Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectivelychallenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

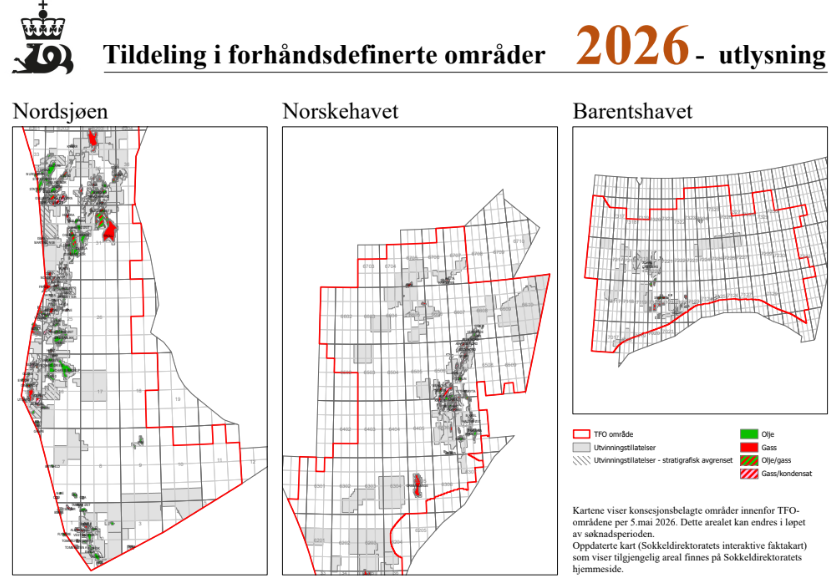

The oil and gas industry is crucial for Norway and for Europe. The government is today announcing new exploration areas in the APA (Allocations in Predefined Areas) to further develop the petroleum sector, so that it can continue to create great value for the community, lay the foundation for good jobs throughout the country, ensure our common welfare and contribute to Europe’s energy security and safety, says Prime Minister Jonas Gahr Støre.

Kudos to Norway for the strong, unequivocal announcement. Consistent acreage offerings are important in sustaining offshore production:

Allocations in Predefined Areas (APA) are an annual licensing round that covers the best-known exploration areas on the continental shelf. Through the APA scheme, oil companies gain predictability regarding access to exploration acreage, which is important for a long-term industry such as the petroleum industry. After more than 50 years of exploration activity, the APA scheme today covers the majority of the area that is opened and available on the Norwegian continental shelf.

New York City Comptroller Mark Levine has urged ExxonMobil shareholders to reject the proposal to move their corporate headquarters to Texas, which he claims has “less robust” shareholder rights. Apparently, he would rather that XOM remain in a State where they can more easily be targeted for frivolous law suits.

James Copland, Senior Fellow and Director of Legal Policy at the Manhattan Institute : “rather than focus on improving New York City’s business climate, the comptroller is more interested in opposing ExxonMobil’s proposed redomiciling from New Jersey to Texas, solidifying its operations in a less hostile business environment.”

Mr. Levine’s chutzpah is indeed impressive, even by NYC standards, but shareholders will not vote against their own financial interest.

ExxonMobil’s move means that the three feature pieces of John D. Rockefeller’s Standard Oil legacy will now be domiciled in Texas – Standard Oil of New Jersey (Exxon), Standard Oil of New York (Mobil), and Standard Oil of California (Chevron).

California Attorney General Bonta asks the Court to stay Energy Secretary Wright’s Order directing Sable, under the Defense Production Act to restart production and preliminarily enjoin Defendants, and all those acting in concert with Defendants (i.e. Sable), from enforcing or relying on it. See the attached Federal Court filing.

The AG’s irreparable harm and public interest arguments seem particularly weak, and this may not be the best time to attempt to halt a 20+% increase in California oil production.

Requesting a 60 day extension (double the comment period specified by BOEM)

Need more time to:

review the detailed proposed changes

conduct studies to inform agency

analyze the studies and data

consider alternatives

organize, complete, and review the findings of subject matter workgroups

In API’s favor:

Agencies have discretion on extending comment periods.

60 days is typically considered the minimum comment period; 90 days would have been more appropriate for this proposal.

API members are clearly affected parties.

The BOEM proposal relaxes financial assurance requirements for smaller companies while increasing predecessor lessee risk exposure. Those predecessors would typically be API members.

There are divisions within the industry which complicate trade association commenting.

On the other hand:

API’s letter is dated May 1, just one week prior to the end of the comment period.

The letter was not posted at Regulations.gov until May 6, 2 days before the end of the comment period. Only those tracking the comment letters would have been aware of the request even at this late date.

As of early this morning (May 7th), the docket still specifies a May 8 due date for comments.

An extension could be viewed as inequitable to other concerned parties who made special efforts to honor the deadline.

Comments:

This is why it’s best to specify a reasonable comment period at the time the regulation is proposed, and make it clear that there will be no extension. That way, everyone is treated the same.

For this proposal, 90 days would have been reasonable.

Given the number of significant issues that need to be addressed, the best outcome for this rule would be a re-proposal. See the comments submitted by John Smith and me.

Attached are my comments on BOEM’s proposed revisions to the decommissioning financial assurance regulations. These comments were submitted to Regulations.gov yesterday (3 days early 😀). Bud

Concluding Remarks

MMA’s highest priority must be assuring that facilities are safely decommissioned without public funding. Supplemental financial assurance determinations and lease assignment approvals must be consistent with that priority.

Predecessor liability is an important financial assurance principle, but legal boundaries and administrative procedures must be clearly established.

Safety and compliance are inextricably related to financial performance, and must be considered in determining supplemental assurance requirements.

Using reserve estimates to reduce supplemental assurance exposes taxpayers to geologic and accounting risks.

Unacceptable public risks have resulted from financial assurance decisions intended to advance offshore wind development.

The transition reflects more than a decade of operational experience managing offshore resources. By consolidating the planning, permitting, inspection, and enforcement responsibilities currently divided between BOEM and BSEE, the Department aims to:

Improve coordination and consistency

Reduce duplication of efforts

Strengthen oversight and environmental safeguards

Modernize organizational structure

All current regulatory responsibilities and protections will remain in place throughout the transition. There will be no disruption to permitting, environmental reviews, or enforcement activities.

What to Expect

Phased Transition: Internal alignment activities begin soon.

No Regulatory Rollbacks: Existing requirements remain in full effect.

New Website and Branding: The Marine Minerals Administration’s full digital presence will launch in the coming months.

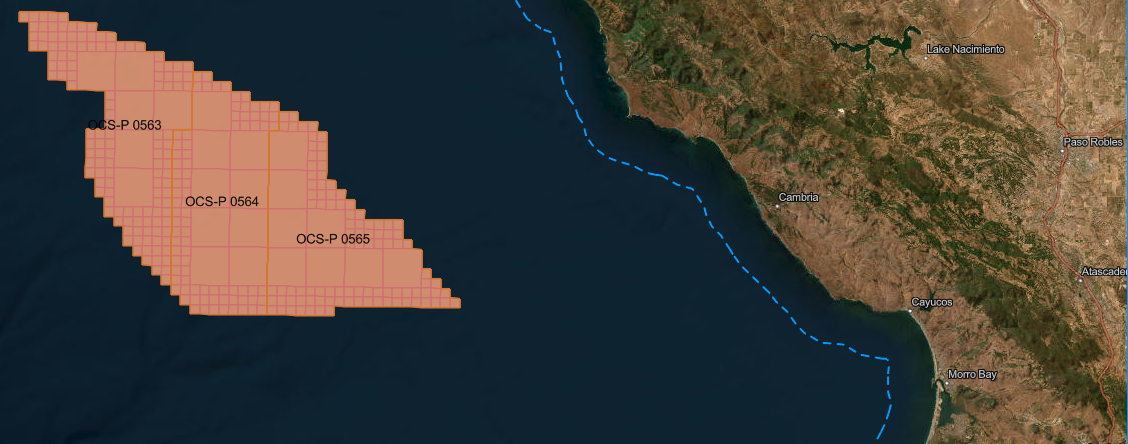

Bluepoint Wind Lease 0537 owned by Global Infrastructure Partners, a part of BlackRock, and Ocean Wind (Engie, France and EDP Renewables, Portugal)Golden State Wind Lease 0564 owned by Ocean Wind (Engie, France and EDP Renewables, Portugal) and the Canada Pension Plan Investment Board

These are mutually beneficial “Win-Win” agreements. Bluepoint and Golden State benefit by escaping bad business decisions:

Bluepoint massively overpaid ($765 million) for Atlantic lease 0537 during the brief irrational exuberance era of the offshore wind program. The intense bidding was driven by the lure of subsidies, guaranteed power sales, unprecedented Federal and State promotion, peak climate activism, inattention to mounting public opposition, and irrational expectations regarding the role of offshore wind in powering the economy.

The value of Atlantic wind leases declined by 99.4% between 2022 and 2024, and this was before the Presidential election!

Golden State bid $150 million for a wind lease that will require floating turbines. The 50 MW Kincardine Offshore Windfarm, which is billed as the “world’s largest floating wind farm,” experienced a £30 million loss in 2023 following a £18 million loss in 2022. Another floating wind project, Hywind Scotland, had to be taken offline for 4 months for maintenance after less than 6 years of operation. BOEM was forced to “postpone” the Oregon wind sale given the absence of bidders.

Significant work had not yet begun on either the Bluepoint or Golden State projects.

Many in Morro Bay and elsewhere along the Central Coast of California are not pleased with the attempt to “industrialize the coast.” Opposition to offshore wind projects is now well established along the Atlantic Coast.

The companies get to invest their inflated wind dollars in profitable energy projects without penalty. What prudent executive wouldn’t jump at the deal?

Waiting for the next Administration is not likely to improve the fundamental economics of offshore wind development, and increased subsidies are not popular.

A pro-wind govt would facilitate permitting, but is unlikely to buyback existing leases.

The Administration also benefits:

Two more wind leases are off the books.

Removing one of three leases could significantly affect the economics of Central Coast (CA) wind development.

Agreements were necessary because it’s difficult to cancel leases, and compensation would be required. If settled in court, the compensation could easily exceed the lease purchase price.

The companies agreed not to pursue any new offshore wind projects in the United States.

The rebates will be invested in projects favored by the Administration.

Question: Are the partners and parent companies also precluded from investing in offshore wind projects or just the Bluepoint Wind and Golden State Wind entities? If BlackRock, EDP, and Engie can no longer make such investments, that is a big deal. This is especially true given the agreement with Total, Vineyard Wind’s problems, Orsted’s financial challenges, BP and Shell’s apparent exit from the US offshore wind market, and Equinor’s reduced renewable energy ambitions.

Finally, a December 7, 2022 release by the Canada Pension Plan Investment Board heralding the 50% partnership in Golden State Wind might be of interest to our Canadian readers. That bad investment can now be removed from the books.

Restart seems likely for decommissioning financial assurance rule

Posted in Regulation, decommissioning, energy policy, tagged API, BOEM, Chevron, comments, decommissioning, financial assurance, NEFSA, proposed regulation, Shell on May 18, 2026| Leave a Comment »

Thankfully, from the standpoint of those of us whose primary concerns are the integrity of the OCS program and protecting taxpayers from decommissioning liabilities, the API comments (attached), along with those submitted by Shell and Chevron, have exposed the folly of eliminating financial assurance whenever there is a financially strong company somewhere in the lease chain of custody.

Mindful of ongoing and anticipated decommissioning liability battles, API effectively challenges the BOEM proposal on legal grounds. API also demonstrates why revisions intended to improve regulatory efficiency and increase production would do exactly the opposite. Excerpts from the API comments (emphasis added):

Further, foisting financial assurance obligations on predecessors will not achieve BOEM’s stated aims of financial “savings” and increased OCS oil and gas production; it more likely will do the opposite. The Proposed Rule would just shift financial assurance burdens to financially stronger predecessors, many of which remain engaged in the majority of leasing and production across the OCS and are far more likely to be future investors in increased OCS development and production. By contrast, nothing ensures that entities standing to benefit from the Proposed Rule will reinvest saved financial assurance premium dollars into OCS production; in fact, such entities largely do not explore or increase reserves, but merely buy pre-discovered reserves and produce them to a lower economic limit.

Nor would the Proposed Rule promote or save costs for future OCS transactions since, in the absence of any option for BOEM-demanded financial assurance from current interest holders, assignors will demand financial assurance at sufficiently conservative levels to address the risk of residual liability if assignees default on their obligations.

Even more problematically, the Proposed Rule would retroactively impose this new regulatory burden on entities that divested their OCS property interests years (or decades) earlier—in reliance on BOEM’s regulations that required their assignees to provide any supplemental financial assurance. Such entities are no longer in privity with BOEM, and have no control over current operations on those OCS properties. The Proposed Rule would reach back even to impose these obligations on predecessors that divested their interests before the 1997 regulatory imposition of joint and several liability for assignors (a time period on which the Proposed Rule is silent).

This novel and misguided approach allows, and even encourages, current interest holders to eschew their lease and grant obligations, and instead freely operate on the backs of predecessors and taxpayers. Meanwhile, current interest holders could choose to allocate little or no funding for end-of-life obligations like decommissioning whenever they desire to conclude production, file for bankruptcy, and leave BOEM to eventually issue decommissioning orders to predecessors that have not operated the grants and leases for years or even decades. This would create higher administrative and financial burdens for the government and system as a whole, including where no viable predecessor had accrued liability for decommissioning all facilities present on the lease or grant, and potential operational impacts that a predecessor has no obligation to cure.

This new proposed obligation on predecessors is arbitrary and capricious and unlawful on multiple grounds. It violates the rule against retroactivity by creating new federal liability stemming from already-completed transactions. It violates the agency change in position doctrine, particularly given that BOEM on multiple occasions has rejected precisely the same approach as in the Proposed Rule. It is unsupported, as it overstates the burdens under the discretionary Existing Rule, disregards repeated U.S. Government Accountability Office (“GAO”) and BOEM findings calling for more robust financial assurance by current interest holders, cites only anecdotal prior comments while ignoring the bulk of countervailing comments detailing reality on the OCS, and identifies no means by which BOEM can compel collect, and assess adequate financial information for all predecessor entities. And it is self contradictory, including by tying up more capital among entities producing the vast majority of oil and natural gas on the OCS.

Chevron points to their potential liability balance of ~ $2 billion for satisfying the decommissioning obligations of default owners:

John Smith and I do not agree with the industry support for the use of reserves as financial assurance. The margin of error in reserve, oil price, and decommissioning cost estimates, not to mention the potential for facility damage, the ever-changing political environment, and the administration challenges, present an unacceptably high risk for taxpayers. If companies want to guarantee decommissioning based on reserves, let them do so. Shell makes a good point about why it is especially important to prohibit the use of reserve estimates on a company-wide basis:

Lastly, kudos to the New England Fisherman’s Stewardship Association for raising the concern about financial assurance for decommissioning offshore wind facilities

Read Full Post »