This wonderful satellite image of Cape Cod, Nantucket, and Martha’s Vineyard was posted by a Facebook friend. Cape Cod is quite young, having been formed by a retreating glacier about 20,000 years ago.

I moved to Cape Cod 43 years ago in preparation for the exploratory drilling operations on Georges Bank. I met so many amazing and supportive people during my 4 years there including (most importantly) my wife, State and local officials, congressional representatives, Woods Hole scientists, fishermen, reporters, airport officials, industry representatives, Coast Guard officers, offshore workers, environmental activists, and concerned citizens. All contributed to an outstanding work experience for me and my colleagues.

The 8 exploratory were at locations 112 to 155 miles SE of Nantucket (map below).

I lived in Hyannis, not far from the Kennedy compound (pictured below) which was on my jogging route. It was an easy bike ride to our office at Barnstable Municipal Airport, where we departed to inspect the exploratory drilling operations.

RFK Jr. talks about the Kennedy compound and the “Camelot years” during JFK’s presidency.

The final NTSB report on the 12/29/2022 GoM helicopter crashthat killed 4.To the NTSB’s credit, their preliminary report was timely. Hopefully, the NTSB is considering the muddled regulatory regime for helidecks (regulatory fragmentation).

Report on the Nord Stream sabotage: As the anniversary nears, the prospects for an official report are fading.The absence of a report from Sweden, Denmark, or Germany speaks volumes.

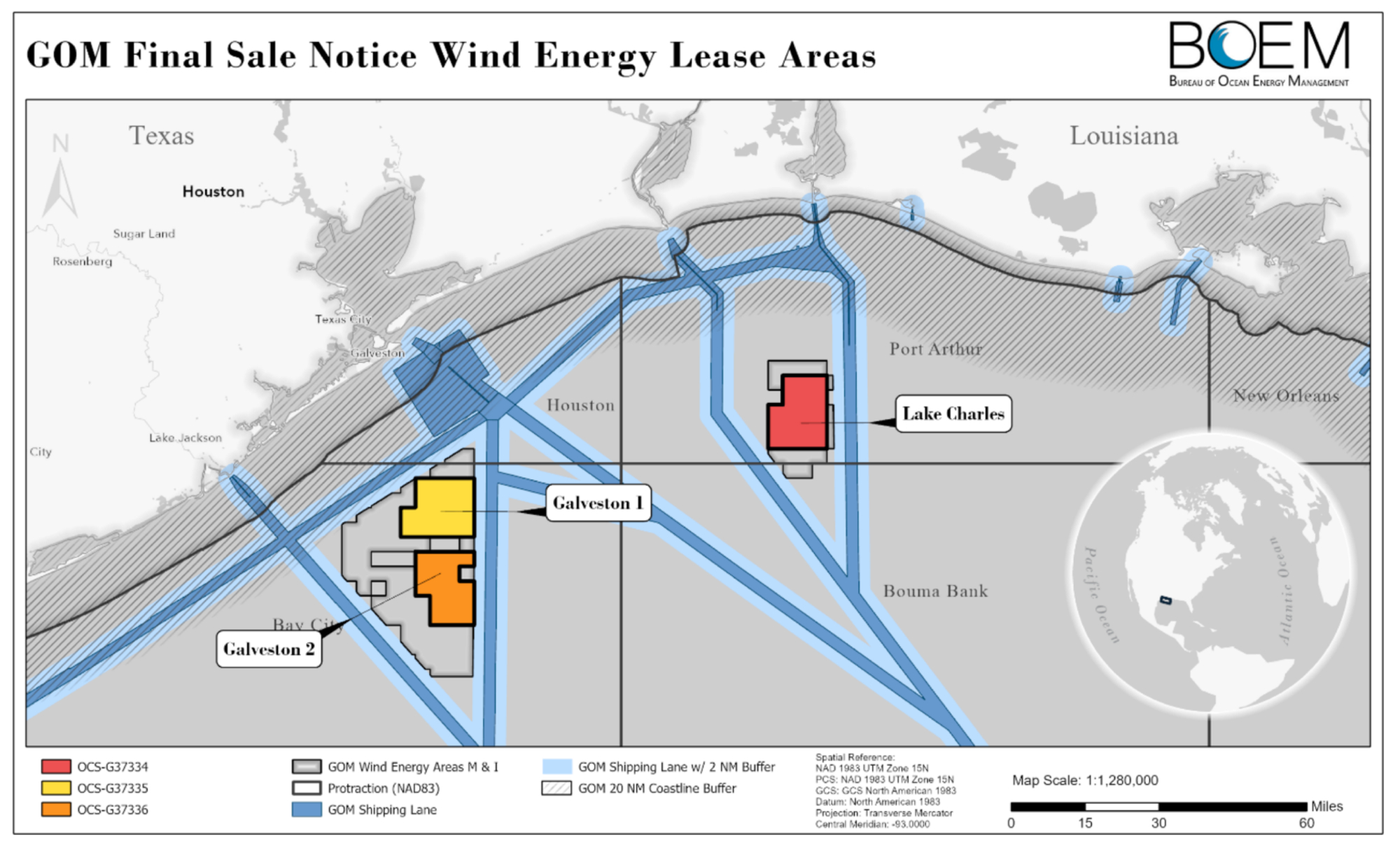

BOEM’s Final Sale Notice for the upcoming Gulf of Mexico wind auction identifies 3 lease areas (see map below). Wind operations in these areas should not significantly conflict with other GoM activities, including oil and gas operations.

Those who followed Exxon’s recent lease acquisitions may be amused by the map below from BOEM’s siting analysis document. The 94 Exxon leases acquired at Oil and Gas Lease Sale 257 (yellow blocks) are misidentified as “Carbon Capture Lease Blocks.” As has been discussed at length on this blog (most recently here), Sales 257 and 259 were oil and gas lease sales. Although Exxon’s intentions are now well known, they may not conduct carbon sequestration operations on these leases unless they are competitively reissued or converted. (Is BOEM’s siting document implying that conversion of the Exxon leases is a fait accompli?) The regulations for such conversions, and for CCS operational activities, have yet to be promulgated. A draft of these regulations is expected later this year, and the comments should be spirited and diverse.

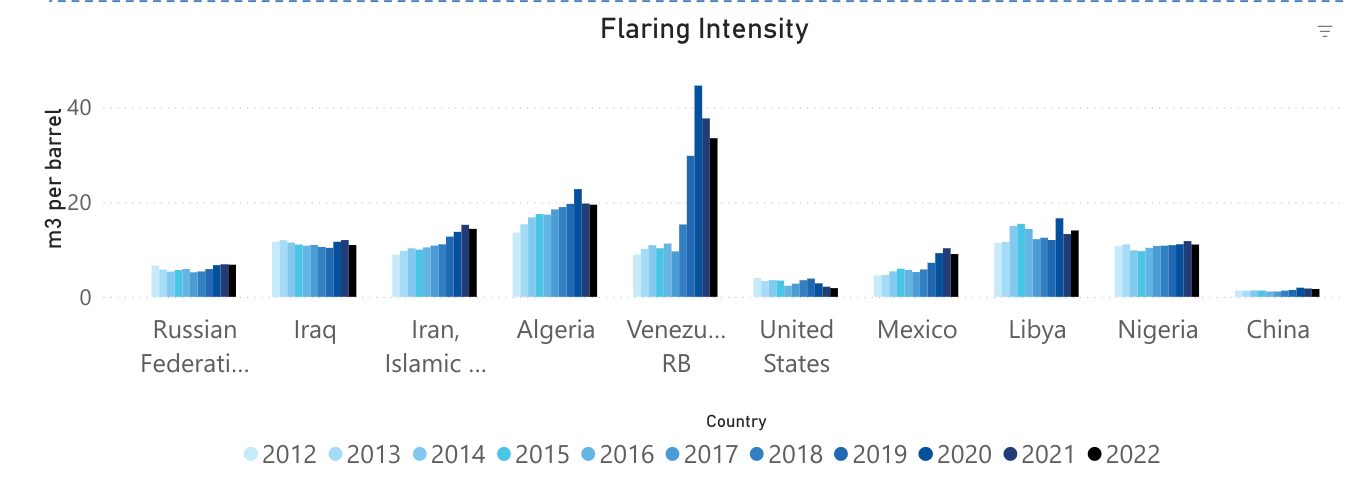

The latest World Bank data tell us that significant gas flaring issues persist. Worldwide, 138,549 million m3 of gas were flared in 2022. This equates to a massive 4 tcf, the equivalent of the reserves in a major gas field and more than 5 times the total gas production in the Gulf of Mexico in 2022.

The top ten “flarers” are listed below. Each of these fields flared from 19 to 42 bcf. For comparison, the top ten GoM gas producers in 2022 produced 10 to 57 bcf, so single fields are flaring more than GoM companies are producing in total. Assuming for discussion purposes a gas-oil ratio of 1000 cu ft/bbl, all of the gas associated with 19 million to 42 million barrels of oil production was wasted from each field.

Posted below are the World Bank’s flaring intensity data (m3 of gas flared per bbl of oil produced) for the 10 countries with the highest flaring volumes. Venezuela’s flaring intensity rose to 44.6 m3/bbl in 2020, before declining moderately the following 2 years. 44.6 m3/bbl equates to 1575 cu ft/bbl. This gas flaring to oil production ratio implies that a very high percentage of Venezuela’s associated gas production was flared.

Here in North America, we have flaring issues of our own. Mexico’s Cactus Field is a top ten flarer (first table above) with 534.5 million m3 flared in 2022. The World Bank also lists 6 Permian Basin fields with >50 million m3 of gas flared in 2022.

Zeroing in on the US/Canada offshore sectors, fields with >1 million m3 of gas flared (2022) are listed below. Four of the top 7 are offshore Alaska and Newfoundland where the gas cannot currently be marketed and reinjection, field use, and flaring are the only options. Can production from these fields be better managed to reduce flaring volumes?

“The farm-out campaign remains a key focus for United, as we seek to take this potentially transformational project forward into the next phase of the Licence. In order to do so, a commitment to drill a well will need to be made by end January 2024.

We have continued to engage with potential partners to participate alongside us in drilling this exploration well, and earlier in the year, a deadline for indicative offers had been set for the end of H1. We are encouraged by the number and quality of companies that are in the process of completing their evaluations, and as they have requested additional time, we have agreed to extend the deadline. Additional updates will be provided in due course.”

January 2024 is fast approaching. What constitutes a commitment to drill? How soon must a well be spudded?

Could Jamaica extend the deadline? Should they?

United Oil and Gas is “encouraged by the number and quality of companies that are in the process of completing their evaluations.” We’ll soon find out how serious that interest is.

For those following the Barbados Offshore Licensing Round, no updates have been posted by the Ministry of Energy and Business; nor has the BOE team received any feedback on our comprehensive bid 😉

Pioneering subsea engineer, Jean Louis Daeschler, is also an acclaimed artist. He recently shared two paintings that are very much on-topic for this blog. The paintings depict a wind turbine installation with support from a jackup vessel, and a drilling operation with jackup rig. The paintings give a sense of the commonality of these mutually supportive industries.

Keathley Canyon (KC) Block 96, the tract receiving the highest bid in the entire sale ($15,911,947 by Chevron), had a BOEM MROV of only $576,000. Clearly, Chevron and the government have a very different view of the value of this tract. BP was the second bidder for KC 96, and their bid ($4,003,103) was also considerably higher than BOEM’s MROV. This one will very interesting to follow.

The only bid that was rejected in Sale 257 was the BP/Talos bid of $1.8 million for Green Canyon Block 777. BOEM’s MROV in the Sale 257 evaluations was $4.4 million. BP again bid on GC 777 in Sale 259, but their bid was only $583,000 (even though BOEM’s Sale 257 evaluation was public information). BOEM’s MROV was reduced only slightly to $4.2 million, and they again rejected BP’s bid. We’ll see what happens in the next sale.

51 of the 230 accepted bids were >$1 million, all for deepwater tracts. All of the rejected bids were for deepwater tracts, and a higher percentage (4/14) were >$1 million. This makes sense given that the higher potential prospects are in deepwater.

These results demonstrate again that resource evaluation is far from an exact science. BOEM is not selling barrels of oil and cubic feet of gas. BOEM is evaluating prospects, and companies are bidding on the opportunity to explore these prospects.

Bidding strategies differ; the more companies participating, the better the long-term prospects for the OCS program.

ENERGYWIRE has reported that the Department of the Interior will publish the legislatively mandated carbon sequestration rule later this year. Given that even close followers of the OCS program were completely unaware of the enabling legislative provisions prior to their enactment, the proposed DOI rule will provide the first opportunity to formally comment.

Within the oil and gas industry and the environmental community, there are considerable differences of opinion about carbon sequestration in general, and more specifically, offshore sequestration. All interested parties are encouraged to submit comments on these important regulations.

Some background information on the sequestration legislation and subsequent actions:

amend the OCS Lands act to authorize “the injection of a carbon dioxide stream to sub-seabed geologic formations for the purpose of long-term carbon sequestration.”

exempt CO2 injection from the restrictions on ocean dumping by stipulating that such injection “shall not be considered to be material (as defined in section 3 of the Marine Protection, Research, and Sanctuaries Act of 1972.” Without this exemption, CO2 streams would clearly be “material,” as defined in 33 U.S.C. 1402, and would be subject to the stringent requirements of that act.

direct that “not later than 1 year after the date of enactment of this Act, the Secretary of the Interior shall promulgate regulations to carry out the amendments made by this section.” (This deadline has been missed, which is rather common for such directives.)

3/29/23: Exxon bid at Sale 259 on 69 nearshore tracts with little oil and gas potential. Once again, this was strictly an oil and gas lease sale and Exxon’s CCS intentions were clear. Nonetheless, the leases were awarded.

Exxon and other companies intend to commercialize carbon sequestration, and Exxon projects an astounding $4 trillion CCS market by 2050. Such a market will of course be dependent on mandates and subsidies, and the costs will ultimately be borne by taxpayers and consumers.

Is it not a bit unsavory and hypocritical for hydrocarbon producers to capitalize on the capture and disposal of emissions associated with the consumption of their products? Perhaps companies that believe oil and gas production is harmful to society should exit the industry, rather than engage in enterprises that sustain it.

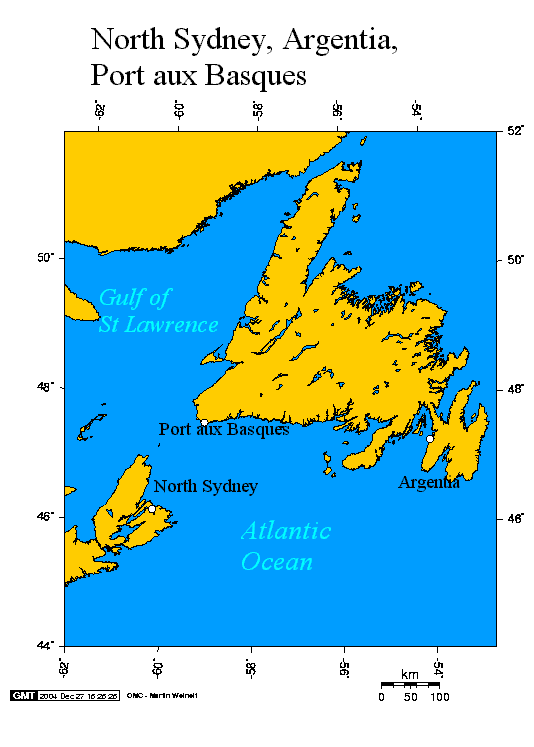

The Jones Act, protectionism at its finest, was enacted 113 years ago, and stipulates that vessels which transport merchandise or people between two US points must be US built, flagged, owned, and crewed. Congress tightened the screws further by ordaining that offshore energy facilities, including wind farms, are US points. That precludes the transportation of wind turbine components from US ports to offshore wind farms.

The Jones Act has thus provided an opportunity for the Port of Argentia, a former US Navy base in southeast Newfoundland, and the port is set to become a key node in the offshore wind supply chain. Monopiles constructed in Europe will be stored in Argentia, until they are delivered to US wind farms in the North Atlantic. Kudos to the folks at the Port of Argentia for taking advantage of this opportunity.

Dutch company Boskalis will be transporting the monopiles, which are expected to land in the Port of Argentia in a few weeks. (Boskalis)

Of course, the 3 Stabroek Block partners who are responsible for this production – Exxon (45%), Hess (30%), and CNOOC (25%) – are also doing quite well. If you are wondering about this curious mix of companies – a US supermajor, a large US independent, and a state-owned Chinese mega-company – this OilNow post explains what happened.

Initially, Exxon and Shell were 50/50 partners in the Stabroek Block. Shell thought the chances for success were slim and opted out a year before the world class Liza discovery (ouch!). After Shell departed, Exxon sent “at least 35 letters” to prospective partners and only Hess and CNOOC responded favorably (actually, it was Nexen, not CNOOC that responded). The Liza discovery followed and the rest is history.

Will exploration offshore Jamaica and Barbados also prove successful? Stay tuned.