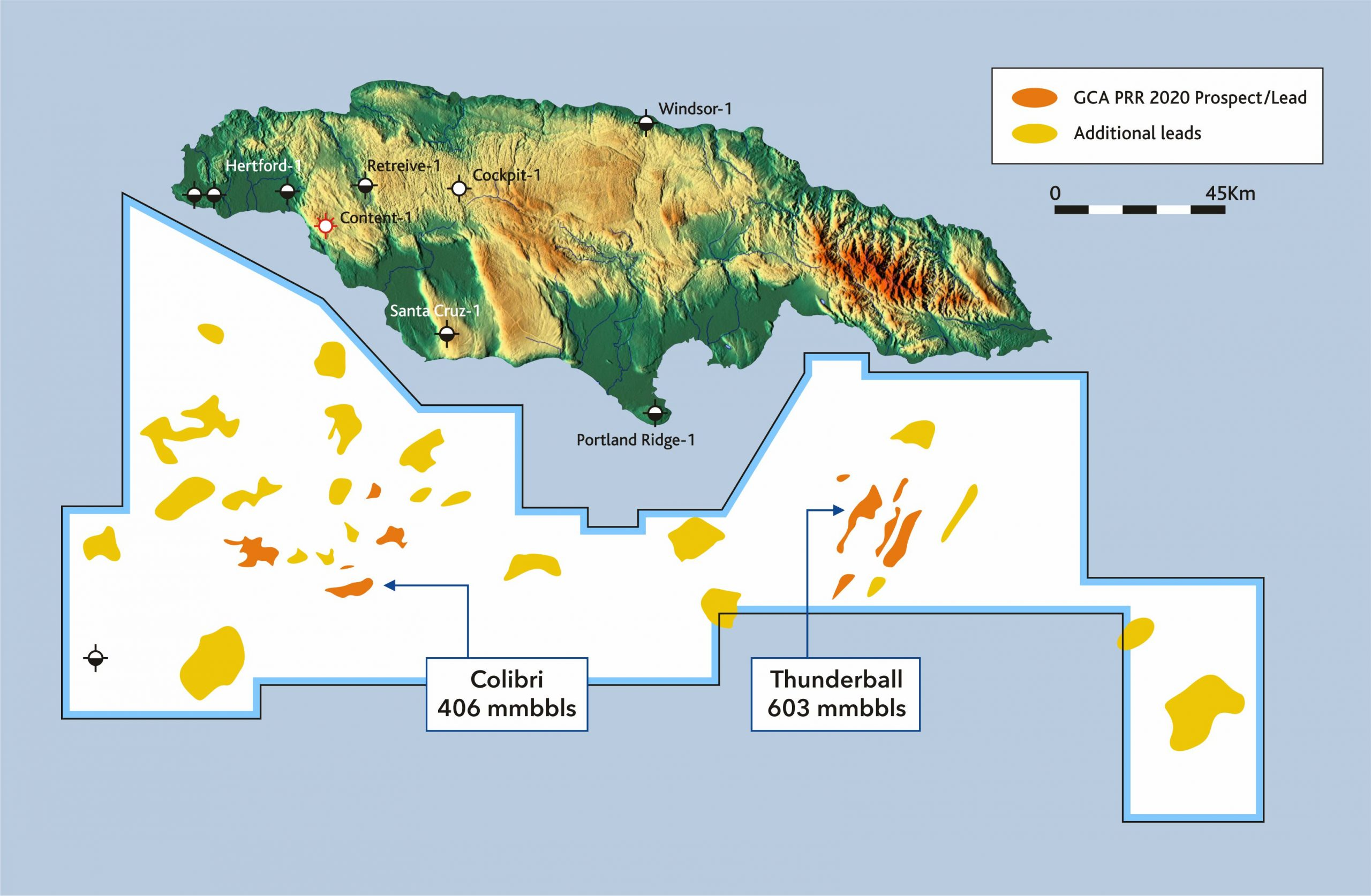

United’s 22,400 sq km offshore Walton-Morant exploration license offshore Jamaica. Typical US offshore leases are only 23.3 sq km. The Jamaican license is thus nearly 1000 times larger than a US offshore lease!

“United has undertaken a geochemical analysis on the 42 piston cores acquired across the Walton-Morant Licence. The analysis has identified C4 and C5 hydrocarbons, including butanes and pentanes, in select piston cores within the headspace gas dataset. United note that these higher order hydrocarbons are not typically associated with biogenic gas systems and are therefore consistent with a potential thermogenic contribution. (This is true.)

There is an established body of evidence for an active petroleum system in Jamaica in general, and on the licence in particular, including repeat satellite slick anomalies, thermogenic hydrocarbon geochemistry from existing onshore and offshore wells, onshore and offshore oil seeps, and onshore surface outcrops. Furthermore, petroleum systems modelling suggests the presence of oil-mature source rocks. The 2026 SGE survey is the first on the licence to be optimally positioned using 3D seismic, multibeam echosounder (MBES) seabed mapping, and satellite-derived slick anomaly data. Taken together, the data are interpreted as consistent with an active petroleum system offshore Jamaica.“

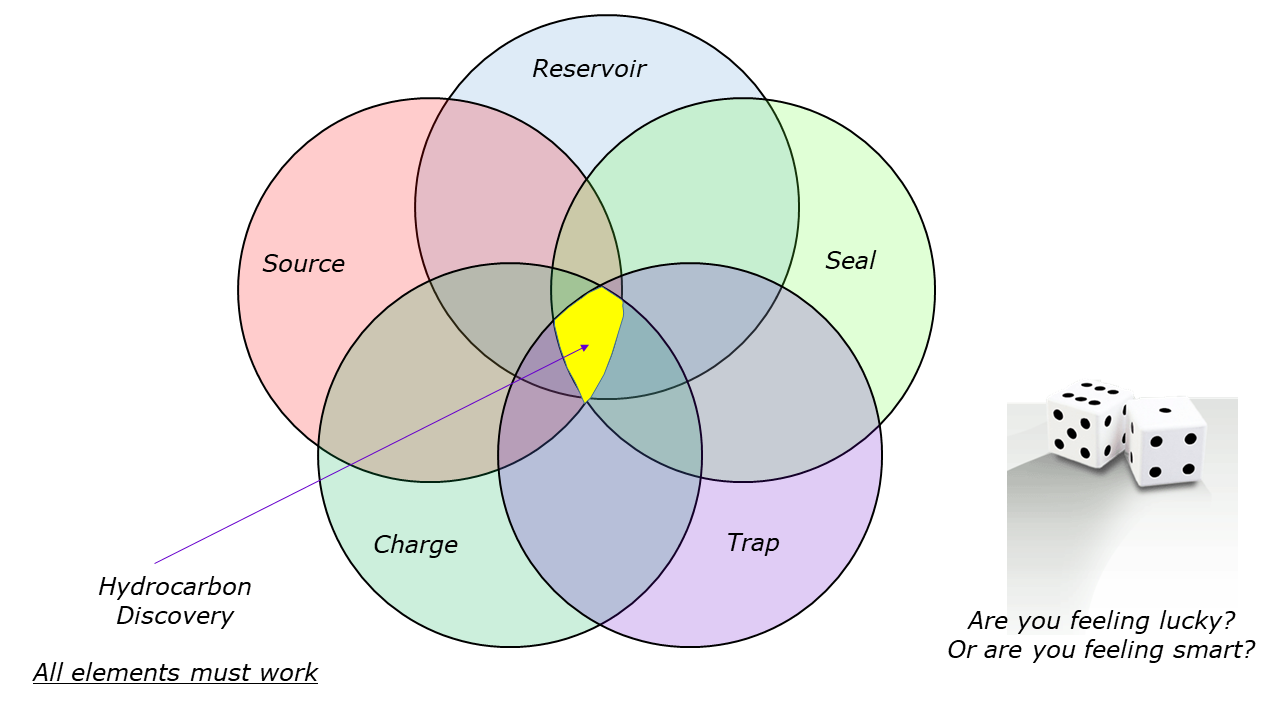

United estimates that the piston coring results boost the Geological Chance of Success (i.e. the source rock, reservoir, trap, and seal—are present and working) for the flagship Colibri prospect from 19% to 32%, which is quite good for frontier exploration.

Will these new data help entice majors to fund exploratory drilling? In the video below (ignore the click-bait title cover 😉), Energy Minister Daryl Vaz does a good job of adding perspective.

BOEM extends comment period on the financial assurance proposal, but only by one week!

May 7, 2026 by offshoreenergy

BOEM has extended the public comment period and will accept comments on the proposed rule through 11:59 p.m. Eastern Time on May 15, 2026.

Interesting decision, and not the one many of us expected.

Posted in decommissioning, energy policy, Regulation | Tagged BOEM, decommissioning, extension of comment period, financial assurance, proposed regulation | Leave a Comment »