Old York Road near West Olney Avenue. December 14th, 1914.

I saw this old picture and was intrigued by the “Mobiloils” sign. I didn’t think Standard of New York had already evolved into Mobil in 1914. A couple of Wiki excerpts explain:

Following the break-up of Standard Oil in 1911, the “Standard Oil Company of New York” (or ‘Socony’) was founded, along with 33 other successor companies.

Socony merged with Vacuum Oil Company to form Socony-Vacuum. Vacuum Oil had used “Mobiloil” automobile lubricating oil brand since 1904, and by 1918 it became recognizable enough that the company filed it for registration as a trademark (it was registered in 1920)

Korea President Yoon Suk Yeol sings “American Pie” by Don McLean during entertainment portion of State Dinner with President Biden. pic.twitter.com/M91Tj4WrHa

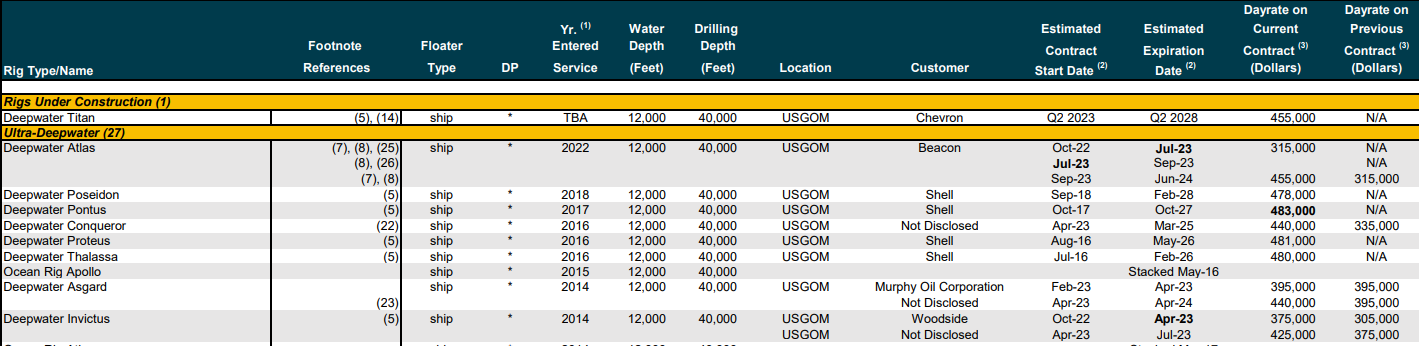

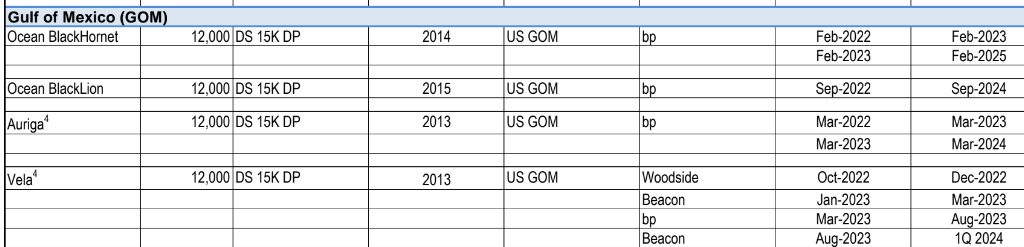

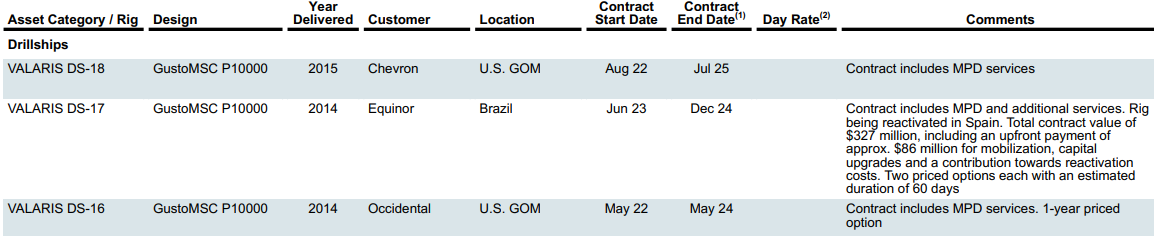

Based on drilling contractor rig activity reports, the table below lists 19 deepwater MODUs under or soon to begin contracts in the GoM. (Further details are pasted at the end of this post.) Per the Valeris report, platform rigs are operating on bp’s Thunder Horse and Mad Dog platforms. Per the BSEE borehole file, Arena and Cantium continue to drill development wells on the GoM shelf.

“BSEE will continue to evaluate the process for issuing decommissioning orders and will continue to issue decommissioning orders to jointly and severally liable parties on a case-by-case basis.“

Although the news release for BSEE’s final decommissioning rule asserts that the regulations “provide the certainty requested by industry,” that does not seem to be the case. The main change in the final rule was to delete the reverse chronological order (RCO) provision which called for issuing decommissioning orders to the most recent predecessor first. Instead, BSEE may continue to issue decommissioning orders arbitrarily.

While deleting the RCO provision may be advantageous for the regulator, and in some cases for the public, claiming that the decision provides certainty for industry is quite a stretch. BSEE may continue to issue a decommissioning order to anyone in the ownership chain, whether the company was a recent lessee or one that had owned the lease decades ago. Original or early lessees may be held liable for decommissioning old facilities regardless of subsequent damage, modifications, or neglected maintenance.

The absence of a defined procedure for issuing decommissioning orders may also expose BSEE to new legal challenges, particularly in cases where a company has not held the lease for decades. A 1988 letter from the Director of the Minerals Management Service to Amoco (attached below) explicitly relieves the assignor (predecessor) of decommissioning liability after the lease has been assigned. A revised bonding rule published on May 22, 1997 reversed that policy, but decommissioning liability for leases assigned prior to the 1997 rule may still be very much in question.

Another concern is the split jurisdiction for decommissioning between BSEE and BOEM. The financial, land management, operational, and environmental aspects of decommissioning are inextricably intertwined and attempts to divide these responsibilities between two bureaus with separate regulations is a prescription for gaps, overlap, inconsistency, inefficiency, disputes, and confusion. Decommissioning should be regulated holistically, not with separate “BOEM-only” and “BSEE-only” regulations.

Finally, wind facility decommissioning may prove to be even more challenging given the higher facility density and economic uncertainties. The regulatory regime needs to be clearly established early in the development phase.

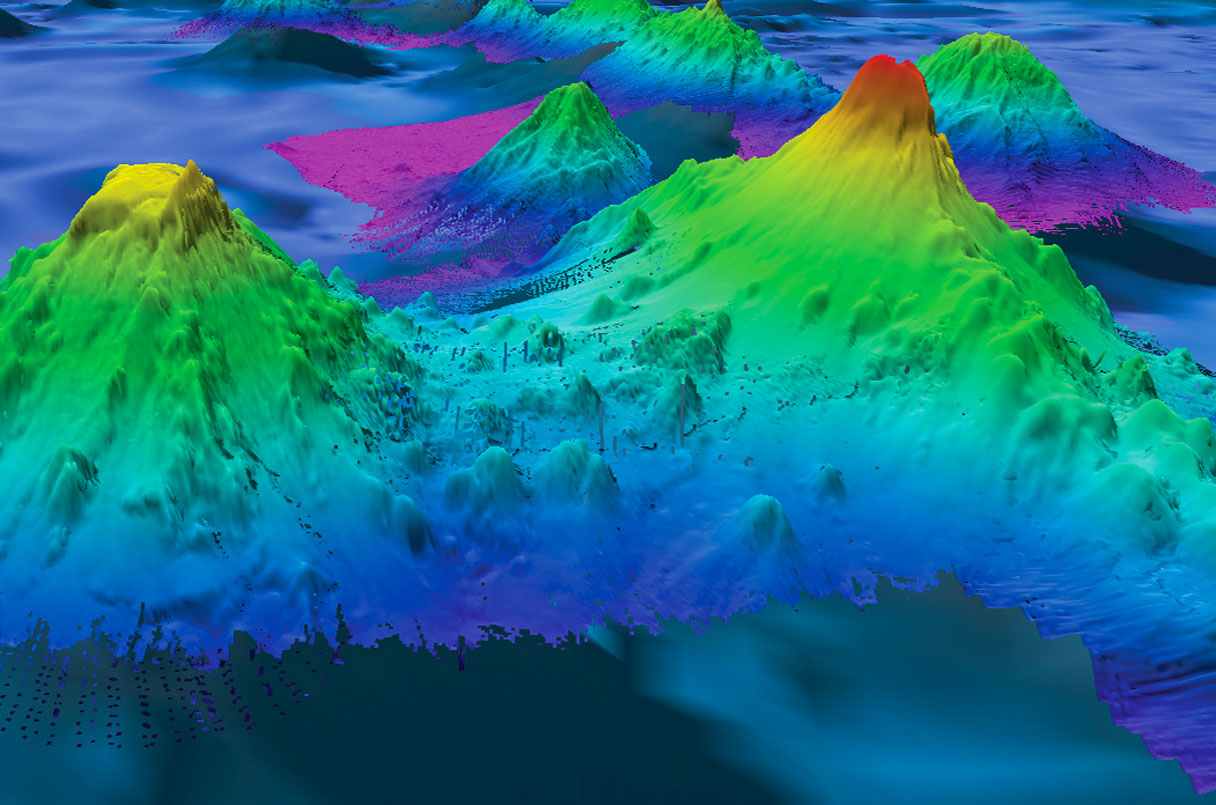

“The 4776-meter-tall Pao Pao Seamount (right) in the South Pacific Ocean has been mapped by sonar. Many others haven’t.” NOAA OFFICE OF OCEAN EXPLORATION AND RESEARCH

This Science article underscores how little we know about the oceans.

With only one-quarter of the sea floor mapped with sonar, it is impossible to know how many seamounts exist. But radar satellites that measure ocean height can also find them, by looking for subtle signs of seawater mounding above a hidden seamount, tugged by its gravity. A 2011 census using the method found more than 24,000. High-resolution radar data have now added more than 19,000 new ones. The vast majority—more than 27,000—remain uncharted by sonar. “It’s just mind boggling,” says David Sandwell, a marine geophysicist at the Scripps Institution of Oceanography, who helped lead the work.

Besides posing navigational hazards, the mountains harbor rare-earth minerals that make them commercial targets for deep-sea miners. Their size and distribution hold clues to plate tectonics and magmatism. They are crucial oases for marine life. And they are pot-stirrers that help control the large-scale ocean flows responsible for sequestering vast amounts of heat and carbon dioxide, says John Lowell, chief hydrographer of the National Geospatial-Intelligence Agency (NGA), which runs the U.S. military’s satellite mapping efforts.

Only 11 exploration wells have ever been drilled in the entire country (comprising an area of around 258,137 km2 including all the offshore areas), all between 1955 and 1982

Hydrocarbon shows were observed in all but one of these wells despite not having tested valid structures, as is evident on the latest data

Just 2 of the 11 wells were drilled offshore

Extensive onshore fieldwork and seep analysis studies have confirmed mature Eocene and Cretaceous oil-prone source rock potential, with migrated oil identified in onshore wells and outcrop samples. These include Late Cretaceous (Cenomanian-Turonian) aged organic shales exhibiting total organic carbon (TOC) up to 8% with maturity.

Modelling also suggests significant oil potential exists in mature Cretaceous source kitchens in both the Walton and Morant basins while shallower Palaeogene shales with TOCs up to 15% could also locally be deep enough to be mature.

An independent Prospective Resources Audit completed by Gaffney Cline & Associates in December 2020 estimates that just 11 of the total 21 prospects & leads defined to date contain a combined total unrisked mean prospective recoverable resources in excess of 2.4 Billion STOOIP (stock-tank oil initially in place). Of this, 406 MMbbls is attributable to the Colibri Prospect alone, with an upside of 966 MMbbls STOOIP.

United is offering a material interest and potential operatorship to suitably qualified parties in the license in return for a commitment to fund a well to test the Colibri Prospect before January 2026, which would fulfill the obligations for the current Second Exploration Period of the Licence.