While the majors and large independents garner most of the attention, smaller companies are an integral part of the mosaic that is the Gulf of America petroleum province. Some focus on producing and identifying remaining reserves on the shelf; others partner in deepwater projects.

Sale participants like Arena, Cantium, Walter, W&T, Beacon, Kosmos, and Houston Energy are well established Gulf leaseholders. Red Willow has attracted attention as a successful Southern Ute energy corporation.

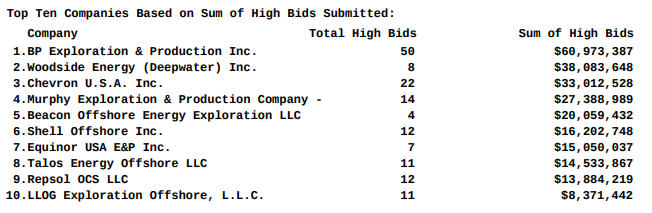

Which majors will be the most active bidders? BP (50 high bids), Chevron (22), and Shell (12)

Will former Gulf of Mexico stalwarts Exxon and Conoco Phillips participate for the first time in years? They did not.

How many companies will submit bids? Would like that to be a number >35. Only 30 companies participated.

How many tracts will receive bids? A number >300 would be very encouraging. Only 181 tracts received bids.

Will the total high bids exceed $400 million? No, the total was $279.4 million.

Will we see an increase in shelf interest? Shelf bidding continued to be limited (map). Renaissance, Byron, Arena, GOM Shelf LLC, Walter, W&T, Cantium, and WYOTEX Offshore submitted bids for shelf leases.

Which independents will be the most active? Woodside and Murphy are large independents, and their participation was most impressive. Murphy submitted 14 high bids totaling $27.4 million. Woodside had 8 high bids including the sale’s two highest for a total of $38.1 million, second only to BP in terms of the sum of their high bids.

The sale was beautifully conducted by BOEM, and Leslie Beyer – Assistant Secretary for Land and Minerals Management, Dept of the Interior – and Matt Giacona, Acting BOEM Director, delivered strong messages in support of the OCS oil and gas program.

However, as a colleague commented just after the sale, it was beautiful but not big. He and I expected more given the time since the last sale and the attractive terms.

Below is a comparison with the previous 3 Gulf sales. More to follow.

Sale No.

257

259

261

BBG1

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

companies participating

33

32

26

30

total bids

2233

2842

3161

219

tracts receiving bids

2143

2442

2751

181

sum of all bids $millions

198.5

309.8

441.9

371.9

sum of high bids ($millions)

101.7

263.8

382.2

279.4

highest bid company block

$10,001,252.00 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

$18,592,086 Chevron KC 25

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

50 bp 61.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

61.0 bp

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

14-Murphy

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

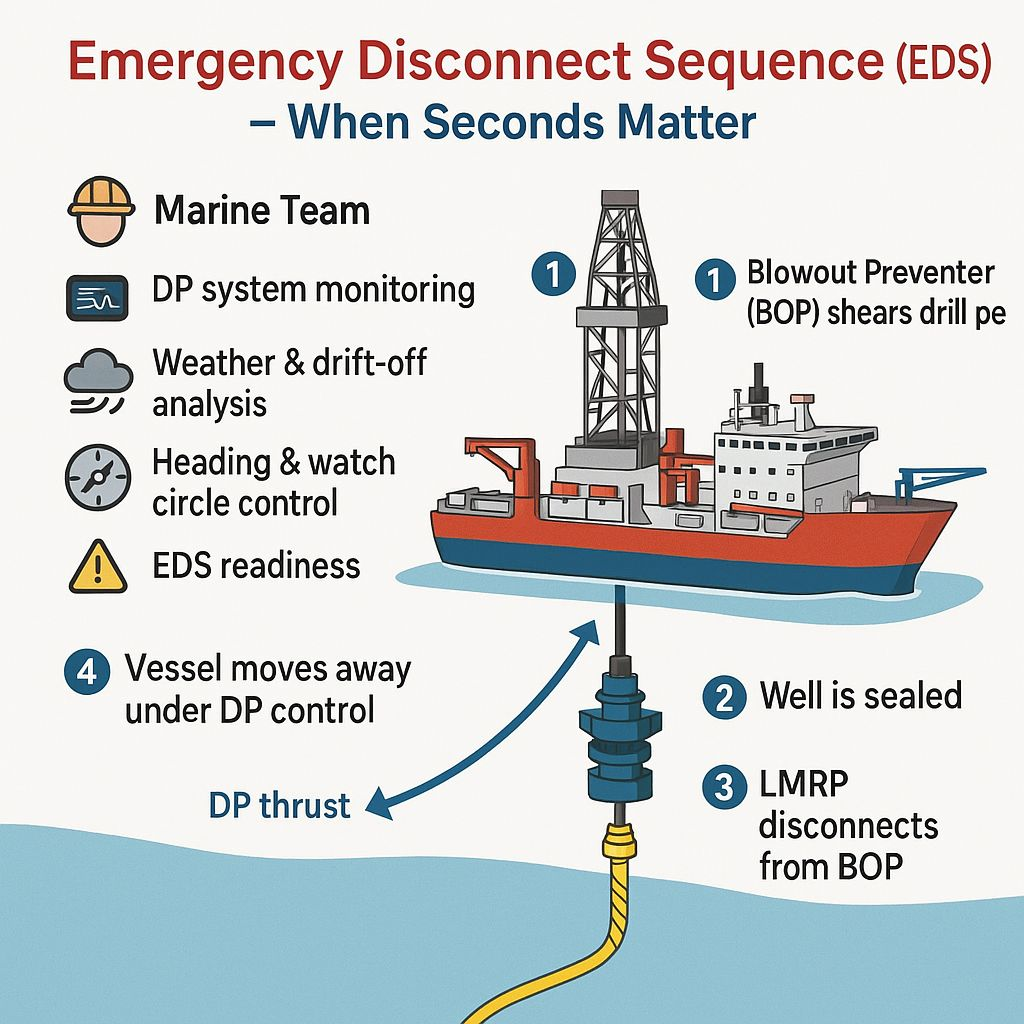

Seconds matter – training, equipment maintenance, and effective leadership are critical!

Several BSEE Safety Alerts have just been released. Of particular importance to those interested in deepwater drilling is the attached alert describing two separate Emergency Disconnect Sequence (EDS) incidents.

The EDS (see the diagram above) is a critically important safety protocol that ensures that a well is sealed and the riser and rig are disconnected from the blowout preventer in the event of a well control emergency, unforeseen weather/ocean conditions, loss of power, or positioning system malfunction. Note that the Macondo blowout could have been prevented if the Deepwater Horizon crew had activated the EDS in a timely manner.

The two EDS events cited in the Safety Alert were presumably the March 28, 2025 and March 5, 2024 incidents investigated by BSEE district offices. The drillships were the Stanley Lafosse and the Deepwater Poseidon The investigation reports provide detailed information on these incidents.

Unintended riser disconnects not associated with EDS activations are a related safety and pollution concern that necessitated the issuance of a 2000 Notices to Lessees that was subsequently updated:

BOEM informs (post below) that Wednesday’s BBG1 oil and gas lease sale will be streamed live here at 10 AM ET. Given that this is the first sale in two years and the first BBG sale, some dignitaries may be in attendance.

On December 10, we will host the Big Beautiful Gulf 1 oil and gas lease sale, our first under the One Big Beautiful Bill Act.

Location: In the Ionian Sea 30 km west of Corfu Island (note: that’s 18.6 miles, not the 125 mile buffer that Florida views as sacred)

Water depth: 500 to 1,500 m

Block size: 2,422.1 sq Km, the largest unexplored offshore structure in the Mediterranean (note: Gulf of America leases are only 23.3 sq km or < 1% as large)

First drilling: late 2026 or early 2027. This will be the first exploratory offshore drilling in Greece since 1981!

Energean’s participation is set at 30%, down from 75%.

Helleniq participation is now 10%, down from 25%.

Energean will remain the operator during the exploration stage.

In the event of a commercial discovery, Exxon will assume the operatorship during the development phase.

Andreas Shiamishis, CEO of HELLENiQ ENERGY: “Greece is emerging as one of Europe’s newest and promising regions for hydrocarbon exploration and development. This transaction represents a positive step not only for the joint venture partners, but also for the Greek economy.”

Will the oil and gas lease sale boldly named Big Beautiful Gulf 1 (BBG1) live up to its grand name? Given the more favorable lease terms and the 2 year gap since the last sale, BBG1 should surpass the previous 3 sales (table below). Questions:

Which majors will be the most active bidders? Chevron? Shell? BP? Oxy/Anadarko?

Will former Gulf of Mexico stalwarts Exxon and Conoco Phillips participate for the first time in years? Probably not, but US super-majors should participate in the US offshore program.

How many companies will submit bids? Would like that to be a number >35.

How many tracts will receive bids? A number >300 would be very encouraging.

Will the total high bids exceed $400 million?

Will we see an increase in shelf interest?

Which independents will be the most active?

After the not-so-clever carbon disposal acquisitions in the last 3 sales, will the number of carbon disposal bids be zero? For the first time ever, the Federal government felt compelled to stipulate the obvious (see the proposed notice for OCS Sale 262) – that an Oil and Gas Lease Sale is only for oil and gas exploration and development.

See the summary data below for the last 3 Gulf lease sales. We’ll fill in the blanks next week.

Sale No.

257

259

261

BBG1

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

companies participating

33

32

26

total bids

2233

2842

3161

tracts receiving bids

2143

2442

2751

sum of all bids $millions

198.5

309.8

441.9

sum of high bids ($millions)

101.7

263.8

382.2

highest bid company block

$10,001,252.00 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

“Natural gas and LNG are fast becoming the gravitational center of the global energy system, but some energy experts said the world is only beginning to grasp the scale of what’s to come.” ~Natural Gas Intelligence

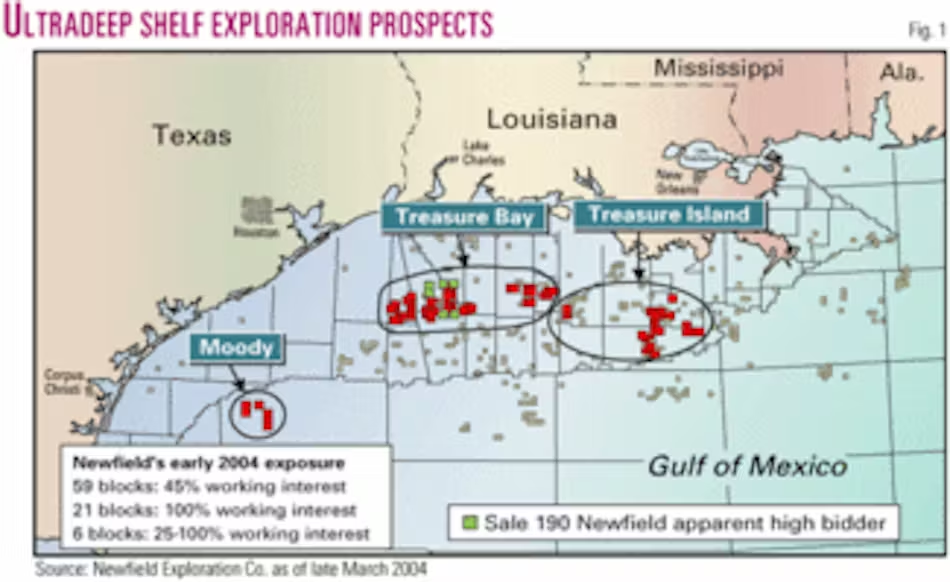

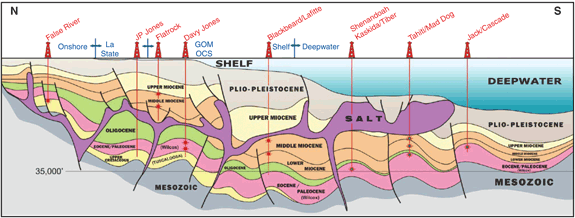

Demand and high well producibility are stimulating exploration in the high pressure, high temperature Western Haynesville (Texas) and other ultradeep onshore gas prospects. Is it time to revisit ultradeep gas on the Gulf of America shelf? See the above targets map from 2004.

20 years ago Newfield, Exxon, and McMoRan drilled pioneering ultradeep wells targeting gas-prone reservoirs below salt welds in Miocene and older formations (diagrams below). The water depths were <100 feet but well depths exceeding 30,000 feet, and high temperatures and pressures, pushed the limits of drilling technology at the time. Noteworthy wells:

Blackbeard West (Exxon): Spudded in early 2005 in 70 feet of water in South Timbalier Block 168. The target was gas in Miocene sands at 27,000-32,000 feet total depth. Drilling reached 30,067 feet by 2006, but was prudently suspended due to extreme pressures, temperatures (up to 600°F), and technical challenges with equipment.

Blackbeard West, part 2: In 2008, McMoRan re-entered the well with upgraded equipment and drilled to a record 32,997 feet below the mudline. They encountered hydrocarbon shows in multiple zones, including potential gas pay in Middle and Deep Miocene sands below 30,000 feet, validating the ultradeep concept.

Followup McMorRan wells:

Blackbeard East (2010-2011): Drilled to 33,400 feet in South Timbalier Block 144, logged potential hydrocarbons in Sparta and Vicksburg sands.

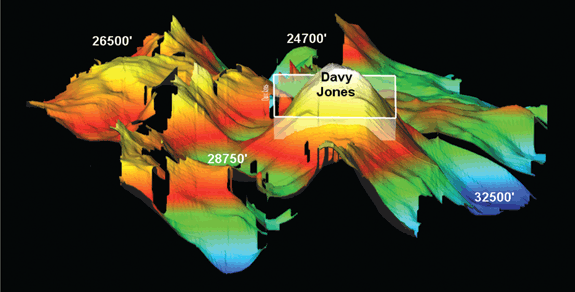

Davy Jones (2009-2010): South Marsh Island Block 230 in 20 feet of water; reached 29,122 feet; discovered gas in Wilcox sands, but faced flow-testing challenges.

Lafitte (2011): Eugene Island Block 223, found additional pay in ultradeep Miocene zones. These wells targeted gas reservoirs but encountered operational hurdles.

Also, note that a company targeting hydrocarbons below 25,000 feet (true vertical depth subsurface) may earn an additional 3 years on their lease. (See the Notice for next week’s lease sale.) Will improved technology and demand expectations finally open the ultradeep gas frontier?

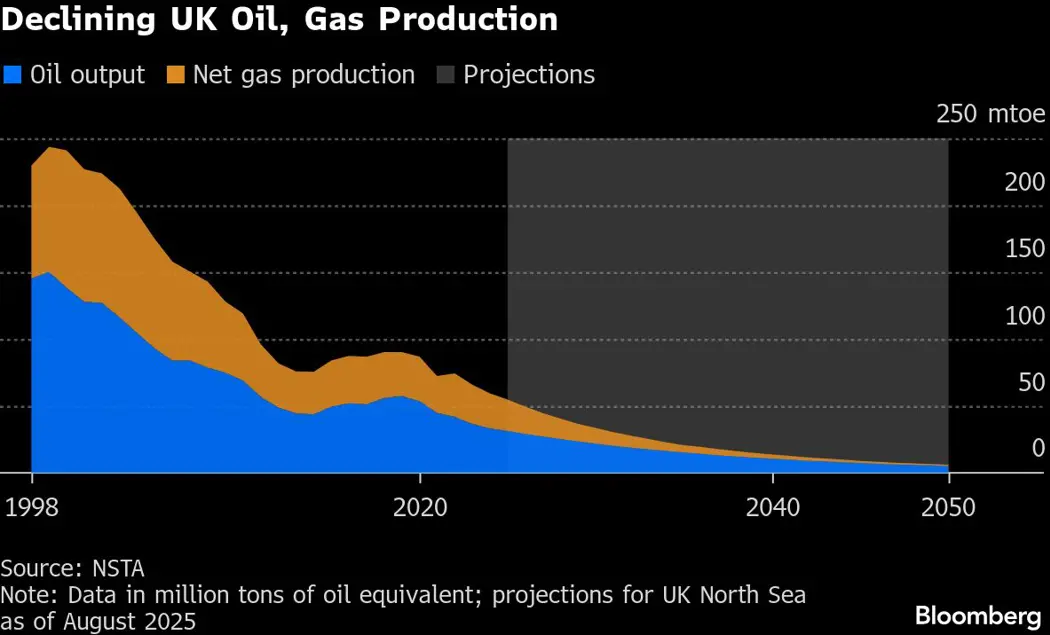

JL Daeschler, other North Sea veterans, and those of us who once admired the UK offshore program, lament the sad plight of their oil and gas industry and the destruction of the economy in northeast Scotland.

Incomprehensibly, the UK has retained the Energy Profits Levy, which requires North Sea operators to hand over 78% of their diminished profits to the Treasury. Most have regrettably chosen to do business elsewhere. Investment in the UK North Sea is at a record low and a study from Robert Gordon University says jobs are being “quietly” lost at a rate of 1,000 a month.

The UK government is grudgingly allowing some tieback production to existing facilities, but this will do little to stem the industry’s decline. JL notes that this limited infield development is not the type of new field investment needed to grow production and sustain the service industry (rigs, boats, helicopters, equipment, etc.).

“The term energy transition somehow sounds like it is a well-lubricated slide from one reality to another. In fact, it will be far more complex: Throughout history, energy transitions have been difficult, and this one is even more challenging than any previous shift.”

Related article in the WSJ: “Europe’s Green Energy Rush Slashed Emissions—and Crippled the Economy”

“European politicians pitched the continent’s green transition to voters as a win-win: Citizens would benefit from green jobs and cheap, abundant solar and wind energy alongside a sharp reduction in carbon emissions. Nearly two decades on, the promise has largely proved costly for consumers and damaging for the economy.”

“Europe largely took an “or” strategy: It raced to replace fossil fuels with solar, wind and biomass by taxing carbon heavily, subsidizing renewables and closing scores of fossil-fuel power plants. Britain, which pioneered the use of coal for energy, last year became the first large industrialized country to shut all of its coal-fired power plants. It has also banned new offshore oil-and-gas drilling. Denmark plans to eliminate gas for home heating by 2035. Around one-fifth of Germany’s municipal utilities plan to shut down their gas networks in coming years, according to an October survey by the utilities’ trade association.”