While the Orsted acquisition does not appear to have been directed by the Norwegian government, the State’s 2/3 ownership of the company no doubt influences renewable energy targets and broader corporate strategy.

The initial market reaction to the Orsted purchase was negative (see chart below). On a day when most oil companies’ share prices rose in response to the jump in oil prices, Equinor shares opened sharply lower.

The offshore safety regulator (BSEE) has a very capable technical staff and should produce an informed report on the Vineyard Wind blade failure. The concern is with the internal review process that has seriously delayed the publication of accident investigation reports and safety alerts.

Presumably, DNV, the Vineyard Wind CVA, will provide input into the BSEE investigation. Perhaps the effectiveness of the CVA process and quality control procedures should be separately considered.

Will Equinor, a major oil and gas producer, Dogger Bank partner, and offshore wind advocate, be investigating the Dogger Bank failures?

A comprehensive International data base on turbine incidents and performance is needed.

As previously noted, offshore substations are large structures. A closeup of the Vineyard Wind 1 substation is pasted below.

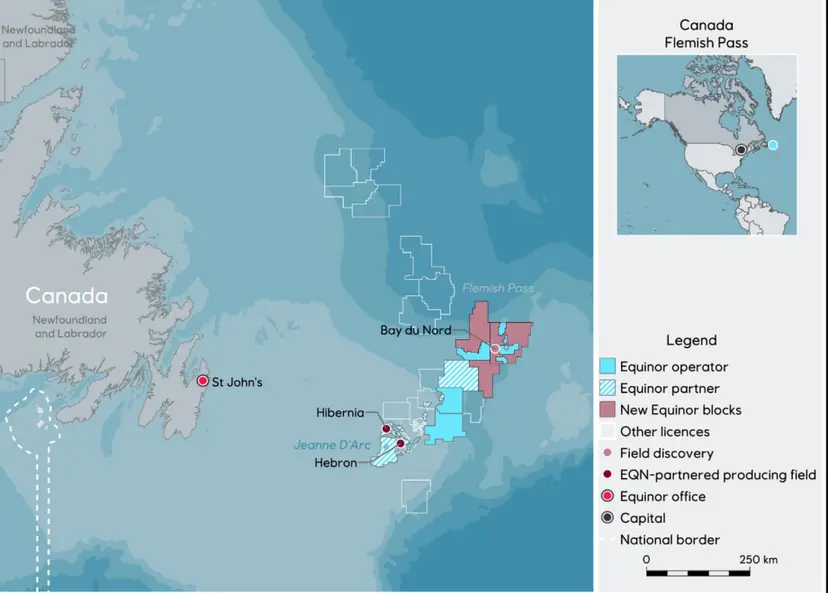

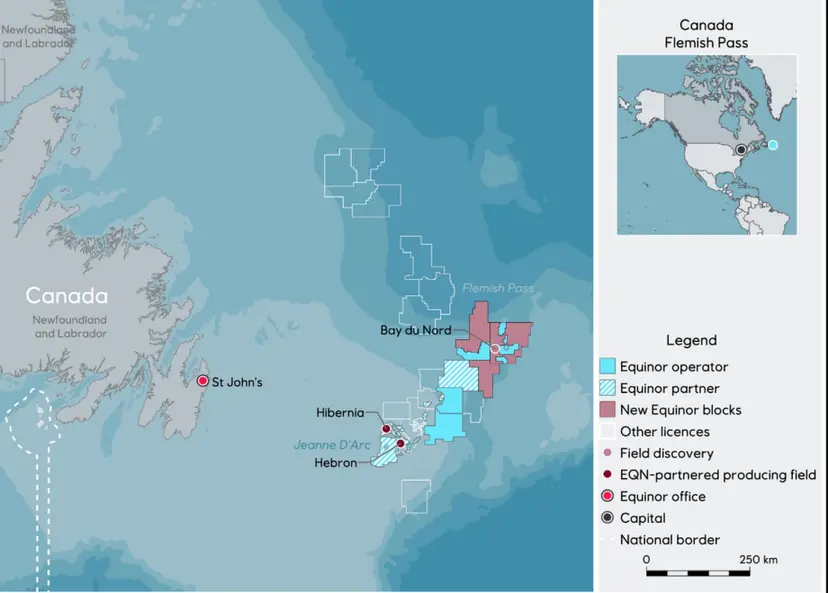

Per the CNLOPB weekly activities report, Equinor spudded the important Sitka C-02 well in the Flemish Pass area on July 10, 2024. This well will help clarify the resource potential in the Bay du Nord project area with the goal of better defining development plans.

Meanwhile, operations on Exxon’s important Persephone well in the Orphan Basin have now been ongoing for 2 months. Some type of announcement by Exxon is expected after operations are completed and the well has been plugged.

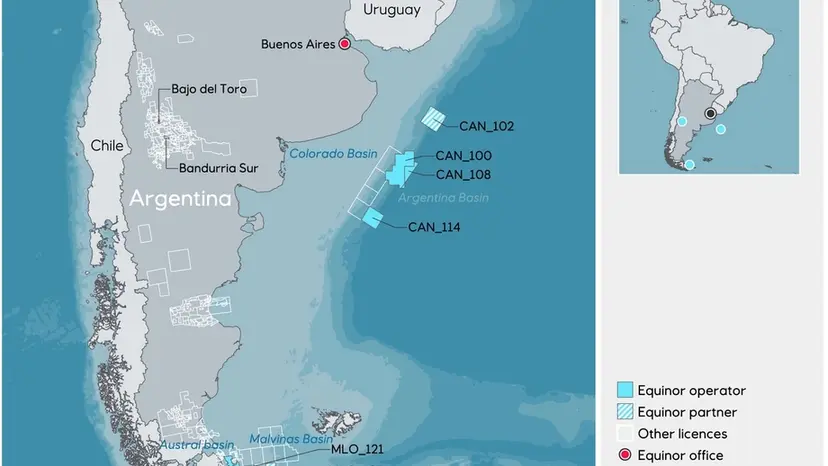

The Valaris DS-17 drillship is now on location to drill the Algerich-1 well for Equinor 315 km from Mar del Plata in 1527 m of water at Block CAN 100.

Concurrently, at the opposite end of the Pan American continents, the Stena DrillMAX is closing in on Exxon’s Orphan Basin location offshore Newfoundland to drill another high potential well.

One person has died following the helicopter crash outside Bergen in Norway on the night of Wednesday 28th February. The helicopter was on a training assignment for Equinor ’s SAR service for the Oseberg area in the North Sea.

Search and rescue service is critical to offshore safety, and North Sea operators have excellent SAR capabilities. Sadly, one person died and five were injured (two seriously) when a Sikorsky S-92 helicopter, owned by Bristow and under contract to Equinor, crashed offshore Bergen last night. The crew was training to serve offshore workers in need.

The CNLOPB has announced contingent resources of 340 million bbls for the Cambriol discovery which would be co-developed with 2 nearby discoveries as part of Equinor’s Bay du Nord project. Per CNLOPB estimates, this brings the Bay du Nord resource total to 1.132 billion bbls. Equinor has announced that 2 exploratory wells will be spudded this summer. Positive results would further strengthen the case for Bay du Nord development.

contingent resources per CNLOPB (million bbls)

Bay du Nord

407

Cappahayden

385

Cambriol

340

project areatotal

1132

“Contingent Resources” are volumes of hydrocarbons, expressed at 50% probability, assessed to be technically recoverable that have not been delineated and have unknown economic viability.

Meanwhile, Terra Nova production is ramping up after a long hiatus for FPSO refurbishment, remarkable Hibernia has produced more than double the original resource estimate of 520 million bbls and is still producing about 60,000-70,000 bopd, and Hebron is impressively producing about 120,000 bopd on average.

There is indeed reason for optimism about North America’s only Atlantic production in what is arguably the continent’s (world’s?) most challenging operating environment.

It’s prudent, if not imperative, to tow floating wind turbines to sheltered coastal locations for major maintenance. For that reason, Hywind, the world’s first floating wind farm will be offline for up to 4 months this summer.

Hywind Scotland‘s operator, Norwegian power giant Equinor, says that operational data has indicated that its wind turbines need work. The pilot project has been in operation since 2017.

The five Siemens Gamesa turbines will be towed to Norway this summer. An Equinor spokesperson said, “This is the first such operation for a floating farm, and the safest method to do this is to tow the turbines to shore and execute the operations in sheltered conditions.”

Published data indicate that Hywind has been the UK’s best performing offshore wind farm. Performance data for Hywind, and a chart illustrating the capacity factors since commissioning, are posted below. The 2024 capacity factor will, of course, be substantially reduced as a result of the essential offsite maintenance.

capacity factor = total energy generated/(hours since commissioning x capacity)

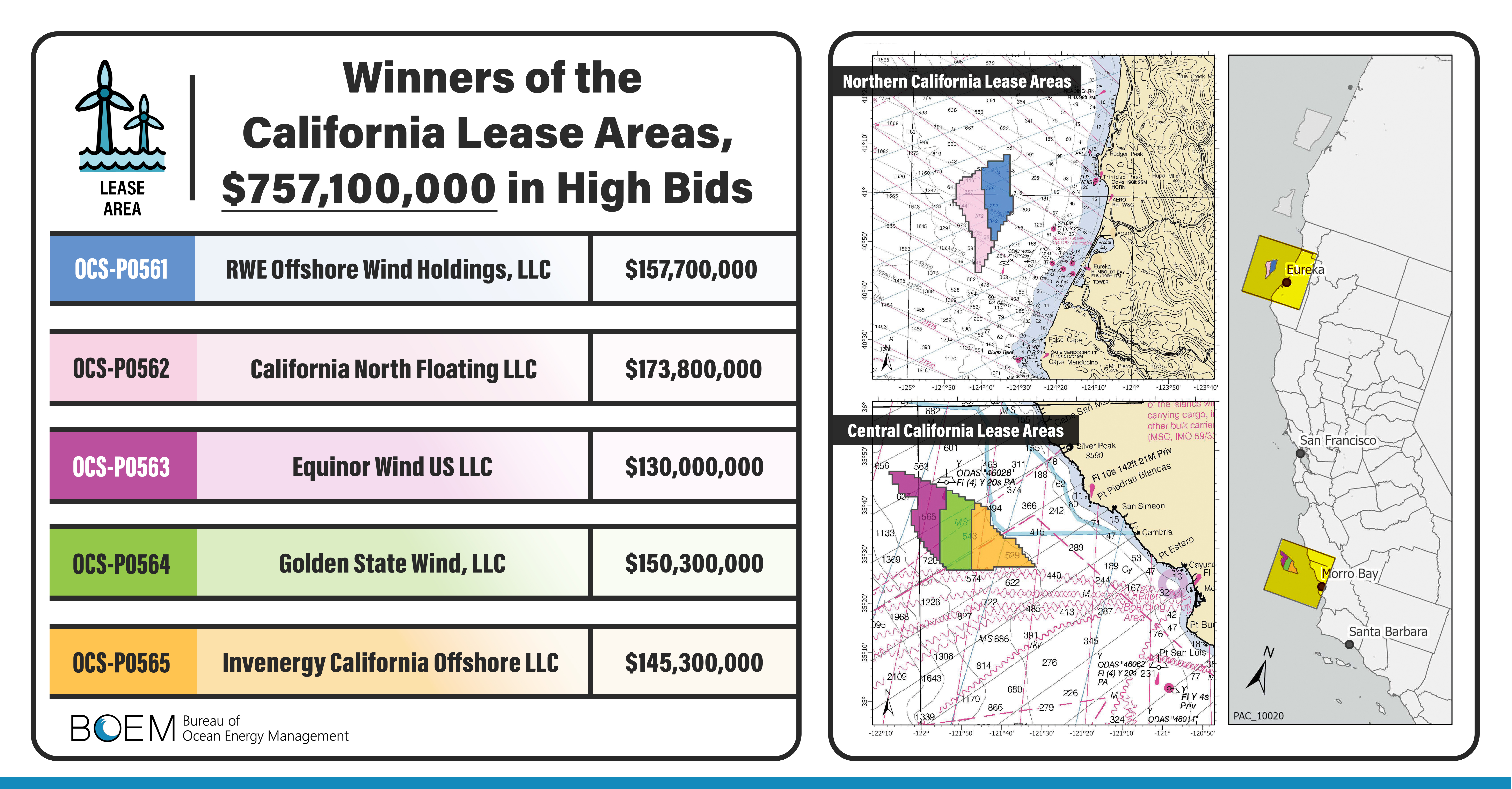

The first US floating turbines are expected to be at these California offshore leases, and Hywind operator Equinor is one of the lessees:

Given the financial challenges facing the offshore wind industry, the still emerging technology, and the risks inherent in California offshore development, the amounts bid on these leases only 13 months ago are stunning.

Some Central Coast residents are not enamoured with “another attempt to industrialize the coast.” Although the turbines will be >20 miles offshore, they will have to be towed to shore for major maintenance. For the Central California leases, nearby harbor areas like Morro Bay (pictured below) would be overwhelmed by the large structures and the maintenance and repair operations. Towing the towers to LA/Long Beach, albeit rather distant from the leases, would seem to be the preferred option for such work.

Ironically, a report for BOEM, points to synergies between the offshore wind industry and oil and gas decommissioning industry. Such synergies will only be possible if longstanding oil and gas decommissioning obstacles are satisfactorily addressed and the offshore wind projects proceed as planned.

Which will come first – platform decommissioning or wind turbine commissioning? For those young enough to find out, what is the over-under for the years until (1) half of those platforms are decommissioned, and (2) half of the wind turbines commissioned? Any number <10 is unrealistic for either.

Biggest prize at the holiday party went to Anadarko: Mississippi Canyon 389 – 5 bids, $25.5 million high bid

Biggest holiday shopping spree: Shell’s 65 high bids accounted for 24% of the sale’s high bids (excluding CCS bids).

Big spender award: Hess – $88.3 million on only 20 high bids. Does Chevron approve? 😀

Aussie, Aussie, Aussie, Oi, Oi, Oi: Strong performance by Woodside. 18 high bids, $24.8 million

Heia Norge!: Equinor continues to shine in the GoM! 13 high bids, $20.6 million

Spirit of America award to Red Willow Offshore which is owned by the Southern Ute tribe. 22 high bids!

Deepwater independents for (energy) independence: Beacon, Murphy, LLOG, Kosmos, Talos, Houston Energy, Ridgewood, QuarterNorth, Alta Mar, CSL, CL&F, and Westlawn

Even pace wins the race: Another solid lease sale for bp – 24 high bids.

So happy together 😀: Chevron and Hess combined for 48 high bids, $114 million

Coal in their stockings? Repsol (Sale 261) and Exxon (Sales 257 and 259) made up their own rules for acquiring carbon dumping leases. Perhaps some solid carbon in their Christmas stockings would be appropriate.

Christmas in July?: A lease sale in 2024 is needed. Sometime near the 4th of July holiday would be good. It’s up to you Congress!

Holiday greetings to our friends around the world!

The Tiberius exploration well tested a four-way structural trap in the outboard Wilcox trend, located in Keathley Canyon Block 964. The well encountered approximately 250 feet (~75 meters) of net oil pay in the primary Wilcox target. Wireline logging has been completed and casing is currently being run to the target depth to enable the well to be used as a future oil producer. The Tiberius well is located in approximately 7,500 feet (2,300 meters) of water and was drilled to a total vertical depth of approximately 25,800 feet (7,800 meters).

BSEE data indicate that Kosmos has an excellent compliance record, having been cited for only 3 violations during 44 facility inspections (83 inspection types) since 1/1/2018.

One quibble: the Kosmos news release does not name the drilling unit or drilling contractor. The rig crew is the group most responsible for safely drilling the well.

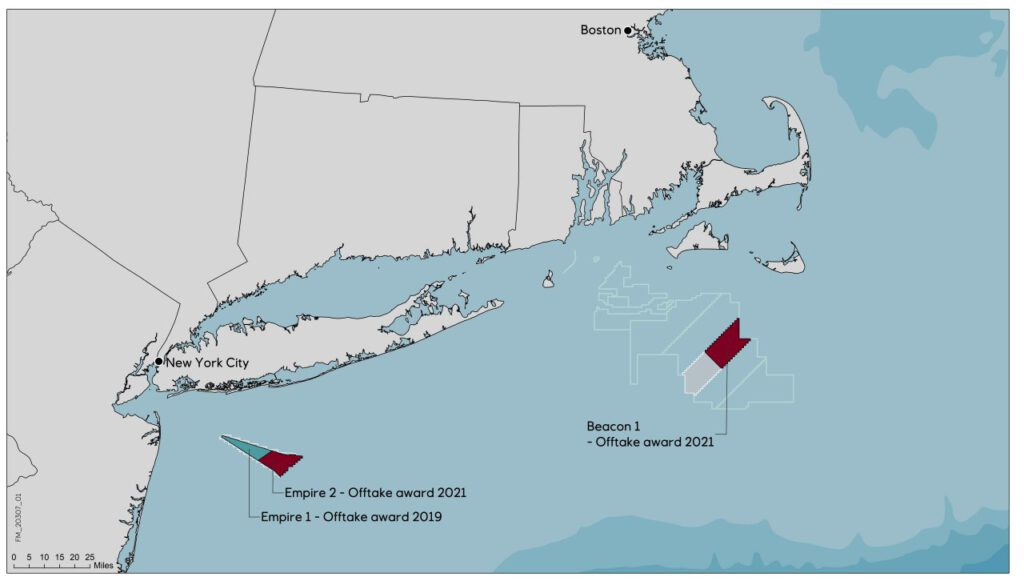

According to the New York State Energy Research and Development Authority, this would result in an average 54% price hike across their portfolio. The strike prices would rise from $118.38 to $159.64/MWh for Empire Wind 1, from $107.50 to $177.84/MWh for Empire Wind 2, and from $118.00 to $190.82/MWh for Beacon Wind.