The Rigs-to-Resistors category in our World Famous Rigs-to-Reefs +++ list has been expanded to include offshore data centers, a concept that is attracting investor interest (see attached brochure).

Advantages of offshore data centers include power availability (natural gas, hydro-kinetic, wind, solar), cooling water, sovereignty, and growth potential.

“use, for energy-related purposes or for other authorized mariner elated purposes, facilities currently or previously used for activities authorized under this Act,”

The attachment summarizes plans to install modular data centers on existing offshore platforms. The advocates see “using fixed platforms ready for decommissioning as a low-cost solution with simpler execution.” Are they a bit too optimistic? 😉

For 40 years, challenges associated with bankruptcies (or the threat thereof), a divided offshore industry, political pressure, hurricane damage, and unresolved legal issues have hindered initiatives to better protect the public from decommissioning liabilities. Nonetheless, regulators and industry were able to prevent taxpayers from incurring any decommissioning costs. Unfortunately that is no longer the case.

For the first time in history, the govt has funded decommissioning on the OCS (and bragged about it – photo below).

Federally funded decommissioning operation in the Matagorda Area of the Gulf.

BOEM’s proposed revisions to the decommissioning regulations (attached) would facilitate the transfer of aging structures to companies with limited assets, and in some cases, poor or undemonstrated safety records.

The proposal would reduce or eliminate the supplemental financial assurance requirement if a predecessor lessee has a strong credit rating. For that strategy to work, related decommissioning issues must be addressed. and clarifications and boundaries provided to ensure taxpayers are protected from decommissioning liabilities.

Predecessor liability, which is important because it helps prevent companies from assigning leases for the purpose of avoiding decommissioning obligations, was not established in the regulations until much of the OCS infrastructure was already installed. In a final rule that was effective on 8/20/1997,my office (thanks to the perseverance of Gerry Rhodes, John Mirabella, and Dennis Daugherty) codified the joint and several liability principle in 30 CFR 250.110 as follows:

(b) Lessees must plug and abandon all well bores, remove all platforms or other facilities, and clear the ocean of all obstructions to other users. This obligation: (1) Accrues to the lessee when the well is drilled, the platform or other facility is installed, or the obstruction is created; and (2) Is the joint and several responsibility of all lessees and owners of operating rights under the lease at the time the obligation accrues, and of each future lessee or owner of operating rights, until the obligation is satisfied under the requirements of this part.

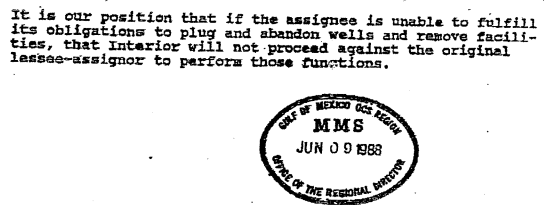

Prior to the that rule, the official policy of the Dept. of the Interior, as expressed in a 1988 letter from the Director of the Minerals Management Service (see excerpt pasted below), was that lease assignors would NOT be held accountable should their successors fail to fulfill their decommissioning responsibilities.

A major unanswered question regarding decommissioning obligations is thus the extent to which predecessor liability applies to leases assigned prior to the 1997 regulation. According to BOEM data, 771 remaining platforms were installed at least 10 years before the rule change, and 504 were installed at least 20 years prior. For assets transferred prior to the rule change, do the predecessors retain liability? BOEM should explain its position on this issue.

Other predecessor liability questions that need to be answered:

Now that the reverse chronological guidance has been scrapped, what will be the process for determining which predecessors will be held responsible?

If the govt doesn’t ensure that the new lessees fulfill their performance obligations (e.g. funding escrow accounts, well plugging, insurance, etc.), are predecessors still liable?

What if the structures were poorly maintained by the new lessees, complicating decommissioning and increasing the costs

Should a predecessor several transfers removed from operating the facilities still be held responsible?

Two examples of what can happen (and has happened):

Example 1: Big AAA Oil assigns a lease to Proud Production, a reputable independent. After years of operations, Proud can no longer profitably produce from the lease. Proud assigns the lease to CCC Oil & Gas, a small and highly efficient operator. After the lease is no longer profitable, even for a company with a low cost structure, CCC assigns the lease to Elmer’s E&P, a sketchy, barely solvent operating company with a poor compliance record. Elmer rather predictably neglects maintenance and declares bankruptcy after a decline in oil prices. Should Big AAA Oil, which had no say in the last 2 transfers in the assignment chain, be financially responsible for decommissioning the facilities?

Example 2: Big AAA Oil assigns a lease to DDD Development Company. Per the terms of the assignment, DDD establishes an Abandonment Escrow Account, as provided for in 30 CFR 556.904. BOEM allows DDD to withdraw funds from the account for purposes not authorized in the regulations. Should Big AAA Oil be liable for decommissioning costs after DDD is no longer solvent? (See “The troubling case of Platforms Hogan and Houchin.”)

For predecessor liability to be fairly and effectively implemented, and survive legal challenges, BOEM should:

Before approving lease assignments, verify that the assignors and assignees have contractually specified, to BOEM’s satisfaction, how the decommissioning of assigned assets will be funded.

Not approve subsequent lease assignments until the predecessor that is being held financially responsible has approved a funding agreement with the new lessees.

Updatedincident tables for OCS oil and gas operations. The most recent data are for 2023! Providing timely details on incidents is a fundamental responsibility of a safety regulator.

A summary of incidents associated with the OCS wind program. From press reports, we know about the fatality during Empire Wind construction. What other incidents have occurred to date?

Information on the mysterious sinking of the Aban Pearl semi-submersiblein May 2010. An investigation was conducted, but the report was never shared. In the interest of offshore safety, the new regime in Venezuela should release this report.

John comments that the project description, which calls for removing the jacket, seep tents and pipelines, and partially removing the upper 5 feet of the 23-foot-high shell mounds, does not make much sense given the abundant fish and invertebrates that reside on or around the platform jacket.Cutting the jacket off 85 feet below the water line and converting the remaining structure to an artificial reef would make more sense and should have been designated the proposed project.

The plan is to send the materials to the Ports of Long Beach, Los Angeles or Hueneme or possibly Ensenada, Mexico. The project involves complex logistics and is going to be a very long (3 years), ambitious and expensive project that will likely set a precedent for future platform decommissioning projects.

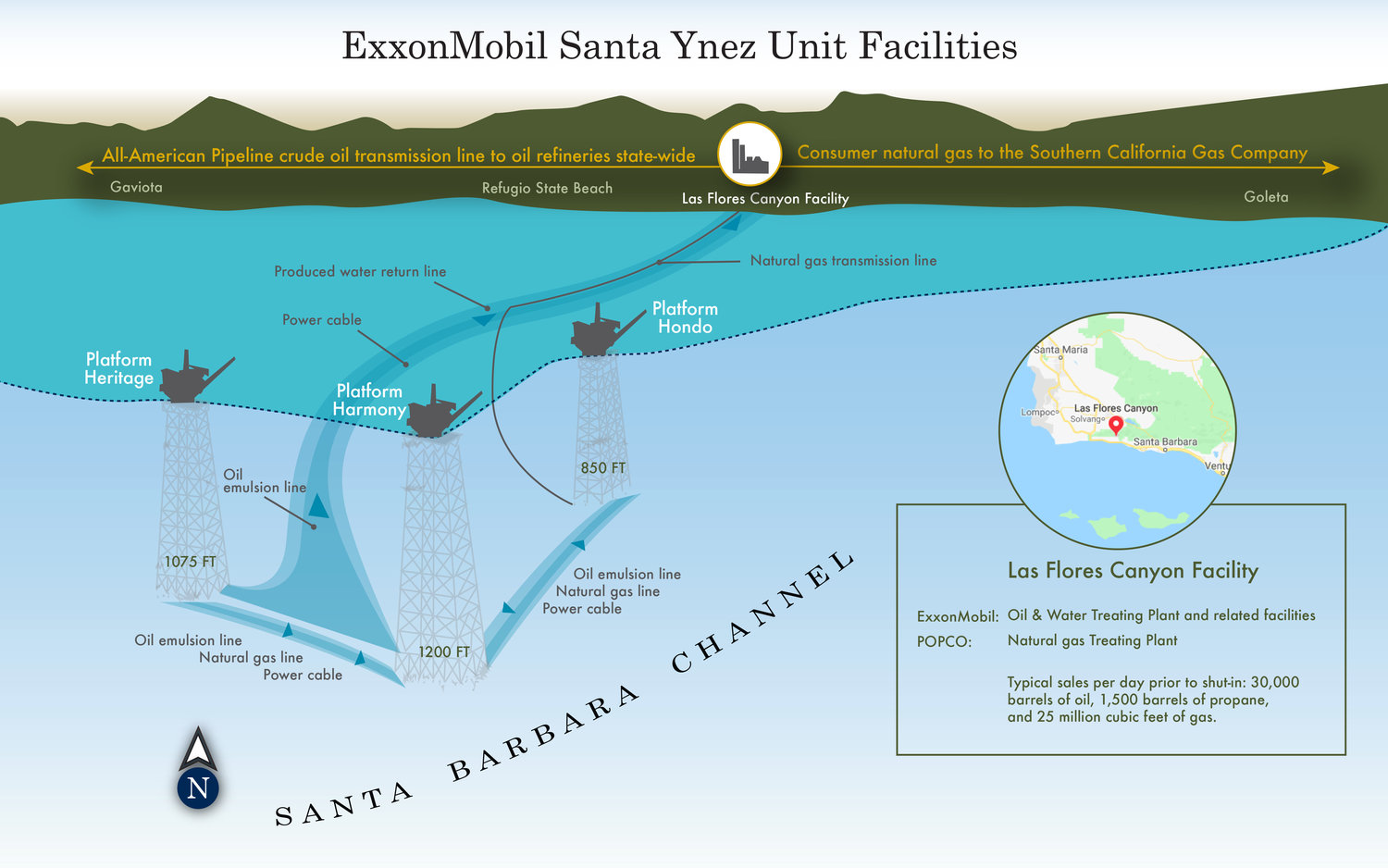

According to their agreement with the CSLC, Exxon is responsible for the decommissioning costs.

Scientific American: The steel “jackets” that support California’s offshore oil platforms are covered in millions of organisms and provide habitat for thousands of fishes. Joe Platko

John Smith, decommissioning specialist and BOE contributor, has shared his comments (attached) on the Marine Fisheries Habitat Protection Act. This legislation would expand the successful reefing programs on the OCS by facilitating the conversion of retired production platforms into artificial reefs.

SEC filing reveals Sable entered October about a month from potential bankruptcy. The company had $41.6 million as of September 30, with $39.7 million in average monthly burn in 3Q25.

When Sable announced its $250 million financing on November 10 at $5.50 per share, the company likely had single digit millions in the bank based on its reported burn, against over $163 million in accounts payable and accrued liabilities. Sable does not generate any revenue.

Sable needs to raise significantly more money: According to leaked audio of Sable’s CEO briefing for select investors, the company will require $2.3 billion to achieve commercial production of oil and gas from its three platforms off the coast of Santa Barbara.

That includes at least $900 million to buy out Exxon, to which Sable must pay 15% interest on debt due by March 31, 2027. By then, the loan would be about $1.1 billion, accruing $200 million in added debt.

One of Sable’s only known assets other than the oil and gas project is a private plane the company purchased from its CEO, Jim Flores. The plane recently flew round-trip from Houston, where Flores lives, to Louisiana, in time for a football game at the CEO’s alma mater.

Comments from Santa Barbara County Supervisor Steve Lavagnino, an oil industry supporter, that explain his opposition to the transfer of Exxon’s pipeline permit to Sable:

“The final straw for me was a Hunterbrook article, which was as disturbing as anything I’ve read. I have many friends in the oil industry and I will continue to support efforts to access our natural resources, but it has to be done responsibly by operators who put safety above profits.”

Sable’s limited response to the Hunterbrook report includes information on decommissioning financial assurance:

Sable’s original SYU Purchase and Sales Agreement (PSA) with Exxon required Sable to post a $350 million decommissioning bond “150 days following the resumption of production from the wells.”

According to Sable, production resumed on May 15, 2025. The bond would have thus been required in October. (SYU production was halted by court order on June 6, so that “resumption date” may be irrelevant. Regardless, the Oct. financial assurance deadline is immaterial given the recent update to the PSA.)

The PSA update extended the date for posting the decommissioning bond to three business days following the new Exxon Loan Maturity Date of March 31, 2027 or 90 days after first sales of hydrocarbons, whichever comes first. (Note the change in language from “resumption of production” to “first sales.” Brief well test production does not trigger posting of the decommissioning bond.)

Under certain circumstances after the bonding is in place Exxon may seek an increase in the bonding amount to $500 million.

The decommissioning obligations are moot if Sable runs out of funds or is unable to resume SYU production prior to the 3/31/2027 PSA deadline.Exxon would remain fully responsible for SYU decommissioning.

Is it time for a public statement from Exxon on the SYU and Sable?

Attached is a court filing challenging Delaware’s approval of the Coastal Construction Plan for that project. Some interesting points from the filing:

Maryland local governments declined to allow the transmission lines from the Maryland Offshore Wind Project to come ashore in their jurisdictions.

The Governor of Delaware agreed to allow the transmission lines to make landfall at the Delaware Seashore State Park.

The transmission pipelines would then traverse the adjacent Delaware Bays, to an inland substation, from which the power would be sent to Maryland.

US Wind applied for a number of permits from the Delaware Department of Natural Resources (DNREC) specific to horizontal directional drilling, laying cable pipelines, and other coastal construction activity.

The approval process, including provisions for public input, was not consistent with State regulations.

The Secretary’s decision to issue the beach construction permit is supported virtually exclusively by documents which were submitted by US Wind after the close of public comment.

Decommissioning and financial assurance information, a favorite BOE topic for both wind and oil/gas, was submitted after the close of the public record.

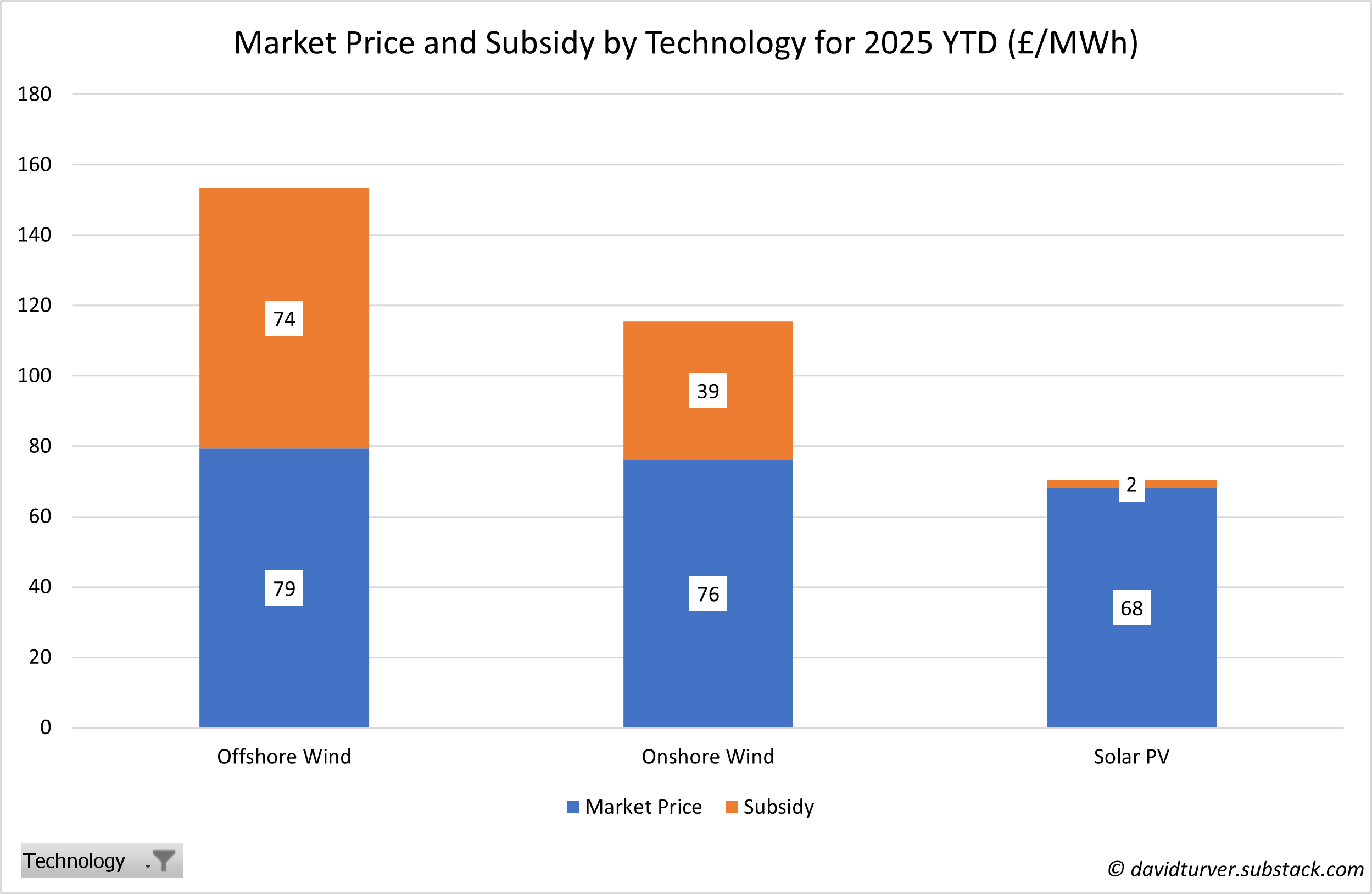

JL Daeschler informs that UK offshore wind energy is 82% foreign-owned. Foreign companies are thus the primary beneficiaries of the UK’s generous renewable energy subsidies (chart below).

“We have been warning for some time that it is crazy for a developed economy to try and run its electricity generation system using technologies that are dependent on the weather. Even though there has been only a relatively modest decline in wind output this year, the operators and owners of wind farms are learning the hard way that it is very difficult to run a business that is at the mercy of the vagaries of the weather. Many of these companies are up to their eyeballs in debt. They better hope the wind blows hard this Autumn and Winter so they can collect higher subsidies, or they will be in real trouble.“

We have consistently raised concerns about decommissioning financial assurance for offshore wind facilities. Turner echoes those concerns noting that the wind industry’s “perilous finances are an even bigger reason to insist that proper funds are set aside to fund decommissioning or the long-suffering taxpayer will be on the hook for another hidden cost of renewables.“

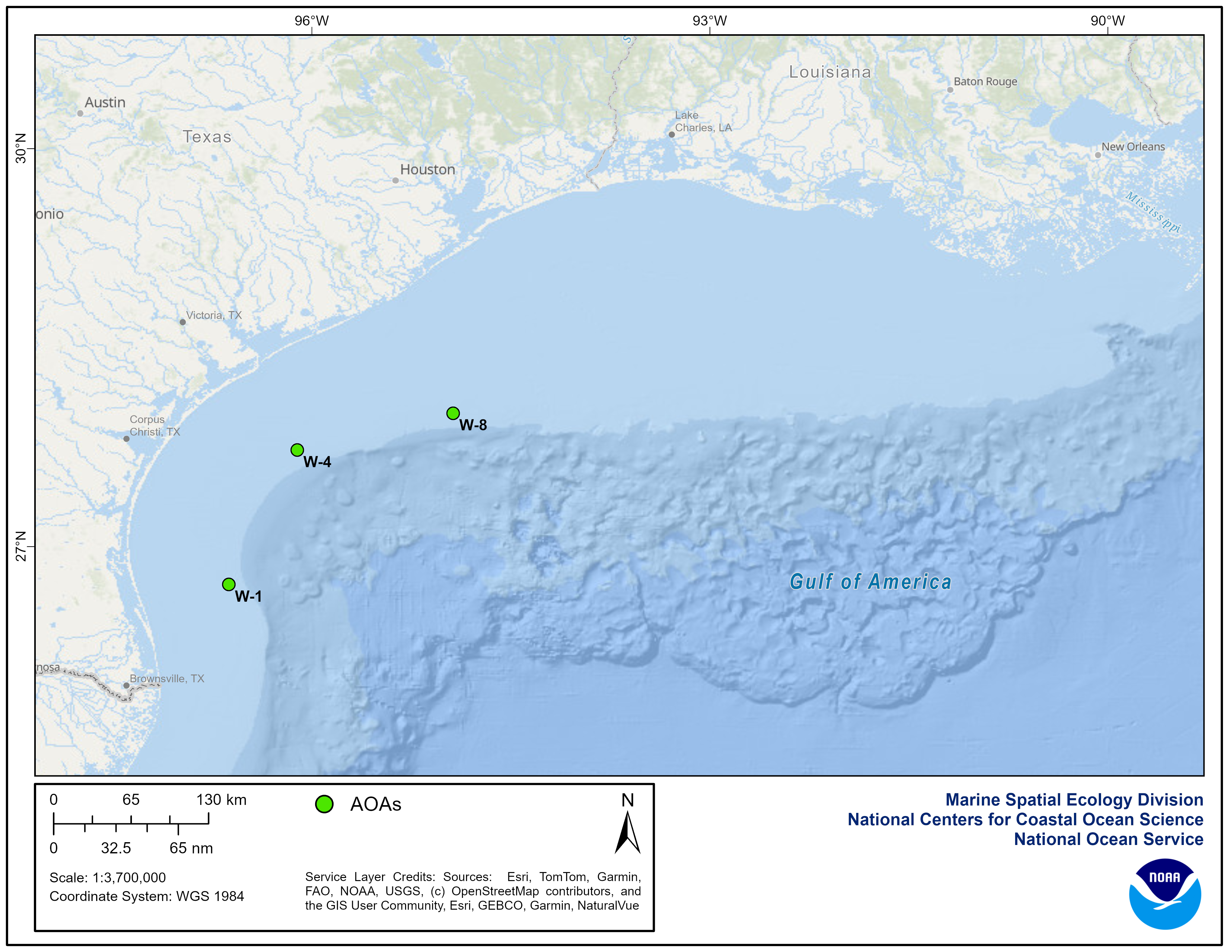

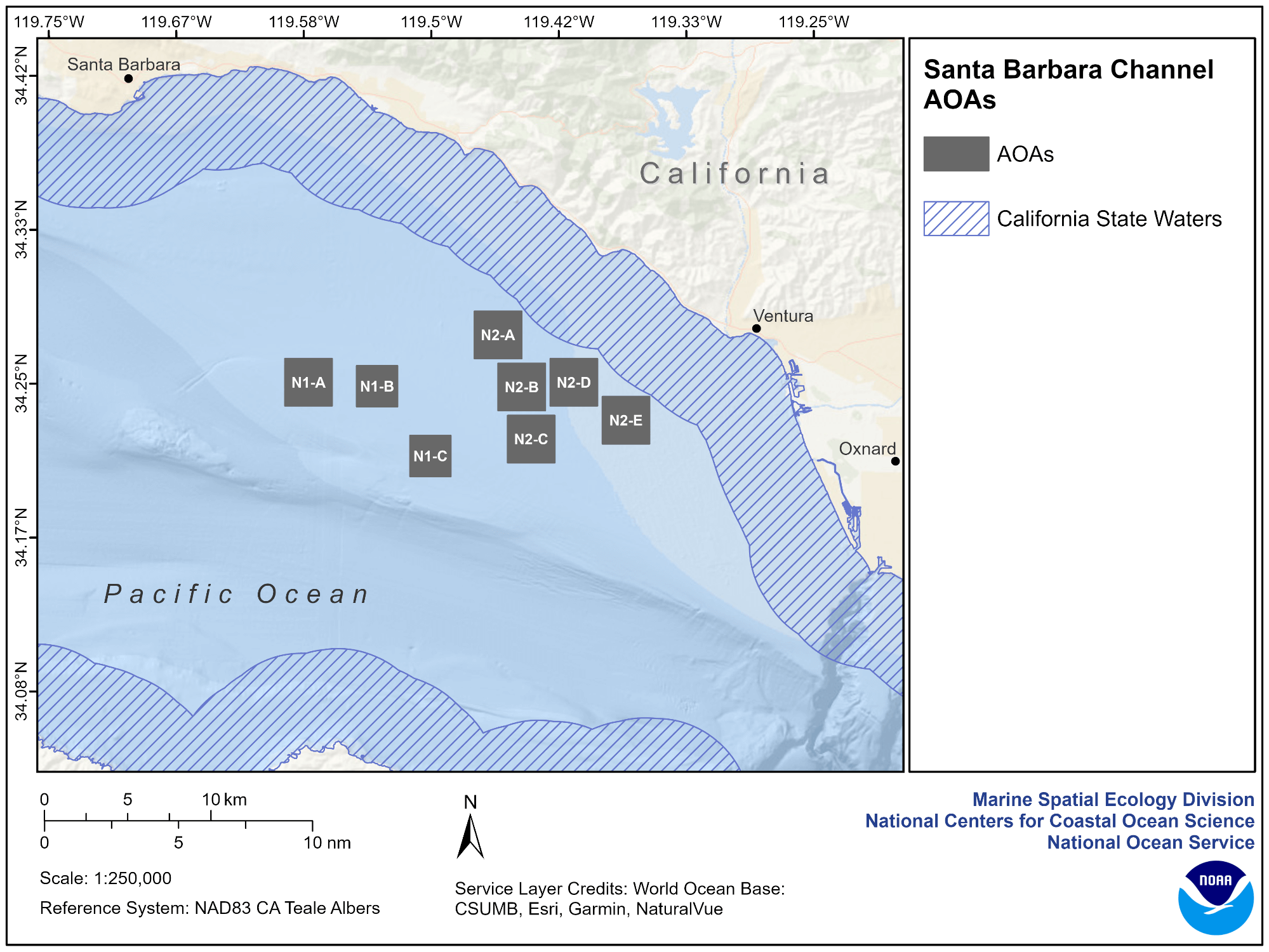

NOAA is touting marine aquaculture and has published Programmatic Environmental Impact Statements for Aquaculture Opportunity Areas (AOAs) in the Gulf of America and offshore Southern California. This is a positive step.

While the focus of these EIS documents is on distinct AOAs separated from oil and gas facilities, NOAA might also have discussed the potential for synergy with existing platforms. The reef effect of platforms can be sustained and new fishery ventures supported by converting older platforms to aquaculture facilities (Rigs-to-Roe/Redfish/Rockfish) rather than decommissioning them.

According to a paper published in 2014 by marine ecologist Dr. Jeremy Claisse of Cal Poly Pomona, the oil and gas platforms off the coast of California are the most productive marine habitats per unit area in the world. “Even the least productive platform was more productive than Chesapeake Bay or a coral reef in Moorea,” said Dr. Love. (Milt Love, UCSB biologist)

Attached is the Dept. of the Interior’s Semiannual Regulatory Agenda (9/22/2025). BSEE and BOEM decommissioning rules are excerpted below.

Of particular concern is the revised BOEM regulation (107) that “would reduce the amount of supplemental financial assurance required from oil gas, and sulfur lessees operating on the OCS.” See our previous post on this regulatory action. Note that a proposed rule is expected to be published by year end.

REVISIONS TO DECOMMISSIONING REQUIREMENTS ON THE OCS [1014–AA53] Legal Authority: Outer Continental Shelf Lands Act, 43 U.S.C. 1331 to 1356a Abstract: This proposed rule would address issues relating to (1) idle iron by adding a definition of this term to clarify that it applies to idle wells and structures on active leases; (2) abandonment in place of subsea infrastructure by adding regulations addressing when BSEE may approve decommissioning-in-place instead of removal of certain subsea equipment; and (3) other operational considerations. Timetable: NPRM ……………… 07/00/26 NPRM Comment Period End: 10/00/26

RISK MANAGEMENT AND FINANCIAL ASSURANCE FOR OUTER CONTINENTAL SHELF LEASE AND GRANT OBLIGATIONS [1010–AE26] Legal Authority: 43 U.S.C. 1331, OCS Lands Act; E.O. 14154, Unleashing American Energy Abstract: This proposed rule would rescind BOEM’s final rule ‘‘Risk Management and Financial Assurance for OCS Lease and Grant Obligations.’’ The proposed rule would revise the criteria for determining whether oil, gas, and sulfur lessees, right-of-use and easement grant holders, and pipeline right-of-way grant holders are required to provide financial assurance above the current minimum bonding levels to ensure compliance with their Outer Continental Shelf (OCS) Lands Act obligations. This rule, if finalized, would reduce the amount of supplemental financial assurance required from oil gas, and sulfur lessees operating on the OCS and would support the goals of E.O. 14154; Timetable: NPRM ……………… 01/00/26

Interesting case: Delaware litigation on approval of the Coastal Construction Permit for the Maryland Offshore Wind Project

Posted in decommissioning, energy policy, Offshore Wind, Regulation, tagged Coastal Construction Plan, court filing, decommissioning, Delaware litigation, Maryland Offshore Wind, public comment, US Wind on October 29, 2025| Leave a Comment »

The Dept. of the Interior is currently reconsidering approval of the Construction and Operations Plan for the Maryland Offshore Wind Project (US Wind).

Attached is a court filing challenging Delaware’s approval of the Coastal Construction Plan for that project. Some interesting points from the filing:

Read Full Post »