EIA reports October production of 1.959 million bopd. September production was revised down from 2.000 to 1.999 million bopd, a very slight but symbolically significant change. Foul play? 😉

“It’s great that the federal government finally has a loose game plan for getting oil companies to clean up their rusty messes,” said Miyoko Sakashita, oceans program director at the Center for Biological Diversity.

Complete removal may be the most politically expedient alternative in California, but it is by far the most environmentally damaging and poses the greatest safety risks. Old disputes about offshore oil and gas production should not be driving decommissioning policy.

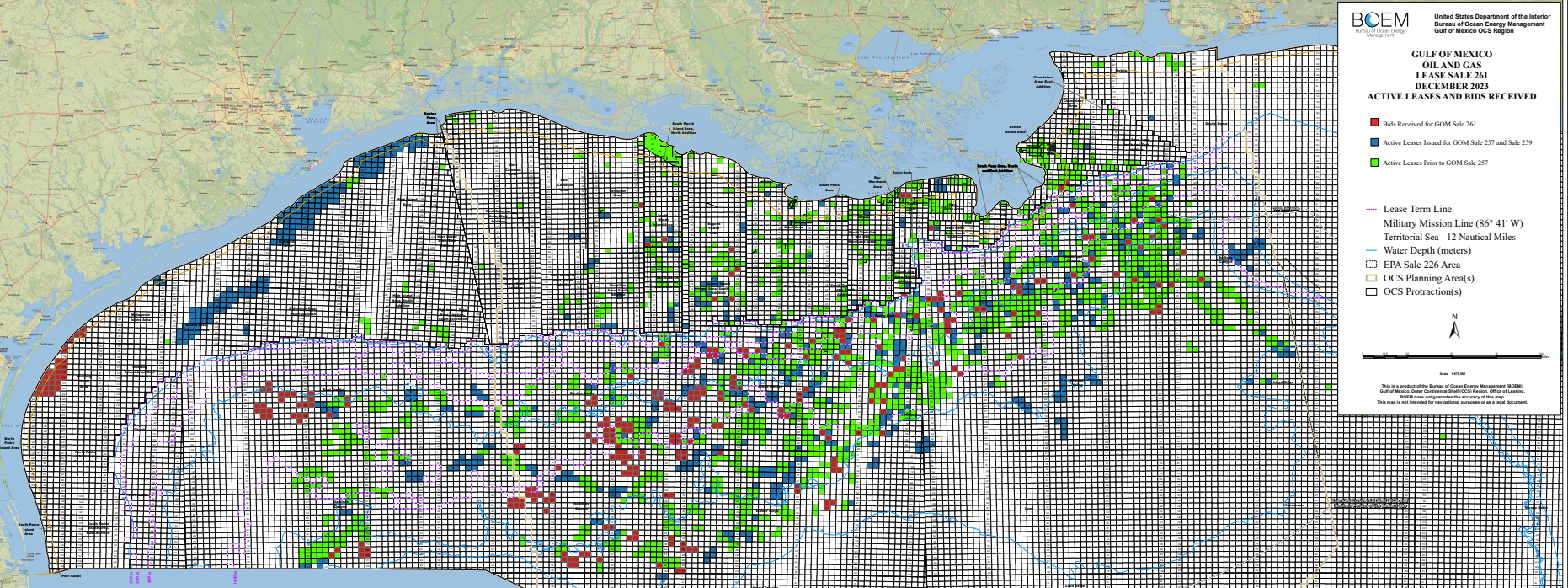

Biggest prize at the holiday party went to Anadarko: Mississippi Canyon 389 – 5 bids, $25.5 million high bid

Biggest holiday shopping spree: Shell’s 65 high bids accounted for 24% of the sale’s high bids (excluding CCS bids).

Big spender award: Hess – $88.3 million on only 20 high bids. Does Chevron approve? 😀

Aussie, Aussie, Aussie, Oi, Oi, Oi: Strong performance by Woodside. 18 high bids, $24.8 million

Heia Norge!: Equinor continues to shine in the GoM! 13 high bids, $20.6 million

Spirit of America award to Red Willow Offshore which is owned by the Southern Ute tribe. 22 high bids!

Deepwater independents for (energy) independence: Beacon, Murphy, LLOG, Kosmos, Talos, Houston Energy, Ridgewood, QuarterNorth, Alta Mar, CSL, CL&F, and Westlawn

Even pace wins the race: Another solid lease sale for bp – 24 high bids.

So happy together 😀: Chevron and Hess combined for 48 high bids, $114 million

Coal in their stockings? Repsol (Sale 261) and Exxon (Sales 257 and 259) made up their own rules for acquiring carbon dumping leases. Perhaps some solid carbon in their Christmas stockings would be appropriate.

Christmas in July?: A lease sale in 2024 is needed. Sometime near the 4th of July holiday would be good. It’s up to you Congress!

Holiday greetings to our friends around the world!

It’s always interesting to compare the high bids with the “runner-up” bids on the same tracts. Usually the gap is large and, as indicated in the table below, that is the case with the Sale 261 “top 10.” This tells us that bidding is independent, that tract evaluation is far from an exact science, that information and expert opinions differ, and that companies have different business and bidding strategies.

Particularly interesting in this sale were the tracts that both Hess and Chevron, its future parent, sought to acquire. Chevron and Hess bid against each other on two of the “top 10” tracts, and Hess outbid Chevron by wide margins. Will this affect post-merger relationships? 😉

In a future post, we’ll look at the 14 rejected Sale 259 high bids and the bidding on these tracts in Sale 261.

26 companies participated (updated from pre-sale stats)

Strong participation by the GoM stalwarts: Shell, Chevron, Oxy/Anadarko, BP, Woodside (BHP), Equinor, Talos, LLOG, Walter, Kosmos, Beacon

Kudos to Arena, Byron, Cantium, Focus for keeping the shelf alive

Contrary to the regulations, it looks like we once again have a company seeking to acquire oil and gas leases for carbon disposal purposes. This time it’s Repsol which was the sole bidder for 36 low-value nearshore tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). At least Repsol also bid legitimately on 5 deepwater tracts.

Exxon was a complete no show, as was ConocoPhillips.

I couldn’t believe the release of the final Five Year Program as just a necessity to hold offshore wind sales. Back in 1969, Carolita Kallaur, Joan Davenport and I worked on a 5-year schedule based on the supply and demand needs of the nation. That approach, which developed into the elaborate process in the OCS Lands Act and the passage of the National Environmental Policy Act, is a thing of the past. Over.those 50 plus years, politics from both sides of the aisle always drove the changes

Alternative 1 (the preferred alternative) calls for “the complete removal of platforms, topside, conductors, the platform jackets to at least 4.6 m (15 ft) below the mud line, and the complete removal of pipelines, power cables, and other subsea infrastructure (i.e., wells, obstructions, and facilities).”

Ironically, the ROD correctly acknowledges that alternative 2 (partial removal) is environmentally preferable. So what drove the decision to select the alternative that destroys “the most productive marine habitats per unit area in the world?” Was there pressure to choose the alternative that is most punitive to an industry that is despised by California activists? If so, their schadenfreude is certain to be delayed by administrative and legal challenges that draw further attention to the social costs and environmental damage associated with “complete removal.”

The announcement boasts about “the fewest oil and gas lease sales in history” while seemingly apologizing for holding any sales at all.

Consistent with the requirements of the Inflation Reduction Act (IRA) concerning offshore conventional and renewable energy leasing, the Department of the Interior today published the final 2024–2029 National Outer Continental Shelf Oil and Gas Leasing Program (Program) with the fewest oil and gas lease sales in history.

These three lease sales are the minimum number that will enable the Interior Department’s offshore wind energy program to continue issuing leases in a way that will ensure continued progress towards the Administration’s goal of 30 gigawatts of offshore wind by 2030.

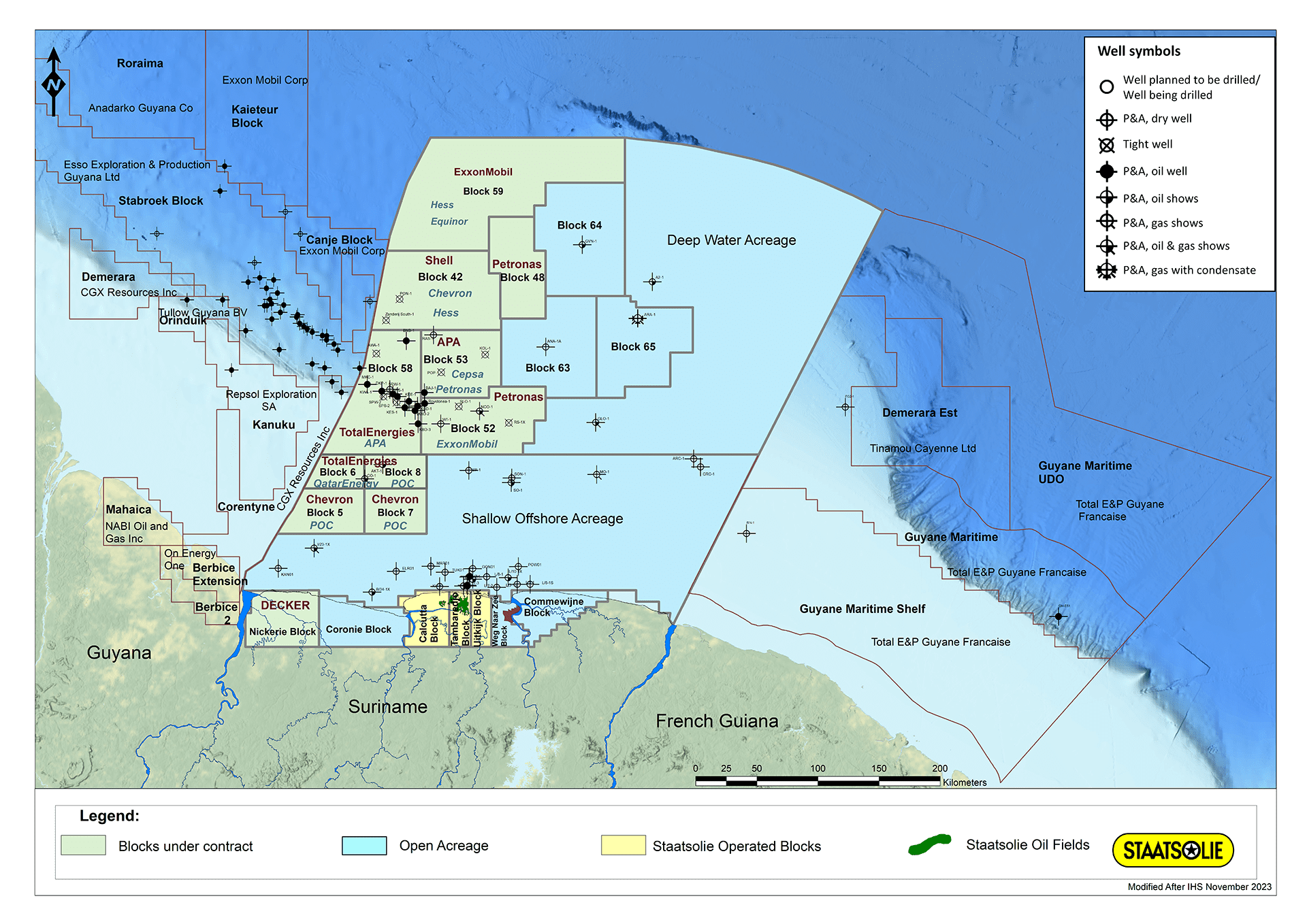

Through the PSCs, Staatsolie extends the rights for exploration, development and production to these companies. The costs and risks during the exploration period are fully covered by the latter. The exploration period consists of three phases and will last seven years. An exploration well will be drilled in both Block 64 and Block 65 in the first phase, which will last three years. In Block 63 the first exploration well follows in the second phase of the exploration period. In the event of an oil or gas discovery that is declared commercial, Staatsolie has the right to participate in all three blocks for a maximum of twenty percent from the development period