A long-time colleague is very familiar with Judge Lamberth, a Reagan appointee, and thinks highly of him. Orsted has a lease contract, and no matter where you stand on offshore wind, you have to have a compelling case to halt a project that is in the advanced stages of development. Judge Lamberth ruled that the govt doesn’t have such a case. Per the judge:

The govt presented insufficient evidence to support alleged permit noncompliance and national security concerns.

The govt acted in an “arbitrary and capricious” manner.

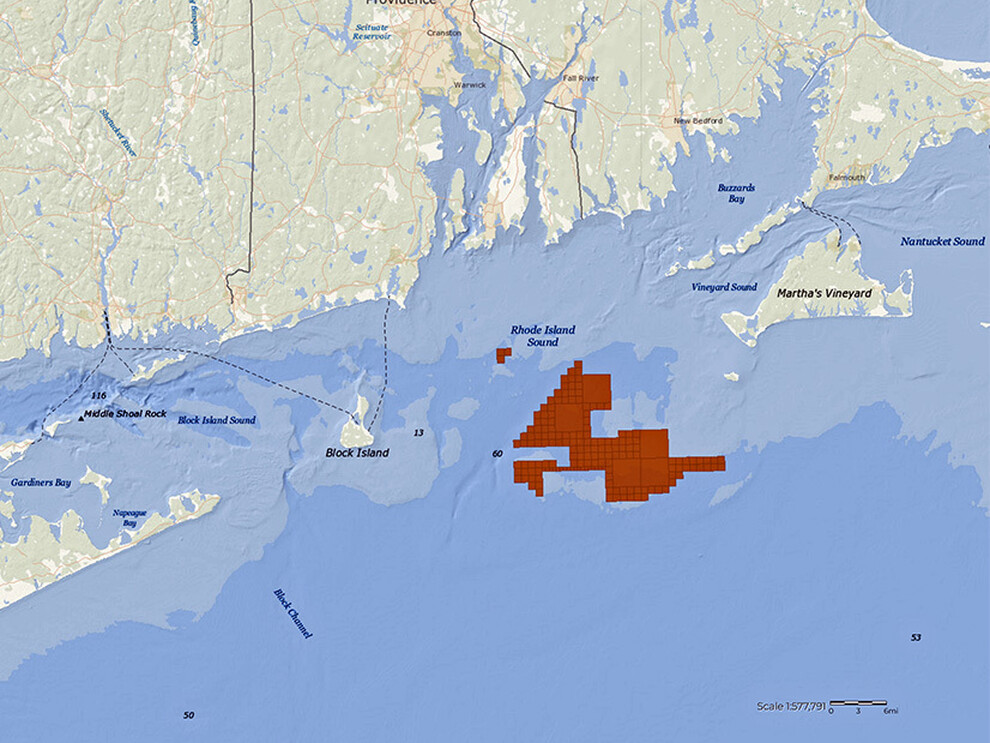

“If Revolution Wind cannot meet benchmark deadlines, the entire project could collapse.”

“There is no doubt in my mind of irreparable harm to the plaintiffs.”

Projects under development will be difficult to pause or stop. The Administration should focus on requiring sufficient decommissioning financial assurance, monitoring and mitigating project impacts, making incident data publicly available, issuing the report on the Vineyard Wind blade failure (finally!), and improving the availability of dispatchable power (i.e. natural gas and nuclear).

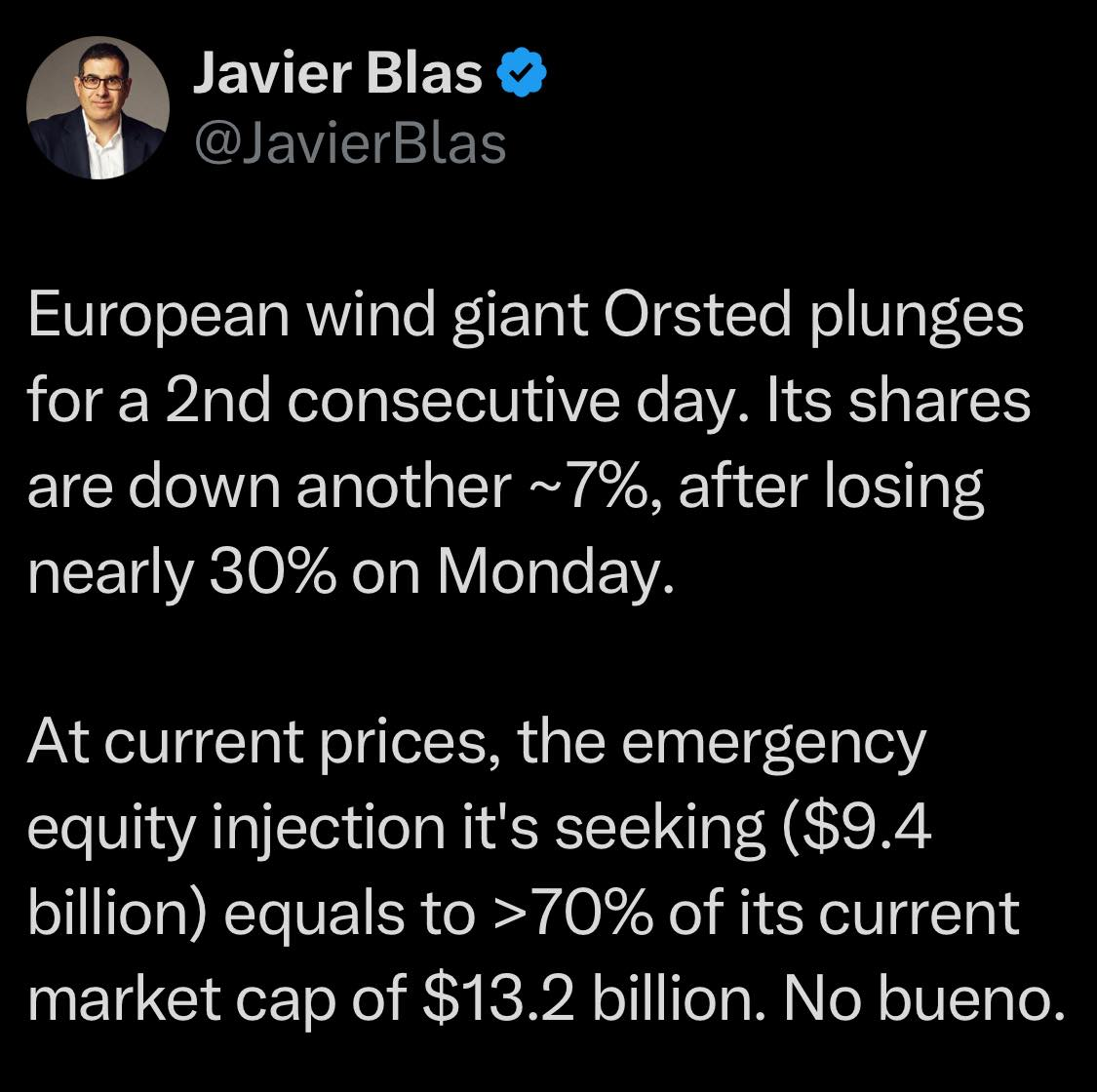

Following the announced $9 billion rights offering to shore up its finances, Orsted’s long-term issuer credit rating has been downgraded to BBB- by S&P, just one step above junk.

Ørsted’s stock price plummeted on Monday following the announcement of a $9.4 billion rights issue to fund the Sunrise Wind project. The share price has remained depressed (chart below).

Also, although Ørsted attributes its financial woes to the change in US policies, it’s apparent in the second chart (5 year trend) that the decline in Ørsted’s valuation has been ongoing since 2021.

In March, Fitch downgraded Ørsted’s rating to BBB from BBB+, and its subordinated rating to BB+ from BBB-. Further downgrades would seem to be a distinct possibility.

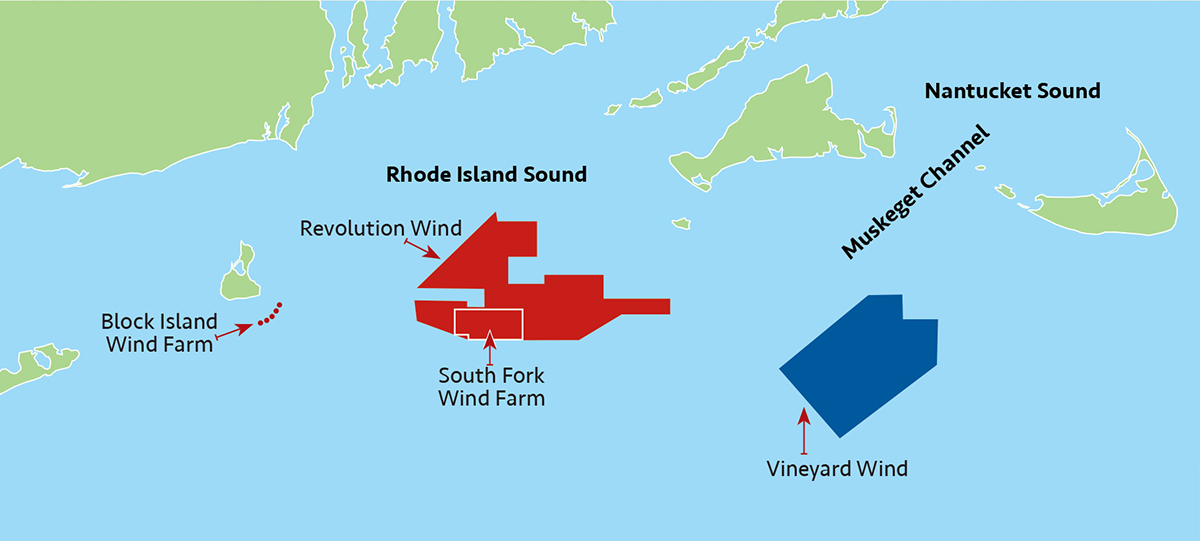

Meanwhile, decommissioning financing for the 3 Ørsted projects under construction in the US Atlantic is far from assured:

Revolution Wind:As they did for Vineyard Wind, BOEM approved Ørsted’s request to defer full decommissioning financial assurance until 15 years after the beginning of construction (see attached letter). This approval was prior to the Renewable Energy Modernization Rule (effective June 29, 2024), which eliminated the need for such waivers.

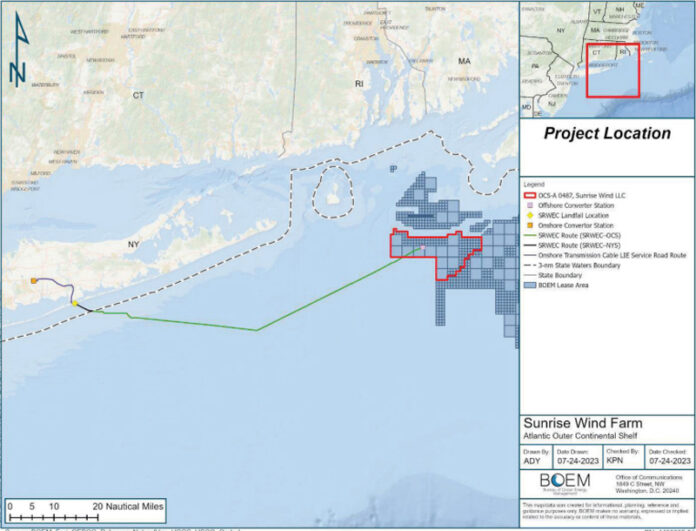

Sunrise Wind: Ørsted is now solely responsible for funding and constructing this project given the company’s failure to find investment partners. Presumably, decommissioning financial assurance was not required given BOEM’s latitude under the so-called “Modernization Rule.”

South Fork Wind: As is the case with Sunrise Wind, BOEM presumably allowed Ørsted to defer financial assurance for decommissioning as permitted by the “Modernization Rule.”

According to Ørsted, almost 70% of the turbines are installed at Revolution Wind and the first foundations have been installed at Sunrise Wind. South Fork Wind, 12 turbines and an offshore substation, is complete.

Given Ørsted’s strained finances, will BOEM now opt to require decommissioning assurance as provided for in 30 CFR § 585.517?

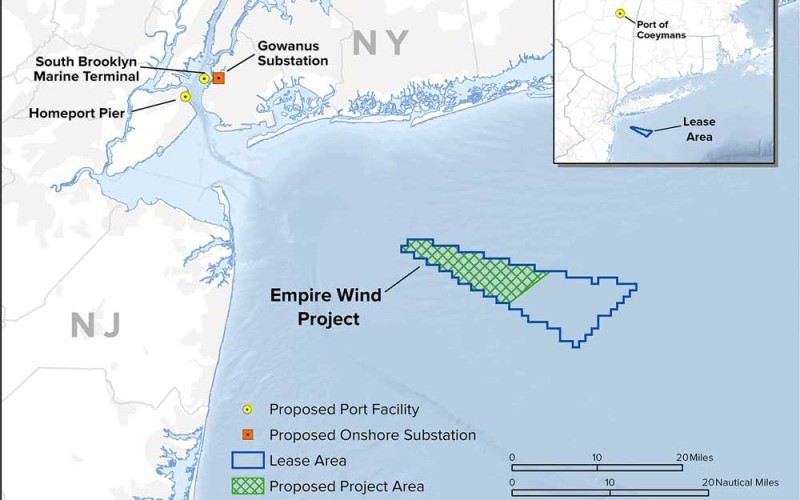

Ørsted’s situation is atypical in that the Danish government owns a majority (50.1%) stake in the company and Equinor, which is 2/3 Norwegian govt owned, holds a 9.8% stake. How will government ownership factor into BOEM decisions regarding decommissioning assurance? Note that Norwegian govt lobbying may have been one of the factors influencing the decision to allow the resumption of construction on Equinor’s Empire Wind project.

BOEM’s streamlining rule codified the deferred financial assurance option. The rule authorizes the transfer of decommissioning risks from developers to taxpayers and consumers by (1) not requiring any additional supplemental financial assurance at the Construction and Operations Plan (COP) approval stage, (2) not requiring supplemental assurance at the installation stage, and (3) providing for incremental supplemental assurance post-installation (e.g. for Vineyard Wind, the full amount is not due until 15 years after installation). See the rule’s previous and current language in the table below (emphasis added).

30 CFR 585.516 – What are the financial assurance requirements for each stage of my commercial lease?

financial assurance required before BOEM will:

language prior to 4/24/2024 “modernization” rule

current language

Approve your COP

A supplemental bond or other financial assurance, in an amount determined by BOEM based on the complexity, number, and location of all facilities involved in your planned activities and commercial operation. The supplemental financial assurance requirement is in addition to your lease-specific bond and, if applicable, the previous supplement associated with SAP approval.

There is no supplemental bond requirement at the COP approval stage.

Allow you to install facilities approved in your COP

A decommissioning bond or other financial assurance, in an amount determined by BOEM based on anticipated decommissioning costs. BOEM will allow you to provide your financial assurance for decommissioning in accordance with the number of facilities installed or being installed. BOEM must approve the schedule for providing the appropriate financial assurance coverage.

A supplemental bond or other authorized financial assurance in an amount determined by BOEM based on anticipated decommissioning costs of the proposed facilities. If you propose to incrementally fund your financial assurance instrument, BOEM must approve the schedule for providing the appropriate financial assurance.

The current financial assurance language is fuzzy enough that BOEM could deny deferred funding requests and require full financial assurance at the time facilities are installed. However, revising the language to clearly require that assurance be fully demonstrated prior to installation would provide clarity and eliminate the deferral option going forward.

The more difficult challenge may be adjusting financial assurance requirements for the projects already under construction. It’s also important to ensure that parent corporations are not shielded from decommissioning and other liability risks.

MV Times: “The recent site visit raised questions on the production of the wind farm. The Times has been able to neither verify the report independently nor confirm disparities between visuals on the ground and the Iberdrola report.”

Avangrid, an Iberdrola subsidiary and one of Vineyard Wind’s developers, reported that 17 out of 62 turbines were currently sending power to the Massachusetts grid.

The MV Times counted between five and nine turbines spinning at different points, and for different intervals, in their two hour visit.

BOE comment: Although there are many possible reasons for this discrepancy, it’s reasonable to question the absence of turbine output data. Developers assert that generator specific data are sensitive and could have market implications. However, these turbines are operating on public lands and were in part publicly funded. Output data and other performance metrics clearly have policy implications.

Note that Iberdrola “expect[s] no impact from new federal budget legislation, as it doesn’t impact 1,000 megawatts under construction.”

An MV Times photo of a Vineyard Wind substation is pasted below. These substations are large structures. Per the Construction and Operations Plan (COP) for Vineyard Wind, the topsides for a conventional electrical service platform (ESP) (also known as an offshore substation or OSS) are 45 x 70 x 38 m, which is larger in surface area than a typical 6-pile oil and gas platform (~30 x 30 m), and is comparable in size to a large jackup drilling rig.

NRW contracted with Array Petroleum to operate the former Cox Assets. Array subsequently sued NRW, asserting that NRW received $78,000,000 in revenue, but disbursed only about $48,000,000 to pay Array’s invoices and those of the subcontractor.

The court filing claimed that NRW failed to pay Array $2.5 million, the subcontractors $10.7 million, and the United States $12 million. A large share of the subcontractor costs were probably for well operations given that 21 Array workover applications were approved in 2024 and 2025. The $12 million due to the Federal government is reportedly for royalty payments. Were any revenues set aside for decommissioning liabilities?

Array’s lawsuit was dismissed by the court on January 3, 2025, after a joint motion to dismiss was filed by the defendants. Information on the reasons for the dismissal is not publicly available.

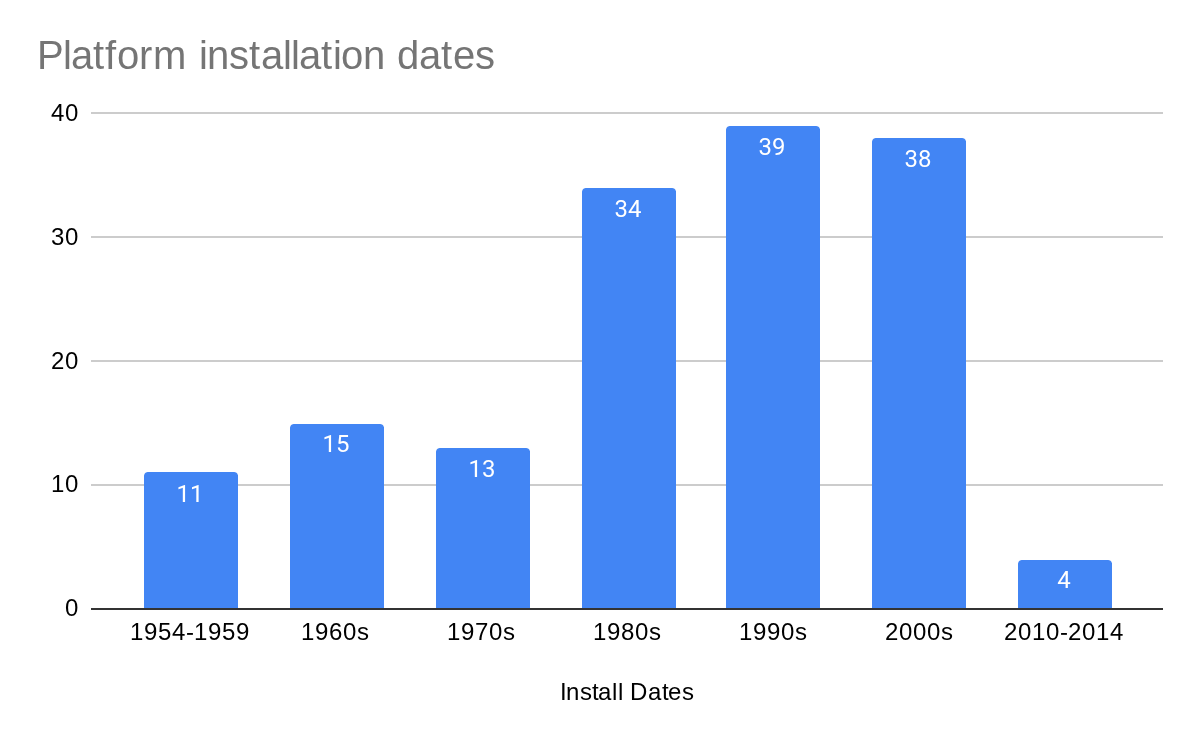

Old platforms: According to BOEM records, Array operates 154 platforms previously owned by Cox. These platforms are in the Ship Shoal, South Marsh Island, and West Delta areas of the Gulf of America. Most are >30 years old and four are more than 70 years old (see chart below). 41 are classified as major structures including 15 of the 26 platforms installed in the 1950s and 1960s. 44 are manned on a 24 hour basis. 79 have helidecks. Massive decommissioning liabilities loom.

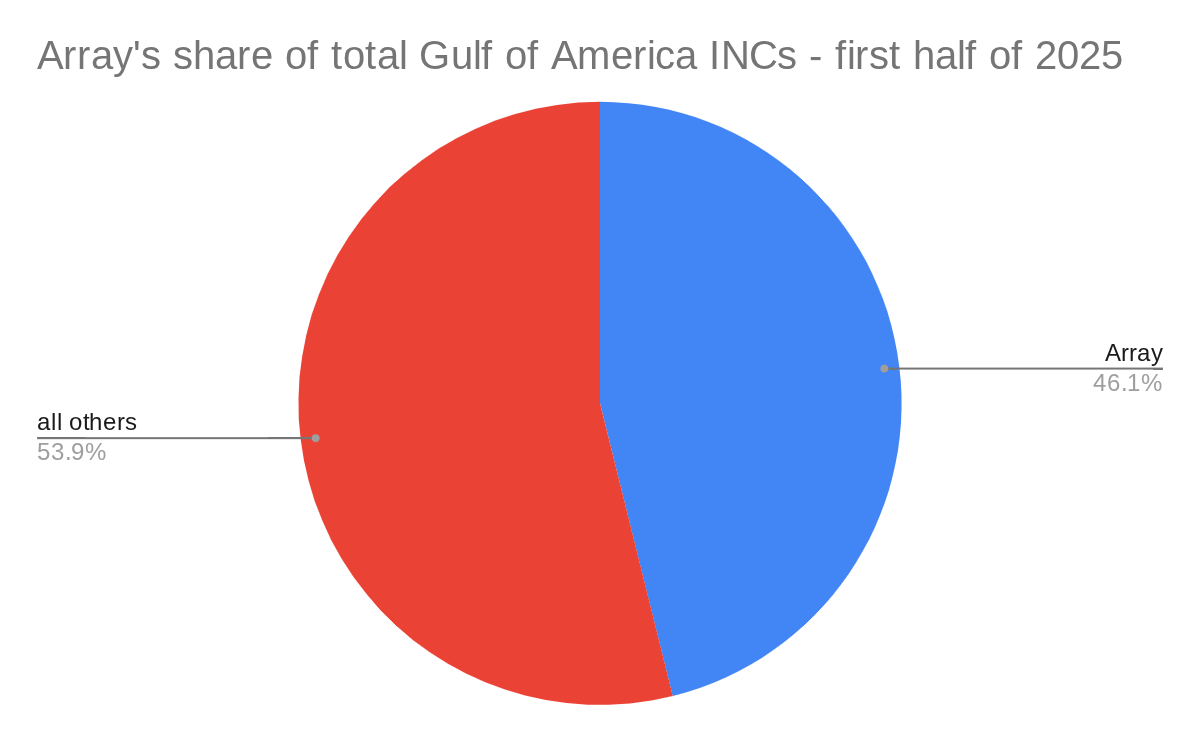

Violations: NRW/Array ranks 37th out of 42 companies in GoA oil production (2025 YTD) and 36th out of 42 companies in gas production, but leads the pack in Incidents of Noncompliance (INCs):

Array accounted for nearly half of all GoA INCs issued in the first half of 2025 (chart below).

Array was issued 9 times more warning INCs (311) than any other operator. Apache was second with 34.

There are many small and mid-sized companies that are responsible operators. Their participation in the OCS program should be encouraged. However, others have demonstrated, by their inattention to financial and safety requirements, that they are not fit to operate OCS facilities.

The growth of Fieldwood, Cox, Signal Hill, and Black Elk was in part facilitated by lax lease assignment and financial assurance policies.

Operating companies should have to demonstrate that they can operate safety and comply with the regulations before they are approved to acquire more properties.

Expect the ultimate public cost of the Cox bankruptcy, in terms of decommissioning liabilities and the need for increased oversight, to be large.

The Federal govt (Justice/Interior) should strongly oppose bankruptcy court asset sales that increase public financial, safety, and environmental risks.

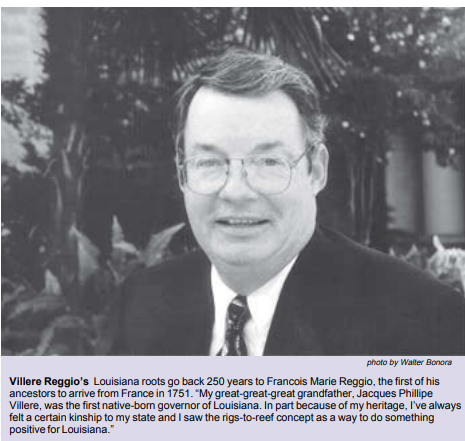

Not mentioned in the film are the extraordinary efforts of the Mineral Management Service’s Villere Reggio in establishing the Rigs to Reefs program. Villere (pictured below), has a most interesting family history as summarized in the caption. See p. 3 of this issue of MMS Today for the complete article.

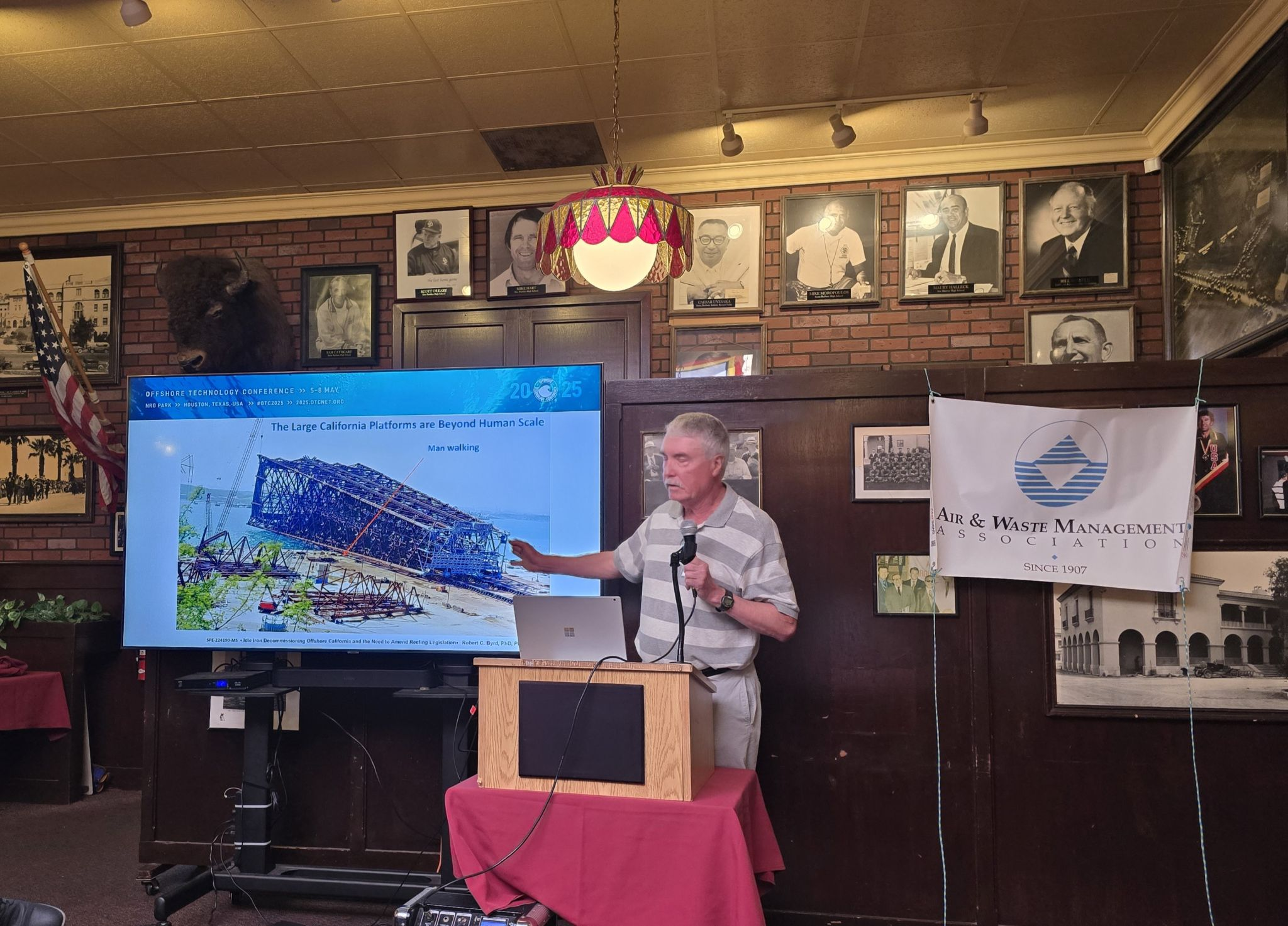

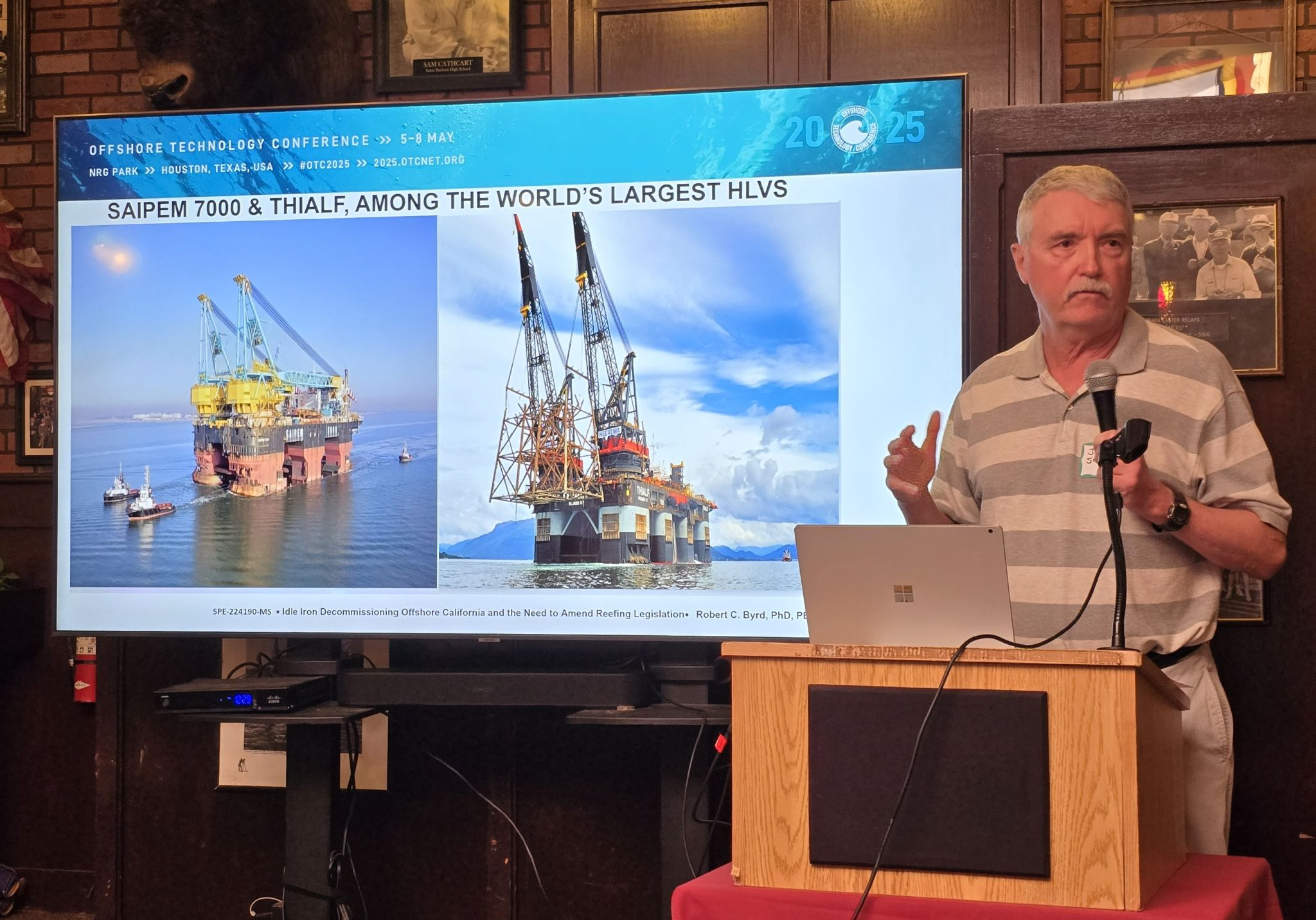

Sharing pictures from John Smith’s excellent decommissioning presentation at the Western States Petroleum Assoc. luncheon in Santa Barbara in May. You can view or download the presentation here.

Thialf: a character in Norse mythology who was Thor’s servant.

The Heerema Thialf, a semi-submersible crane vessel (SSCV), is a rather massive presence in coastal waters. The vessel is 661 feet long and 470 feet high, with a lifting capacity of up to 14,200 metric tons, and is the second-largest of its kind.

The Thialf, which set a world record in 2000 by lifting the 11,883-metric-ton Shearwater topside structure in the North Sea, will be driving piles for 54 Vestas 15 MW wind turbines and a substation structure that are part of Equinor’s controversial Empire Wind project.

John Smith tells me that the Thialf is one of the heavy lift vessels being considered for removing California offshore oil and gas platforms. The vessel is too large for the Panama Canal and would have to make the trip around South America or across the Pacific, depending on where it was last working.

The Thialf’s day rate has not been disclosed, but is likely greater than $500k. Equinor claimed to be losing $50 million/week when the project was paused. Thialf costs were presumably a significant chunk of those losses.

John Smith’s excellent decommissioning presentation at the recent Western States Petroleum Assoc. luncheon in Santa Barbara is attached. John used an amended version of Bob Byrd’s OTC powerpoint, adding slides on the proposed California Marine Legacy Act amendments.

For those who have been following the Santa Ynez Unit story, Harmony, Heritage, and Hondo are the platforms in that unit. Platform Harmony, where production resumed on the date of John’s presentation (5/15), is in 1198′ of water and is one of the world’s largest offshore structures.