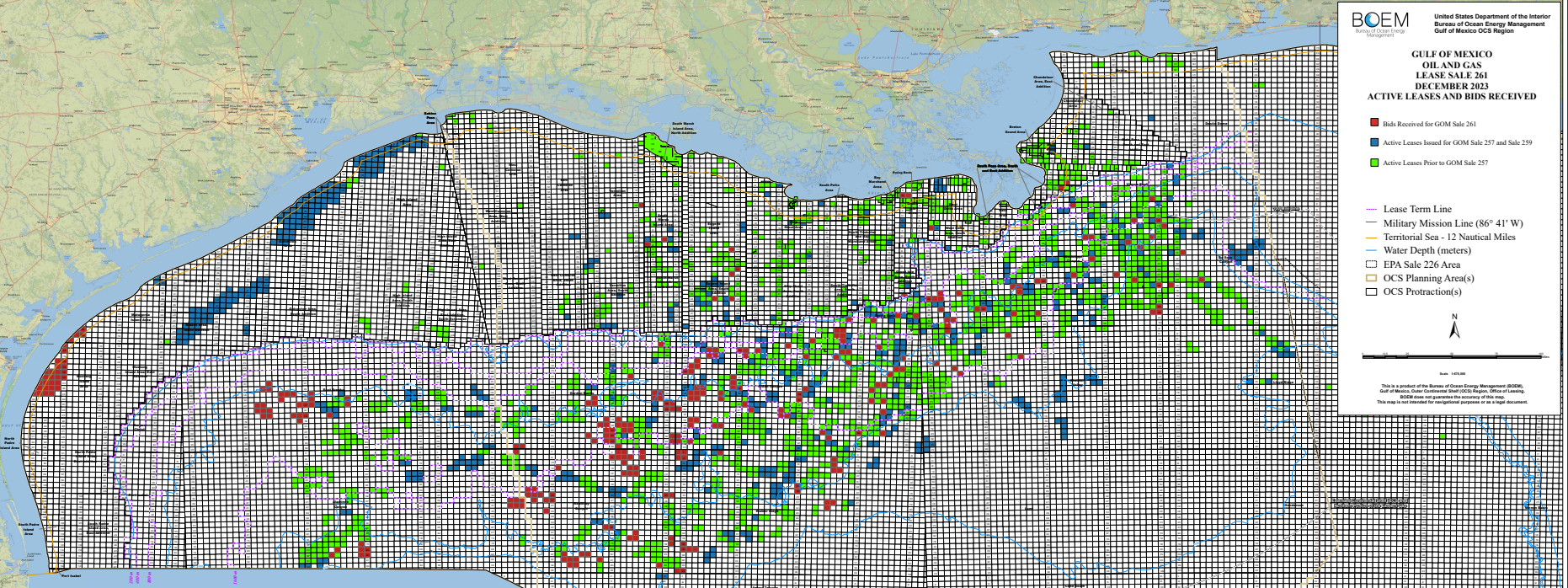

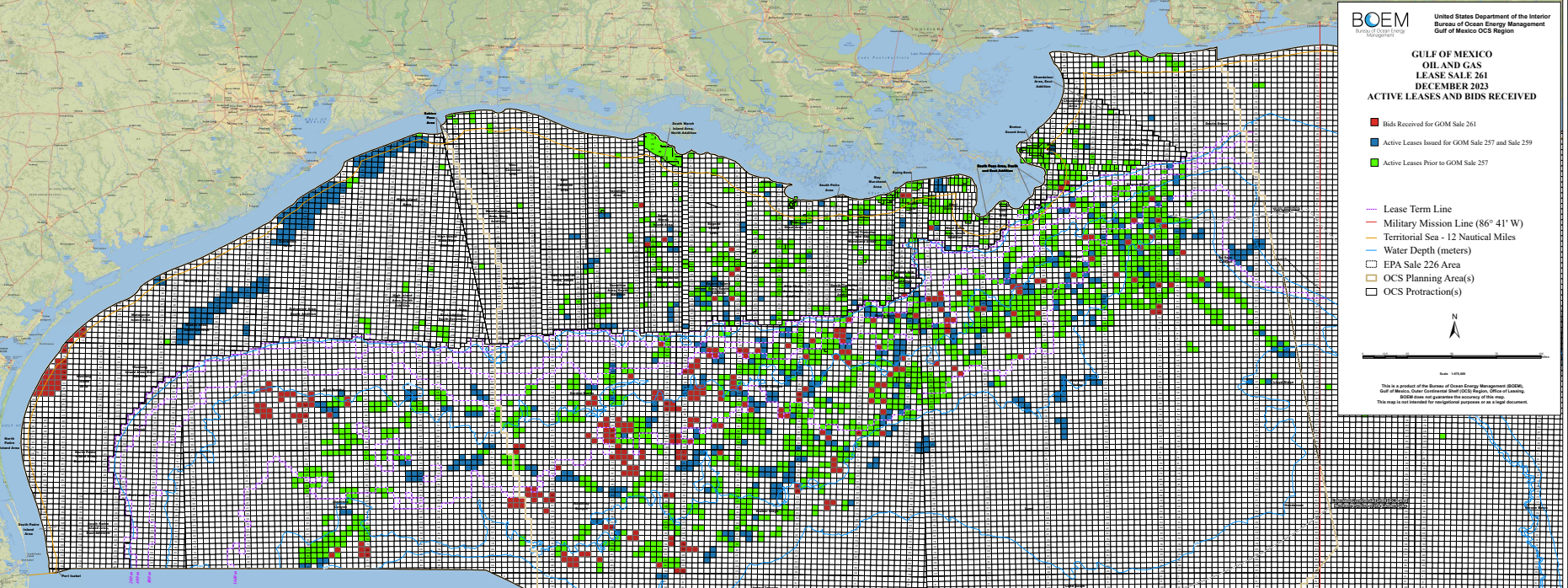

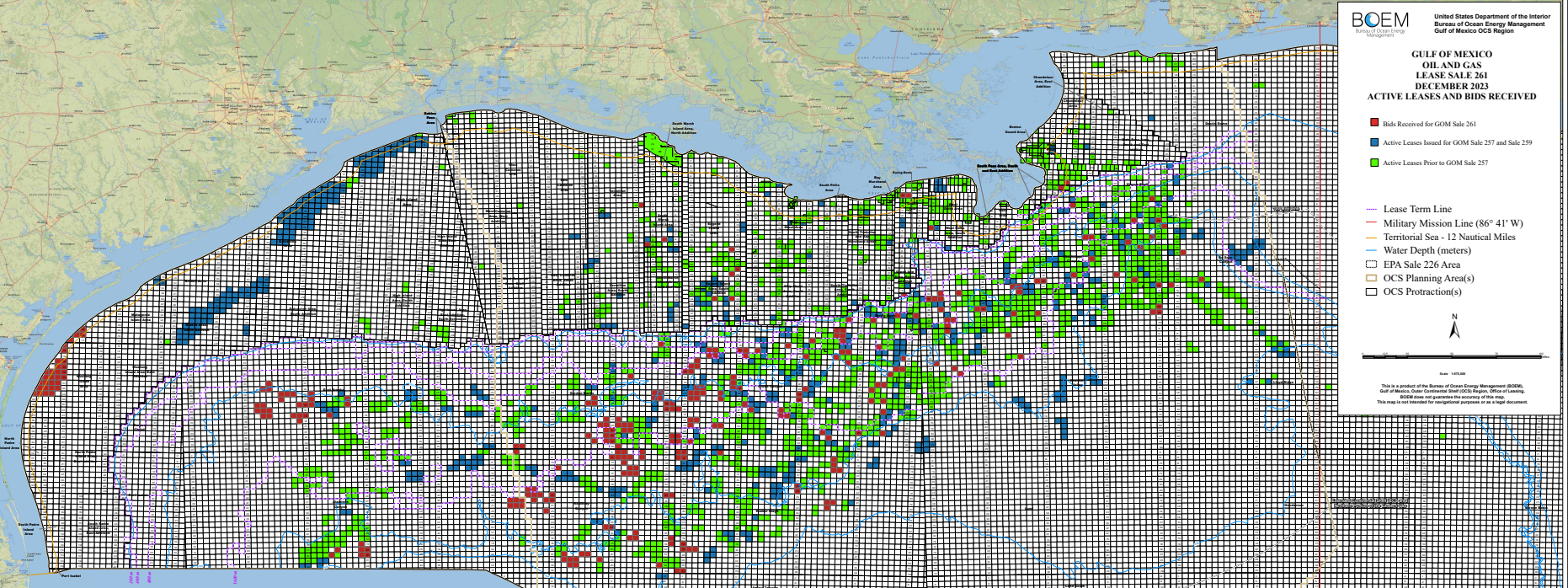

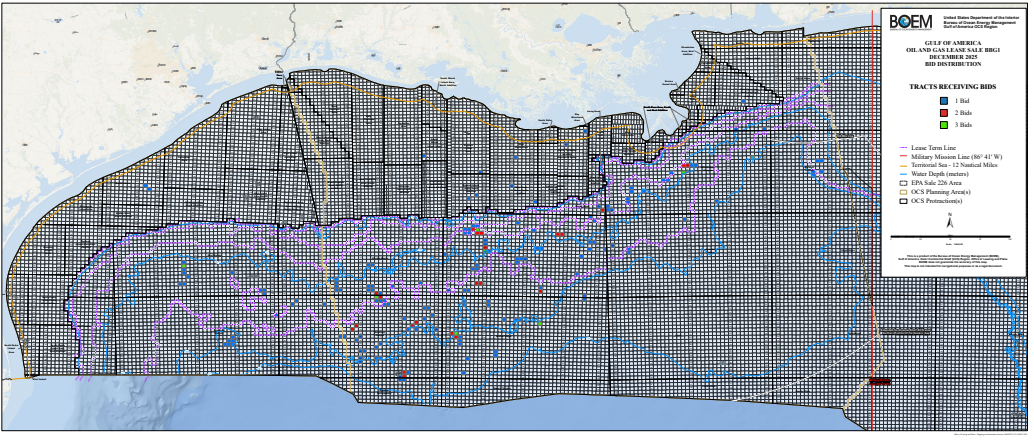

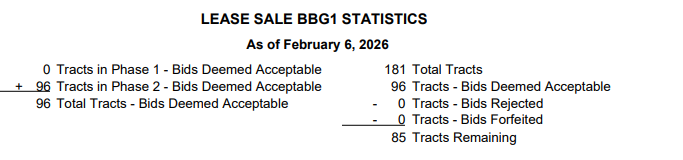

To date,BOEM has deemed 96 of the 181 BBG1 high bids to be acceptable. No high bids have been rejected. Although the sale was “beautiful but not big,” the bids were relatively strong on a per acre basis. The number of rejected bids may thus be quite low.

No bids were accepted during BBG1’s Phase 1 review. This means that none of the tracts receiving bids were determined to be nonviable as was the case for the 199 tracts that were improperly acquired for carbon disposal purposes in Sales 257, 259, and 261. (Unsurprisingly, neither of the acquiring companies has submitted an exploration plan for any of these CCS leases. The leases will likely expire without activity. Much to the dismay of the large and diverse group of opponents, the carbon disposal industry is focusing on onshore locations along the Gulf Coast.)

Meanwhile, a Cook Inlet lease sale is scheduled for March 4, and another Gulf of America sale will be held on March 11. Despite attractive terms, don’t expect either to be a banner “red jacket” lease sale. (See the John Rankin recognition below.)