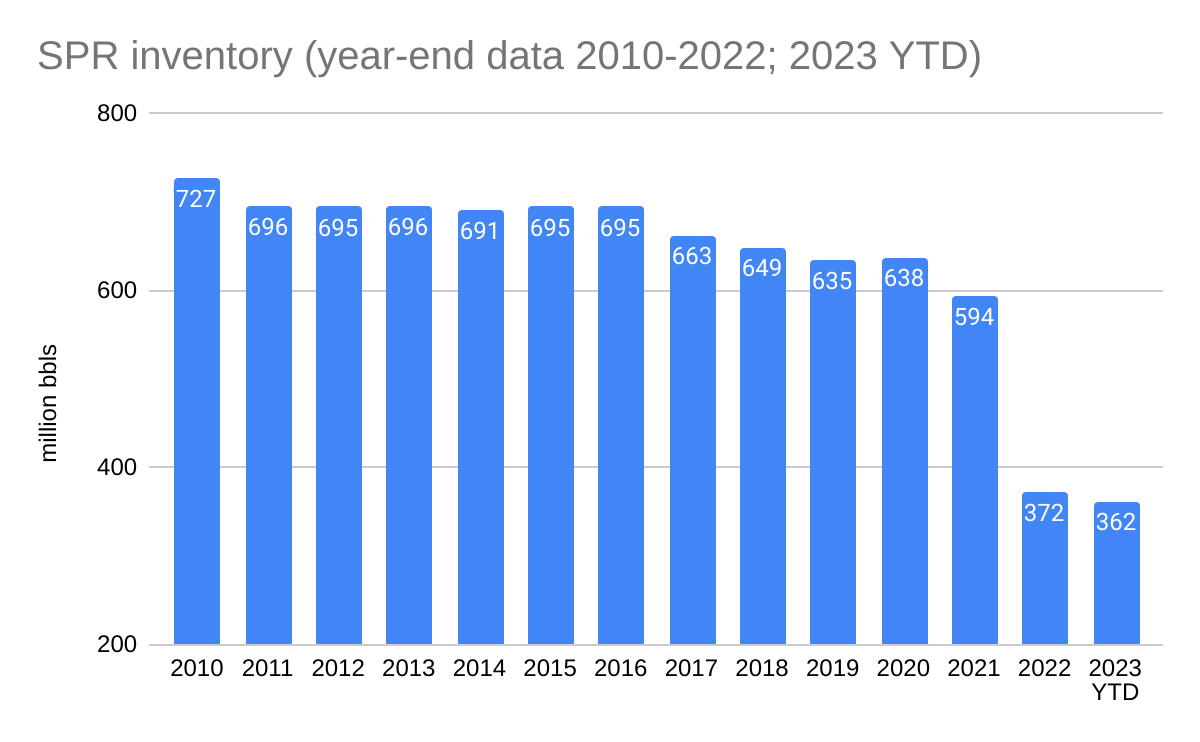

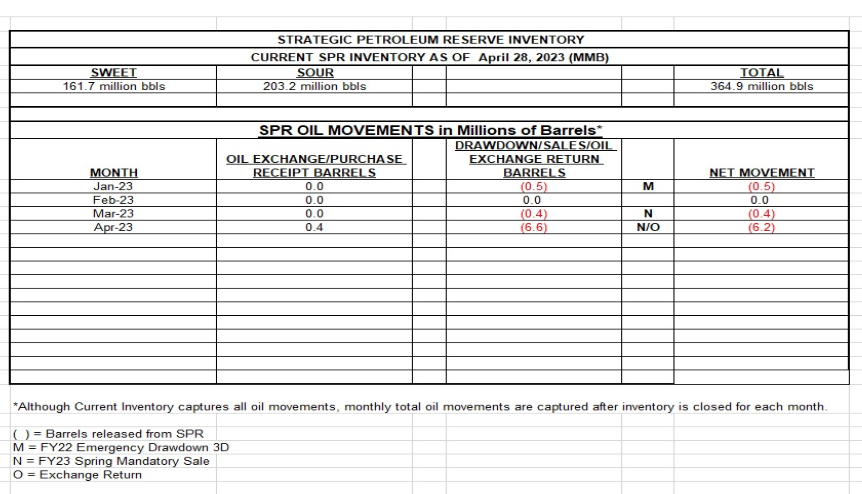

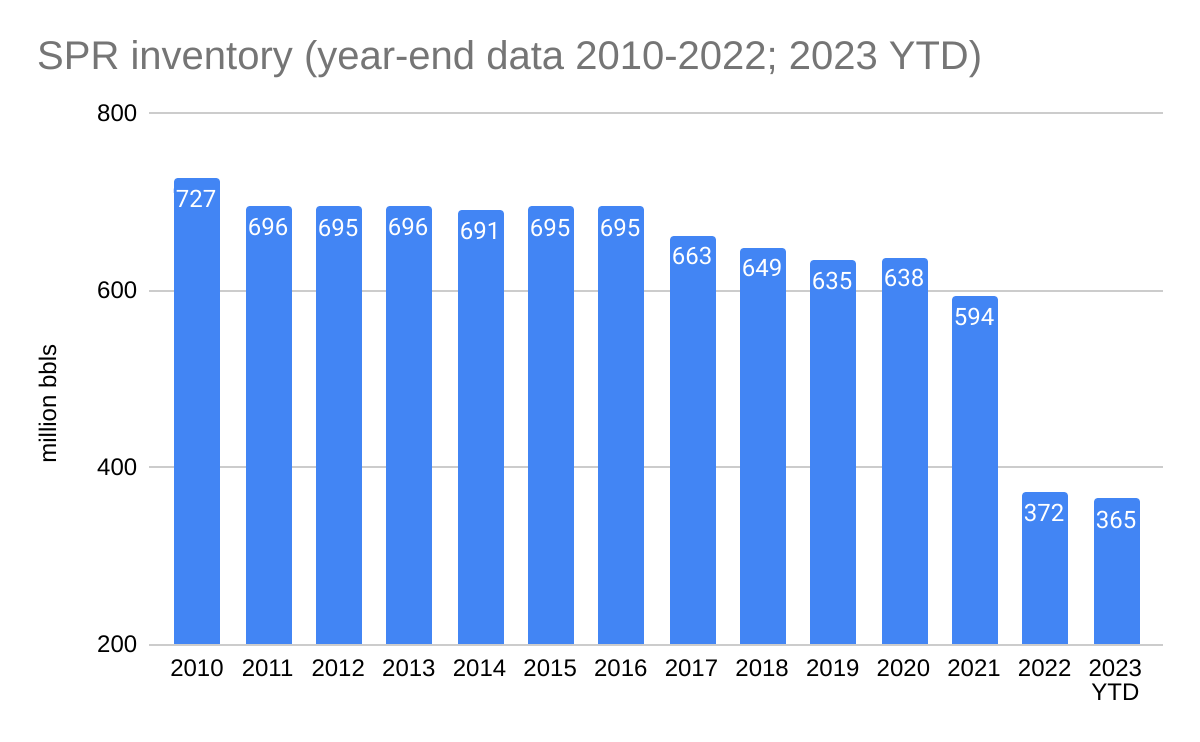

- capacity: 727 million barrels

- current inventory: 362 million bbls (as of 5/5/2023)

- lowest volume since 10/7/1983

- 232 million bbl decline since the end of 2021

Per Bloomberg, DOE says they could begin refilling the reserve this fall “if the price is right.” What if it isn’t?

Keep in mind that the maximum refill rate is 685,000 bopd. A complete refill at the maximum rate would thus require 533 days, not counting acquisition, operational, and maintenance delays. Filling the reserve to its 727 million barrel capacity was a 28 year process.

Lastly, when will DOE conduct the strategic SPR review called for by the General Accountability Office (GAO) in 2018, well before DOE began rashly withdrawing oil to moderate prices? DOE concurred with GAO’s priority recommendation for periodic strategic reviews of the SPR that would be submitted to Congress. DOE told GAO that they “would complete a SPR Long-Term Strategic Review by the end of fiscal year 2021–5 years from the last review in 2016.” That review has still not been completed.

Update: Yesterday, members of Congress asked GAO to evaluate DOE’s management of the SPR and conduct an audit of the SPR modernization program.