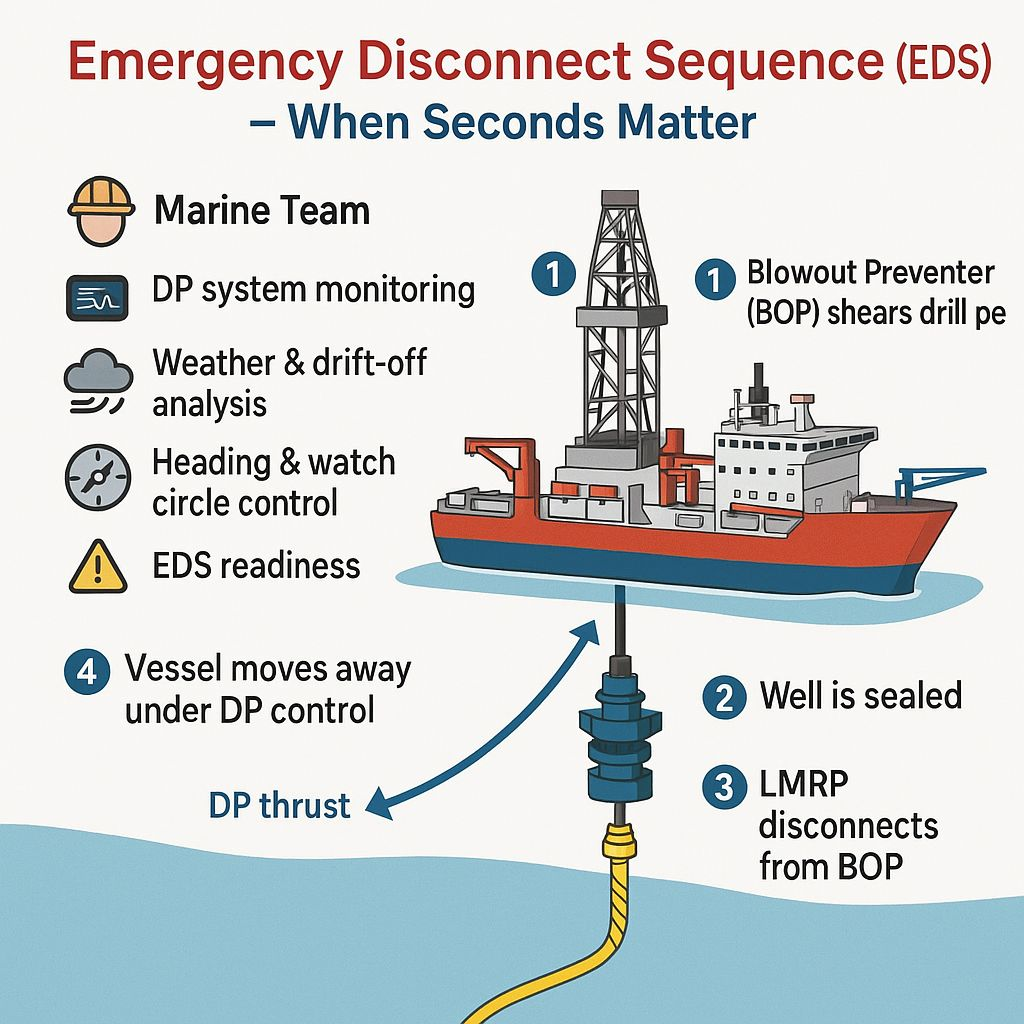

Seconds matter – training, equipment maintenance, and effective leadership are critical!

Several BSEE Safety Alerts have just been released. Of particular importance to those interested in deepwater drilling is the attached alert describing two separate Emergency Disconnect Sequence (EDS) incidents.

The EDS (see the diagram above) is a critically important safety protocol that ensures that a well is sealed and the riser and rig are disconnected from the blowout preventer in the event of a well control emergency, unforeseen weather/ocean conditions, loss of power, or positioning system malfunction. Note that the Macondo blowout could have been prevented if the Deepwater Horizon crew had activated the EDS in a timely manner.

The two EDS events cited in the Safety Alert were presumably the March 28, 2025 and March 5, 2024 incidents investigated by BSEE district offices. The drillships were the Stanley Lafosse and the Deepwater Poseidon The investigation reports provide detailed information on these incidents.

Unintended riser disconnects not associated with EDS activations are a related safety and pollution concern that necessitated the issuance of a 2000 Notices to Lessees that was subsequently updated:

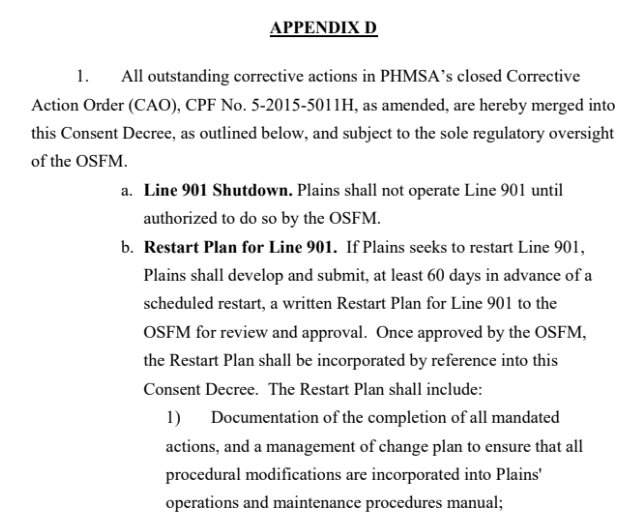

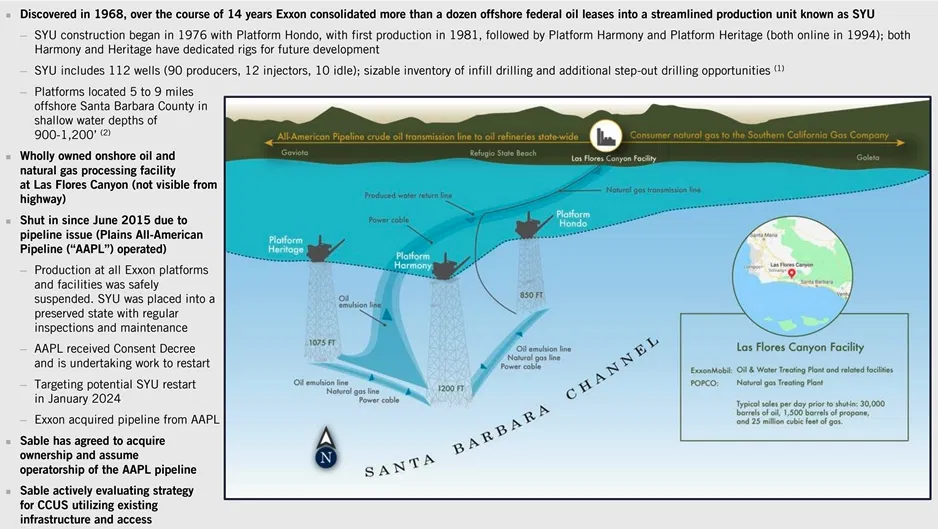

Sable Offshore is attempting to restart the same pipeline that caused the Refugio Oil Spill in 2015. | Credit: Paul Wellman File Photo

Sable Offshore oil believes the federal Pipeline and Hazardous Materials Safety Administration (PHMSA) , not the California Fire Marshal, should have jurisdiction over the company’s onshore pipeline.

I once had the same opinion as Sable. Their pipeline is, by definition, an interstate line because it carries OCS production. Then I read Appendix D of the court approved Consent Decree that was executed following the 2015 Refugio pipeline spill. That Decree is quite clear regarding regulatory jurisdiction, and would have to be overturned to transfer authority to PHMSA.

The full Consent Decree is attached. Pasted below is an excerpt from Appendix D:

The Town of Nantucket’s attorney, Greg Werkheiser of Cultural Heritage Partners, told The Light last month that “it’s taken far too long” to get a final report on the blade failure.

On my favorite holiday, I’m sending best wishes to BOE readers of all persuasions. Offshore energy issues can be divisive, even among friends, and I’m grateful for the opportunity to share information and opinions.

My wife and I will be spending Thanksgiving with my daughter’s family including our 6 grandchildren, none of whom have expressed interest in being offshore safety regulators (no higher calling 😉).

Belated holiday wishes to our friends in Canada where Thanksgiving is celebrated in October, and cheers to those living where a similar fall holiday is observed.

To date, BSEE has used carryover funds and offsetting collections from inspection, rental, and cost recovery fees to continue their priority permitting and inspection programs during the govt shutdown. However, these funds are limited.

At some point, BSEE will have to stop issuing new permits. If the shutdown continues, the next step could be to curtail drilling and production operations. Needless to say, this would not be completely unacceptable.

In the meantime, BSEE employees continue to work without pay. Flying offshore everyday to inspect operations is no picnic and can be hazardous. I lost a colleague in a helicopter crash and others have been injured. It’s shameful that these people are not being paid while members of congress are!

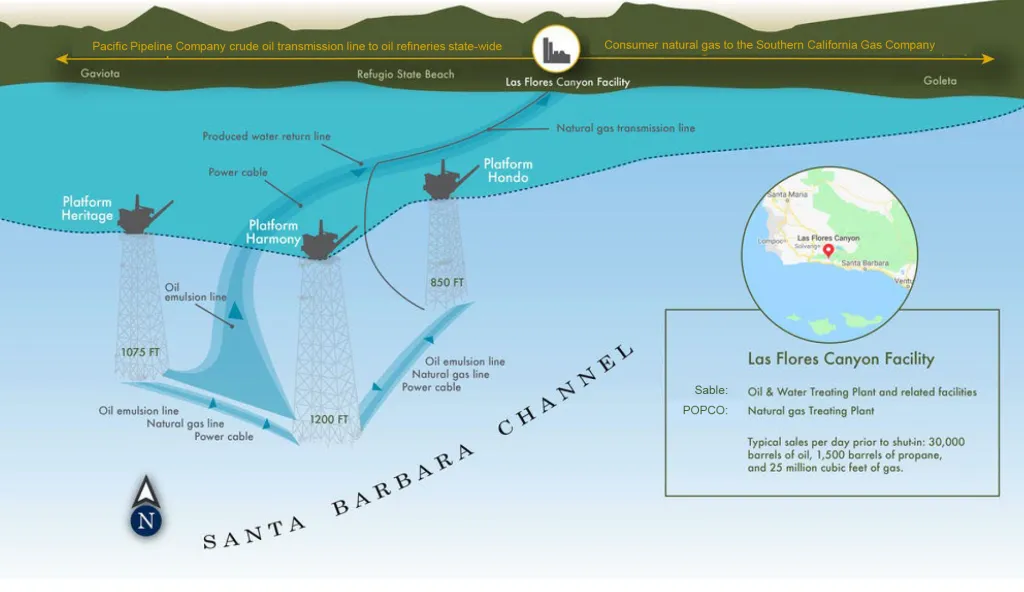

Attached is John Smith’s comprehensive summary of lawsuits related to Sable Offshore’s attempts to restart Santa Ynez Unit production.

If you are keeping score, there are 10 separate cases including a class action lawsuit filed by investors. New legal battles are sure to follow given Sable’s OS&T strategy. Per John:

“The combined legal challenges, injunctions, and restraining orders have significantly delayed Sable’s restart plans and prompted the company to pursue an Offshore Storage and Treatment Vessel (OS&T) strategy, which was utilized to process SYU production in federal waters from 1981 – 1994, and transport oil to markets using tankers.“

Attached is a court filing challenging Delaware’s approval of the Coastal Construction Plan for that project. Some interesting points from the filing:

Maryland local governments declined to allow the transmission lines from the Maryland Offshore Wind Project to come ashore in their jurisdictions.

The Governor of Delaware agreed to allow the transmission lines to make landfall at the Delaware Seashore State Park.

The transmission pipelines would then traverse the adjacent Delaware Bays, to an inland substation, from which the power would be sent to Maryland.

US Wind applied for a number of permits from the Delaware Department of Natural Resources (DNREC) specific to horizontal directional drilling, laying cable pipelines, and other coastal construction activity.

The approval process, including provisions for public input, was not consistent with State regulations.

The Secretary’s decision to issue the beach construction permit is supported virtually exclusively by documents which were submitted by US Wind after the close of public comment.

Decommissioning and financial assurance information, a favorite BOE topic for both wind and oil/gas, was submitted after the close of the public record.

John notes that Exxon’s March 26 contractual deadline for Sable to have the SYU up and running is fast approaching. What will Exxon do in the likely event that Sable fails to meet that deadline? Does Exxon want to re-enter the SYU legal and regulatory quagmire?

The SYU’s 500+ million barrels of oil, 3 deepwater platforms, and onshore processing facilities are an enormous prize, but is that prize attainable?

Meanwhile, the latest skirmish between Sable and the Office of the State Fire Marshal (OFSM) pertains to metal loss anomalies and inspection tool tolerances. The dispute is summarized in the linked filing.

Sable contends that the Fire Marshal’s letter contradicts guidance from OSFM staff and provides examples. Sable goes a step further at the end of their response by calling for the FIre Marshal to coordinate better with the experts on his staff:

“We respectfully request that, given this background, you coordinate further with the expert team at OSFM and revisit the statements in your October 22nd letter.”

It’s not looking good for a quick resolution of these issues.

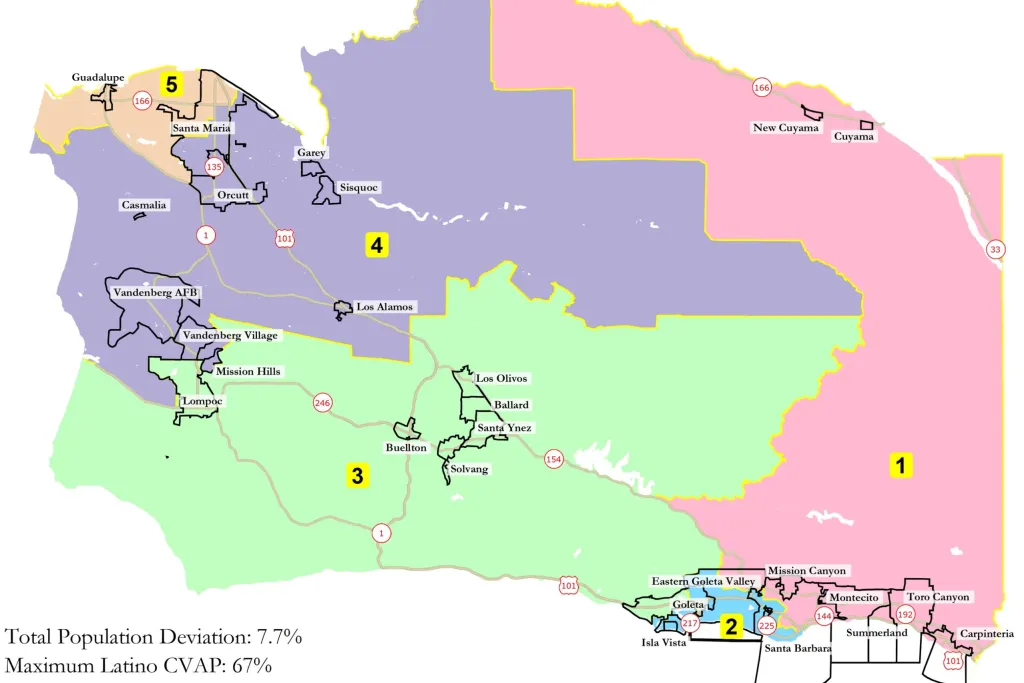

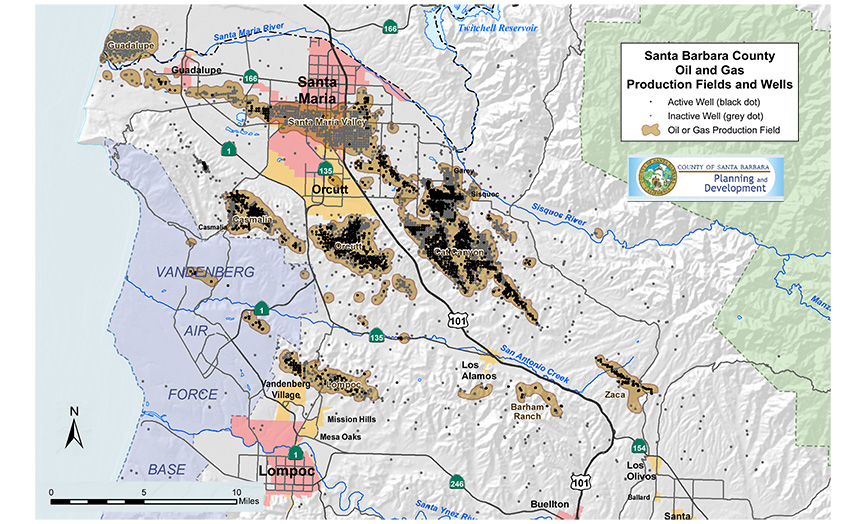

In essence, the 3 Supervisors from South County (Districts 1-3) voted to euthanize an industry that is largely in North County (Districts 4 and 5). Those 3 supervisors, not the marketplace, are terminating a historically important industry. See the maps below.

District BoundariesOil Wells

Supervisors Laura Capps of the Second District, Joan Hartmann of the Third District and Roy Lee of the First District voted for the ordinance.

Ah, but it’s the industry’s fault according to Supervisor Hartmann. She asserted that companies have known since the 1950s about the dangers of climate change, and could have led the way to be part of the solution. How dare they respond to market forces instead of climate ideologues!

Of course, this is the same three vote coalition that is aligned with the Coastal Commission in opposition to the restart of the Santa Ynez Unit, which would benefit the County significantly.

Finally, note that the three supervisors voting for the ordinance represent the districts with the highest income levels and lowest poverty rates. Those opposing the ordinance represent the districts that will be most affected, and have the lowest income levels and highest poverty rates. (See the table below; Information courtesy of Grok AI.)

District

Approx. Median Household Income (2022)

Key Areas Included

Notes

1

$120,000–$140,000

Carpinteria, Summerland, Montecito, parts of Santa Barbara

Affluent coastal communities; high home values (~$1.5M+ median)

2

$95,000–$115,000

Santa Barbara city, Goleta, Isla Vista

Mix of urban professionals, students, and tech; university influence lowers median slightly.

3

$80,000-$95,000

Santa Ynez Valley, Buellton, Solvang, Lompoc

Rural/agricultural with tourism; moderate incomes from wine industry and military base

4

$70,000–$85,000

Lompoc, Vandenberg area, parts of Santa Maria

industrial and defense-related; higher poverty rates (~15–20%).

5

$60,000–$75,000

Santa Maria, Guadalupe

Agricultural North County; majority Latino population; lowest incomes due to farm labor.

Poverty rates: ~8–10% in Districts 1–2 vs. 18–25% in Districts 4–5

Interesting case: Delaware litigation on approval of the Coastal Construction Permit for the Maryland Offshore Wind Project

Posted in decommissioning, energy policy, Offshore Wind, Regulation, tagged Coastal Construction Plan, court filing, decommissioning, Delaware litigation, Maryland Offshore Wind, public comment, US Wind on October 29, 2025| Leave a Comment »

The Dept. of the Interior is currently reconsidering approval of the Construction and Operations Plan for the Maryland Offshore Wind Project (US Wind).

Attached is a court filing challenging Delaware’s approval of the Coastal Construction Plan for that project. Some interesting points from the filing:

Read Full Post »