Those of us who were involved with OCS oil and gas operations in the 1970s remember the heated battles between Exxon and Santa Barbara County that led to the installation of the infamous Offshore Storage & Treatment (OS&T) facility in Federal waters. This was the first floating production, storage, and offloading facility (FPSO) in US waters by 3 decades!

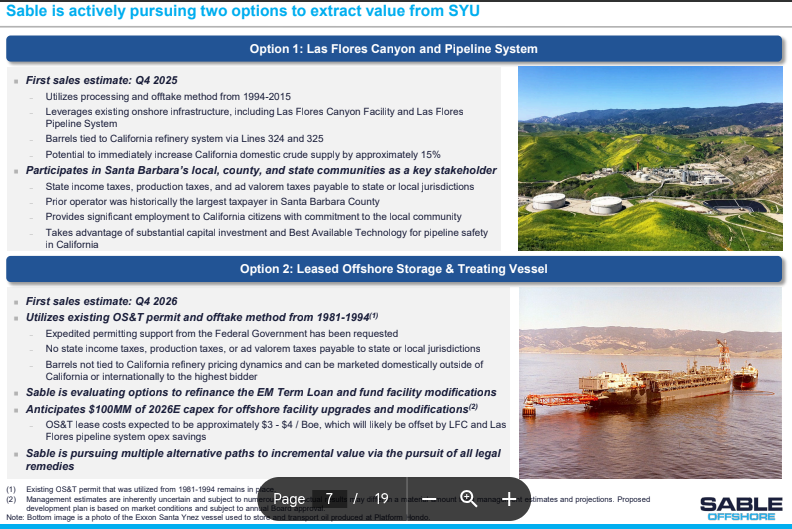

In light of Sable’s difficult (bordering on impossible) onshore permitting challenges, the company resurrected the OS&T option in a recent presentation to investors (pertinent slide pasted above). The extent to which this is purely a tactical maneuver remains to be seen, but this option would be very difficult to execute, even with a supportive Federal regulatory environment.

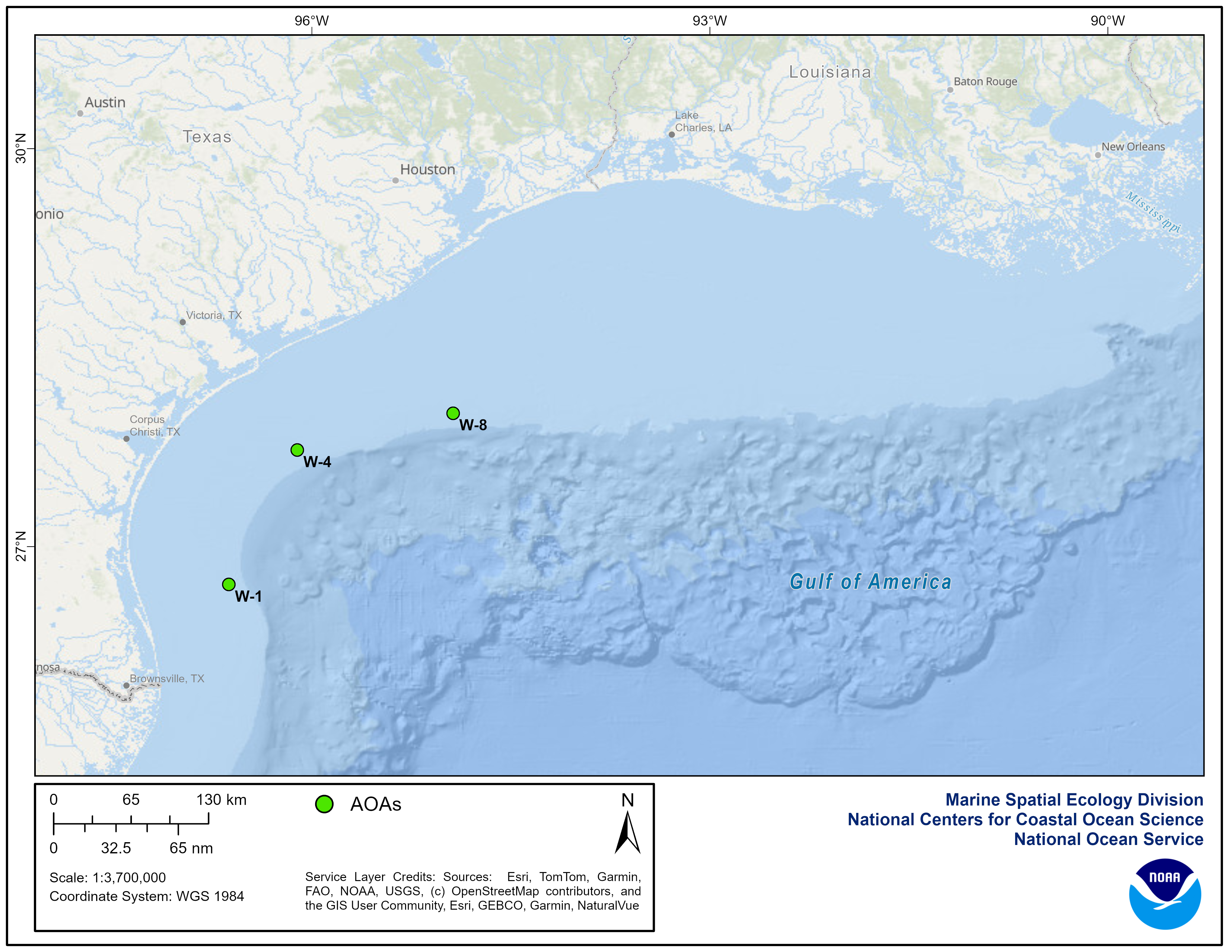

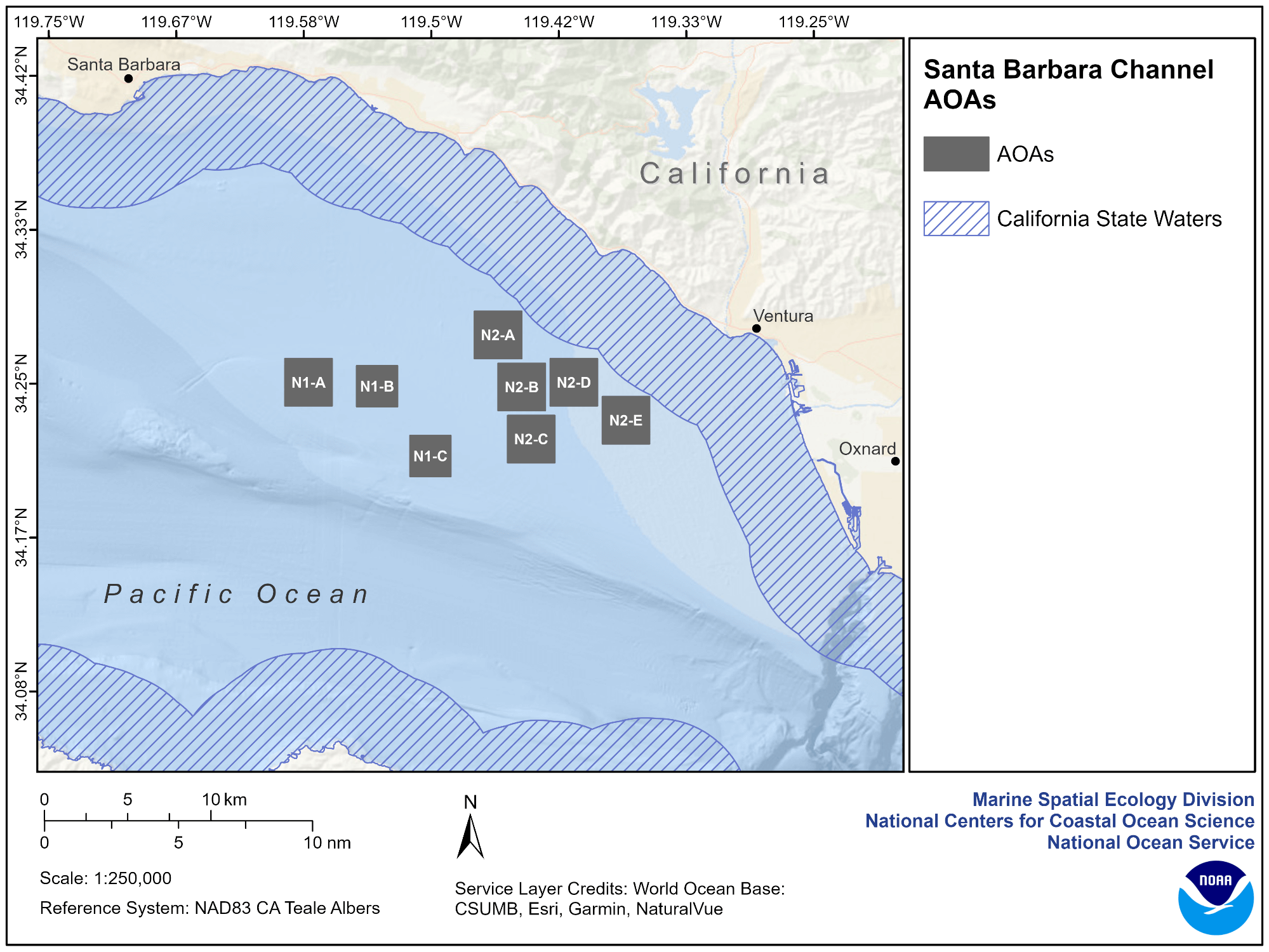

NOAA is touting marine aquaculture and has published Programmatic Environmental Impact Statements for Aquaculture Opportunity Areas (AOAs) in the Gulf of America and offshore Southern California. This is a positive step.

While the focus of these EIS documents is on distinct AOAs separated from oil and gas facilities, NOAA might also have discussed the potential for synergy with existing platforms. The reef effect of platforms can be sustained and new fishery ventures supported by converting older platforms to aquaculture facilities (Rigs-to-Roe/Redfish/Rockfish) rather than decommissioning them.

According to a paper published in 2014 by marine ecologist Dr. Jeremy Claisse of Cal Poly Pomona, the oil and gas platforms off the coast of California are the most productive marine habitats per unit area in the world. “Even the least productive platform was more productive than Chesapeake Bay or a coral reef in Moorea,” said Dr. Love. (Milt Love, UCSB biologist)

Updatedincident tables for OCS oil and gas operations. The most recent data are nearly 2 years old. The public has a right to timely information on the type of incidents that are occurring, the operating companies, and the resulting casualties, pollution, and property damage.

A summary of incidents associated with the OCS wind program. From press reports, we know about the fatality during Empire Wind construction. What other incidents have occurred to date?

This study provides the first evidence that EMFs typical of SPCs elicit sex-specific behavioral responses in C. maenas. Females exhibited significantly greater attraction to EMF zones and avoidance of low-field zones, suggesting higher exposure risk. These differences could affect migration, mating, and larval release, with consequences for population dynamics.

Earlier this week a tree service company was removing some large branches in our backyard. The 2 young workers stopped the job before they finished. They knocked on our door and told me that their foreman was off and they were uncomfortable tackling a large, high branch without him and a crane operator. They would come back with a full crew.

I congratulated them and told them they did exactly the right thing. I told them I was involved with offshore safety and many serious incidents would have been prevented if workers, with their employers encouragement, had been more assertive in stopping work. Developing that type of culture takes time and requires strong leadership and consistent, unambiguous messaging. Leadership matters, both at the site and in the office!

The Macondo well is a worst case example on many fronts, including the reluctance or inability of management and workers to stop taking actions that increased well control risks. Given the narrow pore pressure/fracture gradient, the prudent decision would have been to set a cement plug in the open hole and carefully assess next steps. However, delays and cost overruns were the overriding concerns, and well construction continued despite the long list of issues described here. Sadly, we know how that worked out.

Even after the well started to flow, the crew had time to actuate the emergency disconnect sequence and avert disaster. However, some combination of deficient training, uncertain authority, and fear of repercussions prevented that from happening.

Be it a small tree service company or a major oil company, safety culture development is a journey that has no end point and requires continuous leadership from everyone in the organization.

Attached is the Dept. of the Interior’s Semiannual Regulatory Agenda (9/22/2025). BSEE and BOEM decommissioning rules are excerpted below.

Of particular concern is the revised BOEM regulation (107) that “would reduce the amount of supplemental financial assurance required from oil gas, and sulfur lessees operating on the OCS.” See our previous post on this regulatory action. Note that a proposed rule is expected to be published by year end.

REVISIONS TO DECOMMISSIONING REQUIREMENTS ON THE OCS [1014–AA53] Legal Authority: Outer Continental Shelf Lands Act, 43 U.S.C. 1331 to 1356a Abstract: This proposed rule would address issues relating to (1) idle iron by adding a definition of this term to clarify that it applies to idle wells and structures on active leases; (2) abandonment in place of subsea infrastructure by adding regulations addressing when BSEE may approve decommissioning-in-place instead of removal of certain subsea equipment; and (3) other operational considerations. Timetable: NPRM ……………… 07/00/26 NPRM Comment Period End: 10/00/26

RISK MANAGEMENT AND FINANCIAL ASSURANCE FOR OUTER CONTINENTAL SHELF LEASE AND GRANT OBLIGATIONS [1010–AE26] Legal Authority: 43 U.S.C. 1331, OCS Lands Act; E.O. 14154, Unleashing American Energy Abstract: This proposed rule would rescind BOEM’s final rule ‘‘Risk Management and Financial Assurance for OCS Lease and Grant Obligations.’’ The proposed rule would revise the criteria for determining whether oil, gas, and sulfur lessees, right-of-use and easement grant holders, and pipeline right-of-way grant holders are required to provide financial assurance above the current minimum bonding levels to ensure compliance with their Outer Continental Shelf (OCS) Lands Act obligations. This rule, if finalized, would reduce the amount of supplemental financial assurance required from oil gas, and sulfur lessees operating on the OCS and would support the goals of E.O. 14154; Timetable: NPRM ……………… 01/00/26

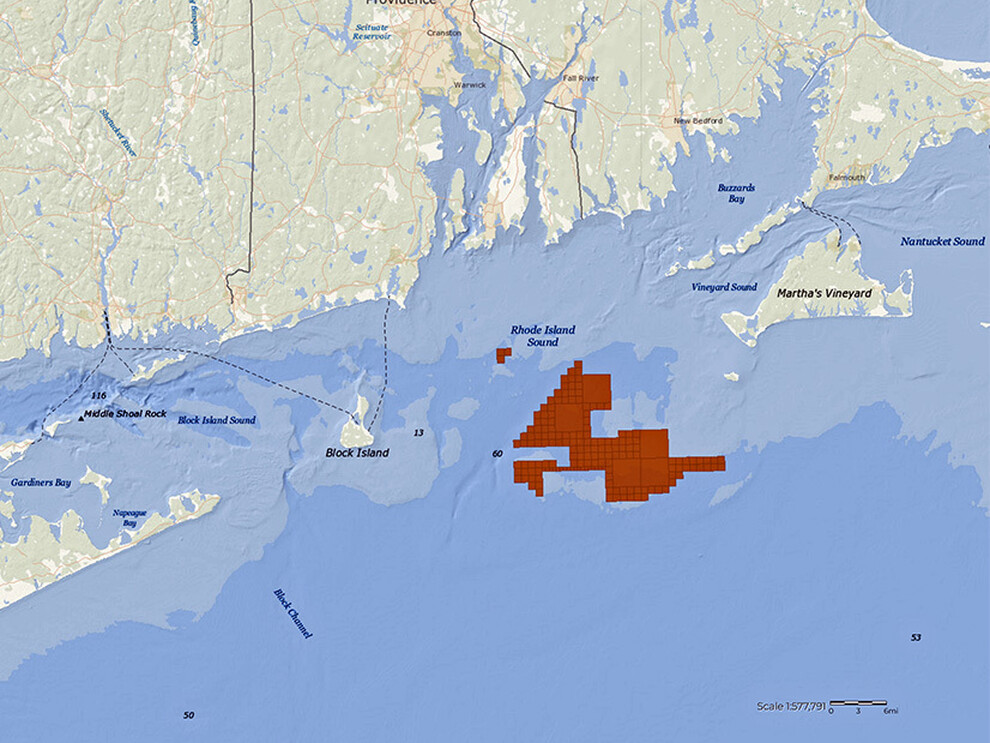

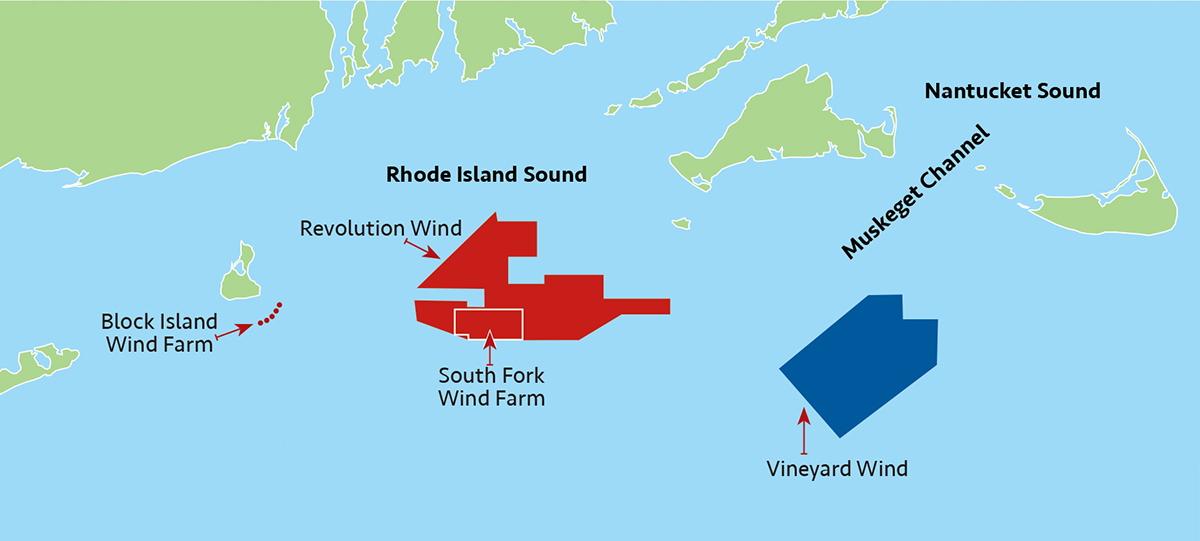

A long-time colleague is very familiar with Judge Lamberth, a Reagan appointee, and thinks highly of him. Orsted has a lease contract, and no matter where you stand on offshore wind, you have to have a compelling case to halt a project that is in the advanced stages of development. Judge Lamberth ruled that the govt doesn’t have such a case. Per the judge:

The govt presented insufficient evidence to support alleged permit noncompliance and national security concerns.

The govt acted in an “arbitrary and capricious” manner.

“If Revolution Wind cannot meet benchmark deadlines, the entire project could collapse.”

“There is no doubt in my mind of irreparable harm to the plaintiffs.”

Projects under development will be difficult to pause or stop. The Administration should focus on requiring sufficient decommissioning financial assurance, monitoring and mitigating project impacts, making incident data publicly available, issuing the report on the Vineyard Wind blade failure (finally!), and improving the availability of dispatchable power (i.e. natural gas and nuclear).

Judge Royce Lamberth granted an injunction allowing Orsted to resume work on the Revolution Wind project. BOEM halted work on the project one month ago.

How can AI and emerging technologies be used in risk management trending and operations?

Why are we not learning from accidents?

Breakthroughs in investigation techniques and sharing

The first IRF Conference was held 20 years ago in London followed by the 2007 conference at the Trump International Resort in Miami (little did we know 😀). More historical background.

The informed, diverse viewpoints about managing and regulating offshore operations sets these conferences apart from your typical professional events. The 2025 conference is highly recommended for those interested in offshore operations, risk mitigation, and regulatory policy.

Gov. Newsom and Danish Foreign Minister Lars Løkke Rasmussen

As is the case for most MOUs, the attached 8/22/2025 agreement between California and Denmark is long on promotion and short on substance. No funds are obligated and there are no work commitments.

The MOU made sense for Gov. Newsom in that he strengthened his green credentials by aligning with the country that is the spiritual leader for climate activists.

The benefits for Denmark were unclear, but the risks should have been apparent. The White House is fundamentally opposed to the climate and energy objectives identified in the MOU. Ørsted (50.1% govt owned) and other Danish business interests are very much dependent on decisions made by the US Federal govt.

Work on Ørsted’s Revolution Wind project has been halted by Interior Secretary Burgum. His decision is being challenged in court, but no matter what the outcome, offshore wind development will be difficult for Ørsted and other foreign companies going forward. The Secretary has broad regulatory authority under the OCS Lands Act, under which there is no such thing as “a fully permitted project.”

Meanwhile, California’s green status has taken a hit with the passage of S 237, which pragmatically authorizes new onshore drilling.

Lastly, as the chart below illustrates, Orsted’s problems didn’t begin in 2025.