Putin suggests that people consider who had an interest in sabotaging the pipelines and who had the capability. He also asks why Germany isn’t allowing gas to flow through the one Nord Stream line that wasn’t damaged.

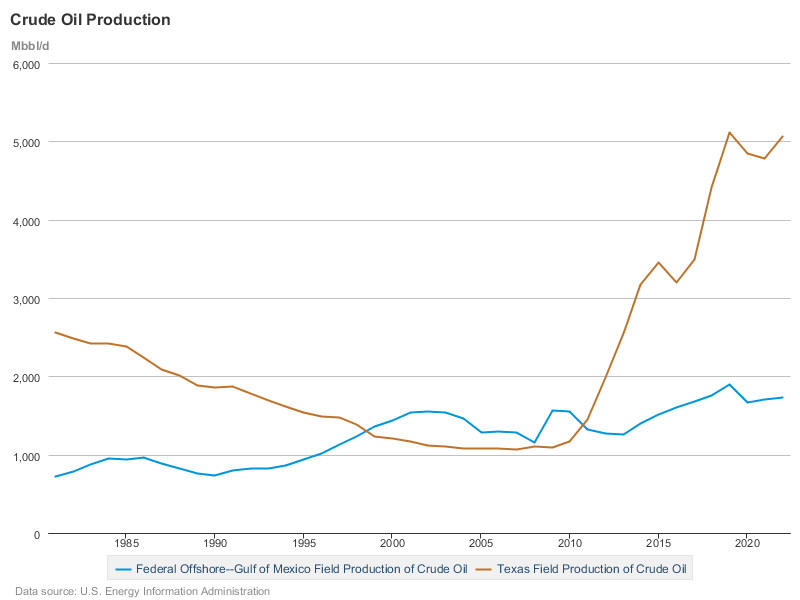

A friend owns land in the Texas Permian. His family gets a nice royalty check every month that has helped them get through some difficult times. Texas Permian production is almost entirely from private land, which is a big part of the success story. Payments to private land owners by responsible producers engender public support, access to resources, and growth in production. Add to that the continuous improvements in horizontal drilling, well stimulation and completion practices, and you have the success story that is the Texas Permian.

Similarly, private and state land plus technology launched the natural gas boom in my native state of Pennsylvania. When I was a student, we looked back at the Titusville/Colonel Drake glory days, and no one dreamed that the state would become a major natural gas exporter. Today, pipeline constraints, particularly in NJ and NY (which has managed to prevent access to the state’s substantial Marcellus and Utica shale resources) are preventing PA from further increasing gas sales.

The offshore lands on the US Outer Continental Shelf are a different story. Unfriendly, bordering on hostile, leasing policy (and not just during the current administration) has been partially overcome by advances in deepwater well and facility design that have lowered costs and increased productivity. However, OCS oil production is a fraction of what it could be.

OCS gas production has fallen dramatically since the turn of the century. Ultradeep (subsurface) gas production was not economically viable and production was fading even before onshore shale gas began to dominate US gas markets. Most of the current OCS gas production is associated with deepwater oil production.

Less attention has been given to natural gas’s other important air quality advantages – low NOx. SO2, and particulate emissions. These emissions have greater local significance from a human health standpoint. Those who have ridden a bike behind a natural gas powered bus have no doubt experienced the natural gas advantage firsthand.

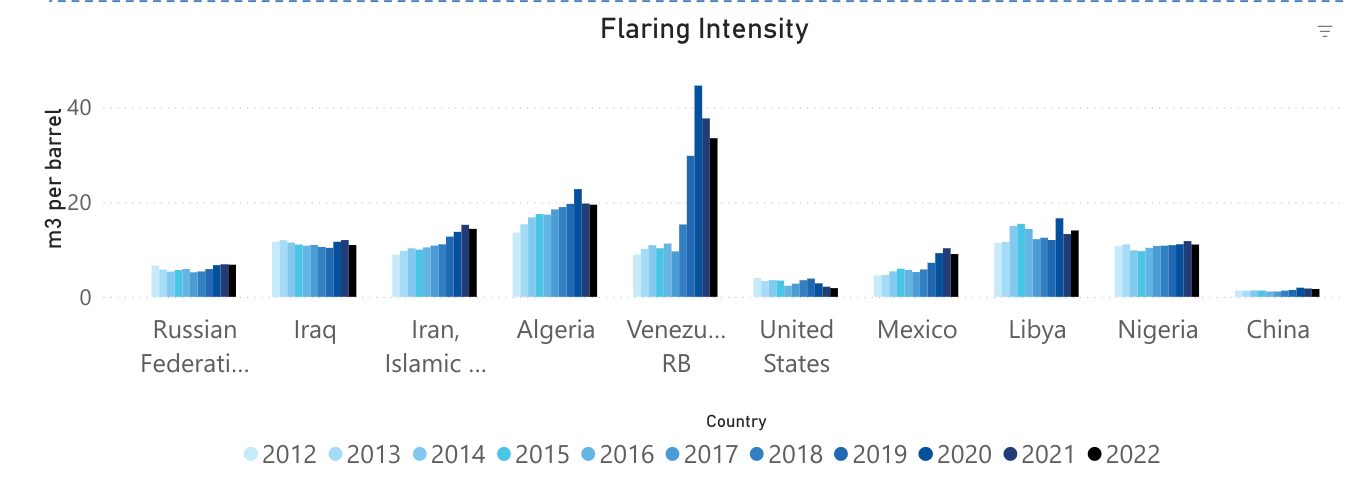

The latest World Bank data tell us that significant gas flaring issues persist. Worldwide, 138,549 million m3 of gas were flared in 2022. This equates to a massive 4 tcf, the equivalent of the reserves in a major gas field and more than 5 times the total gas production in the Gulf of Mexico in 2022.

The top ten “flarers” are listed below. Each of these fields flared from 19 to 42 bcf. For comparison, the top ten GoM gas producers in 2022 produced 10 to 57 bcf, so single fields are flaring more than GoM companies are producing in total. Assuming for discussion purposes a gas-oil ratio of 1000 cu ft/bbl, all of the gas associated with 19 million to 42 million barrels of oil production was wasted from each field.

Posted below are the World Bank’s flaring intensity data (m3 of gas flared per bbl of oil produced) for the 10 countries with the highest flaring volumes. Venezuela’s flaring intensity rose to 44.6 m3/bbl in 2020, before declining moderately the following 2 years. 44.6 m3/bbl equates to 1575 cu ft/bbl. This gas flaring to oil production ratio implies that a very high percentage of Venezuela’s associated gas production was flared.

Here in North America, we have flaring issues of our own. Mexico’s Cactus Field is a top ten flarer (first table above) with 534.5 million m3 flared in 2022. The World Bank also lists 6 Permian Basin fields with >50 million m3 of gas flared in 2022.

Zeroing in on the US/Canada offshore sectors, fields with >1 million m3 of gas flared (2022) are listed below. Four of the top 7 are offshore Alaska and Newfoundland where the gas cannot currently be marketed and reinjection, field use, and flaring are the only options. Can production from these fields be better managed to reduce flaring volumes?

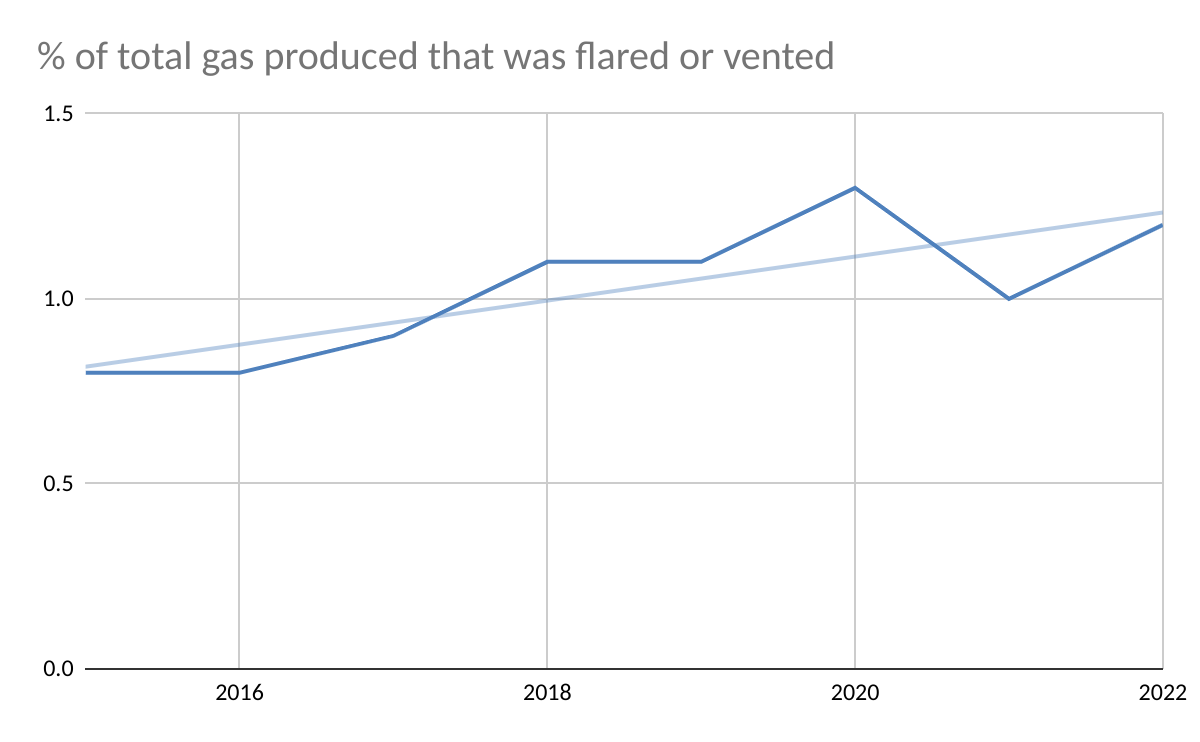

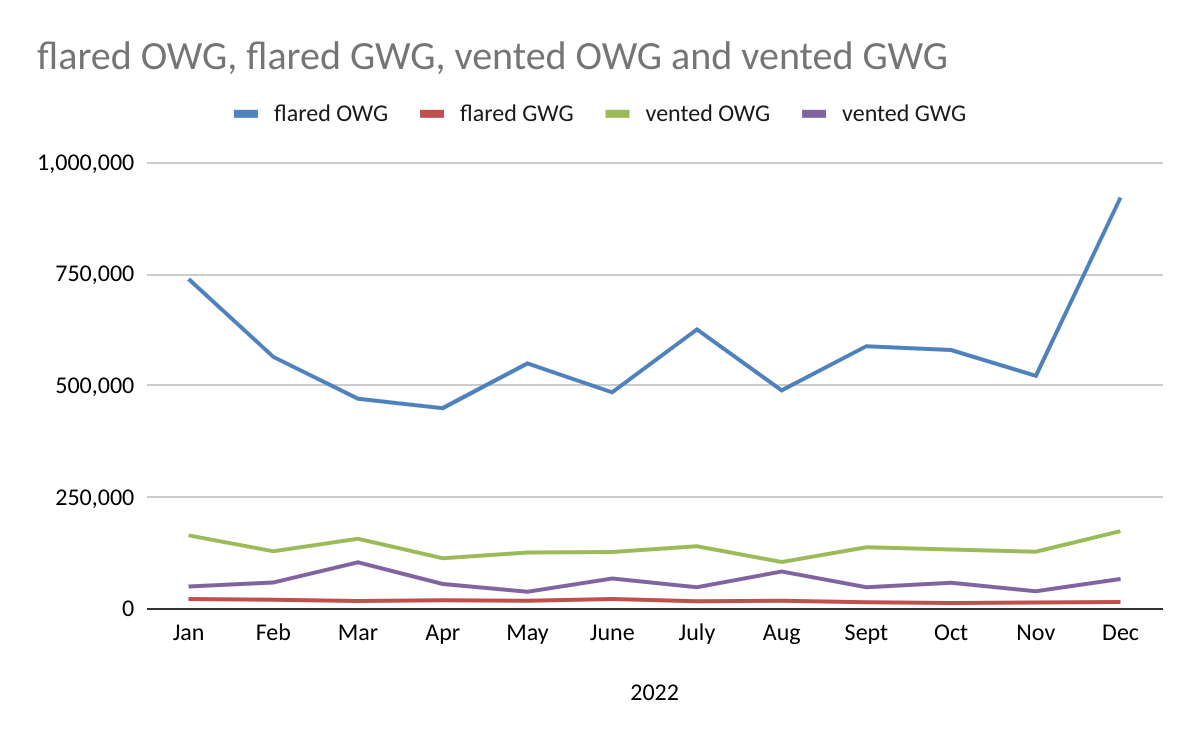

A very large increase in OWG flaring in December skewed the 2022 data (921 million cu ft vs 522 million in November, see 2nd chart below). OWG vented and gas-well gas (GWG) vented also spiked in December (third chart). Were these spikes associated with production startups, major compressor issues, administrative/accounting corrections, or other issues?

Although total venting increased by 407 million cu ft (21%) in 2023 vs. 2022, the overall venting trend is still favorable (last chart).

Kudos to ONRR for posting the flaring/venting data.

More regulator/industry transparency on flaring episodes is needed, particularly in light of the PNAS paper and the June 2022 Inspector General Report.

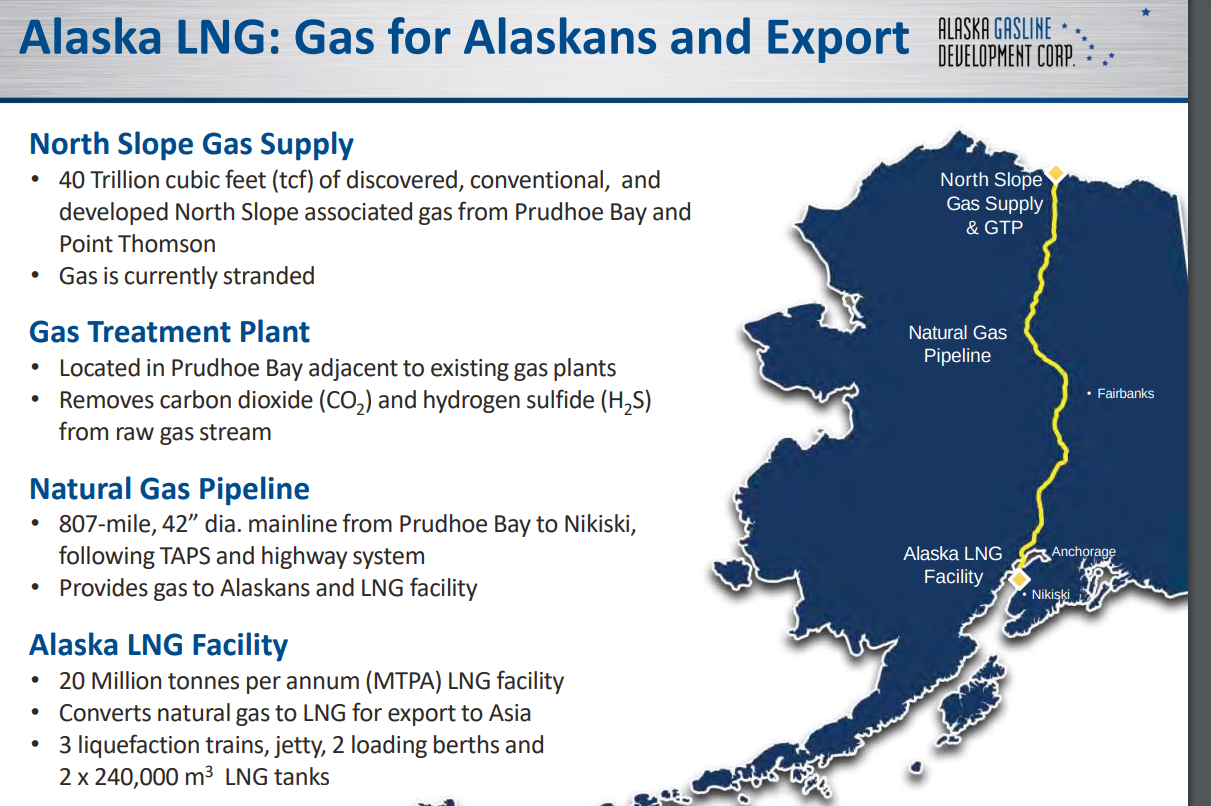

The Department of Energy approved Alaska Gasline Development Corp’s (AGDC) exports of LNG from the project to countries with which the United States does not have a free trade agreement.

Backers of the roughly $39 billion project hope it will be operational by 2030 if it gets investments and all required permits. The LNG would be exported mainly to countries in Asia.

Yesterday, Lars Herbst attended the EIA’s Annual Energy Outlook presentation. The slides are attached.

Below is a custom chart from the EIA data tables. While EIA predicts growth in renewable generating capacity, US oil and gas production are nonetheless projected to increase slightly through 2050.

Victoria Nuland’s glee over the Nord Stream damage (video clip below) is particularly galling to those responsible for offshore production, worker safety, and environmental protection. Does she realize that the Gulf of Mexico has more than 13,000 miles of active offshore pipeline that could be similarly targeted, and that the US has 2.6 million miles of onshore pipelines?

Whether or not the US was involved in the Nord Stream sabotage, Ms. Nuland’s schadenfreude is disturbing given the economic and security implications of the attack.

Offshore gas has important environmental advantages, particularly nonassociated gas-well gas (GWG). While the GoM production chart (below) is not pretty, there are signs that gas production may have bottomed and is slowly rising. This is largely due to growth in oil-well gas (OWG) associated with deepwater oil production.

A successful offshore program requires a mix of strategies, and it is encouraging that companies are still pursuing natural gas on the GoM shelf. The second chart (below), based on BOEM data, shows 2022 YTD (probably through Oct.) GWG production for the 11 companies that (1) produced more GWG than OWG and (2) produced more than 1 BCF of GWG.

Interestingly, 100% of the gas produced by Contango, Samchully, and Helis in 2022 was from gas wells. Contrast this with bp, the third largest GoM gas producer. None of bp’s gas production was from gas wells.

Tennessee Twist:TC Energy’s $29.3 million investment in a RNG (renewable natural gas) production facility near the Jack Daniel’s Distillery will see the Canadian operator producing RNG with a carbon-intensity score that is 50% lower than traditional natural gas, saving up to 16,000 tonnes of CO2e per year, according to the company.

“This investment is our first in the production of renewable natural gas,” said Corey Hessen, TC Energy executive vice president and president, power & Energy solutions. “The production of RNG onsite at the Jack Daniel’s Distillery offers TC Energy one more opportunity to meet the challenge of growing energy needs and reducing emissions while providing customers with access to an affordable, reliable, source of energy.”