Farther in the past, there were noteworthy failures (below) like Mobil’s acquisition of Montgomery Ward, Exxon’s investment in Reliance Electric, and Gulf’s real estate ventures.

Mobil – Montgomery WardExxon – Reliance ElectricGulf Land – Reston

Finally, don’t expect the carbon sequestration boom that some are forecasting. As wind investors have discovered, industries dependent on mandates and subsidies are risky.

Not much unites climate activists and skeptics, but they are largely aligned in their opposition to carbon sequestration (euphemism for disposal), as are fiscal conservatives. The word chutzpah comes to mind when companies seek public funds to dispose of emissions associated with the combustion of their products.

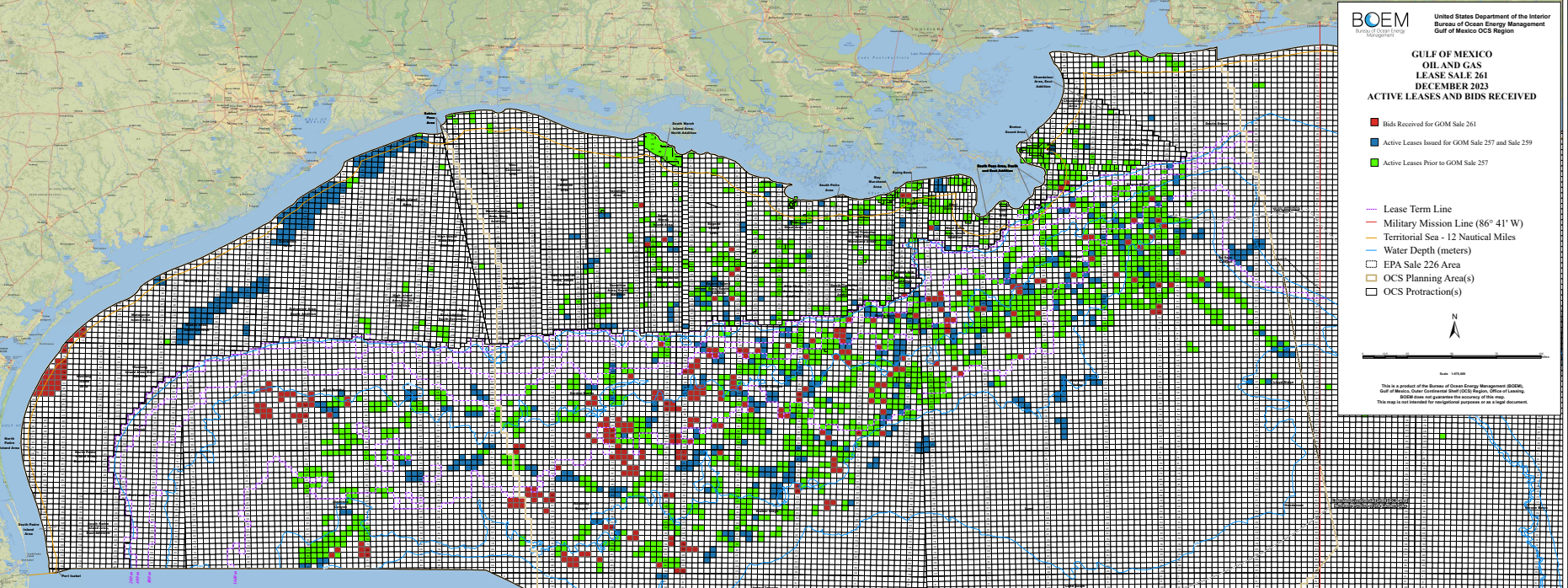

199 oil and gas leases were wrongfully acquired at Sales 257, 259, and 261 with the intent of developing these leases for carbon disposal purposes. Repsol was the sole bidder at Sale 261 for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

BP has announced it will cut its renewable energy investments and instead focus on increasing oil and gas production.

The energy giant revealed the shift in strategy on Wednesday following pressure from some investors unhappy its profits and share price have been lower than its rivals.

BP said it would increase its investments in oil and gas by about 20% to $10bn (£7.9bn) a year, while decreasing previously planned funding for renewables by more than $5bn (£3.9bn).

The future looks like this: BP Argos floating production unit, Gulf of America – simpler, safer, greener

It’s more than okay to be an oil and gas producer – no need to apologize or pretend to be something else. Oil and gas are, and will continue to be, essential to economies worldwide. Companies should focus on safely and cleanly achieving production objectives.

If a company thinks other types of energy investments make good business sense, they should engage in those activities. However, they should not do so to curry favor with anti-oil factions who can never be placated. Attempts to do so will only weaken your company.

BP is doing well in the Gulf of America – no. 2 producer in 2024.

Platform Holly, California State waters in the Santa Barbara Channel, formerly operated by Venoco

Platform Holly sits immediately offshore from the Univ. of California at Santa Barbara, and UCSB scientists have studied the platform and surrounding ecology extensively. Multiple studies have shown that production from Holly reduced natural seepage and methane pollution from shallow formations beneath the Channel. Platform Holly was thus a “net negative” hydrocarbon polluter.

The natural seepage in the Santa Barbara Channel was important to the earliest inhabitants of the area. The Chumash used the tar for binding and sealing purposes, including caulking their canoes. Since Holly shut down in 2015 following the Refugio pipeline spill, offshore workers and supply boat crews have reported a considerable increase in gas seepage.

Earlier this month, it was reported that well plugging operations at Holly had now been completed, but decisions regarding the final decommissioning of the platform remain.

Venoco declared bankruptcy in 2015 and the State of California became the platform owner. According to the State Lands Commission, Exxon will pay the costs for decommissioning the platform. This is because Exxon acquisition Mobil operated the platform from 1993-1997 before Venoco became owner.

The most recent Holly development is that Venoco has settled its law suit with Plains, the company responsible for the 2015 Refugio pipeline spill that halted production from Holly. Terms of the settlement have not been disclosed.

Note: As an aside, I’m curious as to whether Mobil provided a decommissioning guarantee as part of the sale to Venoco or whether the State is simply holding ExxonMobil accountable as a legacy owner. If it’s the latter, why isn’t bp (bp acquisition Arco was Holly’s operator from 1966-1993) also liable? Is it a matter of Mobil being the more recent predecessor owner?

Four of the five simpler, safer, greener deepwater platforms featured on this blog are now producing. The 5th platform (Whale) is on location and scheduled to begin production later this year.

platform

operator

first production

King’s Quay

Murphy

April 2022

Vito

Shell

Feb 2023

Argos

bp

April 2023

Anchor

Chevron

Aug 2024

Whale

Shell

late 2024

These platforms are in 4000 to 8600′ of water, are expected to reach peak production rates of 100-150,000 boe/day, and have favorable emissions characteristics on a per barrel basis.

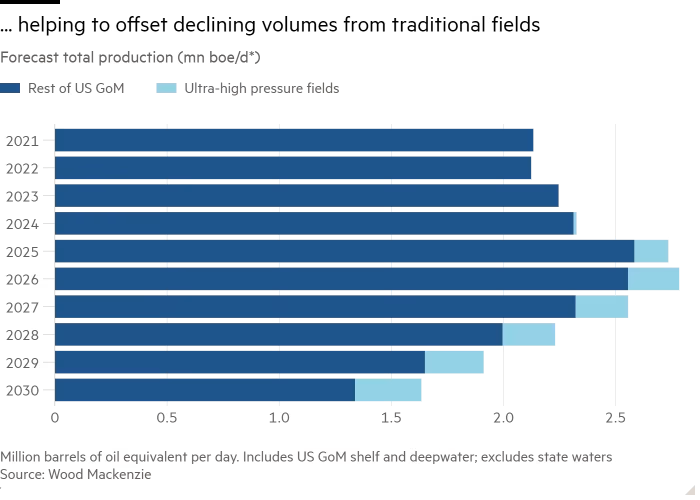

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded below.)

Chevron’s Anchor is the first deepwater, high-pressure development. Three similar deepwater hub platforms (table below) will begin production over the next 5 years. These host platforms will also facilitate additional production from nearby fields. Each will have production capacities of approximately 100,000 boe/day. Note the long lead times in achieving first production given the technological issues that had to be evaluated and addressed.

platform

operator

discovery date

first production

Kaskida

bp

2006

2029

Sparta

Shell

2012

2028

Shenandoah

Beacon

2009

2025

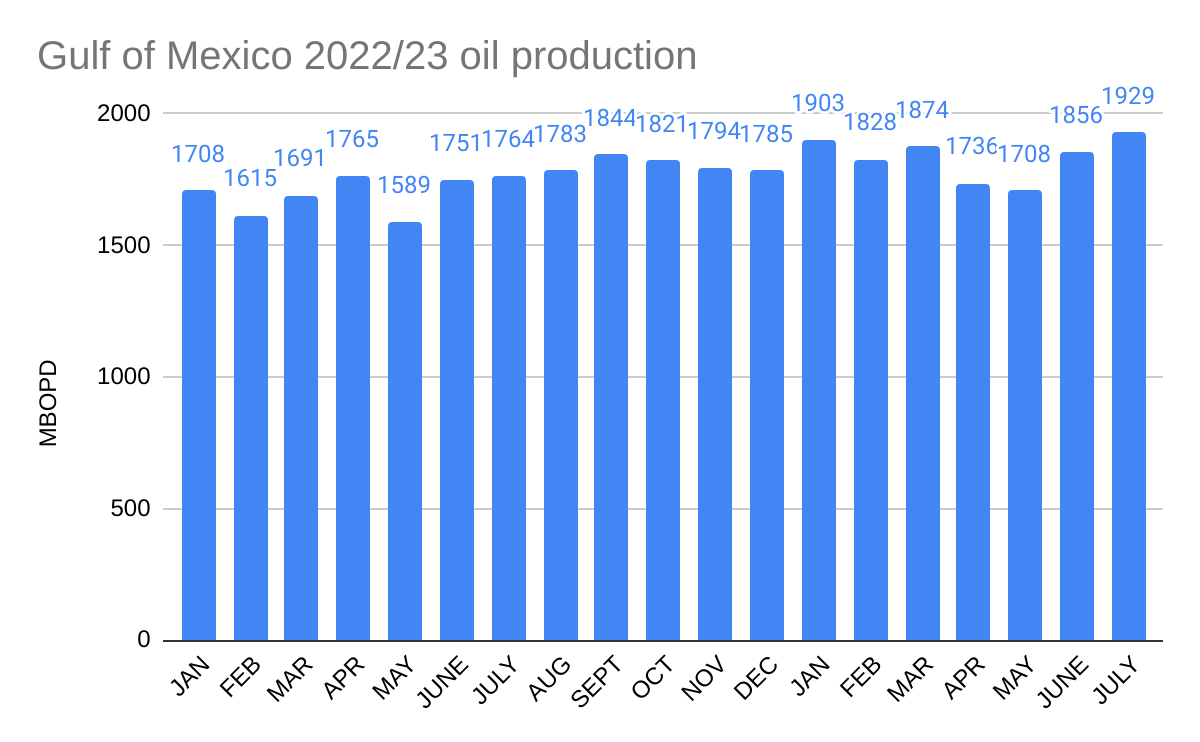

Wood Mackenzie sees these high pressure projects as the key to sustaining GoM production rates. Their projections for 2024 and 2025 seem optimistic based on 2024 YTD data, which adds to the importance of the projected new production.

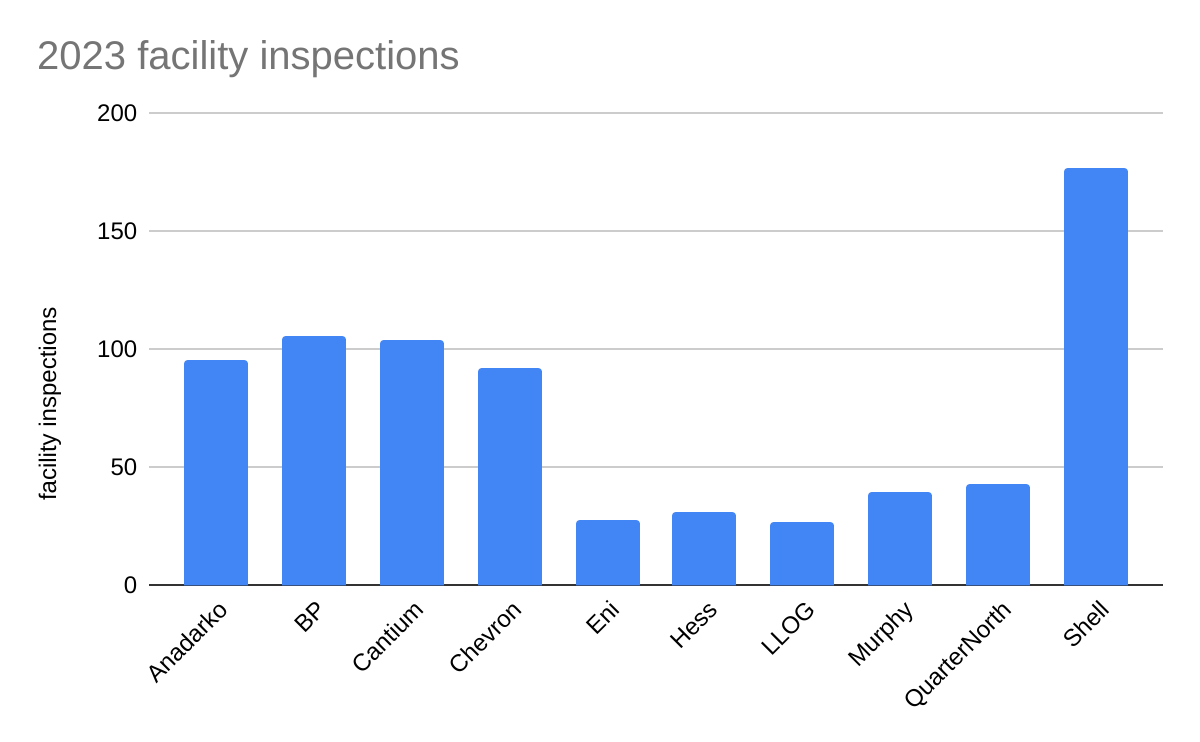

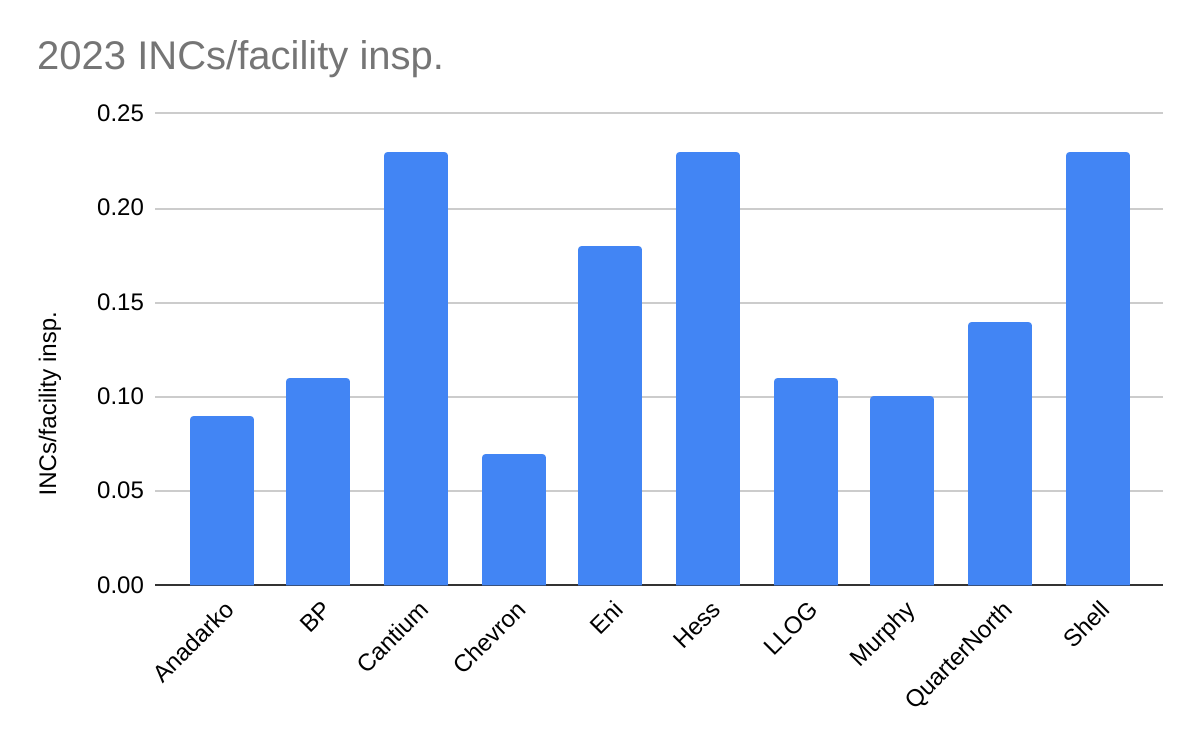

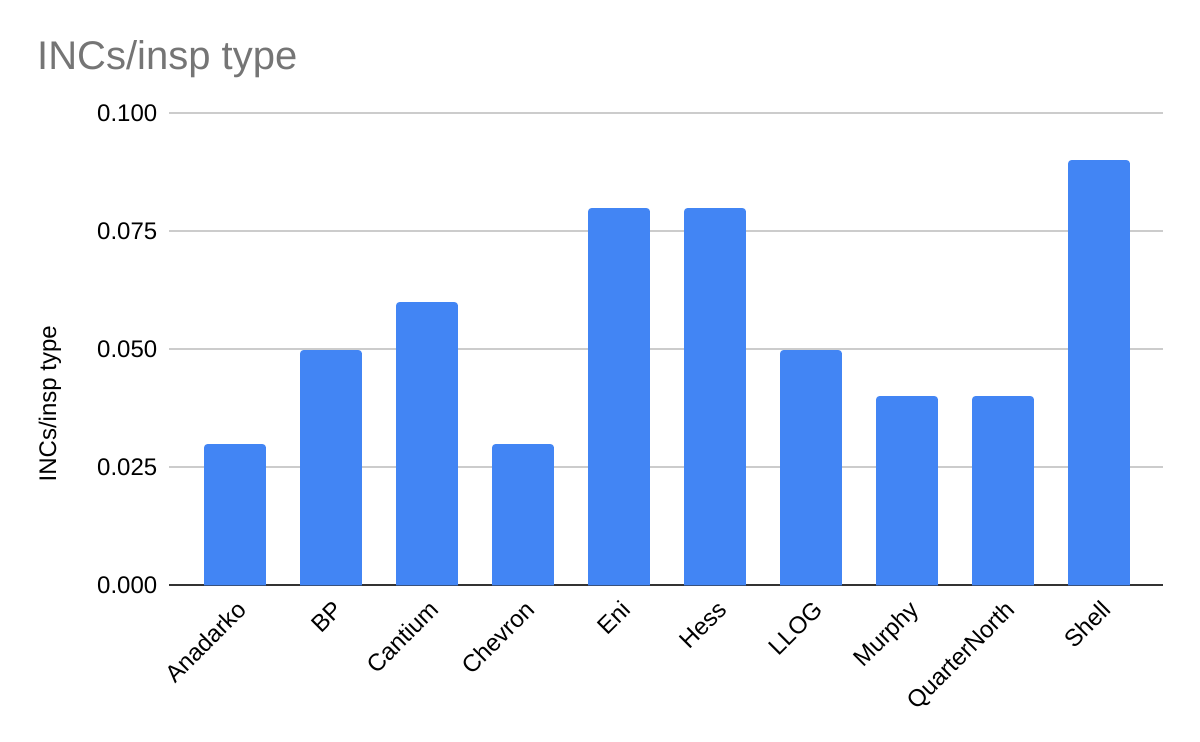

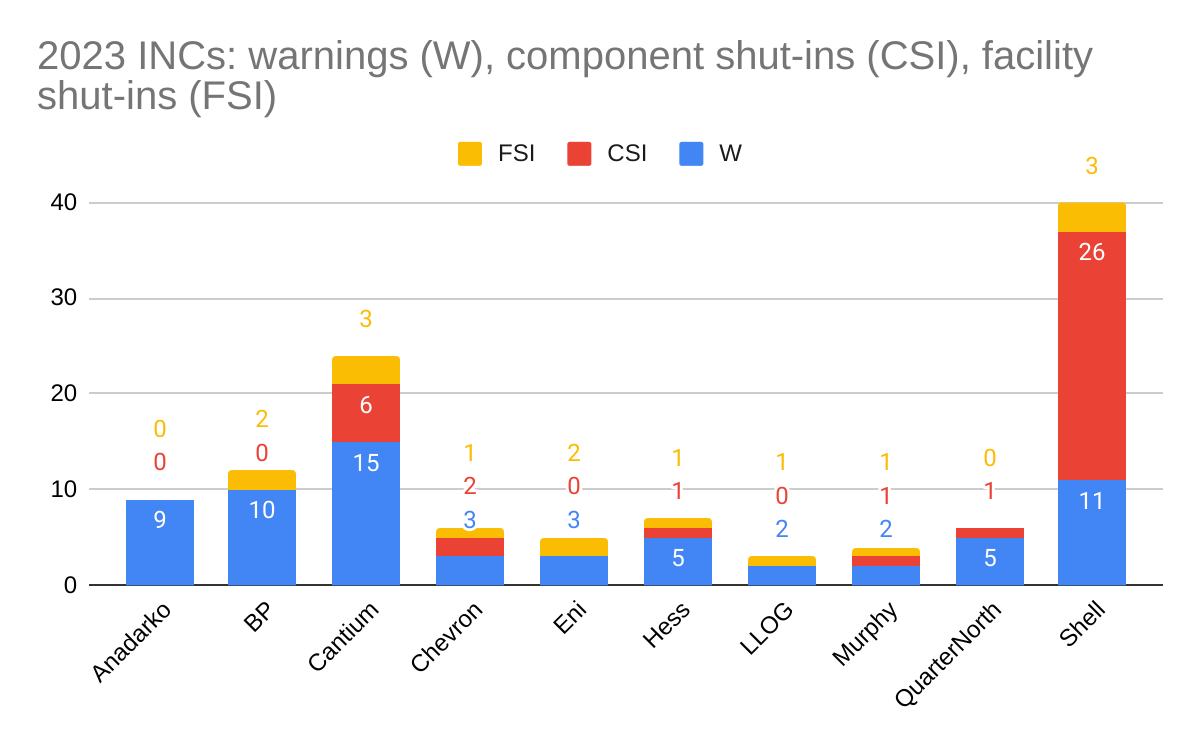

The Honor Roll companies for 2023 (listed alphabetically) are Anadarko, bp, Cantium, Chevron, Eni, Hess, LLOG, Murphy, QuarterNorth, and Shell.

BOE Honor Roll criteria:

Must average <0.3 incidents of noncompliance (INCs) per facility-inspection.

Must average <0.1 INCs per inspection-type. (Note that each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). On average, each facility-inspection included 3.3 types of inspections in 2023. Here is a list of the types of inspections that may be performed.

Must operate at least 3 production platforms and have drilled at least one well (i.e. you need operational activity to demonstrate compliance and safety achievement).

May not have a disqualifying event (e.g. fatal or life-threatening incident, significant fire, major oil spill). Due to the extreme lag in updates to BSEE’s incident tables, district investigations and media reports are used to make this determination.

platforms

2023 well starts

2023 (10 mos.) oil prod. (million bbls)

2023 (10 mos.) gas prod. (bcf)

Anadarko

10

11

66

60

BP

7

11

105

65

Cantium

96

10

5

6

Chevron

8

10

67

39

Eni

3

1

6

13

Hess

3

3

18

36

LLOG

10

7

25

35

Murphy

7

4

42

57

QuarterNorth

9

1

13

23

Shell

20

20

141

140

Also noteworthy:

Zero shut-in violations for Anadarko in 2023

<1 INC for every 10 facility inspections for Anadarko, Chevron, and Murphy

<1 INC for every 20 inspections (all types) for Anadarko, bp, Chevron, LLOG, Murphy, and QuarterNorth

Biggest prize at the holiday party went to Anadarko: Mississippi Canyon 389 – 5 bids, $25.5 million high bid

Biggest holiday shopping spree: Shell’s 65 high bids accounted for 24% of the sale’s high bids (excluding CCS bids).

Big spender award: Hess – $88.3 million on only 20 high bids. Does Chevron approve? 😀

Aussie, Aussie, Aussie, Oi, Oi, Oi: Strong performance by Woodside. 18 high bids, $24.8 million

Heia Norge!: Equinor continues to shine in the GoM! 13 high bids, $20.6 million

Spirit of America award to Red Willow Offshore which is owned by the Southern Ute tribe. 22 high bids!

Deepwater independents for (energy) independence: Beacon, Murphy, LLOG, Kosmos, Talos, Houston Energy, Ridgewood, QuarterNorth, Alta Mar, CSL, CL&F, and Westlawn

Even pace wins the race: Another solid lease sale for bp – 24 high bids.

So happy together 😀: Chevron and Hess combined for 48 high bids, $114 million

Coal in their stockings? Repsol (Sale 261) and Exxon (Sales 257 and 259) made up their own rules for acquiring carbon dumping leases. Perhaps some solid carbon in their Christmas stockings would be appropriate.

Christmas in July?: A lease sale in 2024 is needed. Sometime near the 4th of July holiday would be good. It’s up to you Congress!

Holiday greetings to our friends around the world!

Pictured: Transocean’s Deepwater Proteus. T/O should name one of their drillships Deepwater Diligence 😉

Seven of the deepwater exploratory wells drilled in the Gulf of Mexico in 2023 (YTD) were spudded within 4.5 years of the effective date of their leases. Three of these wells were spudded within 3 years of their lease effective dates (see table below).

These are impressive achievements when you consider the time required for consultation with partners (if any) and contractors, site surveys, exploration plan development and approval, well planning, and drilling permit preparation and approval.

The subject wells accounted for 28% of thedeepwater exploratory well starts in 2023 (25 net YTD wells after subtracting restarts at the same location).

date lease effective

spud date

elapsed time (months)

water depth (ft)

operator

3/1/2021

8/27/2023

30

6498

Shell

8/1/2020

5/21/2023

34

2211

Talos

8/1/2020

3/15/2023

31

3338

Talos

12/1/2019

6/5/2023

42

4228

Chevron

11/1/2019

6/1/2023

43

4603

Hess

7/1/2019

7/11/2023

48

7486

Kosmos

12/1/2018

6/6/2023

54

4127

bp

Below are the exploration plan (EP) and permit (APD) approval timeframes for these 7 wells. With the exception of the Kosmos EP which required a number of modifications, the regulator actions appear to have been timely. For the bp, Shell, and Chevron wells, only 4-6 months elapsed between EP submittal and APD approval.

operator

block

date EP received

date EP approved

APD received

APD approved

Shell

WR 365

3/1/2023

5/17/2023

5/11/2023

8/8/2023

Talos

GC 78

1/19/2021

4/16/2021

3/8/2023

5/26/2023

Talos

MC 162

4/1/2022

7/13/2022

8/2/2022

3/2/2023

Chevron

MC 937

12/7/2022

5/19/2023

4/21/2023

5/21/2023

Hess

MC 727

8/30/2022

11/3/2022

12/21/2022

4/24/2023

Kosmos

KC 964

1/3/2020

10/12/2022

4/18/2023

7/3/2023

bp

GC 436

1/18/2023

4/14/2023

3/29/2023

6/5/2023

Notes: EP=Exploration Plan, APD=Application for Permit to Drill, WR=Walker Ridge, GC=Green Canyon, MC=Mississippi Canyon, KC=Keathley Canyon

According to the New York State Energy Research and Development Authority, this would result in an average 54% price hike across their portfolio. The strike prices would rise from $118.38 to $159.64/MWh for Empire Wind 1, from $107.50 to $177.84/MWh for Empire Wind 2, and from $118.00 to $190.82/MWh for Beacon Wind.