“Today’s announcement delivers on Harbour’s long-standing ambition to establish a presence in the deepwater Gulf of America. With LLOG, we found the right combination of high-quality assets and a talented team, providing a strong strategic and cultural fit with our company. The transaction positions us as a leading player in a region with well-established infrastructure, a supportive fiscal and regulatory environment and opportunities for additional growth.”

LLOG was the 6th largest Gulf of America producer of both oil and gas in 2024 with production of 27 million bbls of oil and 34 BCF of gas. LLOG was the high bidder on 11 tracts in the recent BBG1 sale.

Harbour is not currently a Gulf of America leaseholder.

Reuters had reported that Shell was in advanced talks to acquire LLOG. Apparently, either Shell lost interest or Harbour made a more attractive offer.

🚨BREAKING: Sec. @DougBurgum announces he will PAUSE leases for ALL large-scale offshore Wind projects immediately.

"Today we're sending notifications to the five large offshore wind projects that are under construction, that their leases are being suspended due to national… pic.twitter.com/lFPyMscALr

This picture was posted on the “Rig Pigs” Facebook page by Huston Funk. Per Huston: “First crew photo from the Deepwater Horizon. Taken in the Indian Ocean after we had left Singapore.”

Commenters identified 3 Macondo victims in the photo: Jason Anderson, Don Clark, and Stephen Curtis 🙏

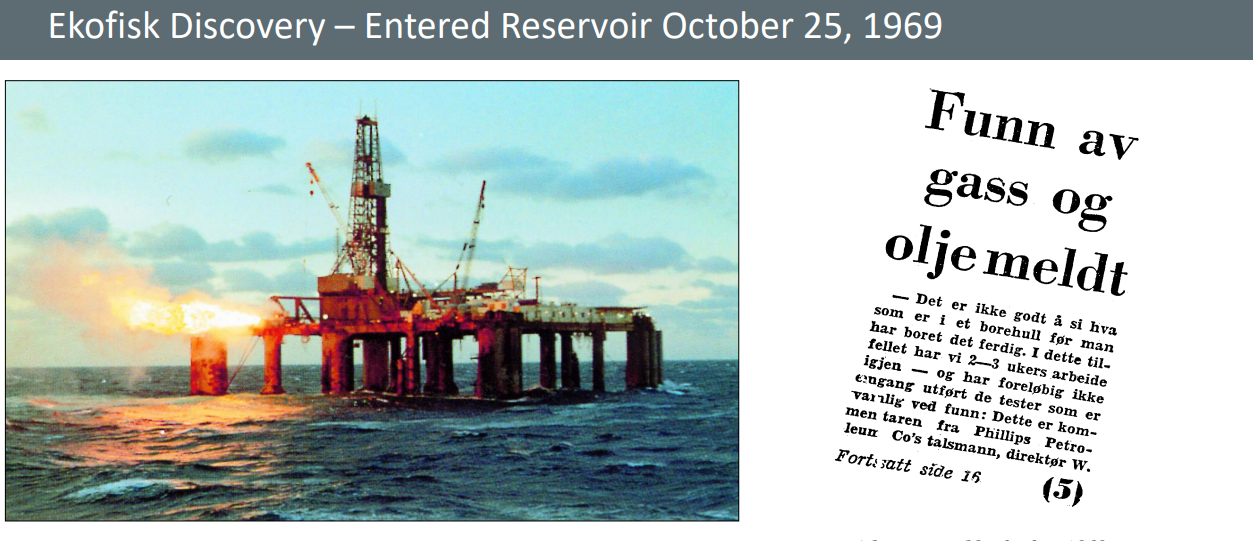

Ekofisk was Norway’s first commercial oil discovery in 1969, with first production in 1971. Another redevelopment phase could extend production to 2050 and beyond. This is a good example of how technology and reservoir management can extend field life indefinitely. Finite resources are not really finite.

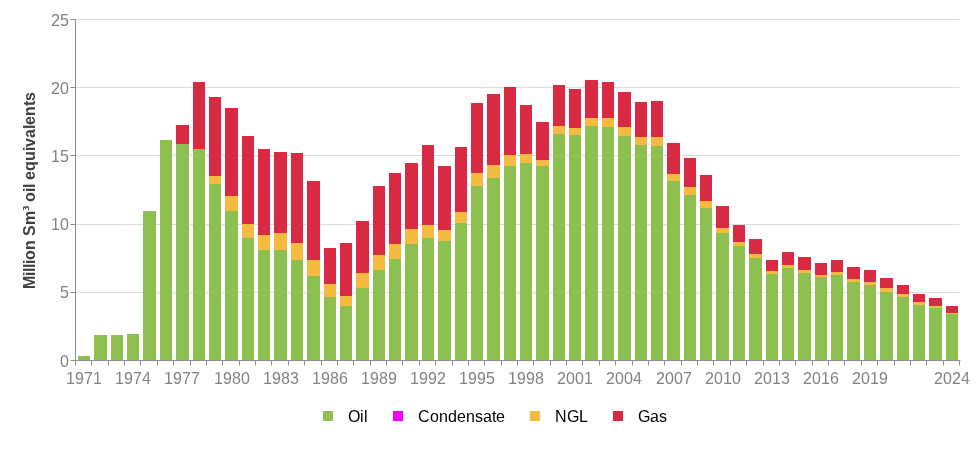

Ekofisk production history; water injection began boosting production in 1987. The expected final recovery factor for Ekofisk is now estimated to be >50%.

ConocoPhillips and partners have approved the redevelopment of three gas and condensate fields depicted below — Albuskjell, Vest Ekofisk, and Tommeliten Gamma. Better well placement and the use of horizontal well technology will increase resource recovery.

The $1.8 billion project consists of four new subsea templates and 11 production wells tied back to the Ekofisk complex. First production is planned towards the end of 2028. Recoverable gas and condensate reserve additions are estimated at between 90 million and 120 million barrels of oil equivalent.

If you ever get to Stavanger, be sure to visit the Petroleum Museum! HIghly recommended!

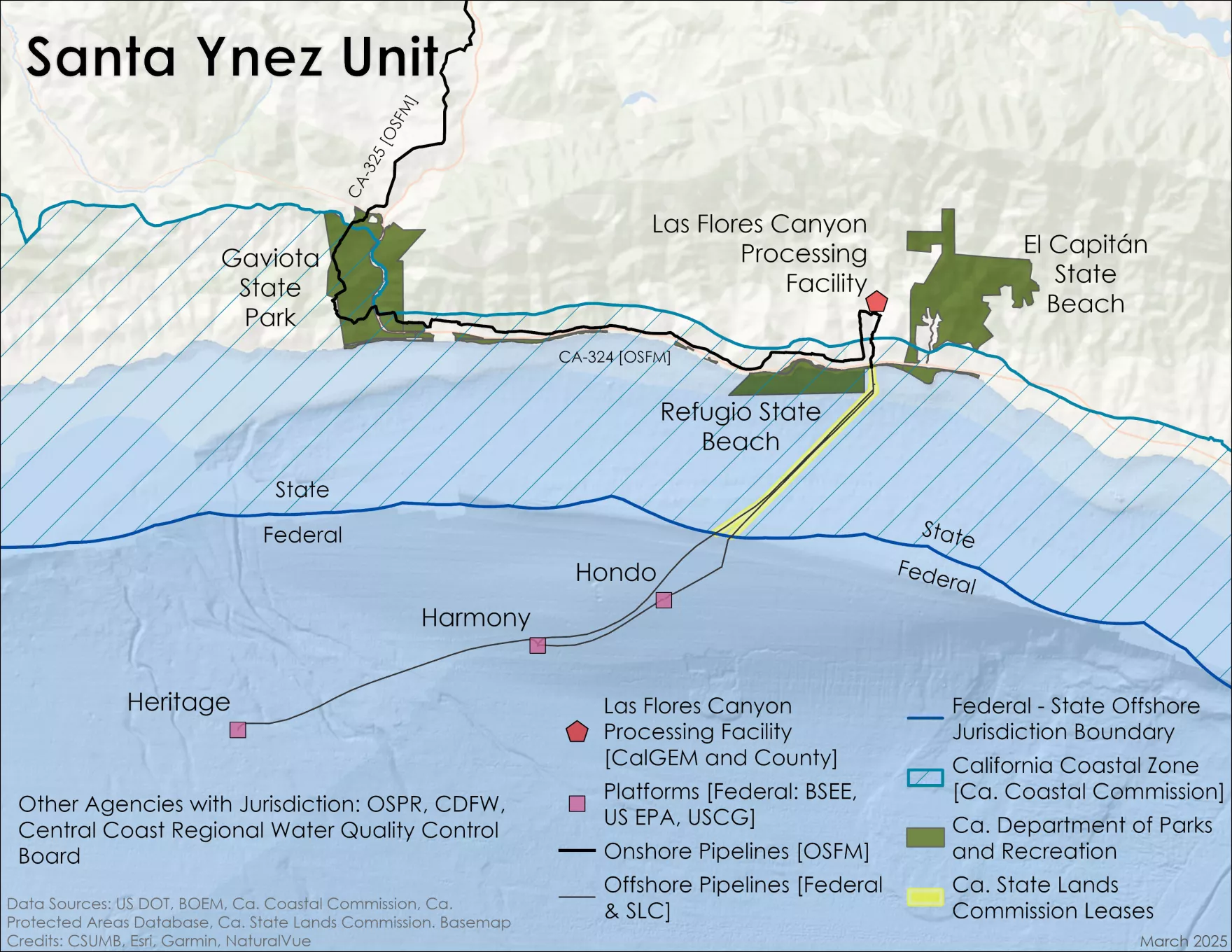

The anticipated State-Federal jurisdictional battle over Sable’s Las Flores Canyon Pipeline is on! See the attached letter from the Pipeline and Hazardous Materials Safety Administration (PHMSA) declaring that the pipeline is under Federal jurisdiction.

The major hurdle for PHMSA/Sable is thecourt approved Consent Decree that was executed following the 2015 Refugio pipeline spill. The Decree, which designates the California Fire Marshal as the sole regulator for the pipeline, is not mentioned in the PHMSA letter. Needless to say, another major legal battle looms.

Excerpt from the PHMSA letter:

PHMSA’s evaluation of the Las Flores Pipeline confirms that it transports crude oil from the OCS to an onshore processing facility at Las Flores Canyon and continues the transportation of crude oil from Las Flores Canyon to Pentland, California. Consistent with Appendix A, the Las Flores Pipeline is an interstate pipeline. As portions of the Las Flores Pipeline were previously considered to be intrastate and regulated by OSFM, PHMSA is notifying OSFM that the Las Flores Pipeline is subject to the regulatory oversight of PHMSA.

The vote on the transfer of Santa Ynez Unit (SYU), Pacific Offshore Pipeline Company (POPCO) Gas Plant, and Las Flores Pipeline System permits from Exxon to Sable Offshore was the last item on the Board’s agenda, so those of us who were streaming the meeting for that topic had to be patient.

The Sable session began with a surprise announcement that opened the possibility that perhaps the outcome might not be as expected. Supervisor Hartmann, who owns property close to the pipeline, had once recused herself from voting on this matter. When it was thought that her property was ~900′ from the pipeline, the Fair Political Practice Commission (FPPC) cleared her participation. However, after a 12/3/2025 letter from Sable informed that her property was as close as 8′ from the pipeline, the FPPC reversed its position and Supervisor Hartmann again recused herself.

Supervisor Hartmann’s re-recusal added some drama to the session given that there were two sure votes against Sable and one sure vote in favor. The swing vote would be that of Supervisor Lavagnino, who was very much supportive of the oil industry, but not Sable.

After strong but predictable presentations by the Environmental Defense Center/Center for Biological Diversity team and Sable, the floor was open to public comments. Although there were more speakers opposed to the Sable position (13), this observer found the Sable supporters (7) to be more compelling. Most were California natives who worked on the project and demonstrated a sincere commitment to the safety and environmental values that we all support. One aptly noted that California unnecessarily imports 2/3 of its oil from foreign sources, some of which aren’t particularly friendly.

As an aside, a County staffer pointed out that 400,000 barrels of SYU oil were in storage as a result of the resumption of production in May prior to receiving the necessary approvals to transport oil through the onshore pipeline.

The vote opened with Supervisor Nelson supporting the transfer of permits to Sable. His commented that the County was “attacking Sable’s finances at the same time they were trying to bankrupt them.”

Sable opponents held serve with Supervisors Capps and Lee opposing the transfer. Ms. Capps deserves credit for the sincere respect she showed for the Sable workers who were present.

So Supervisor Lavagnino would cast the deciding vote. He once again voted against the transfer noting that he was a long time supporter of the oil industry, but that he had lost confidence in Sable.

Bottom line: The outcome was as expected, but the recusal drama and strong presentations made the stream worth watching.

The attached Memorandum of Understanding between Vineyard Wind (VW) and the Town of Nantucket is long on bureaucratic procedures and short on risk mitigation and penalties.

The agreement details requirements for monthly reports, liaisons, written correspondence, plan reviews, and participation on incident management teams, but excludes any monetary penalties for past or future incidents. (With regard to penalties, should BSEE have assessed civil penalties for the 2024 turbine incident in accordance with 30 CFR § 285.400 (f)? This was a major pollution event.)

This MOU provision gives the impression that the Town is subordinate to VW:

“The Town will provide Vineyard Wind 1 up to 4 business days, if required, to identify and correct errors in the Town’s intended public communications about the Project.”

The responsible party should not be exercising oversight over the communications of an affected local government. Can you imagine Santa Barbara County reaching such an agreement with Sable Offshore?

Finally, the MOU further establishes the Town as a de facto partner in the project. VW, not the Town, is the responsible party and must be held fully accountable for project performance.

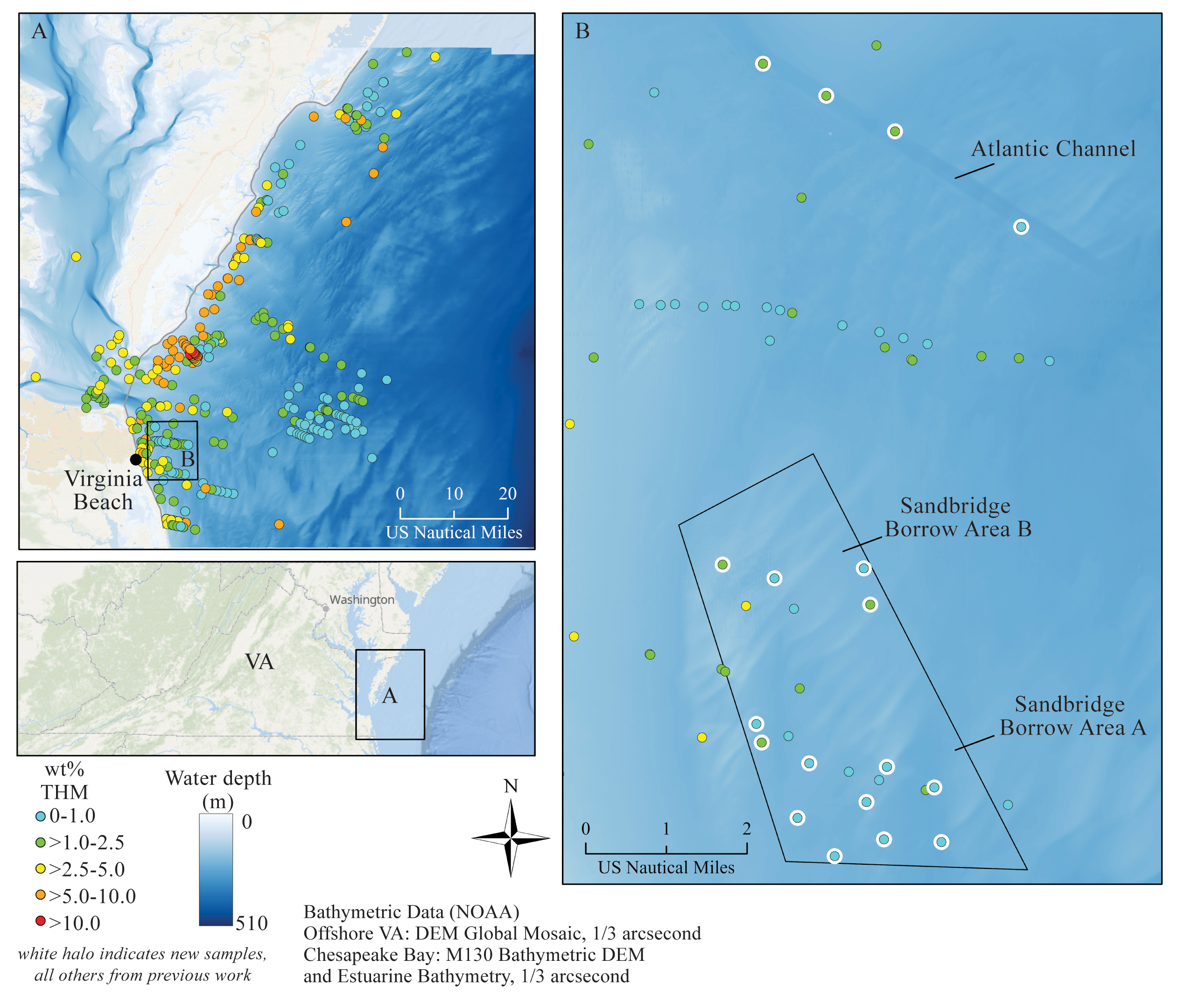

Heavy mineral geodatabase showing marine samples offshore of Virginia. A: 620 samples with heavy mineral data from previous projects, symbol colors determined by the percent of total heavy minerals (THM) obtained through gravity spiral separation methods. B: M21AC00010 samples (indicated with white halo) from Sandbridge Shoal and Atlantic Channel vibracores for THM and mineralogical analyses.

Odyssey’s primary targets are phosphate, which is now on the critical minerals list, and rare earth element’s titanium and zirconium. This would be a shelf dredging operation, in partnership with Great Lakes Dredge & Dock Company, rather than the deepwater module collection being proposed for the Pacific.

The fact that the sand recovered during the dredging process could be used for beach nourishment should appeal to adjacent coastal communities.

Odyssey Marine’s CEO discusses the proposed Virginia offshore program starting at the 4:00 minute mark in the video below.

While the majors and large independents garner most of the attention, smaller companies are an integral part of the mosaic that is the Gulf of America petroleum province. Some focus on producing and identifying remaining reserves on the shelf; others partner in deepwater projects.

Sale participants like Arena, Cantium, Walter, W&T, Beacon, Kosmos, and Houston Energy are well established Gulf leaseholders. Red Willow has attracted attention as a successful Southern Ute energy corporation.