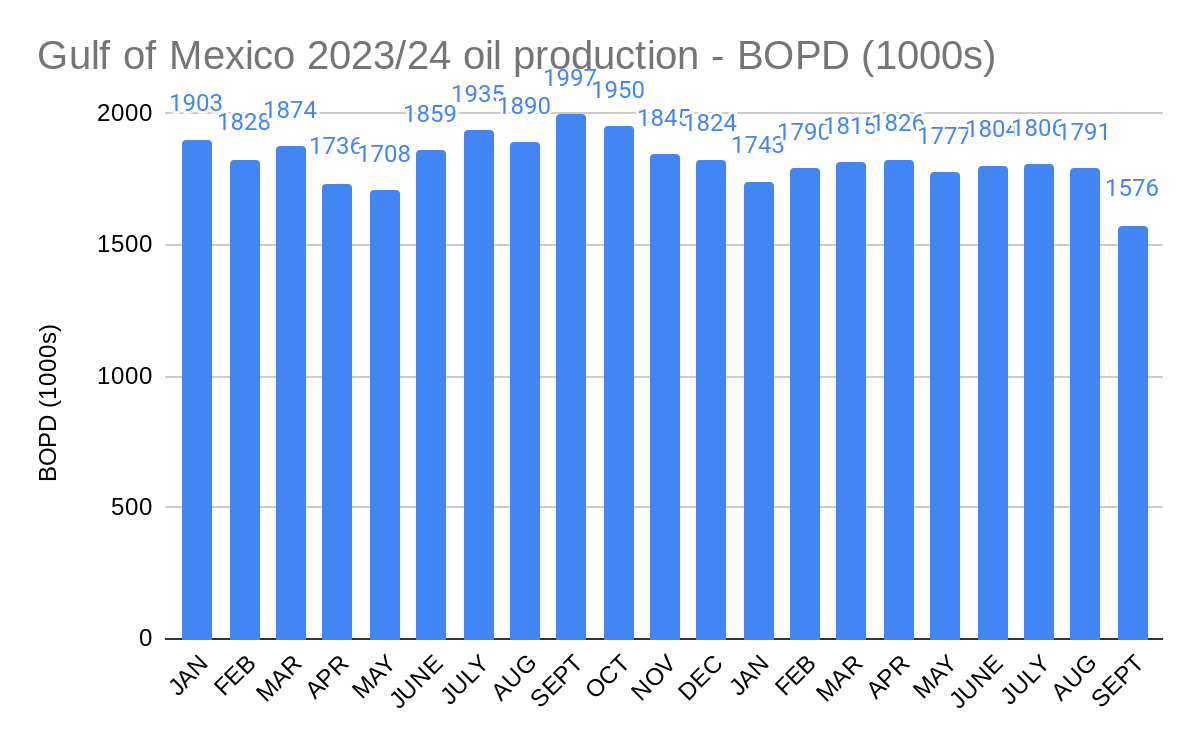

As expected, the Gulf of Mexico’s remarkable 7 month production consistency streak ended in September as a result of shut-ins associated with Tropical Storms Francine and Helene. Nonetheless, average daily production still amounted to 88% of the ~1.8 million bopd average that had been achieved for the previous 7 months. Rather impressive resiliency!

A recent Nantucket Current piece criticizes the Nantucket Select Board for failing to address community concerns about the attached Good Neighbor Agreement (GNA) with Vineyard Wind. In particular, any discussion about the GNA was throttled at a recent public forum on the SouthCoast Wind project.

Some key points from the article and related thoughts:

The GNA established a long-term relationship between Vineyard Wind and Nantucket. In essence, Nantucket became a partner and an advocate for the projects.

Sections 5.2 and 5.3 of the GNA are particularly striking and believed to be unprecedented in the history of Federal offshore energy programs.

Section 5.3 stipulates that “the Nantucket Parties shall use their reasonable best efforts to inform federal, state, and local elected officials of their support for the Projects” throughout the environmental, historical, and state review processes. Wow, nothing subtle about that directive!

By signing the GNA with Vineyard Wind, Nantucket withdrew from the important National Historic Preservation Act consulting process for these projects.

Vineyard Wind, New England Wind, and the other projects that are covered under the GNA will add approximately 350 turbines off Nantucket’s south shore beaches.

Given the partnership with Vineyard Wind, it’s difficult for Nantucket to challenge the mitigations for another project, SouthCoast Wind, which is not covered by the GNA.

The Nantucket GNA controversy should be carefully considered by other communities that are tempted by developer incentives to enter into agreements that may not be in their best long-term interest.

Will Nantucket exit (Nexit) the GNA? The pressure is building.

Attached is an excellent Scientific American article featuring BOE contributor and decommissioning specialist John Smith, former colleague and marine biologist Dr. Ann Bull, and Dr. Milton Love, the leading authority on California’s offshore platform ecosystems.

I had the pleasure of taking a highly informative boat tour around Platform Holly with Dr. Love and a group of international visitors. Holly, which is pictured at sunset in the BOE header, is among the platforms awaiting decommissioning.

Dr. Love on the total removal of California offshore platforms:

“As a biologist, I just give people facts,” he says. “But I have my own view as a citizen, which is: I just think it’s criminal to kill huge numbers of animals because they settled on a piece of steel instead of a rock.”

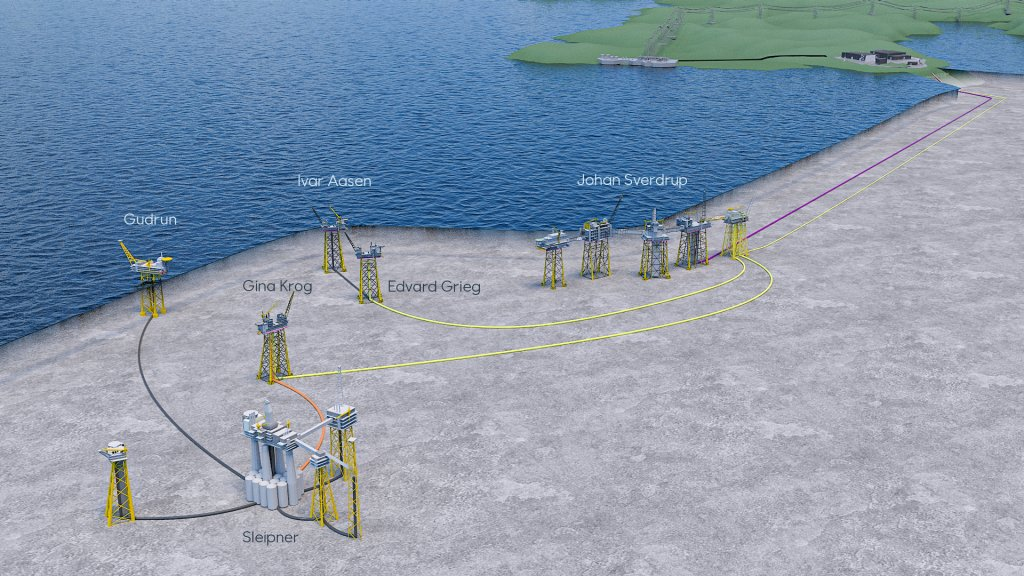

Production from Equinor’s important Johan Sverdrup field, which accounts for 755,000 bopd (36% of Norway’s oil production), was shut-in on Monday as a result of a power outage. Production was in the process of being restored on Tuesday.

According to Equinor, the outage was caused by overheating at an electric converter station onshore.

A 2022 BOE post questioned Norway’s push to power offshore platforms with electricity transmitted from shore. This incident reinforces those concerns. Summary:

Most offshore platforms produce sufficient gas to support their power demands

Assuming gas that is not used to power a platform is marketed and consumed elsewhere, the net (global) reduction in CO2 emissions from electrifying offshore platforms is negligible. (Perhaps there is actually a small increase in net emissions given the power required to transport the gas to markets and the emissions associated with onshore power generation).

Offshore power demands are highly variable, especially when drilling operations are being conducted.

Gas turbines are reliable, and capable of responding to variable power demand. Excess generation capacity is typically provided.

Power from shore increases the cost of platform operations and could decrease ultimate recovery of oil and gas resources.

Per NPD, electrification of the shelf will increase electricity prices for onshore consumers and increase the need for onshore facility investment.

Gas turbines or diesel generators are still necessary to satisfy emergency power needs at the platforms.

Long power cables are vulnerable to damage (accidental or intentional), as are onshore power stations.

I hope the investigation of this incident considers some of these broader electrification policy issues.

Equinor diagram: The purple cable shows power from shore to Johan Sverdrup phase 1, established in 2018. The yellow power cable shows power from shore to Johan Sverdrup phase 2 and the Utsira High area solution, from 2022. The orange cable shows power from shore to the Sleipner field centre and connected fields from late 2022. Black cable shows existing power cables at Sleipner field centre and to the Gudrun installation.

The Secretary of the Interior is the most important energy production position in the US govt, particularly for the offshore sector.

In recent years energy policy has been increasingly influenced (if not directed) by White House staff, most notably the White House Climate Office. Given that Burgum will also lead the new created National Energy Council, direction from White House staffers or other departments should not be an issue.

Burgum should work effectively with Dept. of Energy appointee Chris Wright, an engineer who understands energy production.

There is no apparent Republican dissent, so Burgum should have no problem being confirmed.

All of the offshore policy forecasts in the post-election post still stand.

Burgum is currently the Governor of North Dakota. Some energy production stats for the state:

ND ranks 4th if the OCS, for which Bergum will soon be responsible, is included. The OCS ranked 2nd in oil production, behind only TX, despite seemingly being managed to fail.

Wind: In 2023, wind was the second-largest electricity generating source in ND behind coal. At the beginning of 2024, ND had about 4,000 megawatts of installed wind power generating capacity.

What about carbon sequestration (disposal)?

As Governor, Burgum supported CCS projects that could be lucrative for North Dakota.

As Interior Secretary and Energy Czar, he will have to consider the high Federal subsidy costs, efficacy, and net environmental benefits.

Companies looking to benefit from publicly financed CCS projects will lobby hard for Federal support. Budget hawks and most environmental activists will be strongly opposed. It will be interesting to see who prevails.

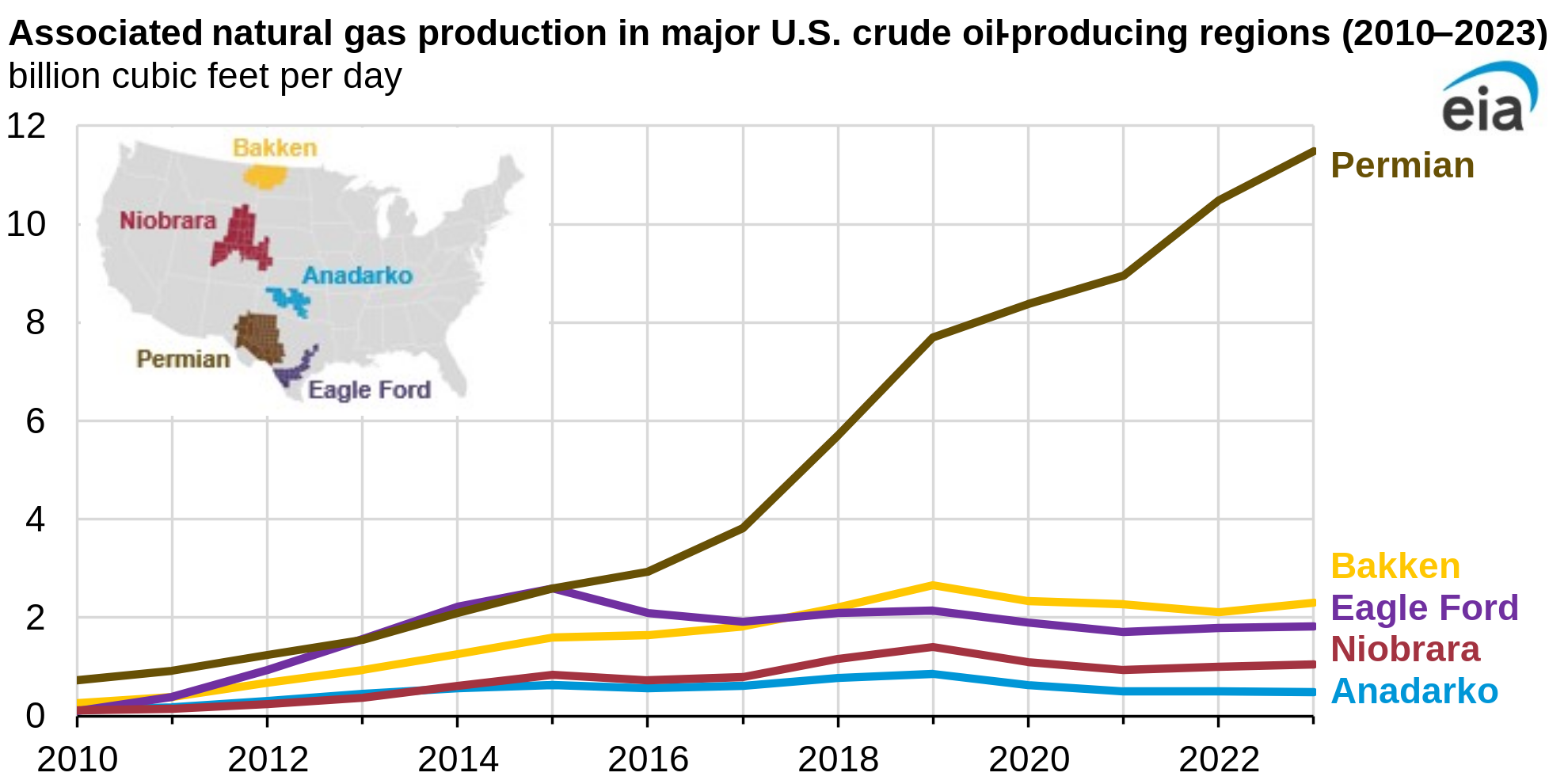

The EIA reports an 8% increase in 2023 US associated gas production as crude oil production rose to record levels. The Permian Basin, the dominant US crude oil producer, is unsurprisingly the leading associated gas producer.

EIA’s analysis inexplicably ignores the Gulf of Mexico OCS. The Gulf produced an average of 1.64 bcf/d of casinghead (associated) gas in 2023, ranking the GoM just behind the Eagle Ford and significantly above the Niobrara and Anadarko regions (see chart above). It’s also noteworthy that most production from the regions on the EIA chart is from private land, and is not constrained by 5 year leasing plans and other restrictive Federal policies.

80% of GoM gas production is from deepwater leases. The % of associated gas produced on deepwater leases is even higher. The 2 leading GoM gas producers, Shell and bp, only operate deepwater leases. The % of their 2023 gas production that was associated gas was 93% for Shell and 100% for bp.

Exxon CEO Darren Woods’ is concerned that US withdrawal from the Paris climate agreement would threaten carbon capture and sequestration (CCS), the foundation for which is government mandates and generous taxpayer subsidies.

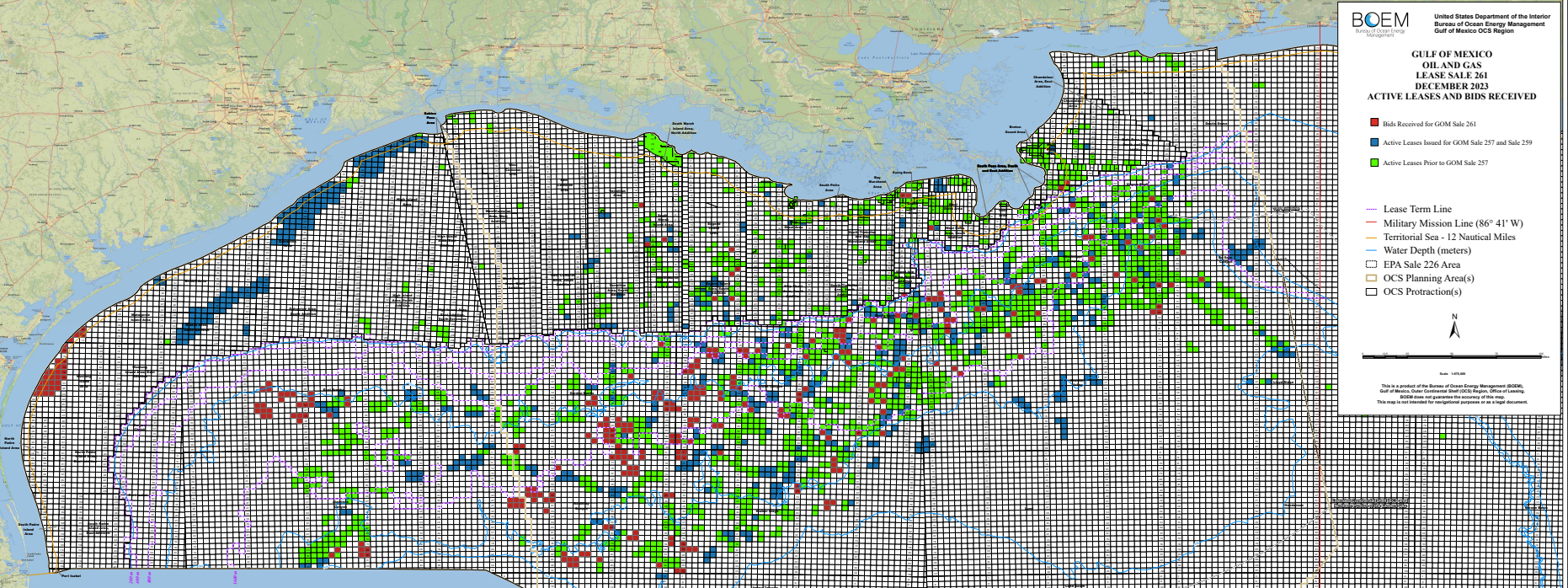

Exxon sought an edge over CCS competitors by improperly acquiring 163 OCS oil and gas leases (map below) for carbon disposal purposes. Conversion of these leases is not authorized, which means they will expire at the end of their primary (5 year) term absent legislative or regulatory action.

The only solid support for CCS is from companies hoping to benefit from subsidies and charges to industries and individual energy consumers. It’s time to end the Federal government’s CCS programs.

199 oil and gas leases were wrongfully acquired at Sales 257, 259, and 261 with the intent of developing these leases for carbon disposal purposes. Repsol was the sole bidder at Sale 261 for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

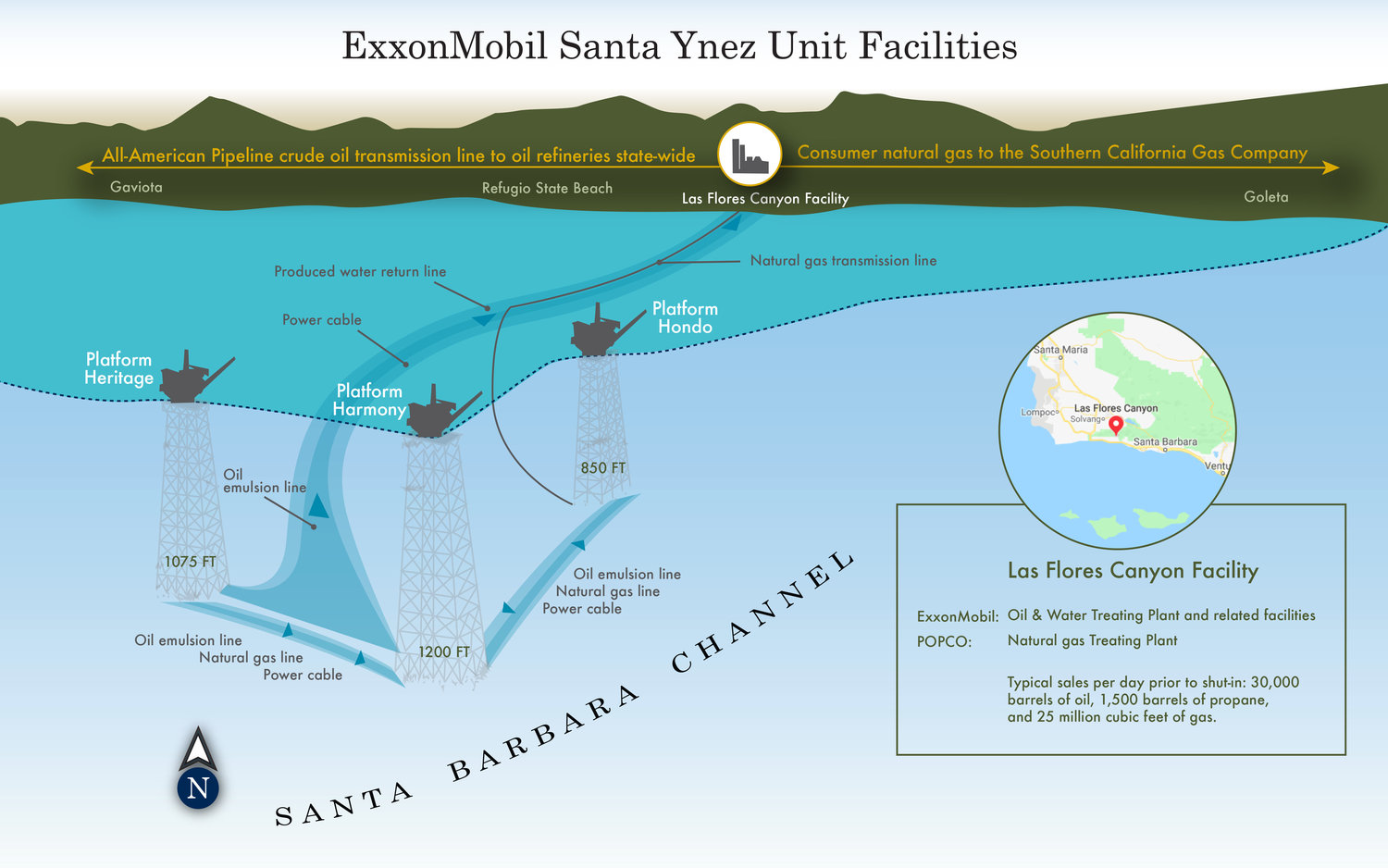

The Santa Barbara County Planning Commission has approved the transfer of the onshore pipeline from Exxon to Sable Offshore. Although the Environmental Defense Center (EDC) is appealing that decision to the Board of Supervisors, the Board’s vote will likely be a 2-2 tie. Supervisor Hartmann’s property is close to the pipeline and she has recused herself from votes on the matter. A 2-2 vote would be a win for Sable, because a tie vote means the planning commission decision stands.

As an investment, Sable is a “pure California permitting play,” which means the risks are high. The company’s chances for success are almost entirely dependent on receiving the necessary approvals from State and local agencies.

Sable’s share price soared to $23.43 on 9/3 after the company reached agreement with Santa Barbara on the installation of required pipeline valves. The price bounced further to $28.30 on 9/19 before falling sharply to $19.43 on 10/9 after being cited for failing to get California Coastal Commission approval to install the required valves. The price rebounded to $24 following the County Planning Commission’s approval of the transfer from Exxon to Sable before settling at $23 on Friday, the date of the EDC appeal.

Expect the financial and psychological roller coaster ride to continue.

“On Sept. 16, 2024, a routine helicopter approach at an offshore facility nearly resulted in a serious accident due to a failure to follow proper helideck procedures. Before landing, the helicopter pilot visually confirmed that a nearby crane was securely stowed and stationary (Figure 1). However, as the helicopter neared the helideck, the crane operator unexpectedly raised the crane boom, bringing it alarmingly close to the landing area as the helicopter was 10 feet from touchdown. The pilots swiftly executed a go-around maneuver, successfully avoiding a collision and ensuring the safety of the crew and passengers onboard.”

The new program will include at least one Gulf of Mexico lease sale annually.

Where there is State support (e.g. Alaska), other offshore areas may be added to the program.

Reversal of the Beaufort Sea Presidential withdrawals, either by executive order or, if necessary, by congressional action, is a distinct possibility.

A Gulf of Mexico oil and gas sale will be held during the first half of 2025. This can be accomplished under the Biden administration’s 5 year plan.

Judge Boardman’s ruling requiring a new biological opinion under the Endangered Species Act (ESA) has created some uncertainty regarding the timing of a GoM sale. Her decision is being litigated and the effective date of her ruling is now 5/21/2024 (see attached). Congressional action could also reverse this decision.

Expect other litigation on NEPA and ESA grounds with the intent of stalling oil and gas leasing. Congressional action could reverse or limit such litigation.

Offshore wind:

Expect offshore wind leasing to be “paused.”

Current leaseholders are contractually entitled to continue developing and operating their leases. Expect construction and operation plans to be more closely scrutinized.

Expect BSEE’s report on the Vineyard Wind turbine blade failure to receive added attention and publicity.

Expect considerable tension between North Atlantic governors, strong supporters of offshore wind, and the new administration.