Important article by E&E News reporter Heather Richards.

BOE blog post: “The troubling case of Platforms Hogan and Houchin, Santa Barbara Channel”

Important article by E&E News reporter Heather Richards.

BOE blog post: “The troubling case of Platforms Hogan and Houchin, Santa Barbara Channel”

Posted in California, decommissioning, Gulf of Mexico, Offshore Energy - General | Tagged BOEM, decommissioning, John B Smith, Platform Hogan, Platform Houchin, Santa Barbara Channel | Leave a Comment »

The table in the Sale 259 bid rejections post has been corrected below. That table incorrectly reported that subsequent bids for Keathley Canyon Blocks 745 and 789 were rejected at Sale 261. Those bids were in fact accepted. Houston Energy was identified as the submitter rather than Beacon Offshore Energy, the company that, per the bidding data, had the largest ownership share. (See the bidding partnership pasted below.)

The acceptance of those 2 bids significantly increases the net gain to the government as a result of the Sale 259 bid rejections. See the corrections in red to the table:

| area and block | Sale 259 rejected high bid – company | Sale 261 high bid | bid accepted | govt gain (loss*) |

| DC 622 | 2,101,836 – Shell | 615,628 – Shell | yes | (1,486,208) |

| GC 173 | 307,107 – Woodside | no bid | NA | (307,107) |

| GC 547 | 1,783,498 – Chevron | no bid | NA | (1,783,498) |

| GC 591 | 1,291,993 – Chevron | no bid | NA | (1,291,993) |

| GC 642 | 605,505 – Anadarko | no bid | NA | (605,505) |

| GC 777 | 583,103 – bp | no bid | NA | (583,103) |

| AT 5 | 1,551,130 – Anadarko | 5,215,628 – Shell | yes | 3,664,498 |

| AT 133 | 607,107 – Woodside | no bid | NA | (607,107) |

| KC 745 | 707,777 – Beacon | 2,422,222 – | 1,714,445 | |

| KC 789 | 707,777 – Beacon | 2,143,299 – | 1,435,522 | |

| WR 794 | 724,744 – Beacon | 1,487,624 – Beacon | yes | 762,880 |

| WR 795 | 774,242 – Beacon | 5,301,107 – Woodside | yes | 4,526,865 |

| WR 796 | 774,242 – Beacon | 3,310,107 – Woodside | yes | 2,535,865 |

| WR 750 | 724,744 – Beacon | 1,498,555 – Beacon | yes | 773,811 |

| total govt. gain | 8,748,365 |

More on the Sale 261 bidding next week.

Posted in Gulf of Mexico, Offshore Energy - General | Tagged bid rejections, Lease Sale 259, Lease Sale 261 | Leave a Comment »

The active rig count in the GoM in 2001 was 148 (AL-4, LA-119, TX-25), which is >8 times the current Baker Hughes rig count of 18. The 2001 rig count was not a one year blip; the number of rigs active in the GoM exceeded 100 for the ten year period from 1994-2003.

While the current rig count is anemic by comparison, the capabilities of the fleet are anything but. Below is a list derived from drilling contractor status reports of deepwater rigs now operating in the Gulf.

All of these rigs are dynamically positioned and are capable of drilling in 12,000′ of water. They have dual derricks and 15,000 psi rated BOP rams (one has a 20,000 psi stack, and another can be upgraded to 20,000 psi). The annular preventers are rated at 10,000 psi. All have impressive storage and hook load capacities, the latest tubular handling equipment, advanced control systems, and efficient power generation.

Note that most of the rigs fly the flag of the Marshall Islands. This “flag of convenience” registration is preferred for reasons related to taxation and operational freedom. For the record, the fact that the Deepwater Horizon was registered in the Marshall Islands had little to do with the Macondo blowout. The DWH was subject to all Coast Guard and MMS regulations under the OCS Lands Act.

The main cause of the Macondo blowout was the poorly planned and executed well suspension operation. Certain equipment capability, maintenance, and employee training issues were contributing factors. However, with that said, the Marshall Islands report on the blowout candidly acknowledges that “the complexity of and interdependence between the drilling and marine systems and personnel suggests a need for increased communication and coordination between the flag State and coastal State drilling regulators.” Hopefully, that coordination is being achieved and the risks associated with the fragmented regulation of mobile drilling units are being effectively managed.

| Contractor | Rig | Operator | Est. end date | Flag |

| Transocean | Deepwater Titan | Chevron | 3/2028 | Marshall Islands |

| Transocean | Deepwater Atlas | Beacon | 4/2025 | Marshall Islands |

| Transocean | Deepwater Poseidon | Shell | 4/2028 | Marshall Islands |

| Transocean | Deepwater Pontus | Shell | 10/2027 | Marshall Islands |

| Transocean | Deepwater Conqueror | Chevron | 3/2025 | Marshall Islands |

| Transocean | Deepwater Proteus | Shell | 5/2026 | Marshall Islands |

| Transocean | Deepwater Thalassa | Shell | 2/2026 | Marshall Islands |

| Transocean | Deepwater Asgard | Hess | 4/2024 | Marshall Islands |

| Stena | Evolution | Shell | 4/2029 | Marshall Islands |

| Noble | Stanley Lafosse | ??? | 11/2024 | Liberia |

| Noble | Valiant | LLOG | 2/2025 | Marshall Islands |

| Noble | Globetrotter I | Shell | 5/2024 | Liberia |

| Noble | Globetrotter II | Shell | 5/2024 | Liberia |

| Valaris | DS-18 | Chevron | 8/2025 | Marshall Islands |

| Valaris | DS-16 | Oxy | 6/2026 | Marshall Islands |

| Diamond Offshore | BlackHawk | Oxy | 10/2024 | Marshall Islands |

| Diamond Offshore | BlackHornet | bp | 3/2027 | Marshall Islands |

| Diamond Offshore | BlackLion | bp | 9/2026 | Marshall Islands |

Short video about the Stena Evolution, the newest entry to the Gulf of Mexico fleet:

Posted in drilling, Gulf of Mexico, Offshore Energy - General | Tagged 2024 vs. 2001, deepwater rig capabilities, Diamond Offshore, Gulf of Mexico drilling, macondo, Marshall Islands, Noble Corp., regulatory fragmentation, rig counts, Stena, transocean, Valaris | Leave a Comment »

After 5 months of investigation, the Main Pass Oil Gathering (MPOG) system has finally been cleared for production. (The Coast Guard update only says that the pipeline passed the integrity test, but I assume the operators may resume production though the MPOG system.)

Only a small connector leak that was previously reported was identified during the extensive integrity testing. The Coast Guard had advised that the connector leak was not the source of the large sheen that was observed in November.

So what was the source of the November sheen and what was the basis for the 1.1 million gallon spill volume estimate? The sheen was not indicative of a spill of that magnitude. Did the Coast Guard et al assume a worst case loss from the MPOG system, even though no leak had been identified?

Is this the most oversight ever for a pipeline integrity test?

The removal and replacement of the spool piece and the subsequent integrity test of the MPOG line were conducted under the close supervision of the Unified Command and Pipeline and Hazardous Materials Safety Administration. During both operations, spill response vessels were on site, along with divers, remotely operated vehicles, helicopters equipped with trained oil observers and multi-spectral imaging cameras, and other containment and recovery equipment. No material discharge of oil was observed during these operations.

Unified Command

The NTSB has the lead in the investigation into the source of the sheen. Don’t expect any findings soon.

Posted in Gulf of Mexico, Offshore Energy - General, oil spill response, pipelines | Tagged Coast Guard, Main Pass Oil Gathering, MPOG, NTSB, pipeline leak, sheen, unified command | Leave a Comment »

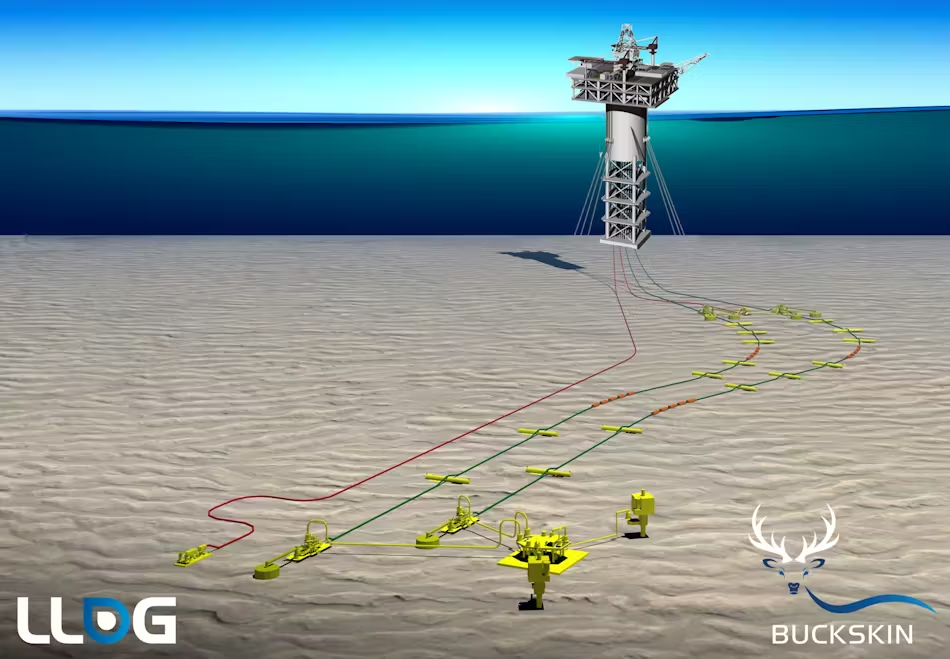

Houston, TX, March 29, 2024. Beacon Offshore Energy LLC (“Beacon”) announced today the completion of the divestment of its non-operated interests in certain fields in the deepwater Gulf of Mexico in accordance with a previously executed definitive agreement with GOM 1 Holdings Inc., an affiliate of O.G. Oil & Gas Limited. The divestment includes Beacon’s 18.7% interest in the Buckskin producing field, 17% interest in the Leon development, 16.15% interest in the Castile development, 0.5% interest in the Salamanca FPS/lateral infrastructure, and 32.83% interest in the Sicily discovery.

Beacon

According to BOEM records, GOM 1 HOLDINGS INC, a Delaware company, registered with BOEM effective 3/15/2024. The parent entity, O.G. Oil & Gas Limited, is a privately held E&P company incorporated in 2017 and based in Singapore.

O.G. Oil & Gas Ltd is part of the Ofer Global Group, “a private portfolio of international businesses active in maritime shipping, real estate and hotels, technology, banking, energy and large public investments.”

After a partial takeover by O.G Oil & Gas Limited in 2018, New Zealand Oil and Gas is now 70% owned by the Ofer Global Group. Among other interests, NZ Oil and Gas produces from fields offshore Taranaki, NZ.

Because they are jointly and severally liable for safe operations and decommissioning, minority investors should take a strong interest in safety management and financial assurance. Investors should remember that partners are adversely affected by the mistakes of the operating company. Anadarko and Mitsubishi took a hit following the Macondo blowout. To what extent had they been monitoring bp’s risk and safety management programs for drilling operations?

Posted in decommissioning, energy policy, Gulf of Mexico, Offshore Energy - General, Regulation, well control incidents | Tagged Beacon Offshore, GOM 1 Holdings, joint and several liability, macondo, New Zealand Oil and Gas, O.G. Oil & Gas Ltd, Ofer Global Group | Leave a Comment »

… and you deniers are fully responsible. There’s a reason why Texas is the most affected state 😉

But fear not, we will line our shores with wind turbines, restrict offshore oil and gas leasing, and subsidize carbon disposal in the Gulf of Mexico. All of this “help” will have a negligible effect on the climate, which will continue to change as it always has and always will.

Posted in climate, energy policy, Gulf of Mexico, Offshore Energy - General, Wind Energy | Tagged climate change, deniers, Offshore Wind, solar eclipse, Texas | Leave a Comment »

As we wait for the International Chamber of Commerce (ICC) arbitration panel to rule on the Exxon-CNOOC-Chevron-Hess Stabroek dispute, key excerpts from Chevron’s SEC filing about their merger with Hess are pasted below. The text highlighted in red is particularly interesting.

If the ICC arbitration panel rules that the right-of-first-refusal (ROFR) provision applies, the Chevron filing says that the merger is off and Hess continues as Stabroek’s 30% owner. If that statement is correct, Exxon and CNOOC cannot obtain the Hess share. Their only benefit from the challenge would be to deny their rival Chevron from participating in the block or to receive payment from Chevron for approving the ownership change.

It’s also noteworthy that Exxon initially showed support for the deal (quote below).

Excerpts from Chevron’s SEC filing:

p. 32: With respect to the Stabroek ROFR (as defined in the section entitled “The Merger—Stabroek JOA”), if the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close. Some of these conditions are not in Hess’ or Chevron’s control.

Further, subject to any then ongoing arbitration relating to the Stabroek JOA, either Chevron or Hess may terminate the merger agreement if the merger has not been completed by October 22, 2024, (or April 22, 2025 or October 22, 2025, if the applicable end date is extended pursuant to the merger agreement) or by such later date as the parties may mutually agree.

p. 81: The Stabroek JOA contains a right of first refusal (the “Stabroek ROFR”) provision that, if applicable to a change of control transaction and properly exercised, provides the Stabroek Parties with a right to acquire the participating interest in the Stabroek Block held by the Stabroek Party subject to such transaction (at a value that is based on the portion of the value of the change of control transaction that reasonably should be allocated to such participating interest and is increased to reflect a tax gross-up) only after, and conditioned on, the closing of such transaction.

Chevron and Hess believe that the Stabroek ROFR does not apply to the merger due to the structure of the merger and the language of the Stabroek ROFR provisions.

p. 82: On October 24, 2023, shortly after the merger was announced, Exxon issued the following statement, indicating its support for the merger:

“Hess has been a valued partner in Guyana since 2014 and we look forward to continuing our successful operations in the Stabroek block with Chevron, pending the deal closing.”

However, Exxon and CNOOC subsequently informed Chevron and Hess that they believe the Stabroek ROFR applies to the merger. Hess, Chevron, Exxon and CNOOC subsequently engaged in discussions regarding the applicability of the Stabroek ROFR to the merger.

If the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close, and, pursuant to the terms of the Stabroek JOA, the Exxon affiliate and the CNOOC affiliate would cease to have rights under the Stabroek ROFR with respect to the merger. In that event, Hess would remain an independent public company and would continue to own its participating interest in the Stabroek Block. Based on the express terms of the Stabroek JOA, Chevron and Hess do not believe there is any material likelihood that the circumstances described in this paragraph will occur.

p. 118: In addition, with respect to the Stabroek ROFR, if the arbitration does not result in a confirmation that the Stabroek ROFR does not apply to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close.

Posted in Guyana, Offshore Energy - General | Tagged Chevron, CNOOC, Exxon, Guyana, Hess, ICC, SEC filing, Stabroek Block | Leave a Comment »

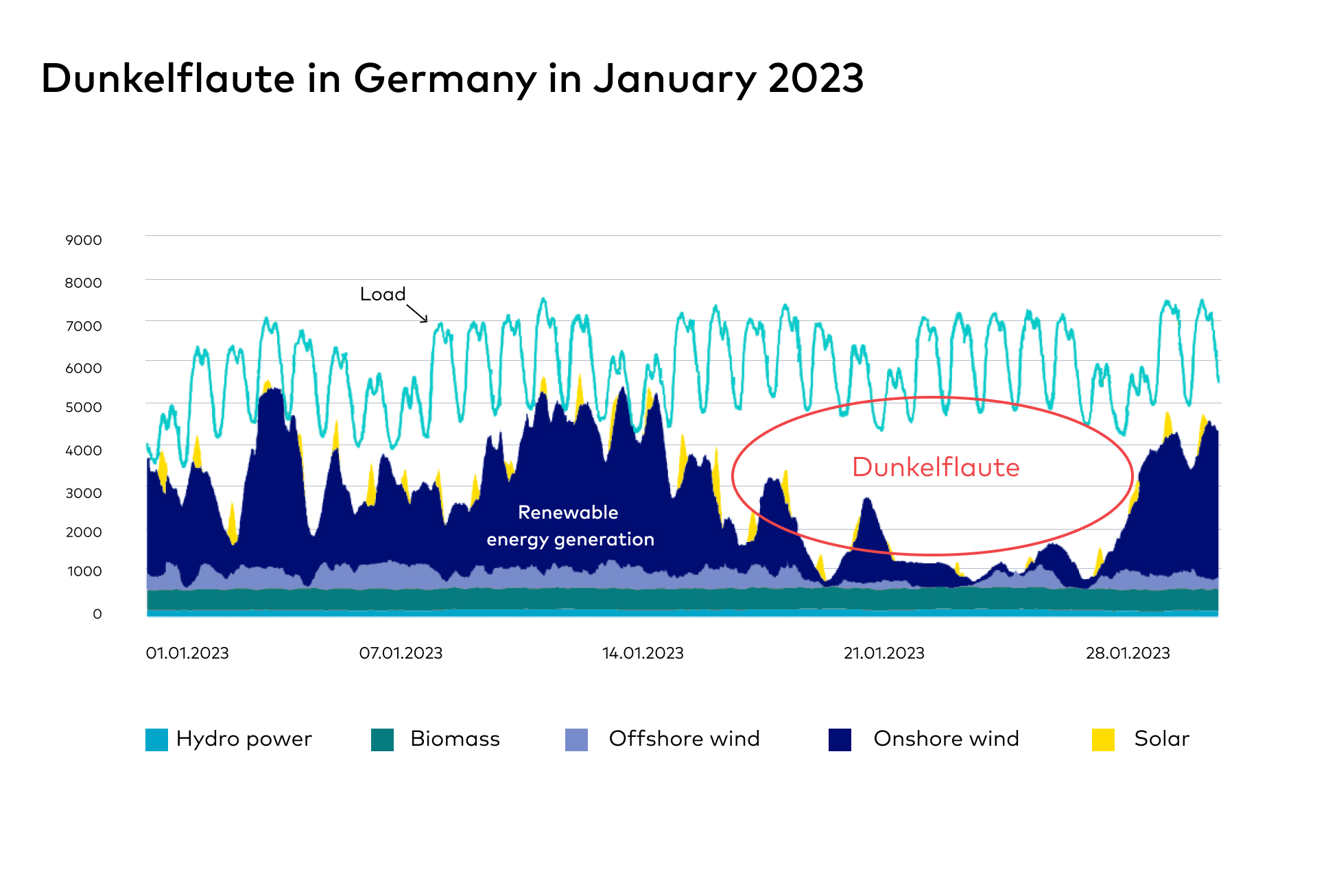

Add Dunkelflaute to the list of interesting and expressive compound German words. Die Dunkelflaute is a dark lull, a period of time in which minimal energy can be generated by the sun or wind. More specifically in German:

Die Dunkelflaute als sogenanntes Kofferwort beschreibt das gleichzeitige Auftreten von Dunkelheit und Windflaute. Diese Wetterlage entsteht typischerweise im Winter und sorgt für geringe Erträge aus Solar- und Windenergie bei gleichzeitig saisonal hohem Strombedarf. Eine Dunkelflaute kann mehrere Tage andauern. Kommen zu Dunkelheit und Windflaute noch niedrige Temperaturen hinzu, die für gewöhnlich den Strombedarf weiter ansteigen lassen, spricht man auch von “kalter Dunkelflaute.”

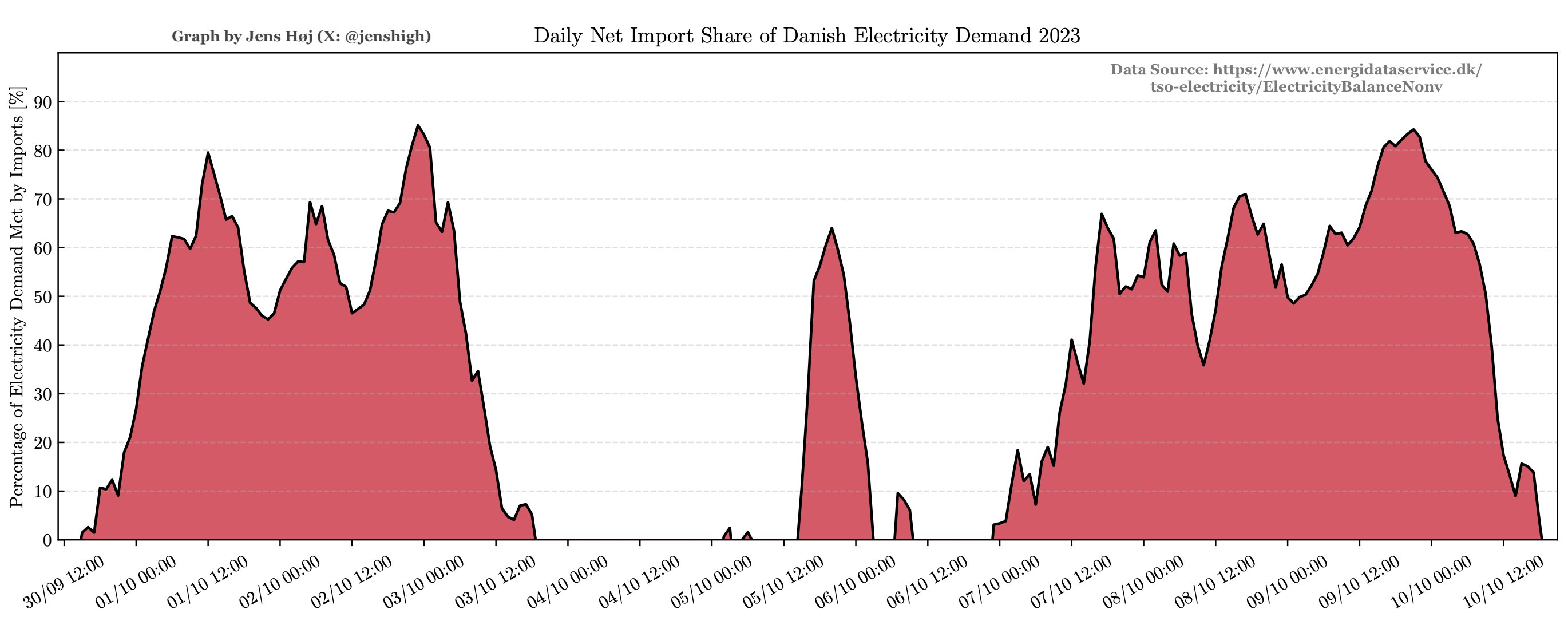

Note the prolonged Dunkelflaute (below) during which renewables provided minimal power in the middle of winter.

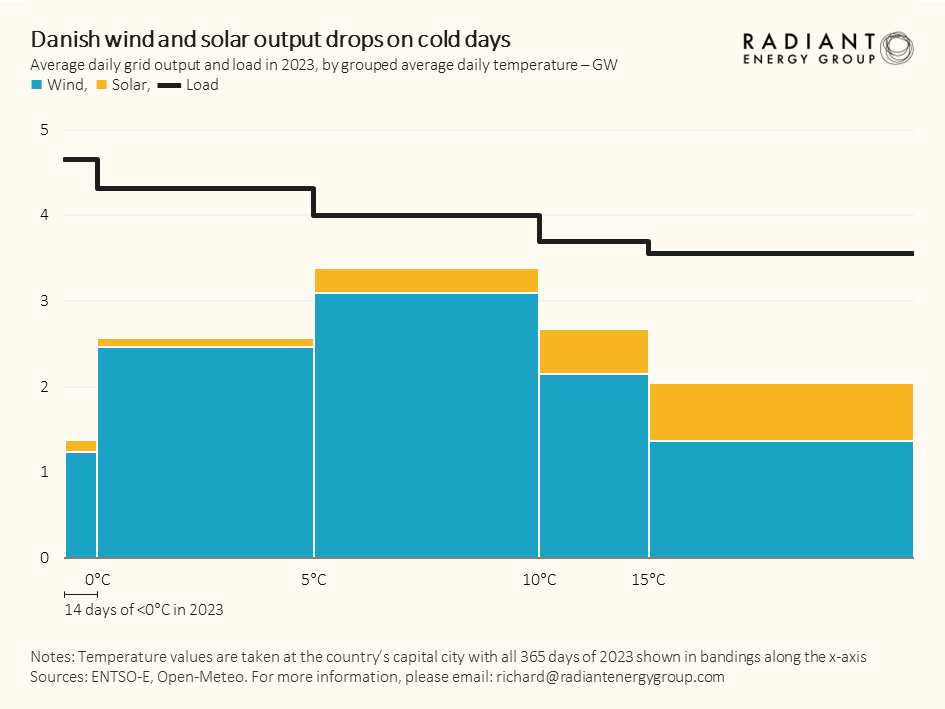

Unsurprisingly, wind and solar output are the lowest when the temperatures are the coldest. See the Danish summary for 2023 below. Note that wind output was also low when temperatures were above 15 deg. C.

Regional wind energy grids are not always an effective solution as Danish physicist Jens Christiansen, a nuclear energy advocate, has illustrated:

‘The wind always blows somewhere.’ Is that really true though? Here I’ve looked at the capacity factors of wind from five northern European countries in August The winds seem highly correlated, and there is almost a week-long period without significant wind anywhere.

Christiansen illustrates Denmark’s reliance on imported electricity:

Paraphrasing Margaret Thatcher: “The problem with electricity imports is that you eventually run out of other people’s electricity.” In the U.S., California imports more electricity than any other state and typically receives between one-fifth and one-third of its electricity supply from outside of the state.

Given that massive battery storage is well beyond current capabilities and restrictions on electricity consumption and economic growth are undesirable, redundant or complementary power sources are essential for a reliable grid. Natural gas power generation is most responsive to variable demand, and is thus a good complement to variable sources like wind turbines and solar panels.

Posted in climate, energy policy, natural gas, Wind Energy | Tagged Denmark power grid, dunkelflaute, Jens Christiansen, kryptonite, natural gas, wind and solar power | Leave a Comment »

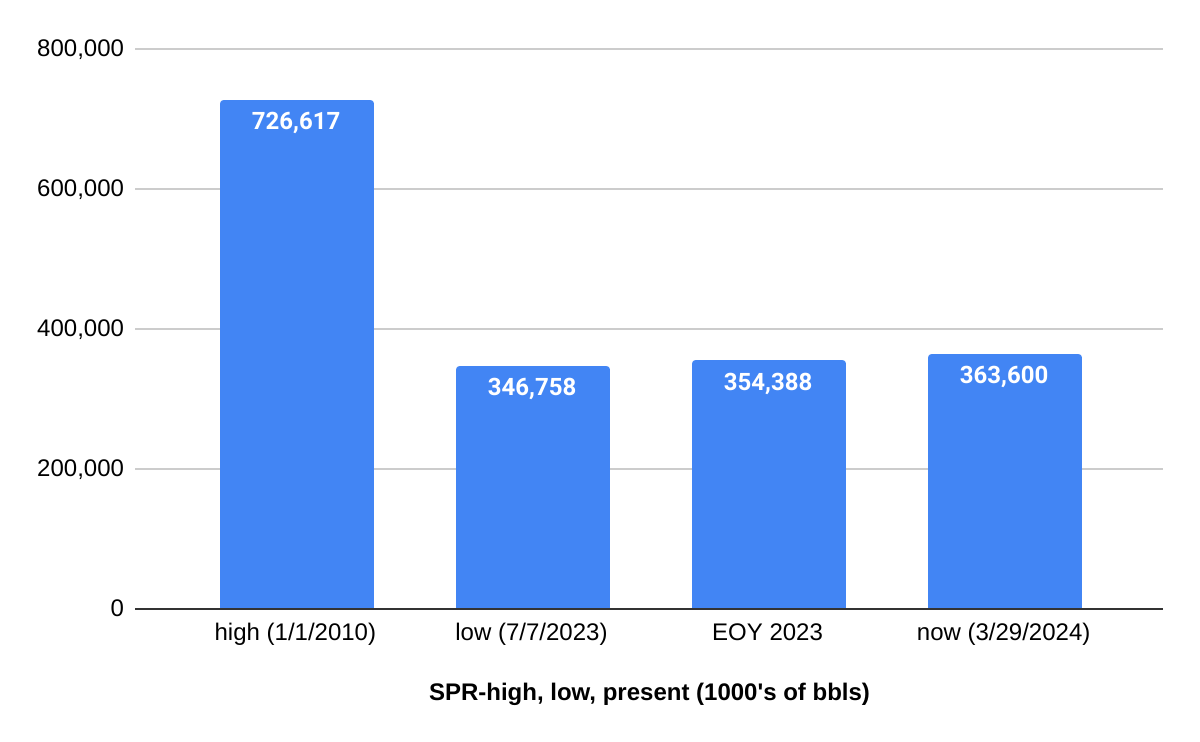

After announcing that the planned 40 million barrel SPR refill would be the equivalent of the massive 180 million barrel withdrawal, DOE has halted the refill at < half the planned amount. There is no end in sight for the SPR deficit (chart below).

Citing rising oil prices, the DOE said, “We will not award the current solicitations for the Bayou Choctaw SPR site and will solicit available capacity as market conditions allow.” Three million barrels of oil had been slated for delivery to the Bayou Choctaw SPR site in August and September.

Forbes

Posted in energy policy | Tagged DOE, SPR deficit, SPR refill, Strategic Petroleum Reserve | Leave a Comment »

14 of the high bids at Gulf of Mexico Lease Sale 259 were rejected. Did those tracts receive bids at sale 261? What was the net gain or loss of revenue? See the summary bullets and table below

For a net bonus revenue gain to date of only 1/4 of one per cent, 8 of the 14 sale 259 tracts with rejected high bids remain closed to exploration. The timing of any future sales is very much in doubt given the minimalist 5 year leasing plan and the associated legal challenges.

Current bid evaluation practices only make sense if regular lease sales are held on a predictable schedule, as has historically been the case.

Meanwhile, 100% of the improper CCS bids (199/199) were accepted at the last 3 oil and gas lease sales.

| area and block | Sale 259 rejected high bid – company | Sale 261 high bid | bid accepted | govt gain (loss*) |

| DC 622 | 2,101,836 – Shell | 615,628 – Shell | yes | (1,486,208) |

| GC 173 | 307,107 – Woodside | no bid | NA | (307,107) |

| GC 547 | 1,783,498 – Chevron | no bid | NA | (1,783,498) |

| GC 591 | 1,291,993 – Chevron | no bid | NA | (1,291,993) |

| GC 642 | 605,505 – Anadarko | no bid | NA | (605,505) |

| GC 777 | 583,103 – bp | no bid | NA | (583,103) |

| AT 5 | 1,551,130 – Anadarko | 5,215,628 – Shell | yes | 3,664,498 |

| AT 133 | 607,107 – Woodside | no bid | NA | (607,107) |

| KC 745 | 707,777 – Beacon | 2,422,222 – Beacon | no | (2,422,222) |

| KC 789 | 707,777 – Beacon | 2,143,299 – Beacon | no | (2,143,299) |

| WR 794 | 724,744 – Beacon | 1,487,624 – Beacon | yes | 762,880 |

| WR 795 | 774,242 – Beacon | 5,301,107 – Woodside | yes | 4,526,865 |

| WR 796 | 774,242 – Beacon | 3,310,107 – Woodside | yes | 2,535,865 |

| WR 750 | 724,744 – Beacon | 1,498,555 – Beacon | yes | 773,811 |

| total govt. gain | 1,032,877 |

Posted in CCS, energy policy, Gulf of Mexico, Offshore Energy - General | Tagged 5 year leasing plan, bid rejections, Gulf of Mexico, Lease Sale 259, Lease Sale 261, revenue gain | Leave a Comment »