Deepwater (>1000′) activity continues to dominate, accounting for 61% of the well starts.

Not a single company drilled both shelf and deepwater wells.

While shelf facilities currently account for only about 7% of GoM oil production, 1122 of the 1179 remaining platforms are on the shelf and they account for 24% of GoM gas production, most of which is environmentally favorable nonassociated gas.

Two companies, Arena and Cantium, accounted for 75% of the shelf well starts. Excluding the CCS bids, Arena and Cantium were the most active shelf bidders in Sale 279. Arena bid alone on 7 blocks. Cantium was the high bidder on 5 blocks. (Focus Exploration was high bidder on 4 shelf blocks and was “outbid” by Exxon for High Island 177.)

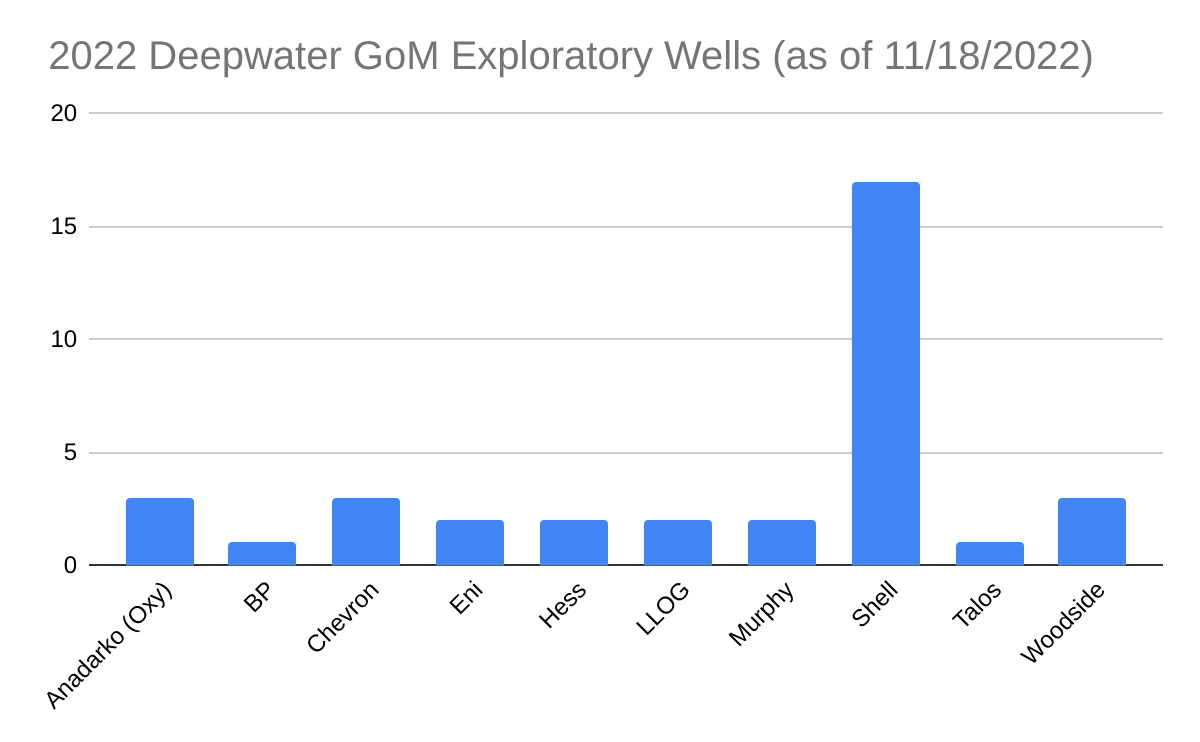

One company, Shell, accounted for 39% of the deepwater well starts

One of BP’s exploratory wells (drilled subsequent to Sale 257) was in Green Canyon 821, immediately south of GC 777, the block that BP/Talos bid $1.8 million for in Sale 257. That bid was rejected by BOEM. In sale 259, BP was the sole bidder for GC 777, and their bid was only $583,000, less than 1/3 of their Sale 257 bid. Perhaps the GC 821 exploratory well reduced the value of GC 777? Will this lower bid now be accepted?

DW expl

DW dev

shelf expl

shelf dev

Anadarko

5

1

Arena

22

BOE

1

4

BP

2

3

Byron

2

Cantium

20

Chevron

3

Contango

2

Cox

2

Eni

2

5

EnVen

5

Greyhound

2

Hess

2

Kosmos

1

LLOG

3

1

Murphy

4

QuarterNorth

2

Shell

25

9

Talos

2

8

Walter

1

Woodside

3

1

Gulf of Mexico well starts during 2022 and the first quarter of 2023

Green Canyon 79 received a bid of $3.6 million at Sale 257, but no lease was ever issued. No explanation was provided and there were no bids for this block at Sale 259.

There was actually a second bidder, Focus Exploration, for one of the 69 “CCS blocks,” that Exxon seeks to acquire (see below). Exxon’s bid was higher. Does this mean that Focus, a company that is presumably interested in exploring for oil and gas, will lose the block to a company that bid on the block for purposes not authorized in the Notice of Sale?

Exxon doubled down on their strategic CCS bidding; their only bids (69 in total) again appeared to be solely for carbon sequestration purposes. As previously noted, acquiring tracts for CCS purposes is not authorized in an oil and gas sale. Arguably, these bids should be rejected.

The other super-majors, BP, Chevron, and Shell, were active participants as were many independents.

It was good to see BOEM Director Liz Klein announcing bids. This shows respect for the OCS oil and gas program.

“I am of a firm view that the world will need oil and gas for a long time to come,” (Shell Chief Executive) Sawan, who started the job on Jan. 1, told Times Radio in the U.K. on Friday. “As such, cutting oil and gas production is not healthy.”

Back in 2021, Shell predicted that its own oil production would decline every year and drop by as much as 18% by 2030. BP had a similar outlook, but CEO Bernard Looney rolled back its climate targets this year and said it will increase investment in exploration and production.

BP and Shell have trailed their U.S. peers in price to earnings ratios. Analysts have said investors interested in exposure to oil and gas have shunned them for putting more money into renewables, while investors focusing on environmental concerns haven’t rewarded them. That’s kept European energy firms trading at a discount.

BOEM published their Sale 257 Decision Matrix on Friday (2/24/2023), and my previous speculation regarding the rejected Sale 257 high bid has proven to be partially incorrect. The rejected high bid was submitted by BP and Talos and was for Green Canyon Block 777. BOEM’s analytics assigned a Mean of the Range-of-Value (MROV) of $4.4 million to that tract, which tied for the highest MROV for any tract receiving a bid. The BP/Talos bid was $1.8 million or just 40% of BOEM’s MROV. BOEM’s tract evaluation is interesting given that the other bid on this wildcat tract (by Chevron, $1.185 million) was considerably lower than the rejected BP/Talos bid.

The Sale 257 bid that I thought might have been rejected was for lease G37261. This lease was never issued per the lease inquiry data base and the final bid recap. BHP’s bid of $3.6 million for that tract (Green Canyon Block 79) was more than 5 times BOEM’s MROV of $576,000, and was accepted per the decision matrix. Why was the lease never issued?

Both Green Canyon 79 and 777 should again be for sale in legislatively mandated Sale 259, which will be held in just a few weeks on March 29, 2023, just 2 days prior to the deadline. It will be interesting to see what the bidding on those tracts looks like.

Meanwhile, Exxon and BOEM are still mum about the 94 Sale 257 oil and gas leases that Exxon acquired for carbon sequestration purposes.Note the large patches of blue just offshore Texas on the map above. These leases were all valued by BOEM at only $144,000 each, which is equivalent to the minimum bid of $25/acre. This valuation reflects the absence of perceived value for oil and gas production purposes. Exxon bid $158,400 for each tract, $27.50/acre or 10% higher than the minimum bid. Given that (1) the Notice of Sale only provided for lease acquisition for oil and gas exploration and production purposes, and (2) it was common knowledge that these tracts were acquired for carbon sequestration, should these bids have been rejected?

Last year, BOE featured 5 deepwater platforms that were under construction: Shell’s Vito and Whale, Murphy’s King’s Quay, bp’s Argos, and Chevron’s Anchor. These floating production units are noteworthy for their lighter, smaller designs. King’s Quay was the first to produce, beginning last April. The spotlight is now on Vito which began producing today. Vito’s peak production should reach 100,000 boe. The other 3 platforms are expected to begin production this year or next.

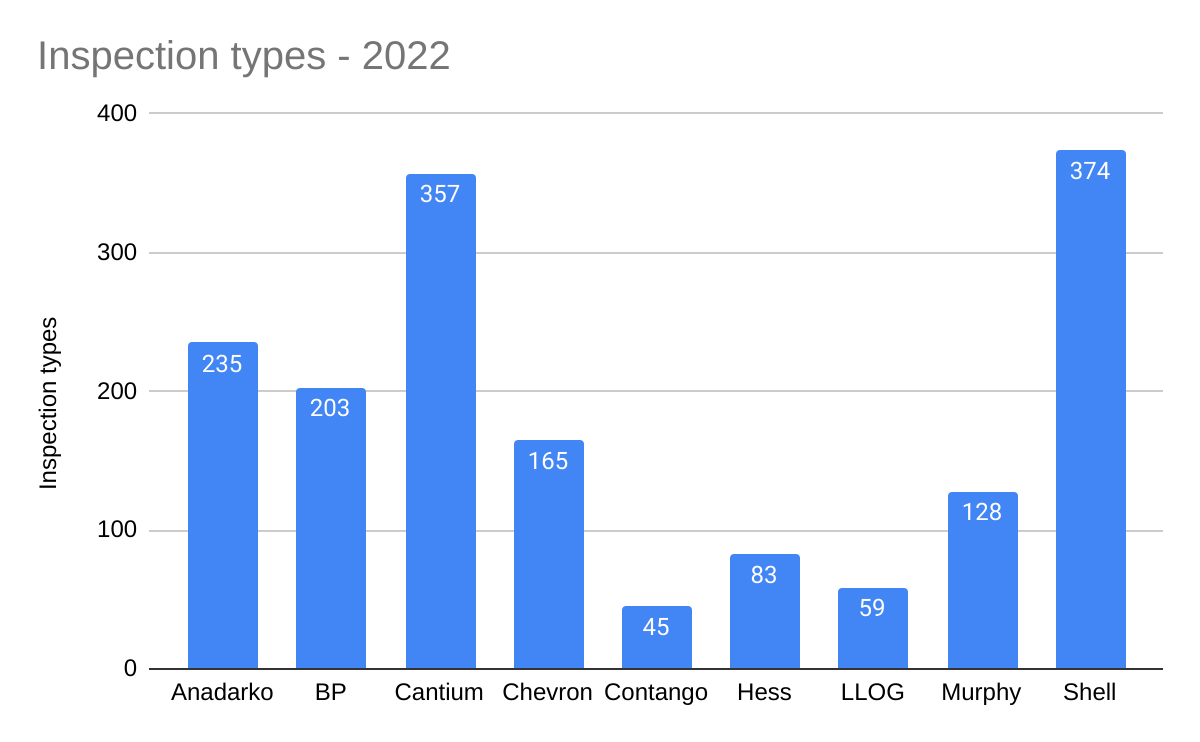

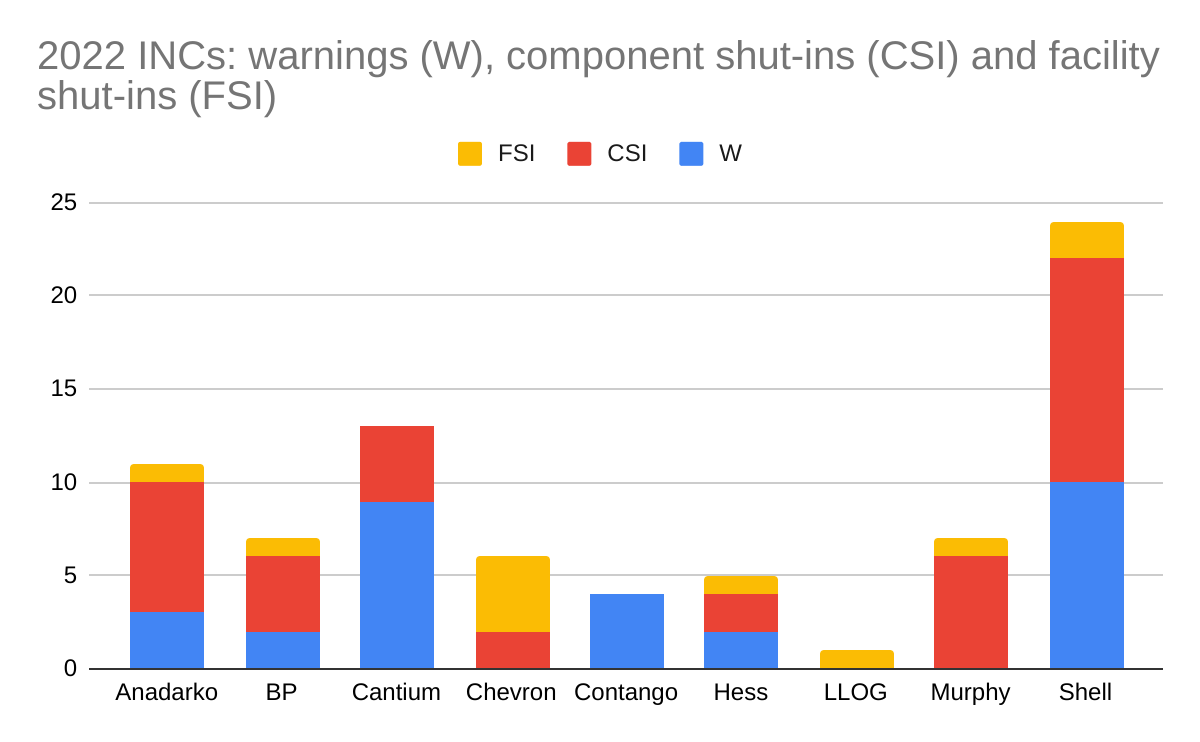

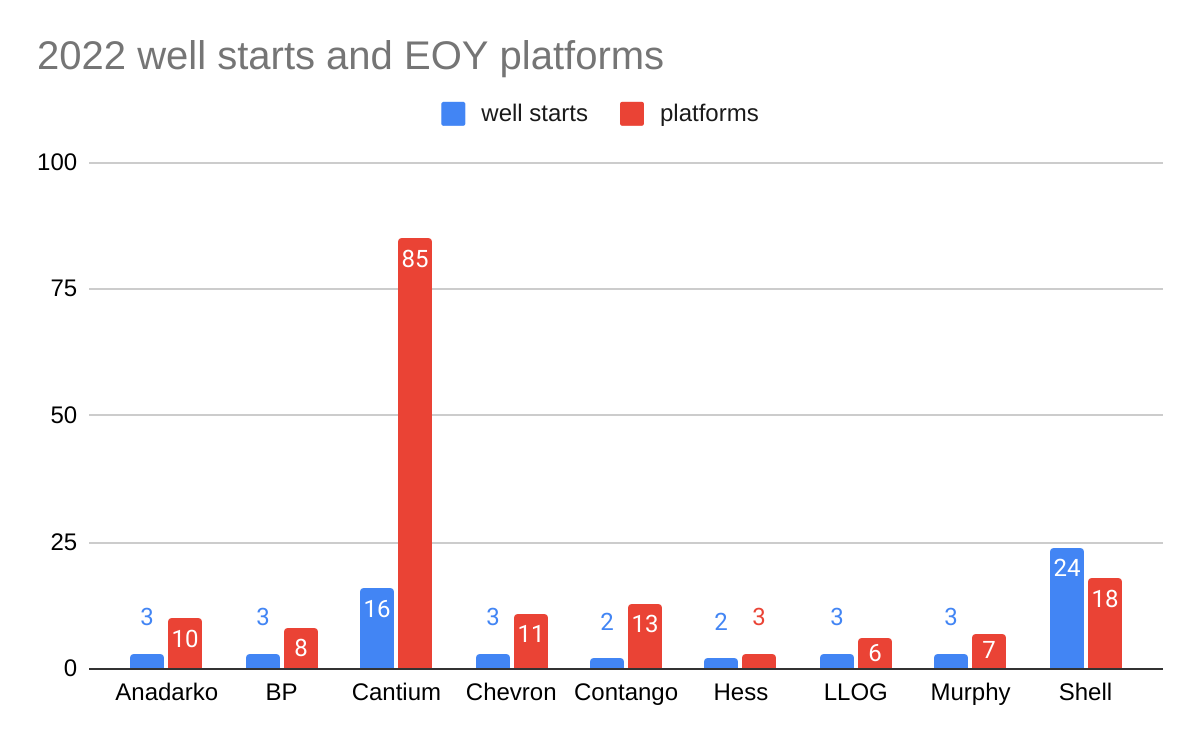

The Honor Roll companies for 2022 (listed alphabetically) are Anadarko (Oxy), bp, Cantium, Chevron, Contango, Hess, LLOG, Murphy, and Shell.

Our criteria:

Must average <0.3 incidents of noncompliance (INCs) per facility-inspection.

Must average <0.1 INCs per inspection-type. (Note that each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). On average, each facility-inspection included 3.25 types of inspections in 2022. Here is a list of the types of inspections that may be performed.)

Must operate at least 3 production platforms and have drilled at least one well (i.e. you need operational activity to demonstrate compliance and safety achievement).

May not have a disqualifying event (e.g. fatal or life-threatening incident, significant fire, major oil spill). Due to the extreme lag in updates to BSEE’s incident tables, investigation and news reports are used to make this determination.

Pacific and Alaska operations will be considered separately.

Foremost energy experts like Daniel Yergin understand that oil and gas will be critical to our economy and security for decades, and that offshore production is an important component of our energy supply chain. Unfortunately, our massive outer continental shelf has, from an oil and gas standpoint, been effectively reduced to the central and western GoM.

Opportunities in the GoM are being seriously constrained by the extended pause in leasing. A lease sale has not been held for 615 days, the longest US offshore leasing gap since the 1950’s.

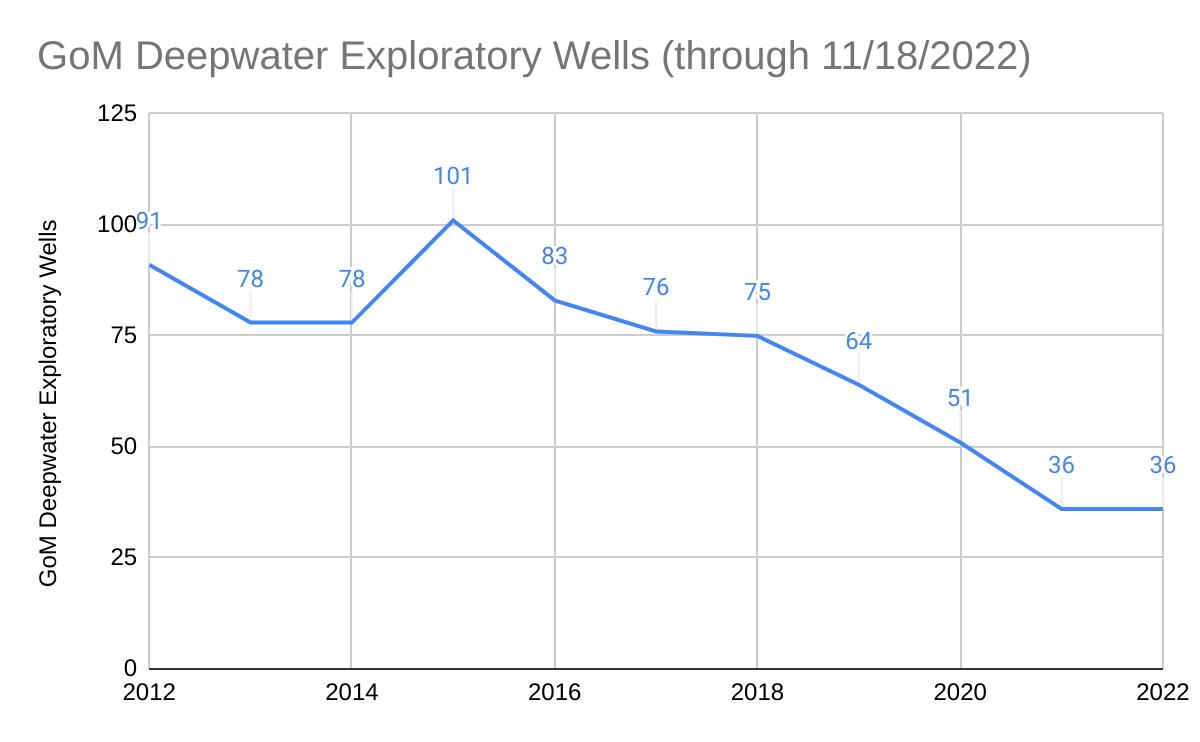

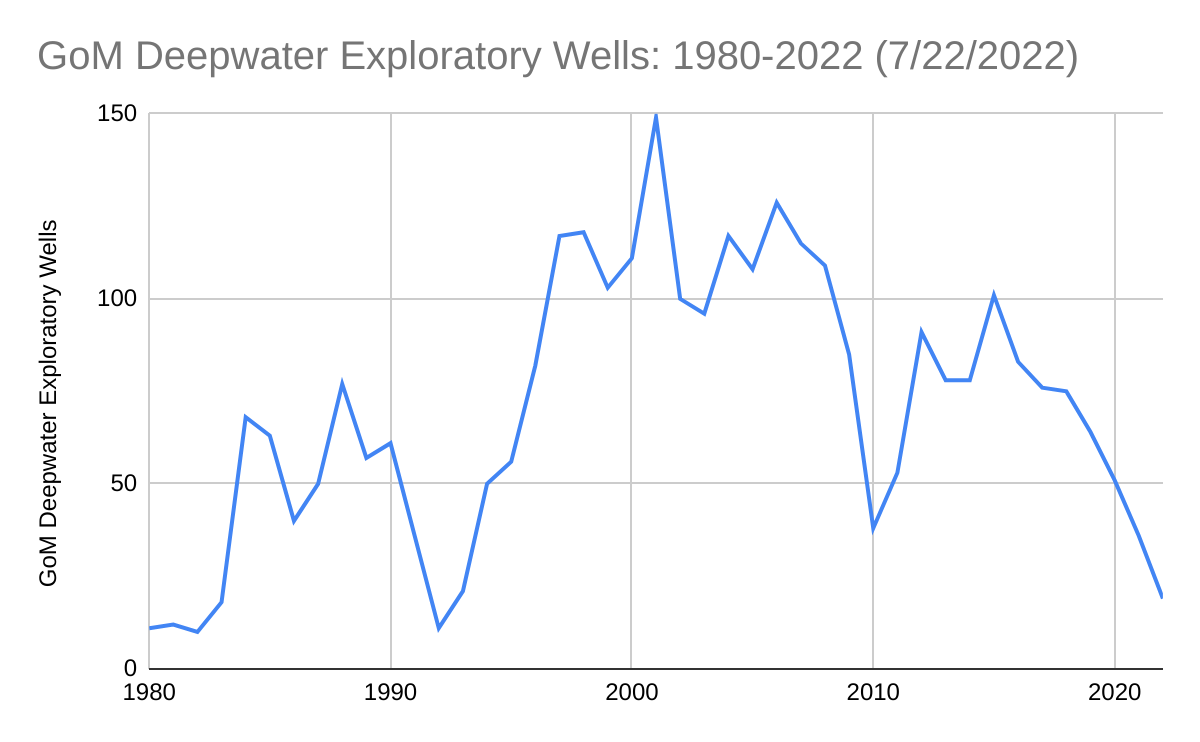

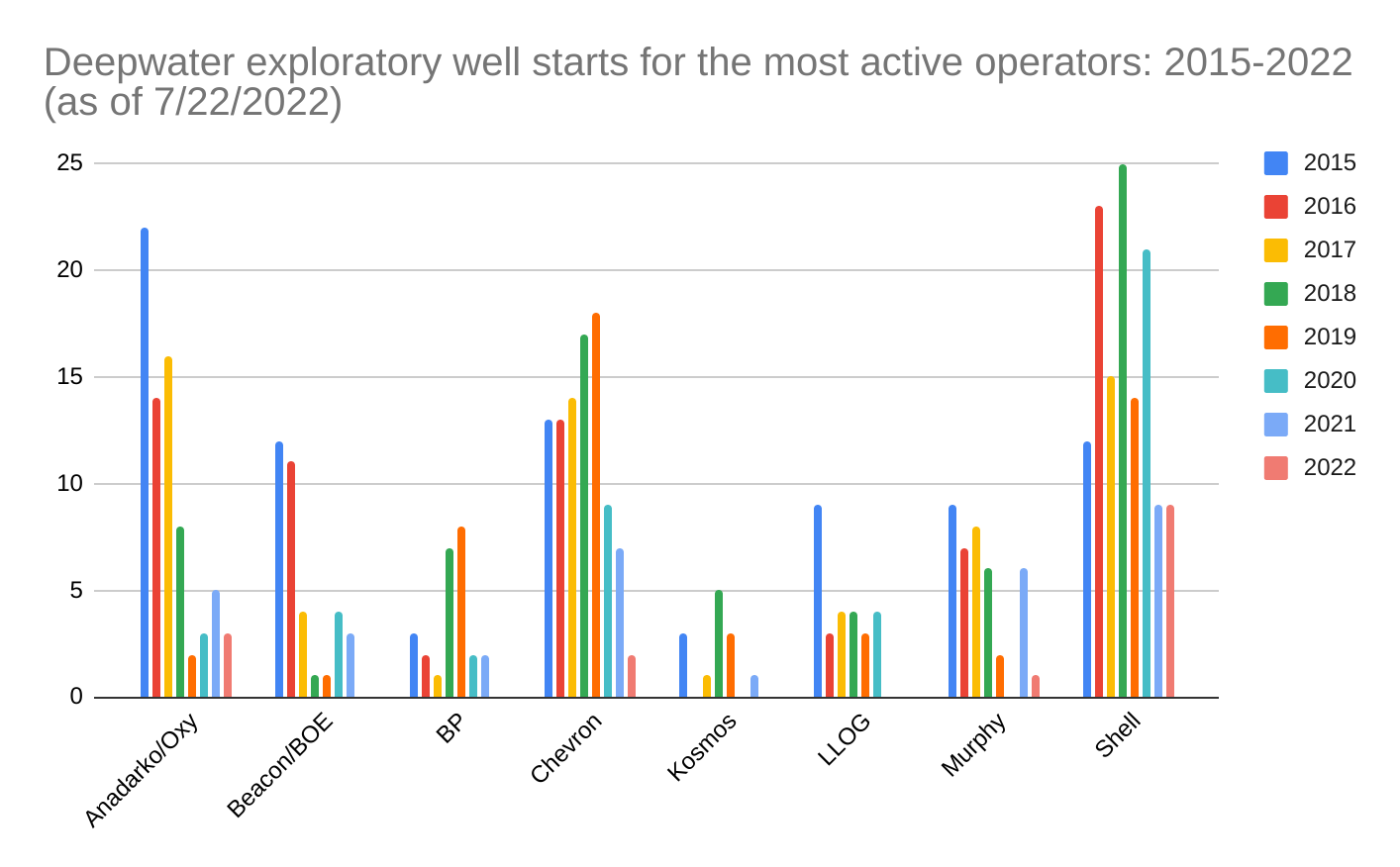

Reserve replacement and sustained production are dependent on exploration. The charts below illustrate the decline in GoM exploratory drilling and the reduced activity by some of the more important operating companies.

Per BSEE data, the number of exploratory well starts averaged only 3/month for the last 18 months (chart 2). This level of activity is the lowest since the early days of deepwater operations (chart 1). There was even more drilling during the post-Macondo moratorium (2010-2011).

ConocoPhillips and Exxon have not drilled a GoM exploratory well since 2016 and 2018 respectively. Activity by other operators has also declined significantly (chart 3). BP has not spudded an exploratory well since Sept. 2021.