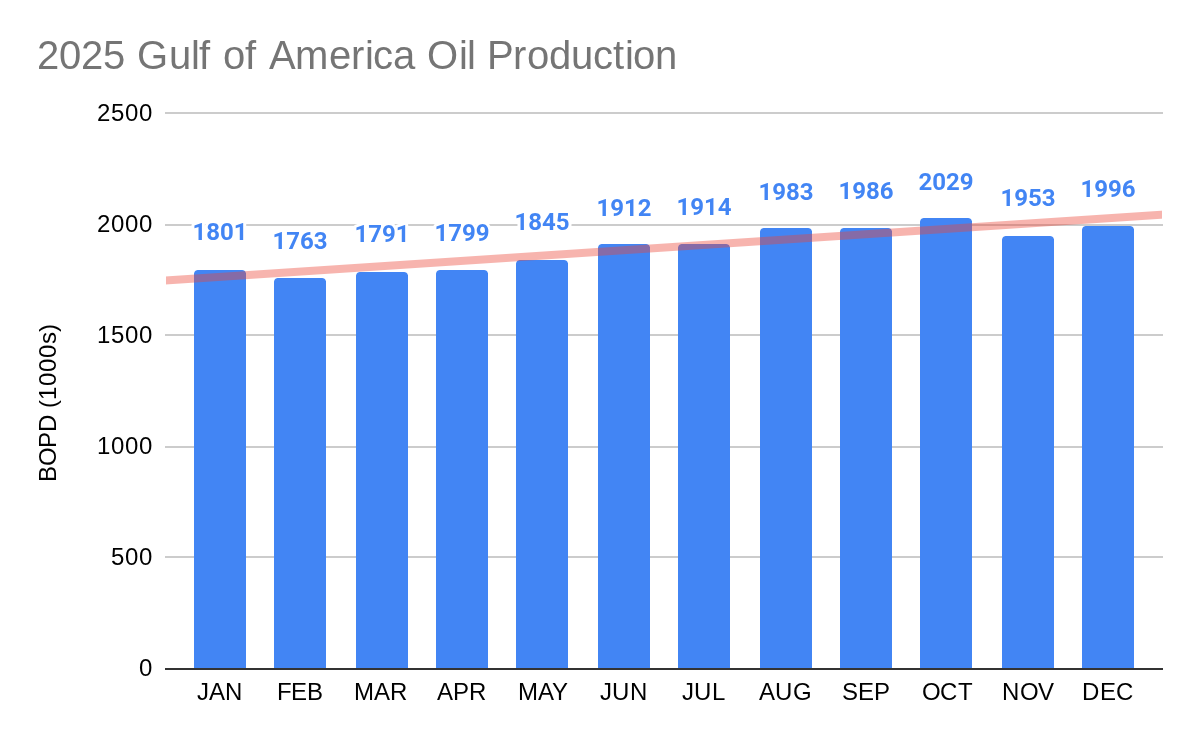

December 2025 Gulf oil production had to average 1.993 million bopd for 2025 to match the 2019 record. It exceeded that mark by 0.003 million bopd. However, October and November production were revised slightly downward resulting in a near dead heat annual average.

A closer look at the numbers (table below) shows that 2025 edged 2019 by a mere 250 bopd. Amazing!

Major caveat: The Nov and Dec 2025 figures will likely be revised slightly when EIA releases the next update at the end of January. Fingers crossed!😀

Per Baker Hughes, the latest (2/20/2026) Gulf of America rig count (2/20/2026) slipped to 9. The count was 10 the previous week and 12 a year ago. In 2023 and 2024, the BH rig count was a more healthy 15-20.

8 of the 9 rigs currently drilling are at high potential deepwater locations: 3 in the Mississippi Canyon Area, 3 in Green Canyon, 1 in Walker Ridge, and 1 in Alaminos Canyon. One rig was drilling on the shelf in the Eugene Island Area.

Per MMS data,the active Gulf rig count in 2001 was 148. The 2001 count was not a one year blip; the number of rigs active in the Gulf exceeded 100 for the ten year period from 1994-2003.

Although drilling and production have become more efficient with improved exploration technology, modern well completion practices, high pressure/temperature equipment, and enhanced recovery programs, drilling activity must still be sufficient to replace reserves and sustain production over the longer term.

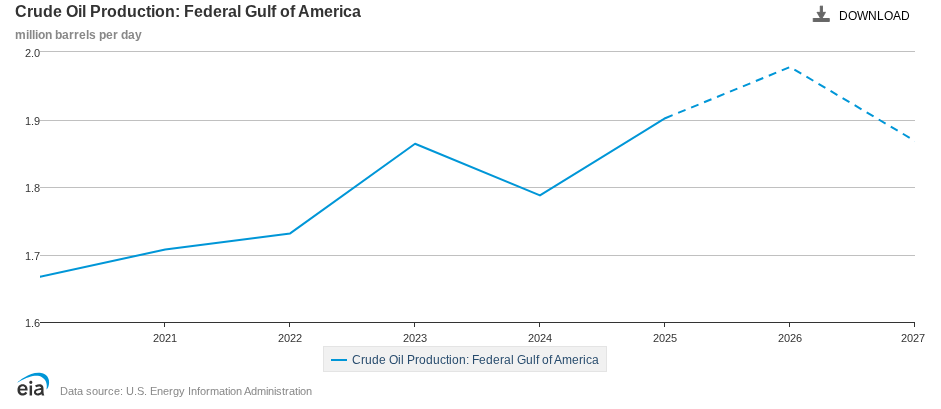

2025 may have been a record production year for the Gulf; we’ll find out at the end of this week. However, that level of production is not sustainable without increased drilling activity.

The EIA (chart below) is forecasting another banner year for Gulf oil production in 2026. However, they are pointing to a decline in 2027, when new production is not anticipated to be sufficient to offset natural declines. The decline in production is likely to continue beyond 2027 absent increased drilling.

BH rig count criteria: To be counted as active a rig must be on location and be drilling or ‘turning to the right’ for 4 out of 7 days during a week. A rig is considered active from the moment the well is ‘spudded’ until it reaches target depth or “TD”. Rigs that are in transit, rigging up, or being used in non-drilling activities such as workovers, completions, or production testing, are NOT counted as active.

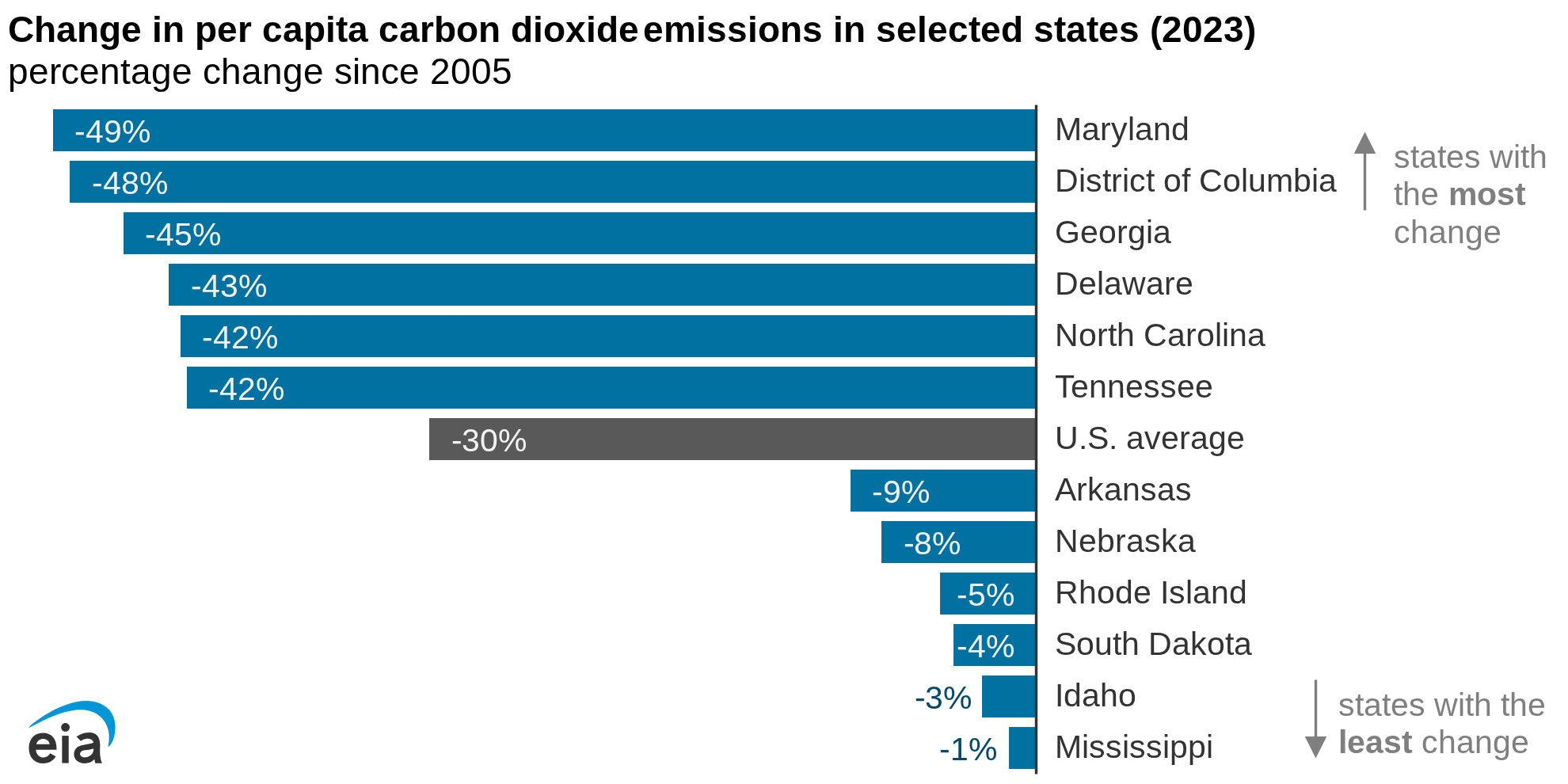

EIA:Per capita CO2 emissions from primary energy consumption decreased in every state from 2005 to 2023, according to recently released data in our State Energy Data System. Total energy-related CO2 emissions in the United States fell 20% over that time, and the population grew by 14%, leading to a 30% decrease in per capita CO2 emissions.

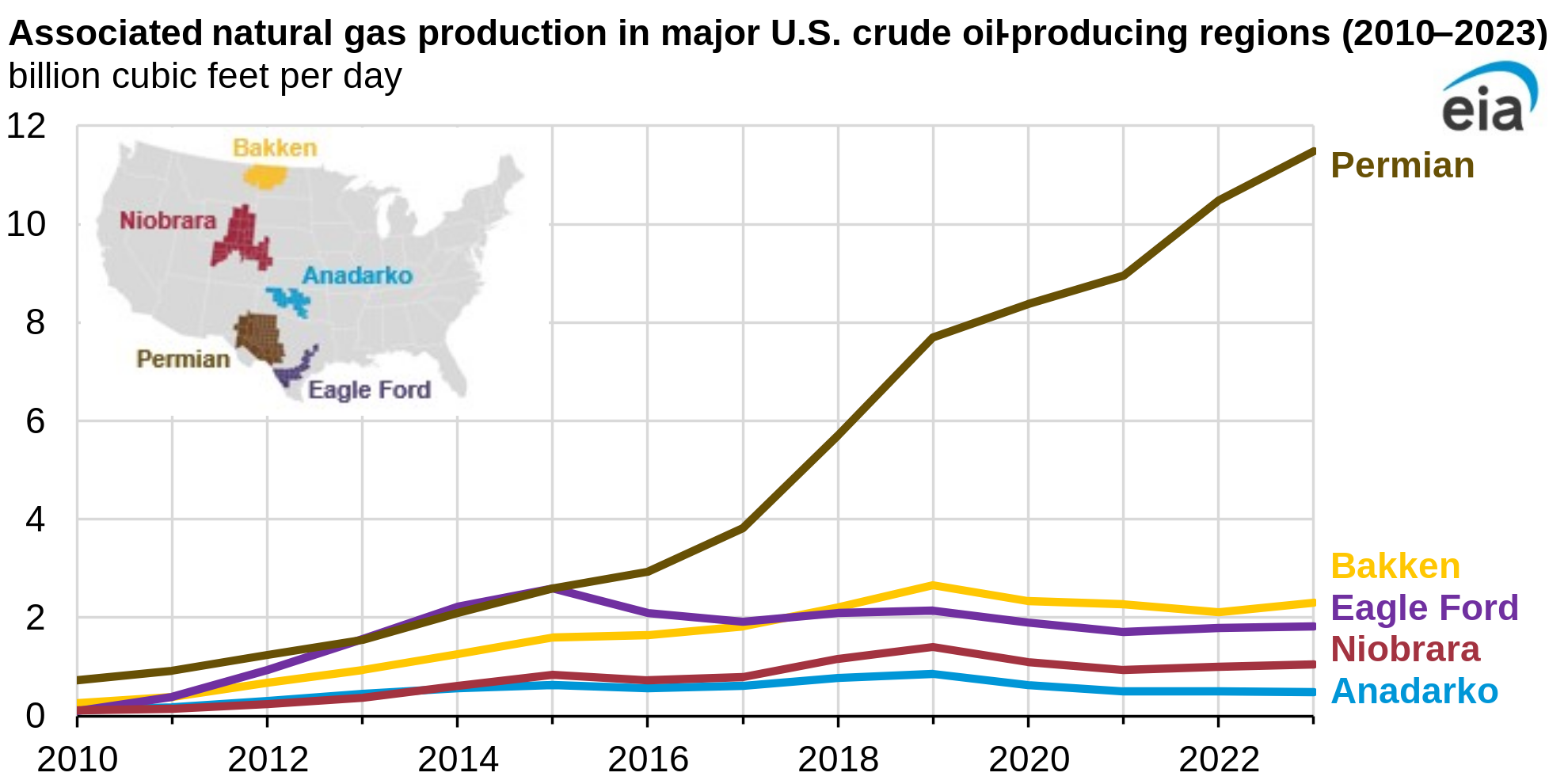

The EIA reports an 8% increase in 2023 US associated gas production as crude oil production rose to record levels. The Permian Basin, the dominant US crude oil producer, is unsurprisingly the leading associated gas producer.

EIA’s analysis inexplicably ignores the Gulf of Mexico OCS. The Gulf produced an average of 1.64 bcf/d of casinghead (associated) gas in 2023, ranking the GoM just behind the Eagle Ford and significantly above the Niobrara and Anadarko regions (see chart above). It’s also noteworthy that most production from the regions on the EIA chart is from private land, and is not constrained by 5 year leasing plans and other restrictive Federal policies.

80% of GoM gas production is from deepwater leases. The % of associated gas produced on deepwater leases is even higher. The 2 leading GoM gas producers, Shell and bp, only operate deepwater leases. The % of their 2023 gas production that was associated gas was 93% for Shell and 100% for bp.

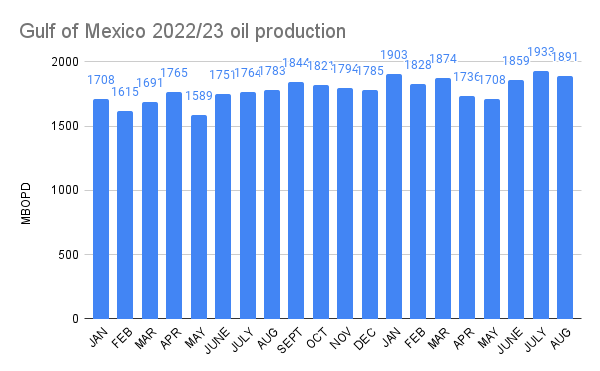

Gulf of Mexico 2023 oil production has dipped over the past 2 months, and is down 10% since January.

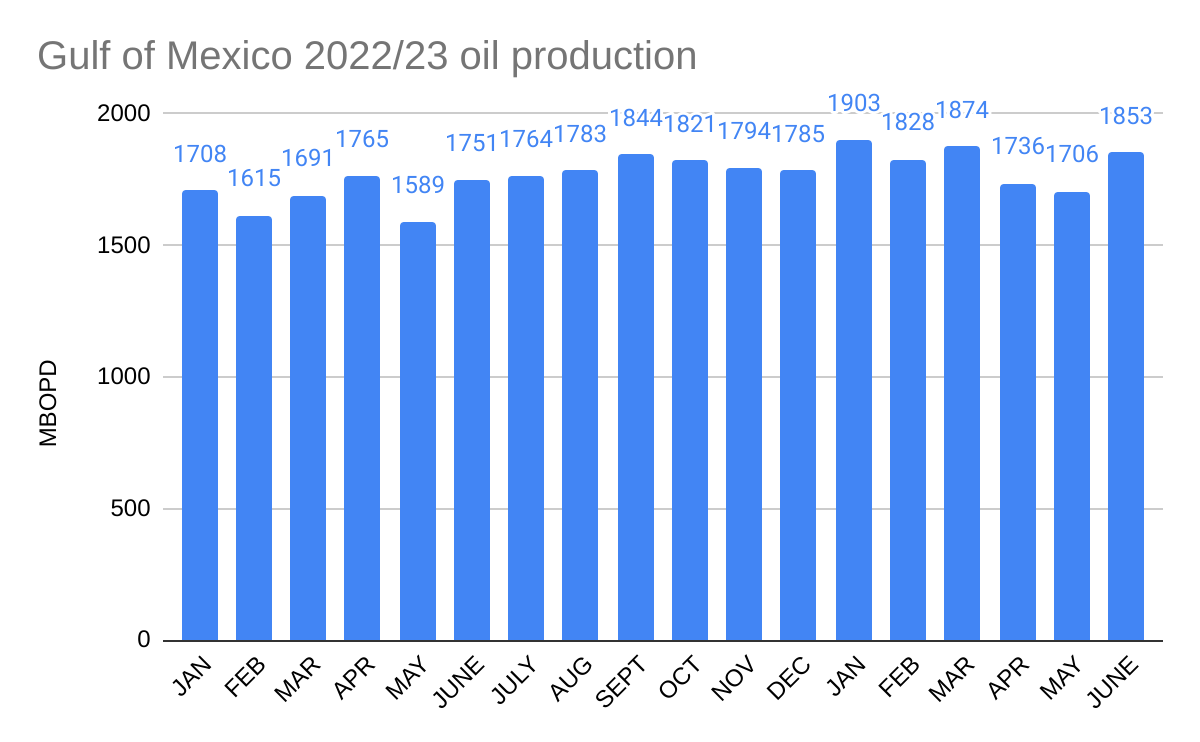

2023 production is reasonably well aligned with the EIA forecast which shows new production being offset by declines in existing fields.

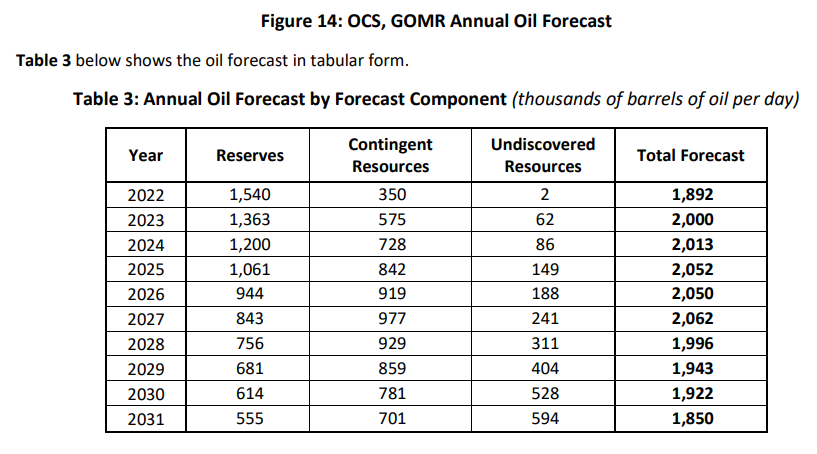

Last year, BOEM forecast that production would average 2.0 million bopd in 2023. That forecast was justification for curtailing BOEM’s Proposed 5 Year Leasing Program. For the first time in the history of the OCS program, the primary concern of the program managers was that production might be too high for too long! This stunning quote from the 5 year leasing plan explains why so few lease sales were proposed:

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

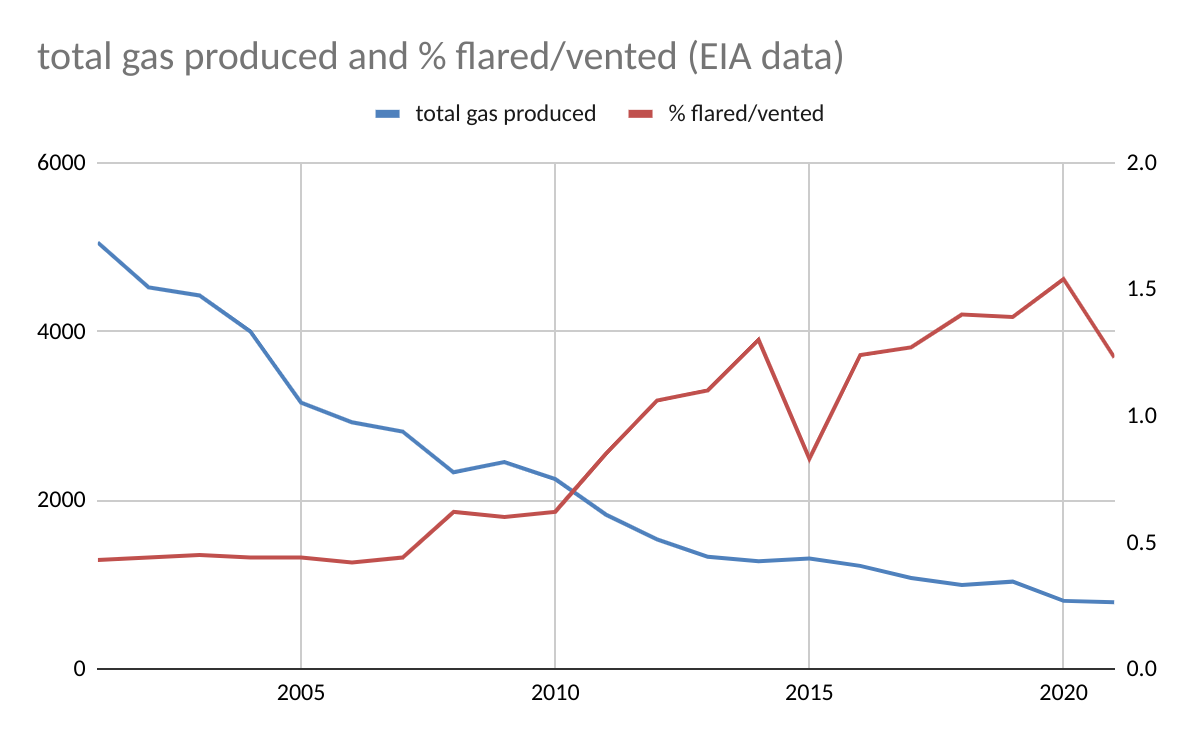

According to EIA data for 2001-2021, Gulf of Mexico flaring and venting volumes peaked in 2001 at 21.6 bcf, 2.25 times the volume flared or vented in 2022 (ONRR data for 2022). However, gas production in 2001 was 5.05 tcf, 6.4 times higher than in 2022. The % of the produced gas that was flared or vented in 2001 was thus 0.4%, less than 1/3 the 2022 rate of 1.22%.

Points to consider:

In 2001, gas production was mostly from gas wells, which have lower flaring/venting rates. As gas production declined because of lower gas-well gas (GWG) production, flaring/venting rates increased (see the chart below). This would account for some of the difference in flaring/venting rates (2001 vs. 2022). However, in recent years, the % of gas-well gas flared or vented has been between 0.3 and 0.5% which is comparable to the rate for all gas production (0.4%) in 2001. So the reduction in GWG production is not the entire reason for the higher flaring/venting rates in recent years. Hence the need for more transparency on flaring/venting performance.

Oil-well gas (OWG) production alone in 2001 (923 bcf) was higher than total gas production (784 bcf) in 2022. If the oil-well gas (OWG) flaring/venting rate was the same as the recent rate for OWG (1.2-1.5%), the volume of gas flared or vented from OWG alone (only 18% of total gas production in 2001) would have accounted for 11.1 – 13.8 bcf or 51-64% of the total volume flared/vented in 2001.

Yesterday, Lars Herbst attended the EIA’s Annual Energy Outlook presentation. The slides are attached.

Below is a custom chart from the EIA data tables. While EIA predicts growth in renewable generating capacity, US oil and gas production are nonetheless projected to increase slightly through 2050.

The EIA 2022 figure is spot-on, as it should be given that 10 months of 2022 production data are now in hand. However, BOEM’s 2022 forecast (published in July) missed the mark considerably. (In fairness to BOEM staff, their work was probably completed months before publication pending internal reviews.)

Of greater concern, given the policy implications, is the rosy BOEM forecast for the out-years. Despite historically low levels of leasing and exploratory drilling, BOEM forecasts oil production to exceed 2 million BOPD through 2027 and to remain well above the current (2022) level through 2031 (second table below).